The first quarter’s market action was driving by the escalation of fear and the ebbing of that fear, ending with expectations of “more of the same” – that is, mixed but moderate economic growth and a very gradual pace of Fed tightening.

In the last two weeks of March, two key economic reports sent economists downgrading their forecasts of 1Q16 GDP growth. Shipments of capital goods were weaker into February, suggesting that business fixed investment will likely make a negative contribution to GDP. Consumer spending (70% of GDP) was soft in February, but the downward revision to January’s figure suggests that the 1Q pace will be a lot slower than anticipated. Much of this is simply arithmetic, merely where the numbers happen to fall. Consumer spending growth was revised higher in 4Q15 (to a 2.4% annual rate) and that may have come at the expense of first quarter growth. The contraction in business investment reflects a further collapse in energy exploration and the impact of a strong dollar on exports. However, some likely reflects recession fears and election-year uncertainty. If, as expected, consumer spending picks back up in 2Q16, business fears should ease. However, political uncertainty may linger well into early 2017 (as it may take some time for the new administration to make its intentions clear and establish that it has the ability to get something done). One soft quarter is not the end of the world. Winter data are noisy and unreliable. However, the 1Q16 figures significantly raise the importance of the spring economic reports.

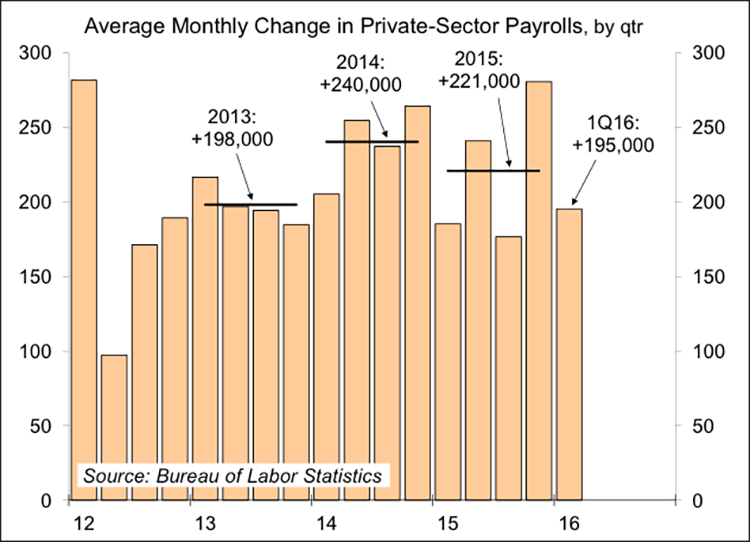

The monthly employment report is valued for its timeliness and relative accuracy (at least, compared to other data releases). Payroll growth remained strong in the first quarter.

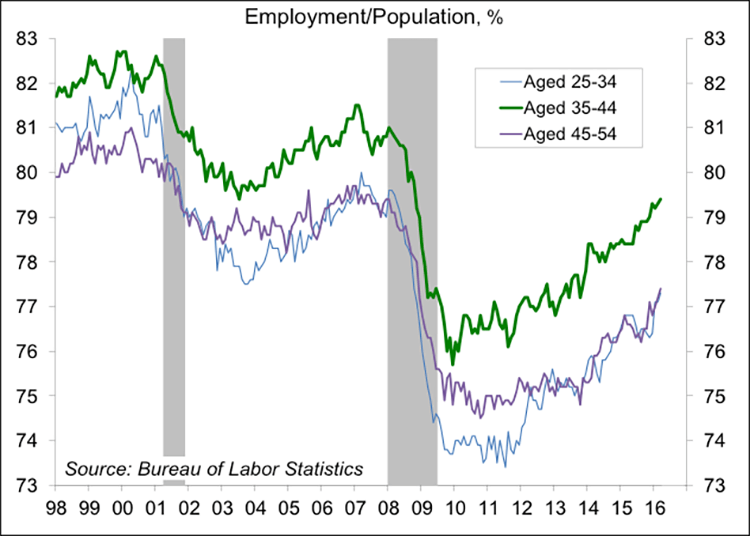

The pace of payroll growth is expected to slow in the months ahead, but not because of a weak economy. Rather, firms are likely to find it more difficult to find qualified workers. The unemployment rate appears to be flattening out, but that reflects an increase in labor force participation. Much has been made of the decline in labor force participation over the last several years. Some of that is the demographics, the fact that the baby-boomers are moving into retirement. However, many unemployed workers have exited the labor force. Participation rates for younger workers have also declined. That trend now appears to have turned. Employment/population ratios are trending higher. This is a key issue for the Fed. Exactly how much slack remains in the job market? The data suggest that there is still plenty of room for improvement. The Fed recognizes this and anticipates that monetary policy will be tightened gradually over several quarters.

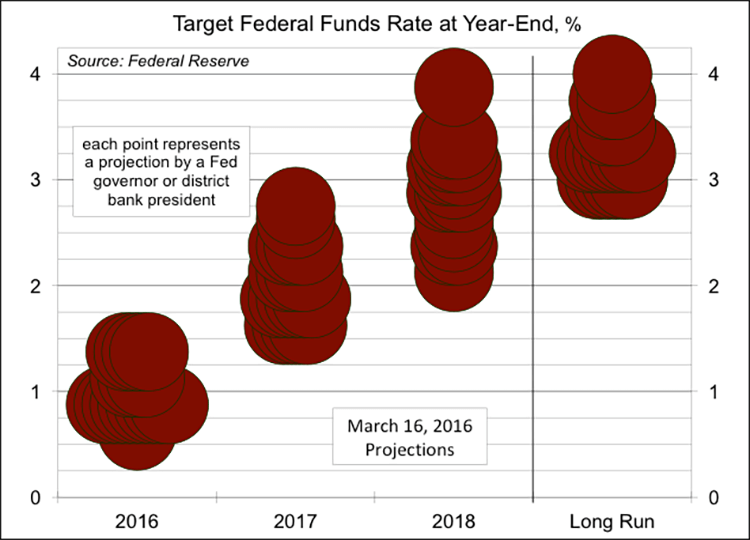

In her speech last week, Fed Chair Yellen countered dot plot misconceptions by emphasizing that these are expectations, not a hardwired plan. Each dot represents an expectation of a senior Fed official and there is considerable uncertainty around each dot (reflecting the uncertainty in the expected evolution of the economy). If it helps, you can simply make the dots bigger: