Mid-Cap Dividend Growth Stocks by Sector: Part 2A Regional Banks

In part 1 of this series on fairly valued mid-cap investment opportunities I primarily focused on non-dividend paying growth oriented mid-caps. In part 2 of this series I turned my focus to finding fairly valued dividend paying mid-caps. However, as I was evaluating dividend paying mid-caps in the S&P 400 mid-cap index, it became clear to me that the differences between dividend paying mid-caps were more important than the similarities. Therefore, I have grouped the dividend paying mid-caps I found into 3 separate offerings focusing on sectors. In this, part 2A, I will be exclusively covering fairly valued mid-sized regional banks.

However, I feel it’s important to note that although there are several regional banks in the S&P 400 mid-cap index, I only found four dividend paying regional banks of reasonable quality that I considered attractively valued at this time. There were others that appeared reasonably valued, but they were excluded primarily because they were apparently willing participants in the financial debacle that many believe led to the Great Recession of 2008. Nevertheless, two of the four research candidates I present below did suffer stress during the financial crisis; however, their post crisis recoveries have been stronger than those I excluded.

4 Fairly Valued Regional Banks

The following portfolio review summarizes the four mid-cap dividend paying regional banks. The portfolio review lists them by ticker, name, credit rating, sector, exchange, P/E ratio, dividend yield and market cap.

Note: S&P Capital IQ does not report debt to capital on banks. Therefore, ignore the debt to capital number shown in the FAST FACTS boxes to the right of the graphs.

Since many readers may not be familiar with each of these small-cap selections, I offer the following overview of each of the 4 research candidates. Courtesy of S&P Capital IQ, I included a short business description on each. Additionally, I have provided earnings and price correlated historical F.A.S.T. Graphs™ on each with a calculated return forecast out to 2017 based on what I considered the most appropriate valuation reference line.

Note: I have moved the return calculation pop-up to the left corner of the graph so that it did not cover up important data listed in the FAST FACTS.

F.A.S.T. Graphs™ Tutorial

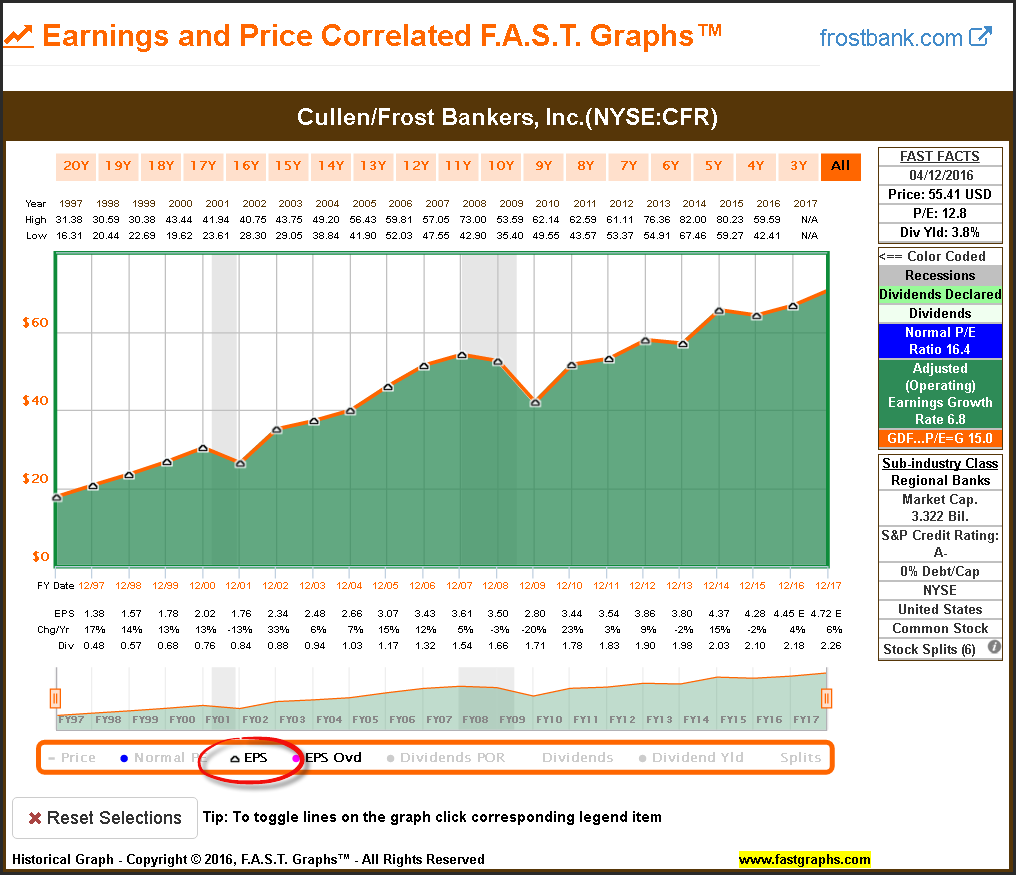

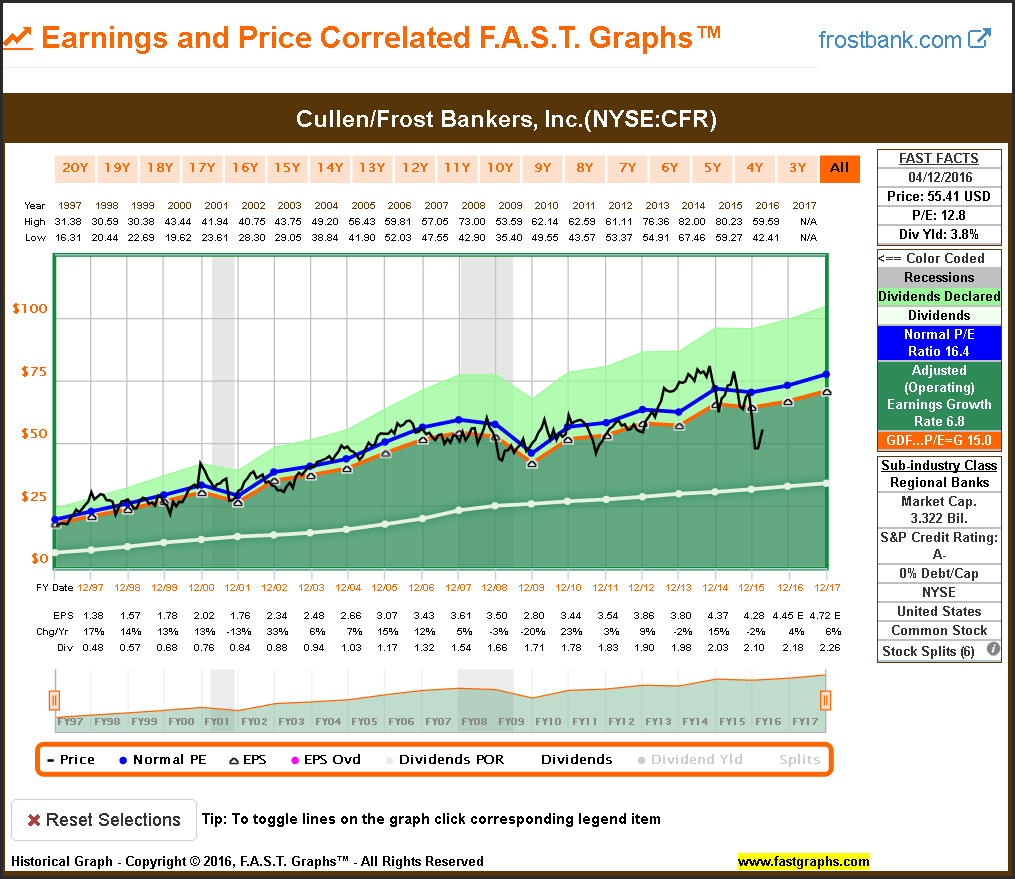

In order for the reader to get the maximum benefit from the following presentation, I offer a short tutorial illustrating the various components presented in a F.A.S.T. Graphs™. To accomplish this, I will present each component of the graph separately as I rebuild an entire graph. I have chosen Cullen/Frost Bankers, Inc. as my tutorial example because it will be the first research candidate I will eventually present.

My first screenshot reflects a plotting of earnings per share. The green shaded area represents a mountain chart of the company’s earnings over the timeframe drawn. The orange valuation reference line contains two important aspects. The first aspect is a multiple of earnings (P/E ratio) that is listed in the orange colored rectangle in the FAST FACTS to the right of the graph. In this example, the orange line represents a P/E ratio of 15. In other words, any time the stock price touches the orange line anywhere on the graph in this example, it will be trading at a P/E ratio of 15.

The second aspect of the orange line is the slope which is equal to the earnings growth rate. In this example, the orange line is increasing at the earnings growth rate (the green rectangle in the FAST FACTS) of 6.8%. Although there is some cyclicality with earnings in between, this growth rate is calculated as the annualized growth from the first year’s earnings per share to the last year on the graph.

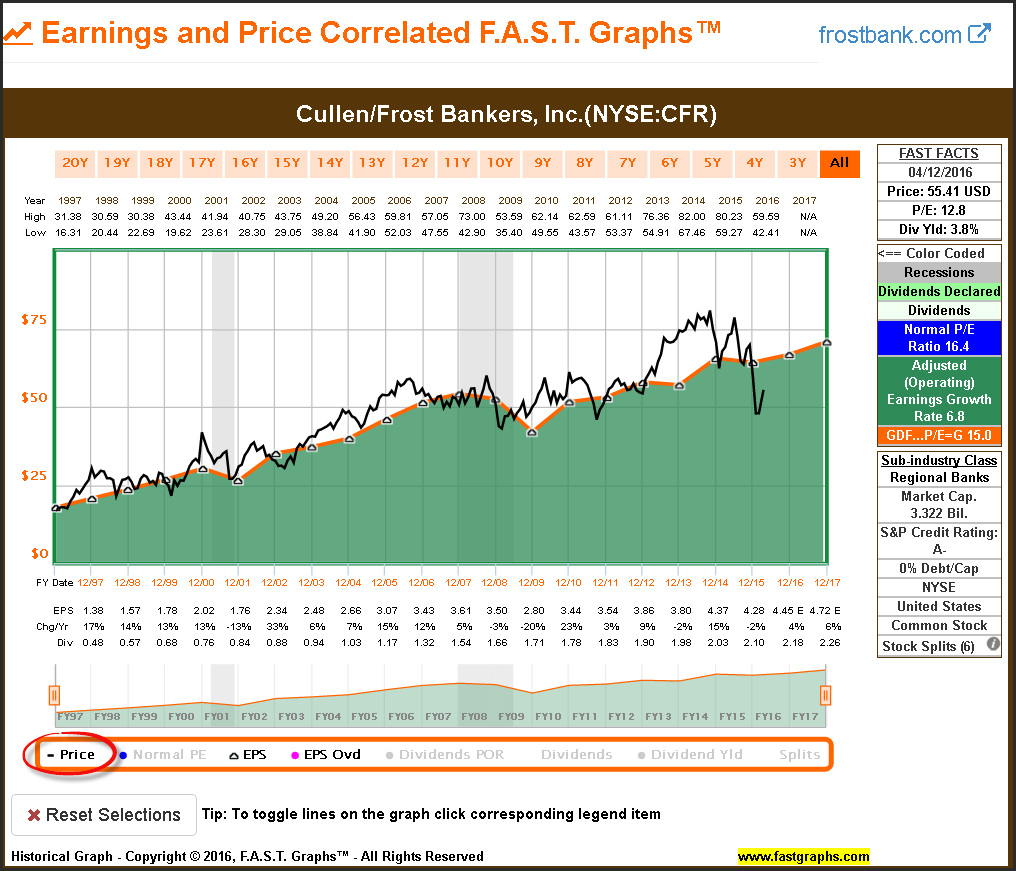

With my second screenshot I overlay monthly closing stock prices. This illustrates how stock prices move in conjunction with earnings over the long run. Moreover, periods of overvaluation (when price is above the orange line), fair valuation (when price is touching the orange line) and undervaluation (when price is below the orange line) is clearly revealed. Most importantly, since stock price tracks earnings, it is clear that the company’s earnings achievement is what drives the capital appreciation component of total return.

This next screenshot adds a second valuation reference line (the dark blue line) which is a calculated normal P/E ratio for the timeframe drawn. In this example, the normal P/E ratio line represents a multiple of 16.4. With both of these valuation reference lines on the graph, a clear perspective of a range of valuation is revealed for analysis.

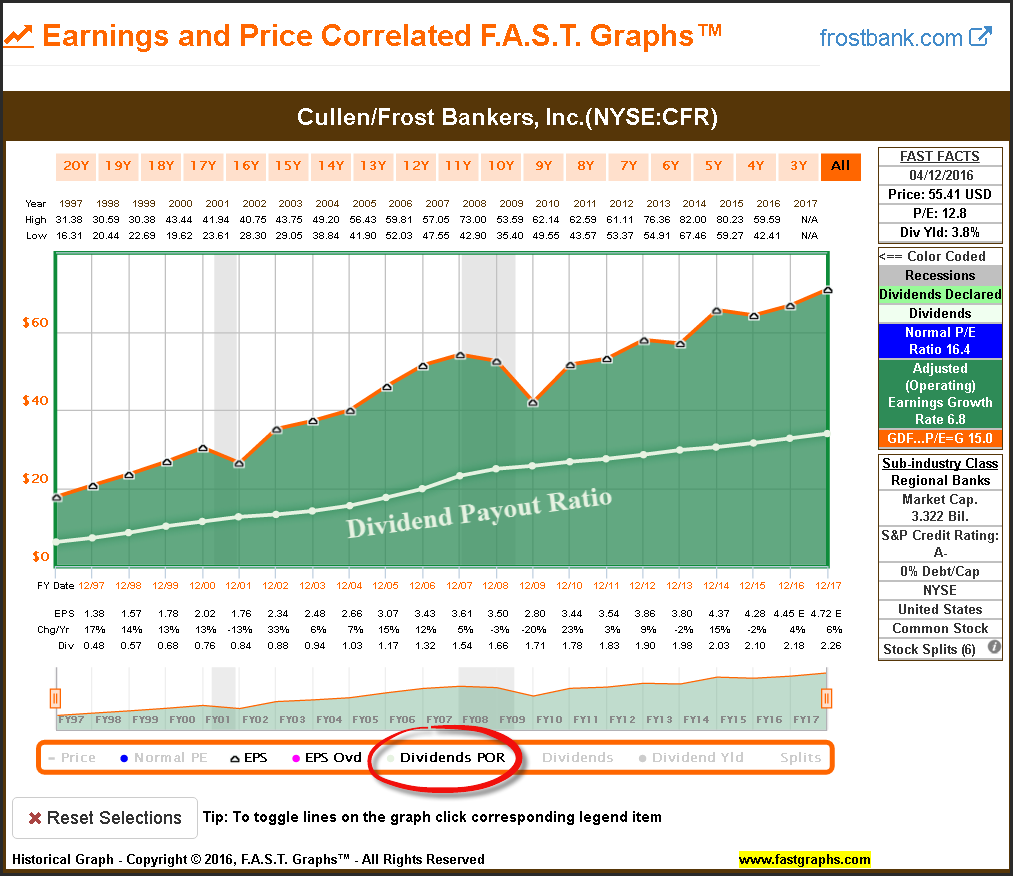

This next screenshot adds a plotting of the company’s dividends per share prior to being paid out of earnings. The area below the light green line (it appears white to many people) represents the portion of earnings paid out to shareholders. Therefore, the company’s dividend payout ratio (POR) is graphically presented for instant reference.

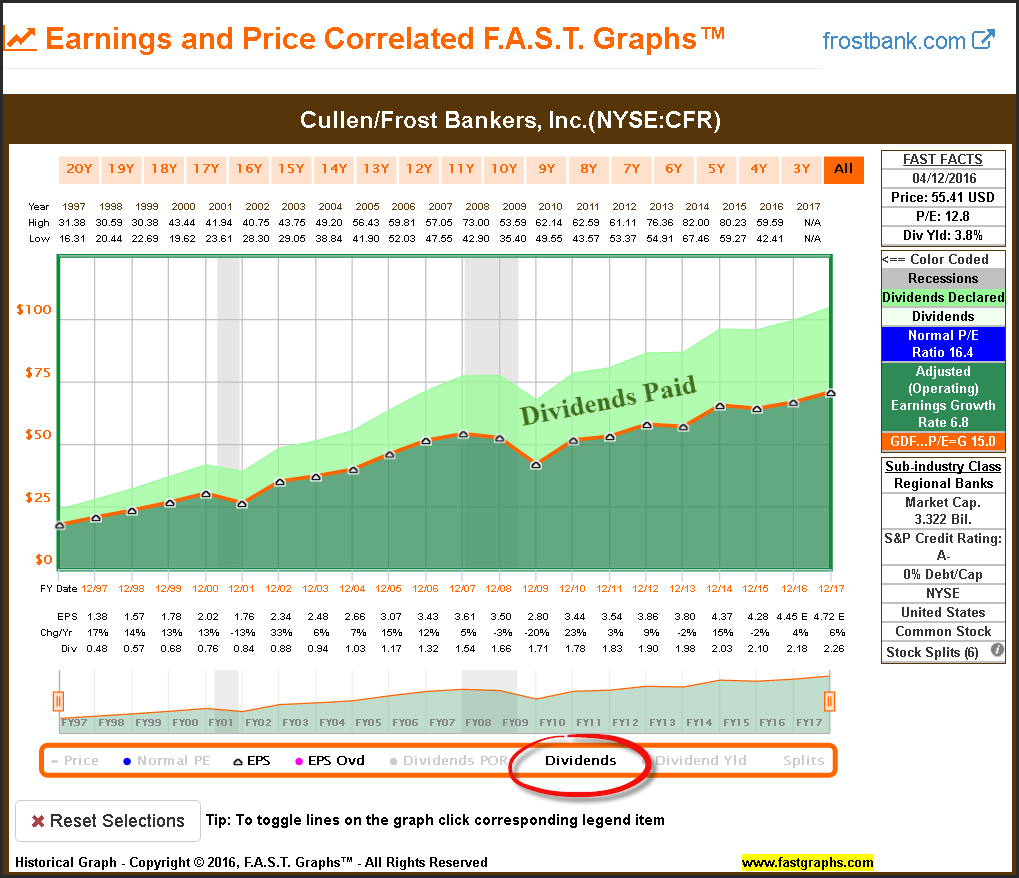

This next screenshot presents a second dividend reference. The light green shaded area above the orange line indicates the same dividends seen above after they have been paid out to shareholders. This light green shaded area (dividends paid) represents the dividend income component of total return.

The complete F.A.S.T. Graphs™ illustrates the earnings and price relationship, offers two valuation reference lines and graphically presents the company’s dividend payout ratio and dividends after they are paid out to shareholders. Most importantly, a perspective of the company’s current valuation relative to fundamentals is clearly illustrated.

Cullen/Frost Bankers, Inc. (CFR)

“Cullen/Frost Bankers, Inc. operates as the holding company for Frost Bank that offers commercial and consumer banking services in Texas. The company operates in two segments, Banking and Frost Wealth Advisors.

It provides commercial banking services to corporations and other business clients, including financing for industrial and commercial properties, interim construction, equipment, inventories, and accounts receivable; acquisition financing; commercial leasing; and treasury management services.

The company also offers consumer banking services, such as checking accounts, savings programs, automated-teller machines (ATMs), overdraft facilities, installment and real estate loans, home equity loans and lines of credit, drive-in and night deposit services, safe deposit facilities, and brokerage services. It international banking services comprise accepting deposits, making loans, issuing letter of credits, handling foreign collections, transmitting funds, and dealing in foreign exchange.

In addition, the company acts as correspondent for approximately 247 financial institutions; offers trust, investment, agency, and custodial services for individual and corporate clients; provides capital market services consisting of sales and trading, new issue underwriting, money market trading, and securities safekeeping and clearance; and supports international business activities.

Further, it offers insurance and securities brokerage services; holds securities for investment purposes; and provides loans to qualified borrowers, as well as offers investment management services to Frost-managed mutual funds, institutions, and individuals.

The company operates approximately 126 financial centers and approximately 1,200 ATMs in Texas. It serves energy, manufacturing, services, construction, retail, telecommunications, healthcare, military, and transportation industries. Cullen/Frost Bankers, Inc. was founded in 1868 and is headquartered in San Antonio, Texas.”

Investment Thesis

I chose to present Cullen/Frost Bankers, Inc. for a couple of important reasons. First and foremost, I was attracted to the consistent historical earnings growth and steadily rising dividend. Although earnings weakened during the Great Recession, this regional bank performed extremely well on an operating basis in comparison to most of its peers. In other words, this regional bank avoided participating in most of the toxic behavior seen with most banks big and large.

I was also attracted to the company’s high current yield and its current low valuation. Consequently, I see the combination of future P/E ratio expansion coupled with earnings and dividend growth in the range of 5% to 6% a compelling opportunity, as depicted in the performance calculation. Additionally, Cullen/Frost Bankers, Inc.’s A- credit rating is also a plus.

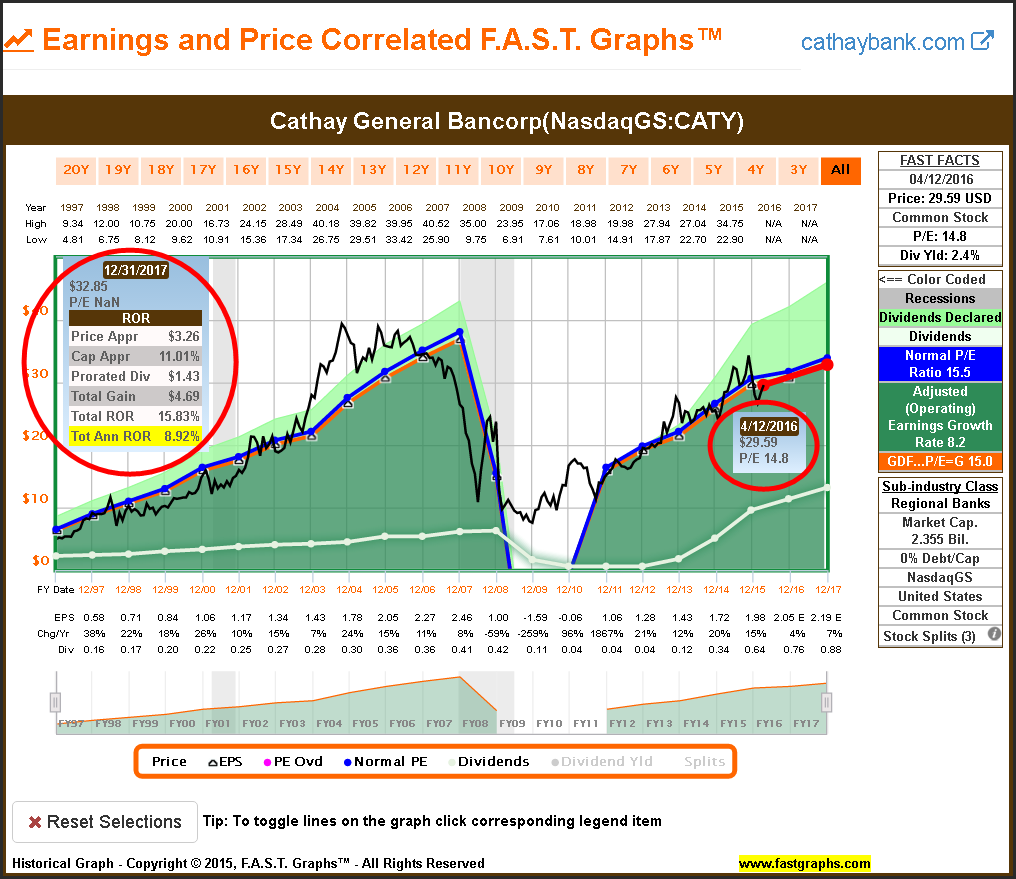

Cathay General Bancorp (CATY)

“Cathay General Bancorp operates as the holding company for Cathay Bank that offers various commercial banking products and services for individuals, professionals, and small to medium-sized businesses in the United States.

It offers various deposit products, including passbook accounts, checking accounts, money market deposit accounts, certificates of deposit, individual retirement accounts, college certificates of deposit, and public funds deposits.

The company’s loan portfolio consists of commercial mortgage loans, commercial loans, small business administration loans, residential mortgage loans, real estate construction loans, and home equity lines of credit, as well as installment loans to individuals for automobile, household, and other consumer expenditures.

In addition, it provides letters of credit, wire transfers, forward currency spot and forward contracts, traveler’s checks, safe deposit, night deposit, social security payment deposit, collection, bank-by-mail, drive-up and walk-up windows, automatic teller machines, Internet banking, investment, and other customary bank services, as well as securities and insurance products.

As of December 31, 2015, the company operated 21 branches in southern California; 12 branches in northern California; 12 branches in New York; 3 branches in Illinois; 3 branches in Washington; 2 branches in Texas; 1 in Maryland; 1 in Massachusetts; 1 in Nevada; 1 in New Jersey; and 1 in Hong Kong, as well as a representative office in Shanghai and in Taipei. Cathay General Bancorp was founded in 1990 and is headquartered in Los Angeles, California.”

Investment Thesis

I included Cathay General Bancorp primarily because of its strong recovery since the Great Recession. Clearly, this regional bank did get caught up in the financial crisis. However, their subsequent recovery has been stronger than most of their peers. Hopefully, this regional bank learned a valuable lesson from the financial crisis. Current valuation is attractive, and I like the dividend yield in conjunction with an increasing payout ratio.

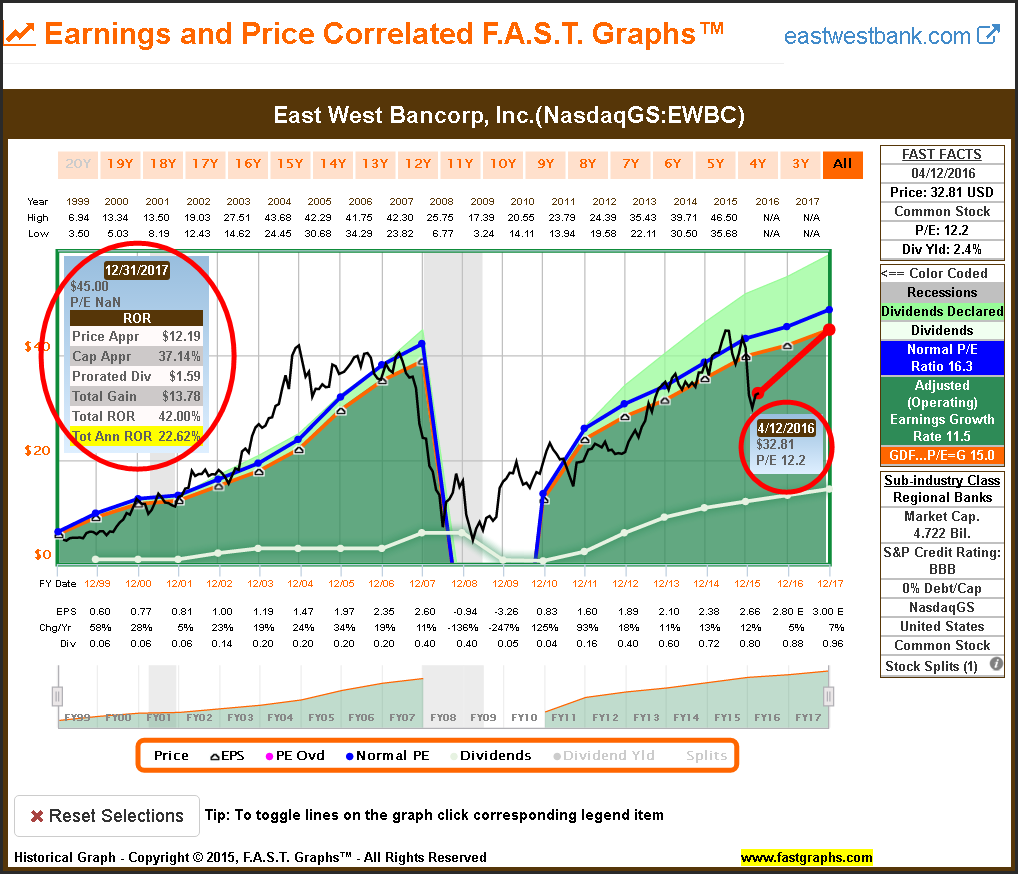

East West Bancorp Inc (EWBC)

“East West Bancorp, Inc. operates as the bank holding company for East West Bank that provides a range of personal and commercial banking services to small and medium-sized businesses, business executives, professionals, and other individuals. The company operates through three segments: Retail Banking, Commercial Banking, and Other.

It offers various deposit products comprising personal and business checking and savings accounts, time deposits and individual retirement accounts, travelers’ checks, safe deposit boxes, and MasterCard and Visa merchant deposit services.

The company’s lending portfolio consists of residential single-family and multifamily loans; commercial real estate loans, and construction and land loans; trade finance loans; commercial business loans, including accounts receivable, small business administration, inventory, and working capital loans; and consumer loans, such as home equity lines of credit, auto loans, and insurance premium financing loans.

In addition, it provides financing to clients needing a financial bridge that facilitates their business transactions between the United States and Greater China. As of January 27, 2016, the company operated approximately 130 locations in California, Georgia, Massachusetts, Nevada, New York, Texas, and Washington; full service branches in Hong Kong, Shanghai, Shantou, and Shenzhen; and representative offices in Beijing, Chongqing, Guangzhou, Taipei, and Xiamen.

East West Bancorp, Inc. was founded in 1998 and is headquartered in Pasadena, California.”

Investment Thesis

I also included East West Bancorp, Inc. primarily because of its strong recovery since the Great Recession. Clearly, this regional bank did get caught up in the financial crisis. However, their subsequent recovery has been stronger than most of their peers. Hopefully, this regional bank also learned a valuable lesson from the financial crisis. Current valuation is compelling, and I also like the dividend yield in conjunction with an increasing payout ratio. Above-average forecast earnings growth coupled with the potential for P/E ratio expansion could lead to substantial total returns.

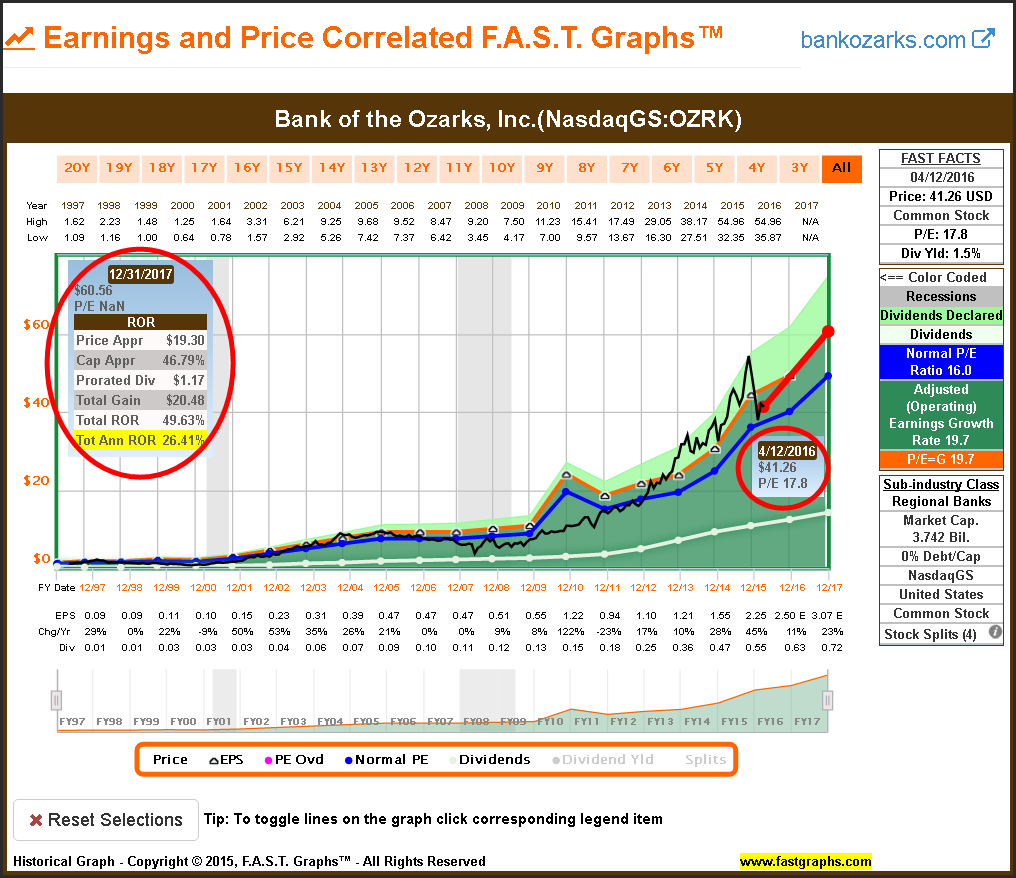

Bank of the Ozarks Inc (OZRK)

“Bank of the Ozarks, Inc. operates as a bank holding company for Bank of the Ozarks that provides various banking products and services. The company accepts non-interest bearing checking, interest bearing transaction, business sweep, savings, money market, and individual retirement accounts; and time deposits. Its loan products include loans secured by residential 1-4 family, non-farm/non-residential, agricultural, construction/land development, multifamily residential properties, and other land loans; and consumer loans.

The company’s loan products also comprise loans for commercial, industrial, and professional purposes, including loans to fund working capital requirements, purchase of machinery and equipment, and other purposes; term loans, balloon loans, and lines of credit; and agricultural loans for financing agricultural production consisting of loans to businesses or individuals engaged in the production of timber, poultry, livestock, or crops. In addition, it offers mortgage lending; treasury management services, such as wholesale lock box services; remote deposit capture services; and trust and wealth management services, including financial planning, money management, custodial, and corporate trust services.

Further, the company provides real estate appraisals; ATMs; telephone banking; online and mobile banking services comprising electronic bill pay and consumer mobile deposits; credit, debit, and gift cards; safe deposit boxes; investment brokerage services; and other products and services, as well as processes merchant debit and credit card transactions. It serves businesses, individuals, and non-profit and governmental entities.

As of December 31, 2015, the company operated 174 offices, which included 81 offices in Arkansas, 28 in Georgia, 25 in North Carolina, 22 in Texas, 10 in Florida, 3 in Alabama, 2 each in South Carolina and New York, and 1 in California.

Bank of the Ozarks, Inc. was founded in 1981 and is headquartered in Little Rock, Arkansas.”

Investment Thesis

I offer Bank of the Ozarks, Inc. as a growth story with a dividend kicker. Although I consider this regional bank fairly valued to even fully valued, I like the company’s historical operating record and growth potential going forward. Although the dividend yield is modest at approximately 1.5%, its record of dividend growth has been significantly above-average. Therefore, I offer Bank of the Ozarks, Inc. as primarily a total return opportunity with modest current dividend income.

Summary and Conclusions

The four mid-cap dividend growth stock research candidates featured in this article illustrate the differences that exist between individual companies. Two of these candidates represented examples of regional banks that avoided the worst of the financial crisis. Interestingly, one of them offered the highest yield with moderate growth, while the other had the lowest current yield with the highest growth potential. This speaks to the importance of selecting stocks that meet the individual investor’s unique and specific goals and objectives.

The other two companies were exposed to the ravages of the financial crisis and their operating results suffered consistent with most huge money center banks. However, they were included because their recoveries were swift and strong and hopefully because they learned their lessons. Nevertheless, the reader should be aware of what happened to these two companies during the financial crisis.

Furthermore, investors most often associate small and mid-cap companies as growth stocks. However, just as it is with larger companies, there are many different types of mid-cap stocks that investors can utilize in their portfolios. In part 2B I will present additional fairly valued mid-cap dividend growth stocks in the consumer discretionary sector.

Disclosure: No position.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.