Financial markets have some tendency to over-react to news and the increased globalization of financial markets means that things can now get out of hand a lot more quickly on a global scale. Minor shifts in the Fed policy outlook have had a large impact on exchange rates. The strengthening of the dollar has had an outsized impact on commodity prices. However, shifts in the financial markets can themselves have important effects on economic conditions. It’s enough to make your head spin.

As with most countries, the responsibility for the dollar falls to the Treasury, not the central bank. The Fed can influence exchange rates, to be sure, and react to the impact of exchange rate movements on the economy, but the exchange rate of the dollar is not its job. Talk of “currency wars” is way overdone. Central bank policy is driven by the outlook for the domestic economy. The strength in the dollar over the last two years has been due to a number of factors, but many would put tighter Fed policy at the top of the list (along with easier monetary policy abroad). Yet, the Fed has raised rates by only 25 basis points – and the expected path of rate increases is very gradual.

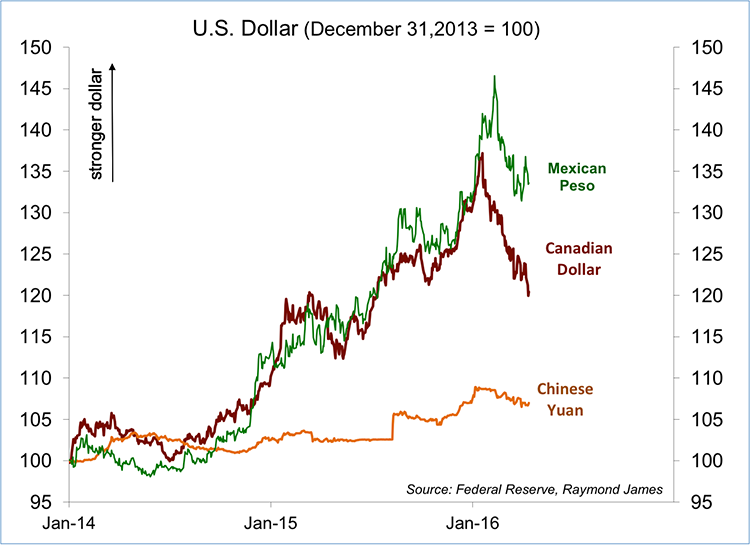

The dollar’s strengthening against the currencies of our major trading partners was especially pronounced. From the end of 2013, the U.S. dollar had appreciated 35% against the Canadian dollar and 45% against the Mexican peso. These are large moves and cannot be justified by monetary policy differentials.

In general, policymakers do not worry too much about the level of exchange rates. It’s the speed of adjustment that is worrisome. Rapid moves are destabilizing. The Treasury can intervene by buying or selling currency reserves, or use open-mouth operations to try to talk the exchange rate in one direction or the other – but when push comes to shove, intervention can be only a temporary fix. Currency flows are simply too large for the authority to do much about it.

Canada and Mexico account for more than a third of U.S. exports. Anecdotal reports from businesses exporting to these two countries were increasingly sour in the first couple of months of the year (and exporters to the rest of the world weren’t exactly cheery either). It’s well known that currency movements tend to overshoot. The currency market did begin to turn in early February, coinciding with economic data and market conditions that suggested a softer Fed rate outlook. Still, while the dollar’s softening has provided some relief, there’s a question of how much damage has been done.

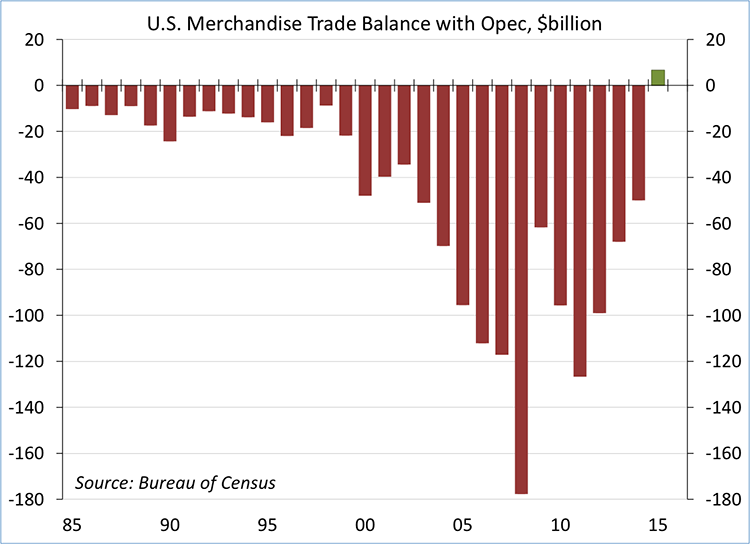

Not surprisingly, the U.S. has imported more stuff from abroad. However, nominal imports (the amount we pay for imported goods and materials) have fallen year-over-year due to the drop in import prices (mostly petroleum). The U.S. ran a trade surplus with OPEC last year (and in the first two months of 2016). This is a huge problem for many of the countries in OPEC, which have tied government spending programs to oil revenues. Moreover, while the contraction in U.S. energy exploration has been sharp, energy extraction is still going strong (down, but still high by historical standards).

U.S. merchandise exports have fallen, but mostly due to lower prices, especially for agricultural products and raw materials. The exception is exports of capital equipment, which have declined in inflation adjusted terms, reflecting the slowdown in capital spending worldwide. That slowdown in business investment is troubling, but it’s unclear how long it will last.

We have an inherently unstable global financial system. That doesn’t mean that downside risks will materialize, but they may. Trade is important to the U.S. economy, but we’ve always been relatively self-contained and strength in the domestic economy should remain the driving force in the quarters and years ahead. For the financial markets, we’re likely to see forces of optimism and pessimism duking it out for some time.