Yesterday, Bryce correctly pointed out the tight relationship between interest rates and stock market leadership that has persisted for the past decade. As interest rates fall, cyclical stocks have tended to underperform while counter-cyclical stocks have tended to outperform. We would like to add another macro data point that has had a very close correlation to stock market leadership over the past decade: changes in China’s Forex reserves.

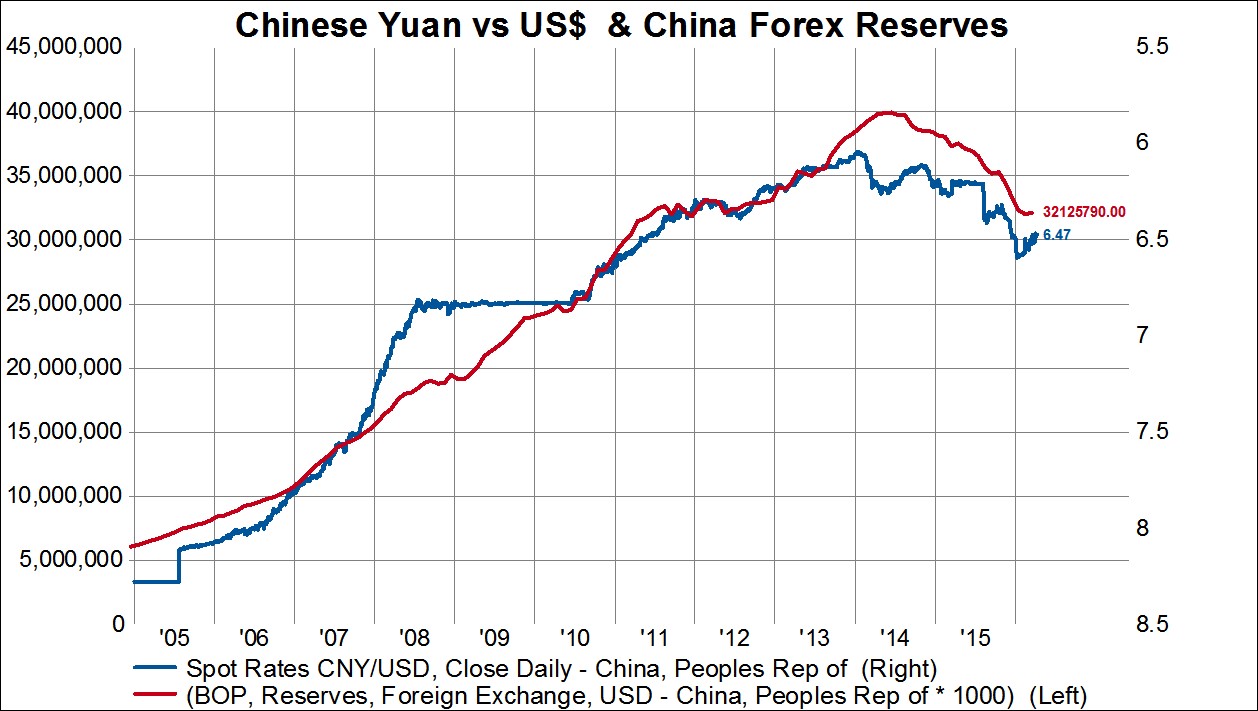

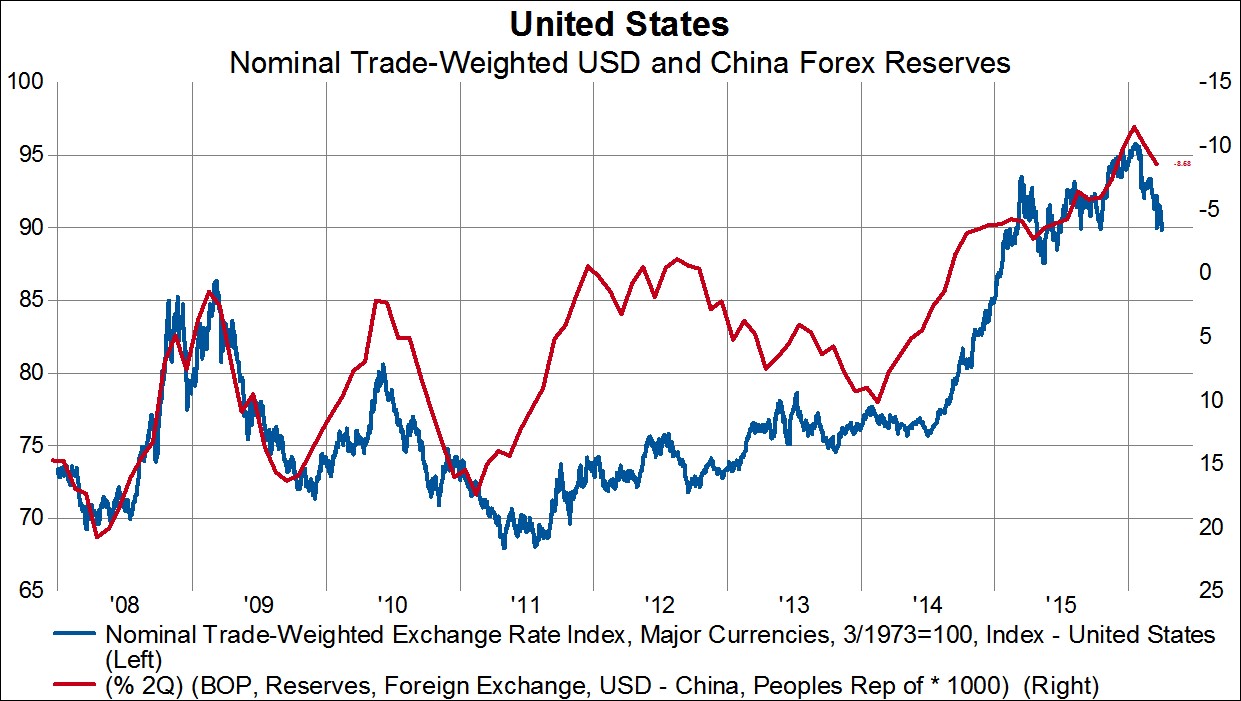

Since 2005 when China moved from a fixed peg to the dollar to a more flexible floating-band currency regime, Forex reserves were built up in order to maintain some control over the currency. From 2005 to early 2014, China’s Forex reserves increased by nearly 800% as the currency strengthened from 8.10 CNY/USD to 6.07 CNY/USD. Since February 2014, the yuan has reserved course and has depreciated by 7% and this decline in the currency was accompanied by a decline in Forex reserves to the tune of about 20%. As developed world bond yields have fallen towards zero thanks to quantitative easing and beggar thy neighbor currency policy, China has been forced to reduce its Forex reserve which has you will see has had major ramifications for cyclical stocks.

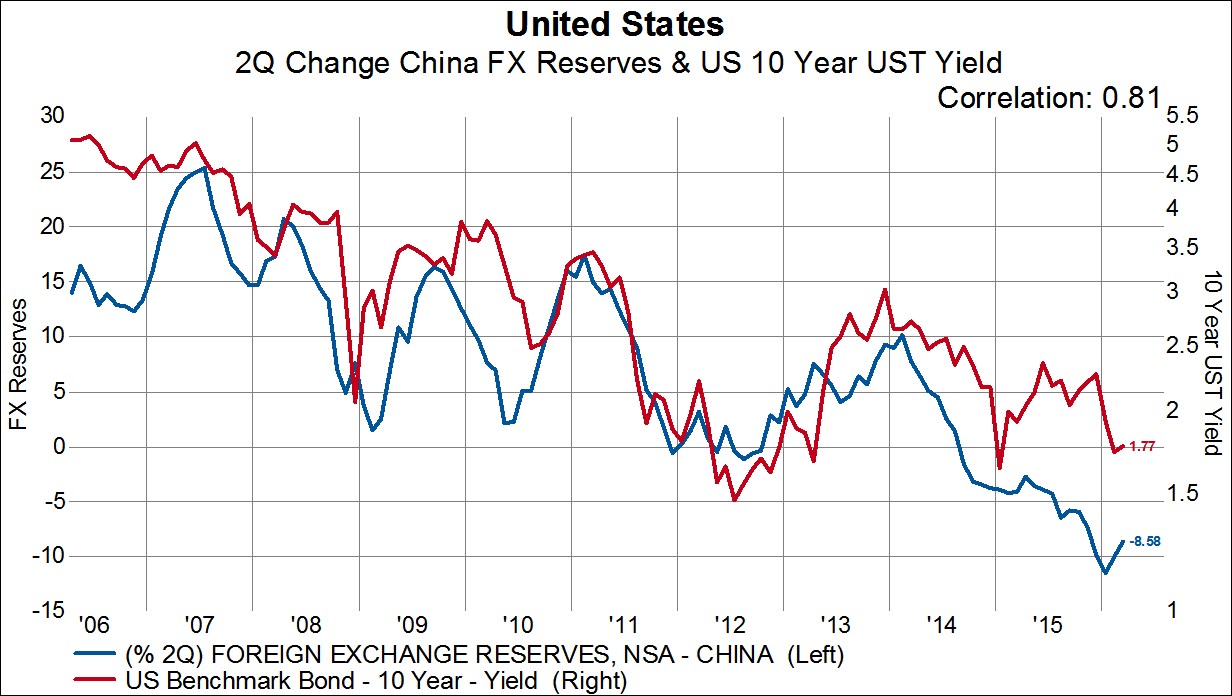

China’s forex reserves have moved from a 2-quarter annualized growth rate of +57% in the summer of 2007 to a -16% 2-quarter annualized decline as of March 2016. During this time, developed world cyclical stocks have underperformed by a little over 14%. Does it surprise anyone after looking at these charts that in February, when we had a bit of cyclical bounce in the stock market, there was also a slight moderation in the declining rate of Forex reserve during February from -21.7% 2-quarter annualized decline to -16.4%?

Cyclicals have once again started to underperformed and so consequently, we wouldn’t be surprised to see China’s Forex reserve decline once again when the the April data is released. Before wrapping up, we wanted to point out that European cyclical stock performance has been correlated with China Forex reserves to a greater degree than any other cyclical region. As the growth rate in Forex reserves has moved from very positive to very negative, European cyclicals have unperformed by nearly 40%. And once again, European cyclicals are underperforming which is another signal that China’s Forex reserves are probably declining once again.