The financial markets reacted strongly to the Fed policy statement. However, the announcement, the Fed’s revised economic projections, and Yellen’s press conference contained absolutely no surprises (at least for anybody paying attention).

The Federal Open Market Committee left short-term interest rates unchanged, as anticipated. Investors often focus on the changes in the wording of the policy statement, and there seemed to be something for everybody. The FOMC noted that“economic activity has been expanding at a moderate pace despite the global economic and financial developments of recent months.” The FOMC recognized that the job market has strengthened further and that inflation has picked up, but also noted weakness in business fixed investment and exports. The FOMC indicated that“global economic and financial developments continue to pose risks,” but in her post-meeting press conference, Chair Yellen said officials believe that the risks to the growth outlook “have diminished.”

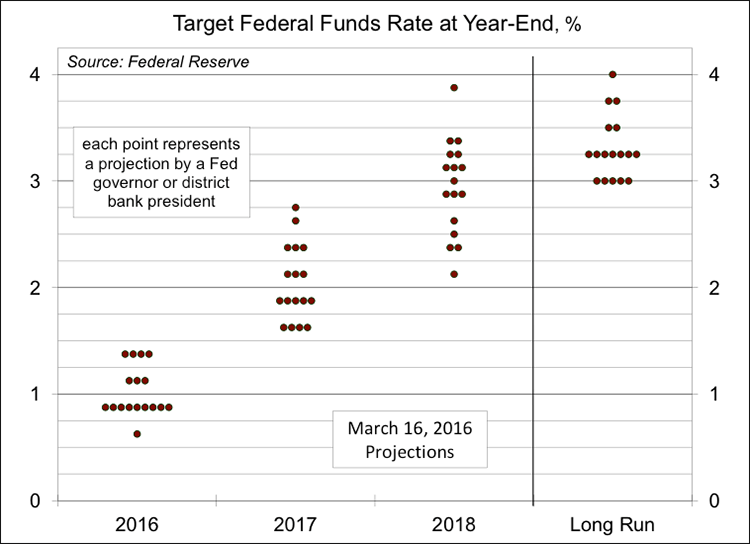

As expected, the dots in the dot plot drifted a little lower. The five Fed governors (note that two nominees have been stuck in the Senate Banking Committee, one since July, the other since January 2015) and 12 district bank presidents expect at least one rate hike this year. In fact, Kansas City Fed President Esther George formally dissented in favor of a 25-basis-point hike at the March 15-16 meeting. Note that each dot is an expectation of a senior Fed official and there is considerable uncertainty around each dot. The dots provide a general sense of what officials anticipate. In the policy statement, and emphasized by Yellen in her press conference, “the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.” In other words, the Fed is still data-dependent.

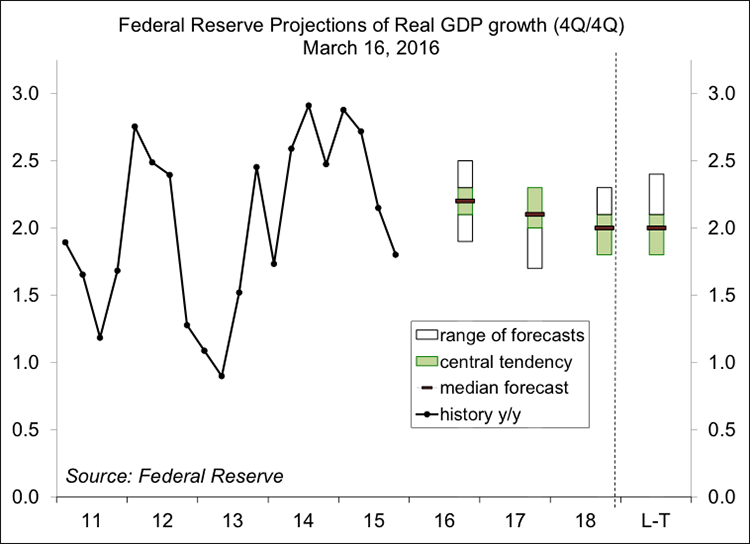

Fed officials’ economic forecasts were not much different from the projections made in December. The forecast of 2016 GDP growth was slightly lower (+2.2% vs. +2.4%), while inflation is expected to be lower (1.2%, vs. 1.6%, reflecting the drop in oil and other commodity prices earlier this year. The estimate of core inflation remained at 1.6%.

The primary drivers of Fed policy are the job market and the inflation outlook. Most indicators suggest that the job market is getting tighter. In fact, the pace of growth in nonfarm payrolls can be expected to slow as it becomes more difficult for firms to find qualified workers. The unemployment rate for college graduates was 2.5% in February (vs. 2.7% a year ago). For high school dropouts, the rate was 7.3% (vs. 9.4% a year ago).

Financial conditions were somewhat tighter in early 2016, which contributed to a more cautious outlook for Fed policymakers. However, Yellen noted in her press conference that financial conditions “have improved notably more recently.” Contrary to what is being reported in the financial press, the Fed policy meeting results were not the catalyst for market action. Rather, earlier fear was simply way overdone.