“Corporate sector metrics have been disappointing of late… Companies are scaling back expenditures of all kinds (capital expenditures, hiring, and inventory-builds, for example), as their top-line revenues and earnings decelerate. Though first-quarter numbers may come in better than beaten-down forecasts, firms are finding that top line revenues are still hard to grow significantly.” Rick Rieder, Head of Global Fixed Income, BlackRock

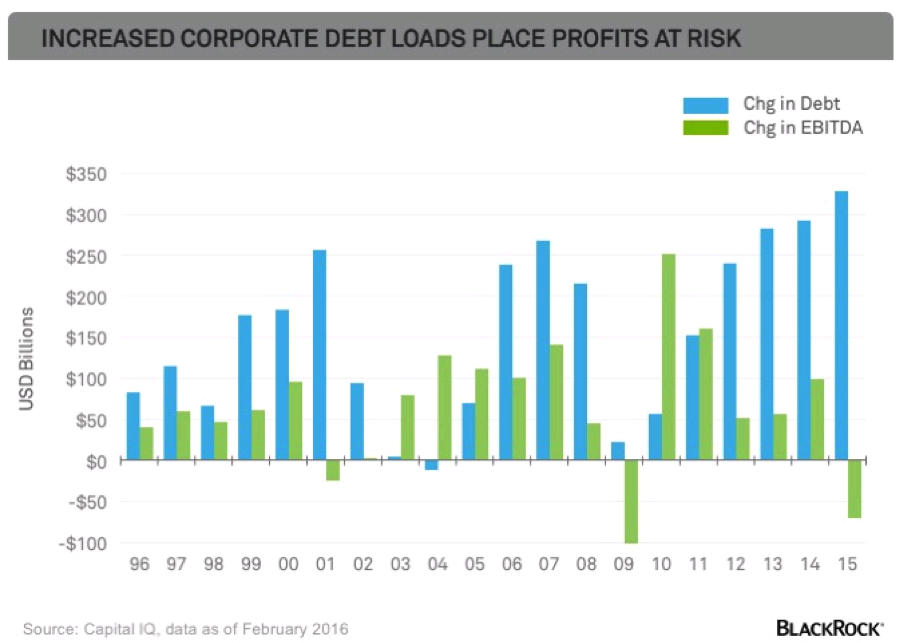

As you see in the next chart, increased corporate debt loads place profits at risk.

It’s profits we need to worry about especially when valuations are high. This is a headwind to further market upside.

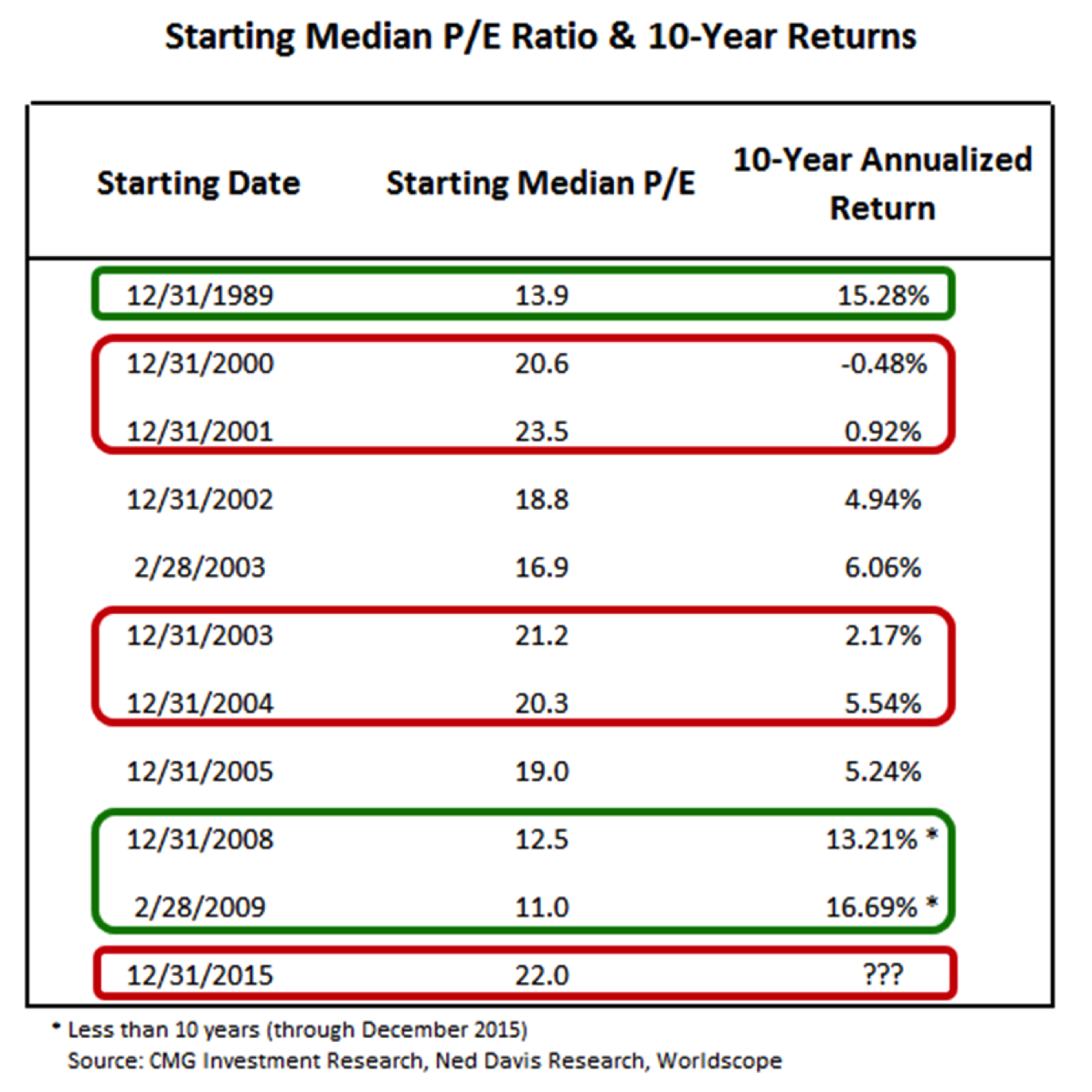

If you want to get a good sense for why high valuations lead to poor future returns, I wrote a piece this week for Forbes titled, “Plump P/E Ratio Suggests Subdued Stock Market Returns Ahead.” Click here to go to the article.

The point is that debt is a drag on profits. It is concerning now but will be even more concerning if (scratch that) when interest rates begin to rise.

So it is forward we must set our gaze.

Chicago Fed President Charles Evans said Tuesday that two rate steps this year are “not at all unreasonable,” while his colleague from Philadelphia, Patrick Harker, said he would like to see policy makers tightening borrowing costs “a little faster.”

St. Louis Fed President James Bullard said policy makers should consider raising interest rates at their next meeting amid a broadly unchanged economic outlook and prospects of inflation and unemployment exceeding targets.

Bullard added, “I didn’t want to be raising rates further in an environment where we had declining inflation expectations,” he said. Since mid-February, “they have bounced back up” so “that is making me feel better. We are moving in the right direction.” Source

Three steps and a stumble is an old rule on Wall Street. That means the Fed raises interest rates three times in a row. NASDAQ defines it as a rule predicting that stock and bond prices will fall following three increases in the discount rate by the Federal Reserve. This is a result of increased costs of borrowing for companies and the increased attractiveness of money market funds and CDs over stocks and bonds as a result of the higher interest rates. Frankly, I recall the rule to be two steps and a stumble but hey, birthday number 55 is knocking on my door.

Three steps seem to make more sense to me today as our starting place was from an unprecedented 0%. Rate hike number one is behind us. The Fed is fighting to create inflation (as are the other suspects: ECB, JCB and China’s Central Bank). All in, including the U.S., they make up over 70% of the world GDP.

I wrote about Henry Hazlett recently and shared my thoughts on inflation (here) and agree with this next statement from Bullard, “I think we are going to end up overshooting on inflation.”

“Now these monetary institutions are expected to continue producing miracles. But their ability to repeatedly pull new rabbits out of their policy hats has been stretched to an increasingly unsustainable degree.” Mohamed A. El-Erian, The Only Game in Town

And just a few more quotes from El-Erian’s book:

“…they have become single-handedly responsible for the fate of the global economy. Responding to one emergency after the other, they have set aside their conventional approaches and — instead — evolved into serial policy experimenters.

Often, and very counterintuitively for such tradition-obsessed institutions, they have been forced to make things up on the spot. Repeatedly, they have been compelled to resort to untested policy instruments. And, with their expectations for better outcomes often disappointed…”

Untested policy instruments. The markets seem to be somewhat smoothed by the Fed “Put” (the backstop for the market). However, I think that floor is thinning. Forward we must march.

Today, let’s keep it short. I share a great opinion piece from David Zervos. He talks about the détente agreement between the ECB, the JCB, the Chinese Central Bank and the Fed. I think he is spot on. The world is awash in unmanageable debt and the chemists are playing with the mix.

I also touch on the deterioration in credit ratings, a 15-year low. What is the catalyst that ignites the debt bomb? My two cents is that it is when inflation and interest rate expectations begin to move higher. I conclude this weeks piece with a few portfolio construction ideas in Trade Signals.

Enjoy your long weekend. Wishing you and your family a wonderful Easter. Thank you very much for your interest in On My Radar. I hope you find it helpful.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- She May Be the Best We Have Ever Seen, David Zervos, Jefferies

- Average Corporate Credit Rating Hits 15-year Low

- Trade Signals – Nearing Extreme Optimism

She May Be the Best We Have Ever Seen, David Zervos, Jefferies

Janet’s performance yesterday was nothing short of stellar. She delivered what was no doubt the most dovish message of her entire central banking career, and she did it without a single communication mishap. Her message contained three key points:

- The balance of risks for inflation is lower, and there should be no concern associated with any temporary inflation overshoots.

- Employment gains have been strong, but there’s still more work to be done in bringing excess labor market slack back into the workforce.

- The international situation poses a great danger to financial stability and thus should be a key factor in determining the timing of future monetary policy moves. (SB here: bold emphasis mine.)

Now to be sure this was not an easy message to convey. The unemployment rate sits almost on top of the NAIRU, and all the major core inflation measures are straddling the target of 2%. A simple rule from the fresh water macro crowd would be screaming for rate hikes towards 3-4% rapidly. But thankfully Janet has treated those nugatory recommendations appropriately!

She was at the G20 meeting in Shanghai. She understood perfectly well that the Chinese monetary policy link to the US “directly” extends the reach of Fed policy far beyond the US borders. And she has surely been scarred (like we all have) by the PBOC moves of August and January.

Thus, in my opinion, Janet fully complied with the “détente” concept which we have been writing about in these notes for many weeks. She called off the DXY rally, and implored her colleagues at the ECB and BoJ to do the same. And as we saw over the last week, both institutions complied!! Everyone at the G20 table realized that monetary policies involving a currency devaluation by the Europeans and Japanese, or monetary policies involving currency appreciation by the US, would be counterproductive.

They would unleash a full-blown CNY devaluation – something that would make the August and January moves look like child’s play.

So where do we stand now? Well, the Europeans and Japanese will basically be leaving interest rate policies alone. Mario dumped forward guidance, and Kuroda drew a “theoretical” line in the sand at -50bps for the Yen deposit rate (his “practical” line may even be higher).

These gentlemen are now only free to pursue DOMESTIC credit easing policies with their balance sheets — such as DOMESTIC corporate bond purchases, DOMESTIC equity purchases, and DOMESTIC funding for lending schemes.

Importantly, they do not have access to the policy lever associated with driving short term risk free real rates lower. That is the détente agreement. In addition, the FOMC will refrain from pushing short-term risk-free rates materially higher, also keeping the DXY in check.

These implicit agreements now allow the Chinese to carefully unwind their domestic asset/debt bubble, and slowly decouple the CNH from the USD. Of course this is a fragile agreement, because if any one party deviates, the peg breaks and the 1998 style fireworks begin. (SB: again emphasis mine)

Looking ahead, I will refer to this détente structure as the “holy foursome” of central banking. And it is worth noting that this agreement not only benefits each of the big four, but it takes enormous pressure off of Emerging Markets, which would have no doubt been crushed by a full blown Chinese devaluation move. I personally cannot think of a better outcome for this very complex global situation than what occurred at the G20 “currency peace” summit.

That said, there will likely be plenty of near-term confusion in markets as folks try to trade off of the old weak currency/strong equity market correlations. My guess is that correlation is about to break hard – and a bunch of black box systematic correlation junkies are about to get their heads handed to them. It’s going to be a very interesting next few weeks in trading. But that complication aside, I cannot help myself in commenting on the overall performance of our favorite trade for 2016 – spoos and blues. It held up amazingly well in the turmoil of January/February, and obviously the currency peace agreement has been a huge boost to its recent performance.

I suppose the core of my thinking on spoos and blues for this year was more of a generic idea that Janet always wanted to run the economy hot. If there wasn’t a China excuse, she would have found another “headwind.” That said, right now I suspect her mentors, Arthur Okun and James Tobin, are looking down from Keynesian heaven with big smiles. Good luck trading.” You can follow David on Twitter @zervoscorfu.

Average Corporate Credit Rating Hits 15-year Low

- According to S&P, the average corporate credit rating is BB-, or two notches below investment grade. A 15-year low means this gauge is weaker today than at the height of the financial crisis.

- At work here — beside the raft of energy and commodity-related downgrades — are easy corporate lending conditions, which allow those companies with weaker credit ratings to tap the borrowing market.

- Unfortunately, says S&P, lower-graded issuers seeking to refinance in the coming months are going to find less welcoming conditions. “A recalibrated, smaller and more conservative lending environment, where restricted capital market access will enable lenders to better dictate terms and conditions, could prompt liquidity challenges, accelerate downgrades, and ultimately lead to a spike in defaults.”

Trade Signals – Nearing Extreme Optimism

Recall the extreme level of investor pessimism of just six weeks ago. In fact, extreme negative investor sentiment readings were the norm last November through February. I’ve been suggesting since December that extreme pessimism was short-term bullish for equities. From the depth of extreme pessimism (ST bullish), we are now nearing extreme optimism (ST bearish), which limits the upside. Further, the market is also at important technical resistance. Should be running out of steam. We’ll see.

This week, you’ll see in the Trade Signals section below that the 13/34-Week Moving Average trend chart is nearing a bullish cross. This would suggest a heathier longer-term trend environment for stocks. My favorite long-term (“weight of evidence”) indicator is the CMG Ned Davis Research Large Cap Momentum Indicator – it remains in a neutral or “sell” signal. Our CMG Opportunistic All Asset Strategy continues to see a risk-on environment with trades over the last two months favoring more equity-oriented ETFs.

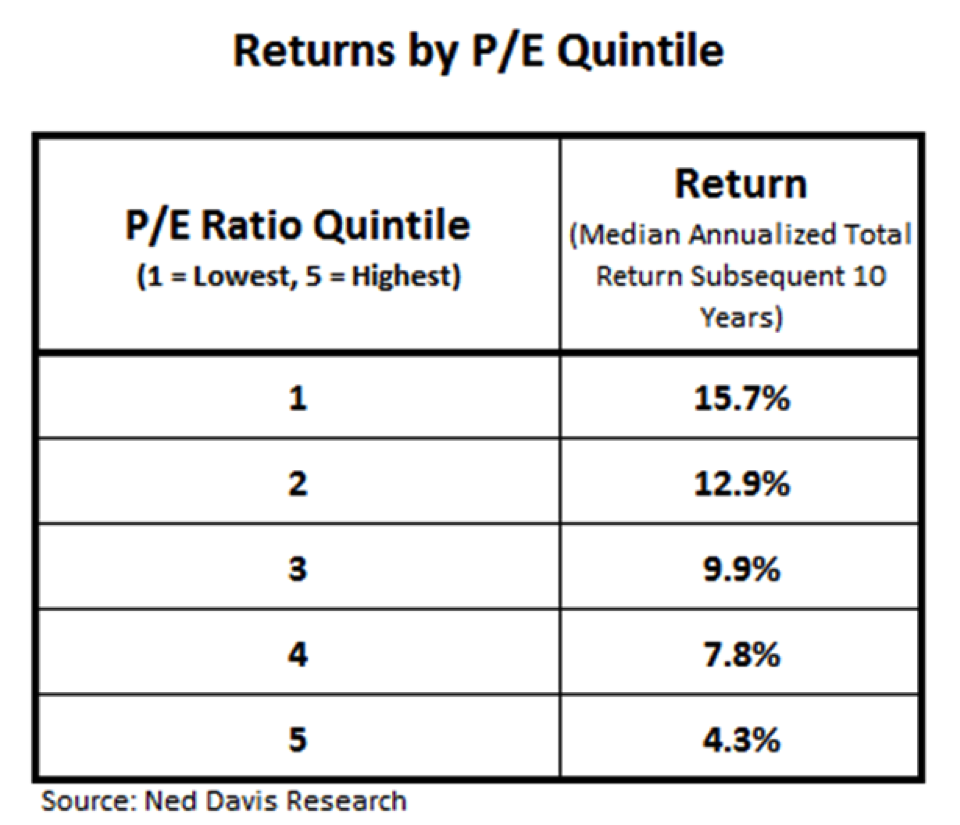

I’m often asked how much one should put into any particular asset class or strategy. My thinking around overall portfolio structure follows. Ultimately, portfolios are a combination of various different risks. I believe how much we allocate to equities should be based upon the current level of valuations. Overweight when forward returns are high (low valuation readings) and underweight and hedge when forward return probabilities are low (high valuations – like today):

Here are the actual median annual returns 1926 through 2014:

Here are a few select periods of time (note the current median P/E today is 22):

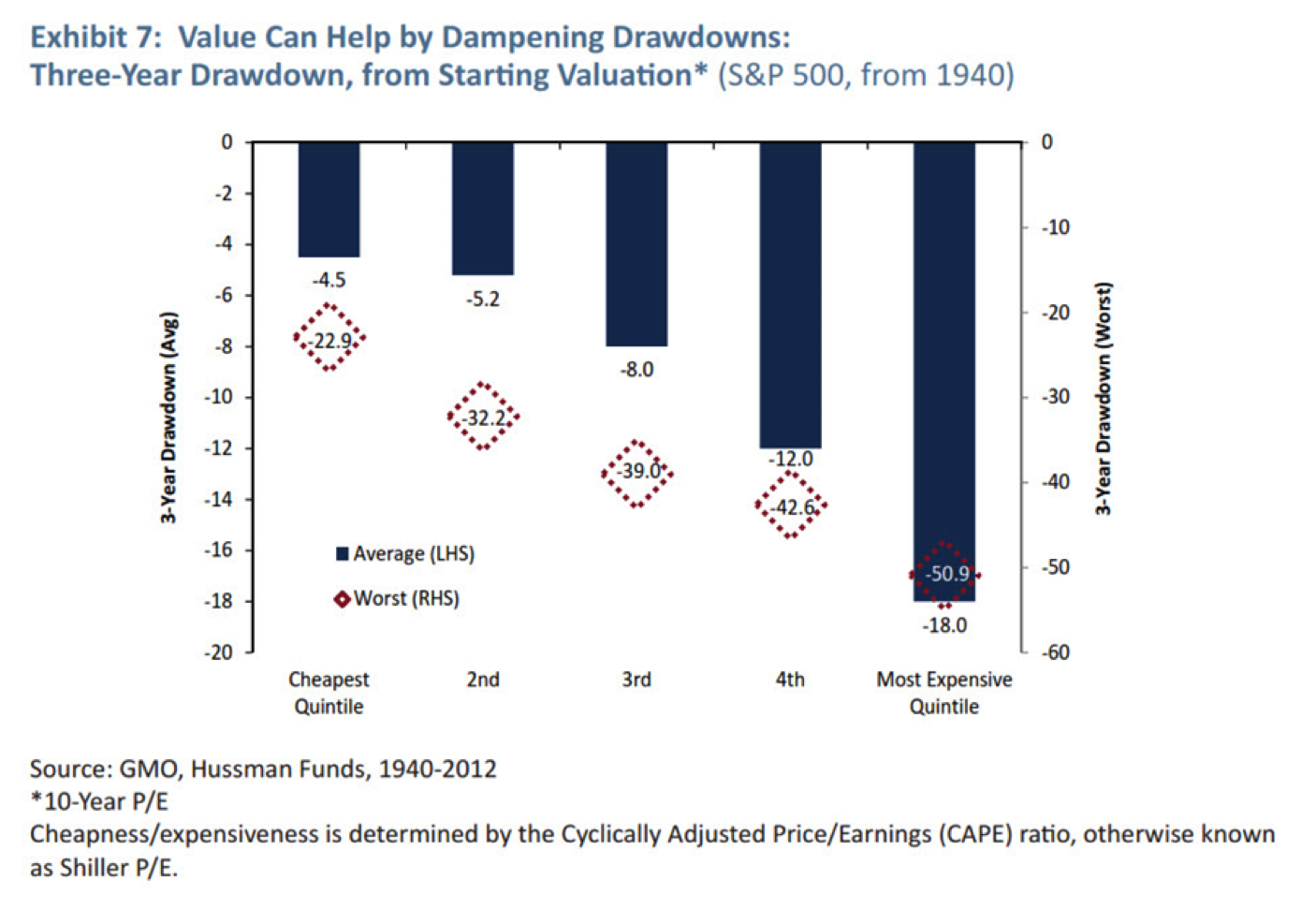

Finally, note that risk is higher when the market is richly priced (average declines and worst declines – next chart, “most expensive”):

My current portfolio weighting preference remains 30% equites (but hedged), 30% fixed income and 40% to liquid alternatives (defined as anything other than traditional buy-and-hold: think tactical, managed futures, global macro, long/short, REITs, MLPs, gold, etc.). Equity valuations remain high. We are in the most expensive median P/E category (“quintile 5”) with a median P/E reading near 22.

Rallies present opportunity to establish or reset hedges. With bullish pessimism nearing extreme and valuations high, now may be a good time. I favor out-of-the-money put options on liquid ETFs, such as SPY. Talk with your advisor to learn more – I also have a few links below to the Chicago Board of Options Exchange).

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Following are the most recent Trade Signals:

Equity Trade Signals:

- CMG Ned Davis Research (NDR) Large Cap Momentum Index: Sell Signal – Bearish for Equities

- Long-term Trend (13/34-Week EMA) on the S&P 500®Index: Sell Signal – Bearish for Equities

- Volume Demand is greater than Volume Supply: Sell Signal – Bearish for Equities

- NDR Big Mo: See note below (active signal: buy signal on 3-4-16 at 1999.99).

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Neutral reading (short-term Bullish for Equities)

- Daily Trading Sentiment Composite: Neutral reading (short-term Neutral for Equities)

Fixed Income Trade Signals:

- Zweig Bond Model: Buy Signal

- High-Yield Model: Buy Signal

Economic Indicators:

- Don’t Fight the Tape or the Fed: Indicator Reading = +1 (Bullish for Equities)

- Global Recession Watch Indicator – High Global Recession Risk

- U.S. Recession Watch Indicator – Low U.S. Recession Risk

(S&P 500® Index monthly declines of -4.8% or greater below its five-month smoothing (MA) signaled recession 79% of the time: 1948 – Present). Data is updated each month end.)

Gold:

- 13-week vs. 34-week exponential moving average: Buy Signal – Bullish for Gold

Tactical — CMG Opportunistic All Asset Strategy (update):

- Relative Strength Leadership Trends: Overall, we are seeing a risk-on environment – a movement away from bonds and into equities. Relative strength in Latin America and Emerging Markets. Our gold position traded into a materials ETF late last week. Approximately 45% is allocated to fixed income ETFs and 55% equity-oriented ETFs (17% of which is international exposure).

Following is a more detailed review of the above Trade Signals (click next link).

Here is a link to the Trade Signals blog page.

Personal Note

I writing from San Francisco, the weather is beautiful and so is the city. Love it here. Susan and I arrived late Tuesday evening, we woke early and walked down to the Ferry Building to grab a coffee. That place has meaning for me. As we neared the building, I started to get a little emotional and said a prayer for my friend and mentor Stephen Mittel. Stephen was a founding partner of Montgomery Securities and hired me in 1982 as their first intern. Basically it was sit, listen, learn and fetch the lunches and coffees. My friend passed almost three years ago.

The Ferry Building houses a number of hedge fund managers and is where Stephen ran his own hedge fund. I owe everything to him and his east coast friend John Ray. They helped me land my first job at Merrill Lynch. I was a kid on an institutional (we covered large pensions, endowments and funds) options trading desk in Philadelphia. Frankly, I knew little about the markets and even less about options. They both wrapped me under their wings and though they may not know it – they continue to help me fly today. Grateful! Steven, you are missed!

A long weekend awaits. Susan and I are going to take in the city and do some hiking and, of course, seek some great food and wine. More fun follows. A few days of skiing in Colorado early next week with my boys, a few meetings in Denver and a tour of UC-Boulder for son Matthew and home on Thursday. I’m really excited for a few days off.

I will be in NYC on April 5 and 6 for a conference and several media interviews. Trips to Chicago and Dallas follow in May.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Hope you find some downtime this weekend. And here is a toast to you and the mentors who helped you fly. And a toast to your beautiful family this Easter weekend.

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History:

Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Following are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group

© CMG Capital Management Group