U.S. Real GDP Growth Was Very Weak in the First Quarter of 2016

Each month, the U.S. Institute for Supply Management (ISM) conducts a survey on the state of the manufacturing and non-manufacturing industries of the U.S. economy and releases data for the previous month. The data are closely followed by the financial media, economists, and wealth portfolio managers as they provide the earliest reading on the state of the economy.

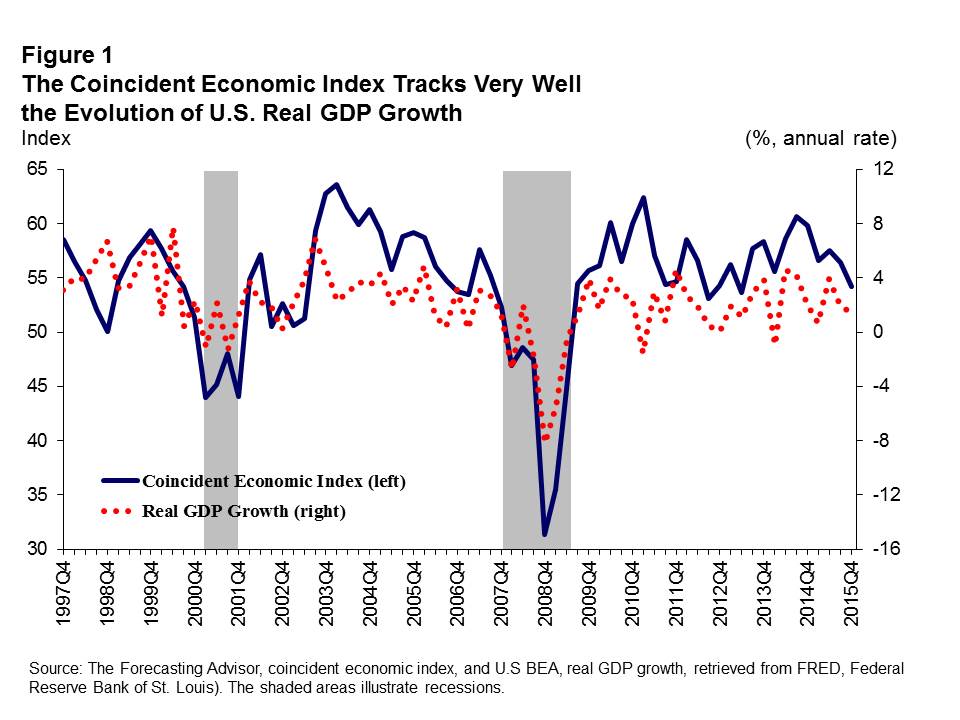

The ISM indicators cover different fields of the manufacturing and non-manufacturing industries, such as production level, employment level, new orders, inventories, exports, imports and prices.1 The Forecasting Advisor choose a number of indicators from the ISM survey to construct a monthly coincident economic index (i.e. a measure of the current overall economic situation) from July 1997. Figure 1 illustrates the evolution of real GDP growth and the coincident economic index from the third quarter of 1997 to the third quarter of 2015. It shows that the coincident economic index is highly correlated with the evolution of U.S. real GDP growth during that period. More specifically, the coincident economic index tracks very well the periods of weakening, including before the start of the recession of 2008-2009 and the periods of strengthening in real GDP growth between 1997 and 2015. Since the ISM data are never revised during the year2 and timely, the coincident economic index is undoubtedly a valuable indicator to assess the state of the U.S. economy.

The Current State of the U.S. Economy

The Forecasting Advisor Model is used here to provide a forecast of the rate of change in U.S. real GDP for the first quarter of 2016. The official first estimate for the first quarter will be released by the U.S. Bureau of Economic Analysis (BEA) on April 28.

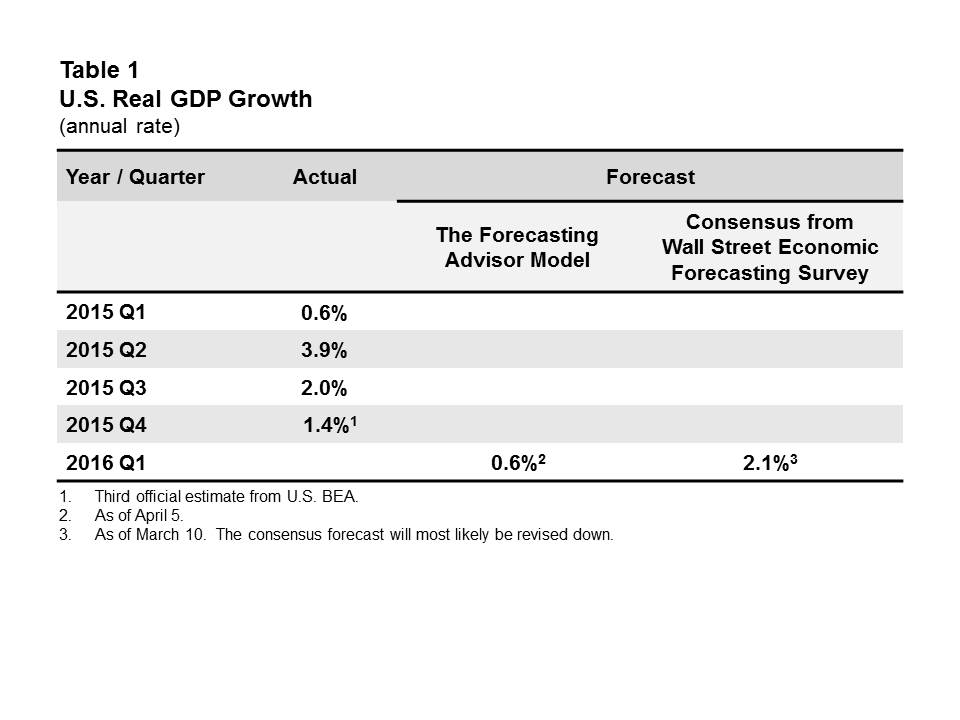

The forecast for the first quarter of 2016 from The Forecasting Advisor Model is reported in Figure 2 and Table 1 below. We also included in the Table the most recent consensus from the Wall Street Economic Forecasting Survey. The Forecasting Advisor Model projects a slight increase of 0.6% (annual rate) in real GDP for the first quarter, based on data up to March. Real GDP grew by 1.4% (third official estimate) in the last quarter of 2015. We will release on May 4 the first real GDP growth forecast for the second quarter of 2016. The model will, thus, continue to provide timely and insightful intelligence on the real state of the U.S. economy leading up to the next recession.

And

And

The Forecasting Advisor Model

The Forecasting Advisor Model

The first estimate on real GDP growth by the U.S. BEA is released one month after the end of a quarter. This estimate does not always provide information on the real state of the economy as the data are subsequently revised and often significantly. For example, at the end of April 2008, the U.S. BEA stated that real GDP grew 0.6% in the first quarter of 2008 (identified as the start of a recession at the end of 20083). The growth rate of 0.6% was subsequently revised down sharply (at least) a year after, to a decline of 2.7%. Thus, the real state of the economy in the first quarter of 2008 was known only after a long lag.

The Forecasting Advisor has built a model to determine the short-term outlook for growth in real GDP. A forecast is calculated only for the current quarter. A key feature of the model is its ability to give without lags reliable predictions of the real current state of the economy. The model uses a number of economic indicators to predict the rate of growth in real GDP. The coincident economic index, the short-term interest rate, and the price of crude oil are among the most important economic indicators of the model.4 The economic indicators are never revised, except once a year for the coincident economic index. To illustrate, the forecasting process for the third quarter of 2015 is described below:

- A first forecast for the third quarter of 2015 was calculated on August 3 using data up to July for the economic indicators of the model.

- The first forecast was updated on September 6 to include new data for the month of August.

- A final forecast for the third quarter of 2015 was calculated on October 5 to include new data for the month of September, the last month of the third quarter.

The first estimate of real GDP growth for the third quarter of 2015 was released by the U.S. BEA on October 29. This is three months after the calculation of the first forecast for the third quarter. Thus, the first forecast provides timely and insightful intelligence on the current state of the U.S. economy well in advance of the release by the U.S. BEA.

Forecasting Performance

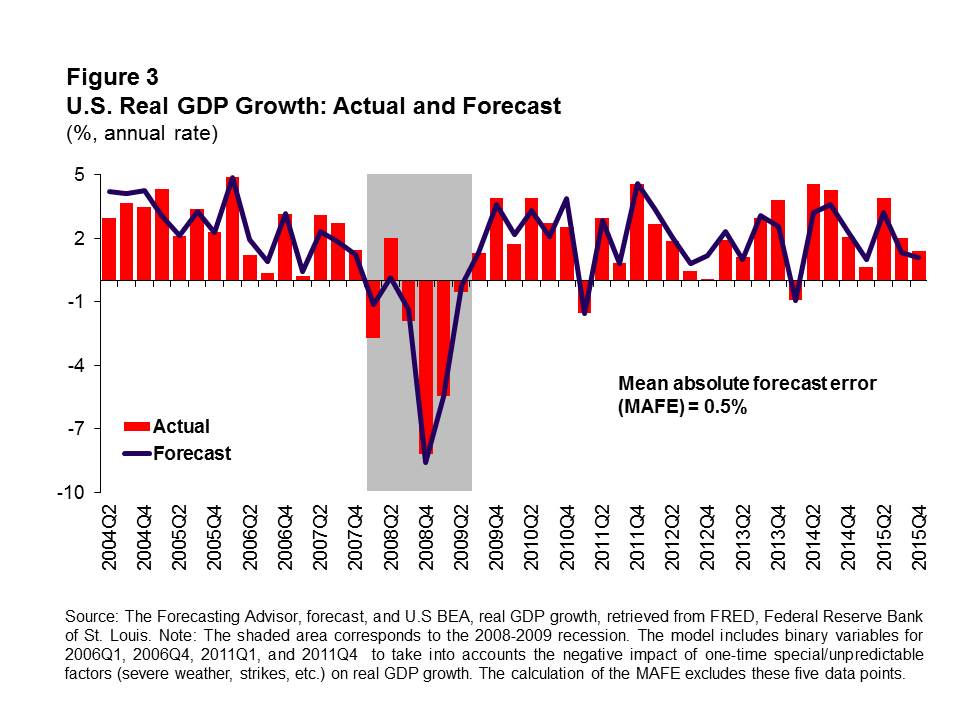

Figure 3 shows the performance of the Forecasting Advisor Model in predicting the rate of growth in real GDP from the second quarter of 2004 to the third quarter of 2015. The model does very well both prior to and during the last recession as well as during all the current expansion. On average, the absolute forecast error (in-sample) is 0.5% (annual rate) per quarter over the full period. For example, the forecast for the third quarter of 2015 was 1.7% compared to a third official estimate of 2.0%. Thus, the model correctly predicted the sharp deceleration in the rate of increase in real GDP in the third quarter. The ability of the model to predict well the direction of the rate of change in real GDP (i.e. the acceleration or the deceleration in the pace of growth in economic activity) from one quarter to the next is evident not just for the third quarter of 2015, but also for the full period. Indeed, the model predicted correctly 85 per cent of the time the direction of the rate of change in real GDP from one quarter to the next between 2004 and 2015.4

In brief, the forecasting model of real GDP growth will provide timely and insightful intelligence on the real state of the U.S. economy leading up to the next recession.

1 Data from the non-manufacturing survey are only available from July 1997. Manufacturing data are available from January 1948.

2 The ISM data are revised in January of each year because of the calculation of new seasonal factors for the previous four years. The change in the values of the ISM data is minimal.

3 The U.S. National Bureau of Economic Research always announced the start a recession with a long lag. For example, they declared on December 1, 2008 that a recession began in the first quarter of 2008.

4 The model includes binary variables for 2006Q1, 2006Q4, 2011Q1, and 2011Q4 to take into accounts the negative impact of one-time special/unpredictable factors (severe weather, strikes, etc.) on real GDP growth