“So what do we do? Anything. Something. So long as we just don’t sit there. If we screw it up, start over. Try something else. If we wait until we’ve satisfied all the uncertainties, it may be too late.” – Lee Iacocca

“This is the persistent tendency of men to see only the immediate effects of a given policy, or its effects only on a special group, and to neglect to inquire what the long-run effects of that policy will be not only on that special group but on all groups. It is the fallacy of overlooking secondary consequences.” – Henry Hazlitt, Economist

It is the fallacy of overlooking secondary consequences that is keeping me up at night. Try telling that one to your spouse.

“Draghi and the ECB announced that they will start a series of targeted longer-term refinancing operations (TLTRO). The first will occur in June 2016. The term will be four years. The cost of this borrowing by a bank is likely to be a zero interest rate. But under certain conditions, it will be at the negative policy rate. Thus the central bank will be paying the commercial bank to borrow from it.

Imagine what would happen in the United States if the Federal Reserve structured a program so that any bank, whether Bank of America or your local community bank, were to be paid by the Fed when that bank borrowed from the Fed and used the funds to make loans to you or to buy assets in the market.” – David Kotok, Cumberland Advisors

David added, “This is a massively expanded stimulus program. It has extremely bullish implications for financial assets and for asset prices in Europe. And because of its size and lengthy term, it is a bullish force for the entire world. We expect other NIRP jurisdictions to use their version of this model. Keep a sharp eye on Japan’s next move deeper into NIRP.”

NIRP stands for Negative Interest Rate Policy. On its own it is a deflationary policy that, I believe, is ill-designed to help us exit the current excessive debt, global deflationary mess we find ourselves in.

Now look at them yo-yos that’s the way you do it

You play the guitar on the M.T.V.

That ain’t workin’ that’s the way you do it

Money for nothin’ and your chicks for free.

Dire Straits – Money For Nothing Lyrics

Banks can borrow for nothing (0%), expand their loan book by 2.5% (by the end of January 2018) and get an extra 40 bps kicker from the ECB. Get your “chicks for free”. Ok, maybe not “chicks” but certainly “money for nothing”. What they are not saying is that the banks are in trouble. Let’s hope the banks can find some qualified and motivated borrowers.

This next quote pretty much sums it all up for me, “In the last three years plus, central banks have had little choice but to do the unsustainable in order to sustain the unsustainable until others do the sustainable in order to restore sustainability.” – Mohamed A. El-Erian, The Only Game in Town: Central Banks, Instability and Avoiding the Next Collapse (Random House, 2016)

What does this mean? I explained it to someone on our research team this way: It’s like you have a shoulder issue. You go to the doc and get a cortisone shot. Perfect, you feel good again. Six months go by and the pain is back. Another shot, another short-term fix. You do it again until finally the doc tells you she’s done all she can do for you. All that cortisone is really bad for your system in the long term. You need to go to a different doctor, a surgeon, who has the tools to fix the structural problem in your shoulder.

El-Erian calls it a handoff: from the Fed (injecting the juice) to our elected officials (who have the power to implement structural reform). I.e.: Individual and corporate tax reform, U.S. foreign profit dollar repatriation, grand infrastructure projects (aged bridges, natural gas pipes, highways, technology) and entitlement reform/repair (we are nearing a breaking point). Simply, policies that stimulate growth. This requires action.

The problem is that the authorities who have the ability to fix the problem don’t seem to be motivated to get to work. Power struggle gridlock. At some point, they’ll get motivated but it might take another financial crisis to wake them up. This has to happen in Europe, Japan and China as well. Debt is a mess everywhere. See this study from McKinsey “Debt and Not Much Deleveraging“.

Are global central banks nearing the “unsustainable?” No one knows for sure. Stay alert and expect the unexpected. Is ZIRP, QEs 1, 2 and 3, TARP, LTRO, NIRP and coming QE4 (helicopter money) working? Going to work? My two cents is that we have a very long way to go.

Buying government and now corporate bonds. What are we enabling? Debt has not come down. What are we messaging to corporate fiduciaries, bank prop desks, levered investors? What did low rates and no-doc mortgages do for the housing market. Who are we helping or hurting with repressed interest rates? Keep your guard up. These are highly unusual times. Stay alert and expect the unexpected.

Equity market valuations remain high and the bull market is aged. Hedge that equity exposure, broadly diversify and overweight to non-directionally dependent strategies. I continue to favor a 30/30/40 (equities, fixed income and liquid alternatives) portfolio mix and hedge that equity exposure. We can change the tilts to overweight equities and remove hedges when forward return potential is high (at which point valuations will be lower and attractive).

To that end, this week you’ll find a great equity market chart that shows us what the forward S&P 500 Index returns are likely to be based on the percentage of household equity ownership. It may help guide your thinking as to when to become more aggressive again.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- All ‘Bout That Fed, ‘Bout That Fed

- What Henry Hazlitt Can Teach Us About Inflation, by James Grant

- Charts That Matter – Forward 10-year Annualized Return 3-4% for Equities

- Trade Signals – “Aged”: The Average Bull Market Lasts 59 Months, This One is Now 84 Months Old

All ‘Bout That Fed, ‘Bout That Fed

Following are several pieces I found interesting – comments on the Fed:

Peter Boockvar, from the Lindsey Group, prior to the Fed’s Wednesday FOMC meeting wrote:

If the Fed was TRULY dependent on the data, they would be raising interest rates TODAY. The six-month job gain average is 235k, the unemployment rate is right at the Fed’s long-term forecast, the core PCE y/o/y rate gain of 1.7% is one-tenth above the Fed’s year-end forecast, the S&P 500 is just 5% from its record high, the US dollar is at the same level it was about one year ago as negative rates from the BoJ and ECB has stopped working in weakening their currencies, oil prices are up 15% from the last Fed meeting, the CRB food stuff index is at a three-month high and the Journal of Commerce index of 19 industrial materials is at a 4½-month high. Also, as the Fed likes to talk about inflation expectations, the 10-year breakeven at 1.50%, the same level it was at in August and the same spot it was at when the Fed hiked rates in December. It is not until September however that the Fed Funds futures market is 100% confident that under the current circumstances they will raise again. We are at 64% for June.

Assuming the Fed doesn’t want to shock the market, they won’t raise today (and they didn’t as we now know) as no one expects it because the Fed seems to be worried about everything else (China and international developments, mediocre US growth, the prospect of another round of a tightening of financial conditions, their own shadow, etc…). William McChesney Martin, the Chairman of the Fed from 1951 to 1970 once said this in a speech, “The idea that the business cycle can be altogether abolished seems to me as fanciful as the notion that the law of supply and demand can be repealed.” He said that in 1955.

And this from Danielle DiMartino, QE Program – An Embarrassment of Stitches

“And so we hear the latest, that the Chinese government will launch its answer to the U.S. TARP program, wherein Chinese commercial banks swap out bad debts to the government in exchange for equity in said bank. Reported non-performing Chinese bank loans rose to $614 billion in 2015, a decade high, even as their economic growth slumped to a 25-year low. Of course, the aim of the package is identical to that of all stimulus measures launched since 2008 — to spur yet more lending to lift economic growth. More and more yet of the same.

Which brings us to the European Central Bank (ECB), which added non-financial corporate bonds to the menu of fixed income instruments it can buy to achieve its goal of flooding the markets with 80 billion in euros every month so as to…drum roll, please…incentive, more lending. It seems that there were simply not enough sovereign bonds and asset-backed securities to get the job done, and that’s before the ECB expanded its QE program from 60 billion euros a month before last Thursday’s meeting.

No doubt, with 900 billion euros outstanding, the ECB has an appreciably large pool of assets at which to aim its buyer-not-beware bazooka. A gut check, though, should prompt the question as to why European policymakers are so keen to increase their own QE program when the effort has produced so few results everywhere else it’s been attempted.

A fine point: at roughly $50 billion in outstanding bonds, life insurers top the list of eligible targets for ECB purchases. Just so we understand each other, ECB President Mario Draghi envisions buying non-financial corporate bonds in the sector most damaged by the policies he’s deployed since vowing to do whatever it takes to reignite inflation via record low interest rates. Recall that low interest rates are the bane of insurance companies that depend on reasonably high interest rates to make good on the long-term promises they’ve made to those who pay stiff premiums in exchange for those promises.”

Ok, you get the picture. Debt is a mess pretty much everywhere and is a drag on global growth. By the way, I think the central banks will ultimately create inflation. But is might be in a stagflation environment.

What Henry Hazlitt Can Teach Us About Inflation in 2014, by James Grant

“The bad economist sees only what immediately strikes the eye; the good economist also looks beyond. The bad economist sees only the direct consequences of a proposed course; the good economist looks also at the longer and indirect consequences. The bad economist sees only what the effect of a given policy has been or will be on one particular group; the good economist inquires also what the effect of the policy will be on all groups.” (Henry Hazlitt)

I mentioned Henry Hazlitt in a June 2014 On My Radar.

Here are several highlights from the piece:

- “In 1946, as now, the government held up the threat of deflation to justify a policy of ultra-low low interest rates and easy money. Now ladies, and gentlemen, I have devoted thirty-one years of my life to writing about interest rates, and I have to tell you that I can’t see them anymore. They’re tiny. And so they were in 1946. Then, as now, the Fed had been conscripted into the government’s financial service. Just as it does today, the central bank pushed money-market interest rates virtually to zero and longer-dated Treasury securities to less than 3 percent. Just as it does today, the Fed had its thumb on the scales of finance.”

- “If interest rates were artificially low, it would follow that prevailing investment values are artificially high. I contend that they are, and you may or may not agree. But you must allow the observation that we live in a kind of valuation hall of mirrors. We don’t exactly know where our markets should trade, because we don’t know where interest rates would be in the absence of central-bank manipulation. Natural interest rates — free-range, organic and sustainable — are what we need. Hot-house interest rates — the government’s puny, genetically modified kind — are the ones we have.”

- “When interest rates are kept arbitrarily low by government policy, the effect must be inflationary,” he wrote. “In the first place, interest rates cannot be kept artificially low, except by inflation. The real or natural rate of interest is the rate that would be established if the supply and demand for real capital were in equilibrium. The actual money interest rate can only be kept below the natural rate by pumping new money into the economic system. This new money and new credit add to the apparent supply of new capital just as the judicious addition of water add to the apparent supply of real milk.”

- Hazlitt concluded that “the money rate of interest can be kept below the real rate of interest only as long as the supply of new money exceeds the supply of new real capital. Excessively low interest rates are inflationary in the second place because they give an excessive stimulation to the volume of borrowing.”

- “Why, I could quote those perfectly formed sentences in Grant’s today (and I believe I just might). They’re as timely now as they were during the administration of Harry S. Truman. The effective federal funds rate has been zero for well-nigh six years.”

Well-nigh almost eight years now…

Charts That Matter: Forward 10-year Annualized Return 3-4% for Equities

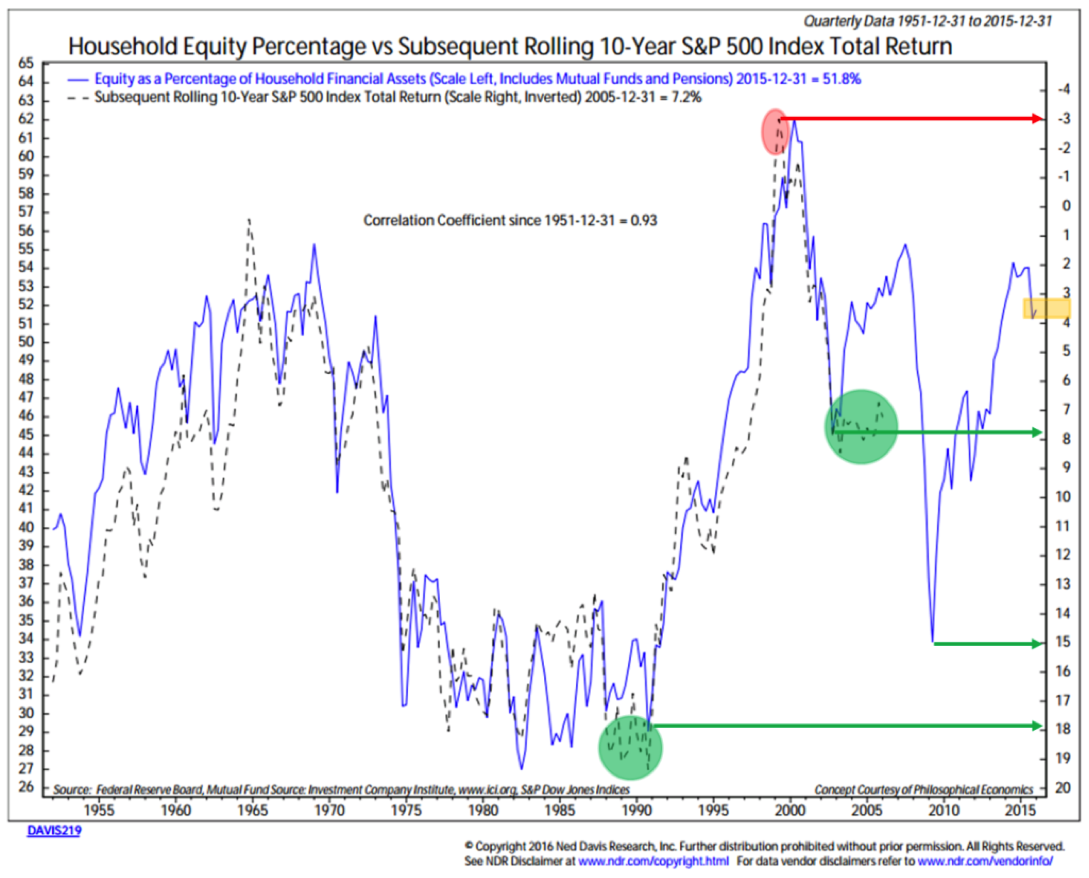

- Household Equity Percentage vs. Subsequent Rolling 10-Year S&P 500 Index TR

Early each month, I share with you the most recent median P/E data. You can see the early March post on valuations here.

This next chart too is amazingly accurate in assessing the probable returns to come over the next ten years. It looks at the percentage of household equity ownership. Think of it this way, when investors are heavily committed in their portfolios to equities, much of the buying power (that may drive equity prices higher) is already in the game. The blue line measures the equity percentage and the dotted line shows what the annualized return was ten years later. The red circle shows the extremely high equity exposure in 2000 and the dotted line within the circle shows what the actual annualized return turned out to be.

The green circles and the green arrows show when equity ownership was low and returns high. The yellow rectangle shows where we are in terms of equity ownership most recently and tells us to expect 3.75% annualized returns over the coming ten years.

Note how closely the actual returns, the dotted line, tracks the percentage ownership line with a high 0.93 correlation.

- BofA Merrill Lynch Global Liquidity Tracker (red line):

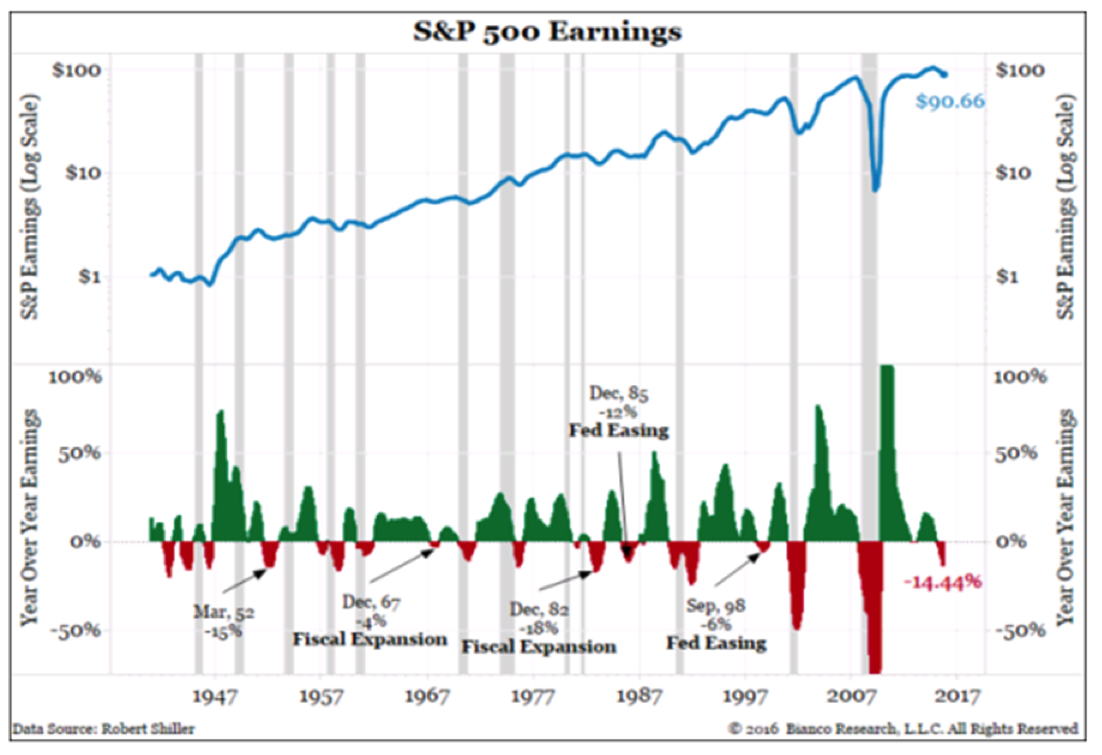

- Earnings rolling over?

Recessions are highlighted in gray. A richly-priced equity market and declining earnings do not mix well. Risk is high.

- Core CPI

Strength in Core CPI Inflation (green line in next chart) – remember that the Fed is targeting inflation at 2% (CPI is at 1%, Core CPI is now at 2.3%). Note the high correlation between the two lines.

Core CPI is rising: Nothing to worry about just yet, but let’s keep a close eye on this.

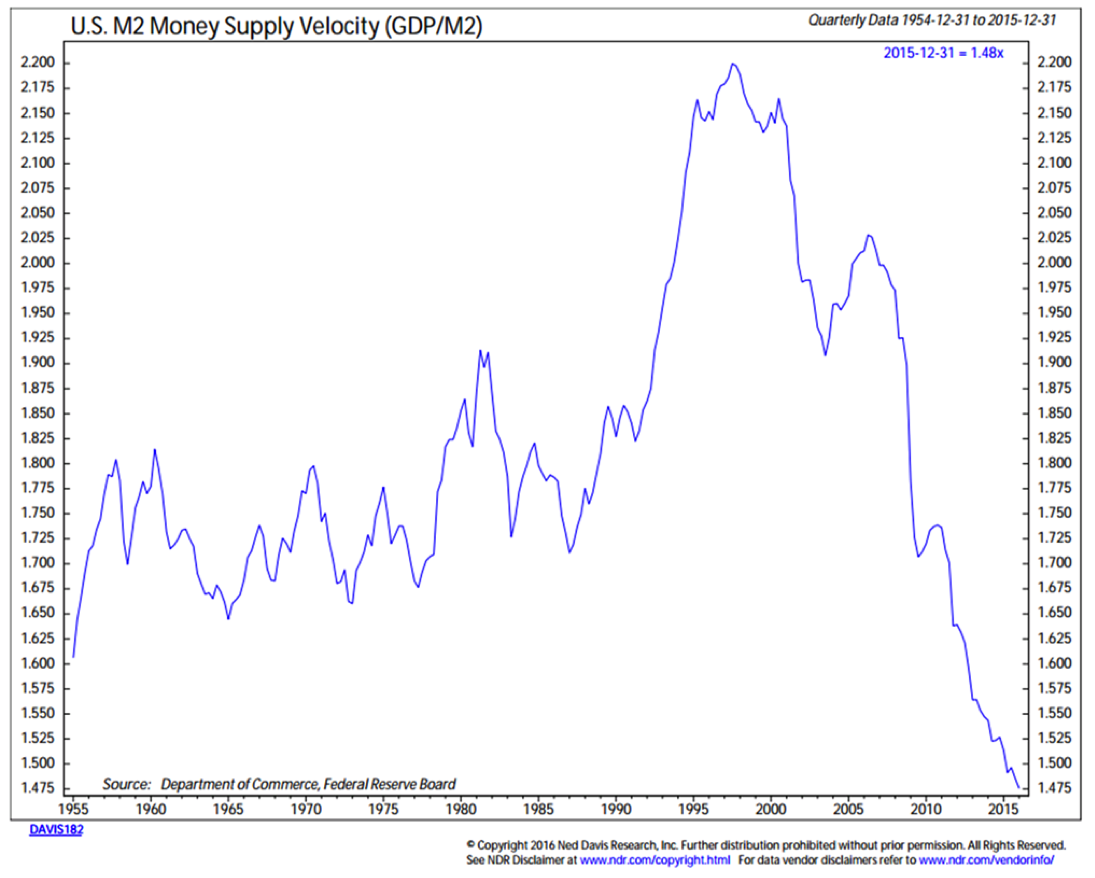

- Money Velocity

Note – at all-time lows. This should cause concern.

- The Shrinking Middle Class

Hazlitt suggests that, “the whole of economics can be reduced to a single lesson, and that lesson can be reduced to a single sentence. The art of economics consists in looking not merely at the immediate but at the longer effects of any act or policy; it consists in tracing the consequences of that policy not merely for one group but for all groups.”

Here is a link to Henry Hazlitt’s book, Economics in ONE Lesson. An oldie but a goodie.

Trade Signals – “Aged”: The Average Bull Market Lasts 59 Months, This One is Now 84 Months Old

Equity Trade Signals:

- CMG Ned Davis Research (NDR) Large Cap Momentum Index: Sell Signal – Bearish for Equities

- Long-term Trend (13/34-Week EMA) on the S&P 500®Index: Sell Signal – Bearish for Equities

- Volume Demand is greater than Volume Supply: Sell Signal – Bearish for Equities

- NDR Big Mo: See note below (active signal: buy signal on 3-4-16 at 1999.99).

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Neutral reading (short-term Bullish for Equities)

- Daily Trading Sentiment Composite: Neutral reading (short-term Neutral for Equities)

Fixed Income Trade Signals:

- Zweig Bond Model: Buy Signal

- High-Yield Model: Buy Signal

Economic Indicators:

- Don’t Fight the Tape or the Fed: Indicator Reading = +1 (Bullish for Equities)

- Global Recession Watch Indicator – High Global Recession Risk

- U.S. Recession Watch Indicator – Low U.S. Recession Risk

(S&P 500® Index monthly declines of -4.8% or greater below its five-month smoothing (MA) signaled recession 79% of the time: 1948 – Present). Data is updated each month end.)

Gold:

- 13-week vs. 34-week exponential moving average: Buy Signal – Bullish for Gold

Tactical — CMG Opportunistic All Asset Strategy (update):

- Relative Strength Leadership Trends: We are seeing relative strength in International Equities and several Emerging Markets. Utilities, Gold and Telecom continue to show strong relative strength. Fixed Income has held top ranking in a number of our models over the last number of months; however, we are seeing a shift towards sector-oriented funds/ETFs, equities in general and International Equity exposure.

Here is a link to the Trade Signals blog page.

Personal Note

We in the Blumenthal home love soccer. Most Saturday mornings, Susan makes the coffee and asks me to see what European soccer games are on TV. The boys wake up later and usually join us. She continues to coach and all of our kids enjoy the game. I love it. And life is great.

Our Philadelphia Union plays its home opener this Sunday afternoon. Excitement has been building at the dinner table, talk of new players and of course we are hoping for a successful year. Chickie’s and Pete’s chicken fingers or a Philly cheesesteak, crab fries and a cold Victory Hop Devil beer awaits. Don’t tell my doctor. Hoping I’m not overlooking “secondary consequences”.

Wishing a fun filled weekend to you and your beautiful family!

I’ll be writing from San Francisco next week. Several meetings and some time to enjoy the city. Meetings in Denver late March then business and media in NYC on April 6. Chicago and Dallas (Mauldin’s Strategic Investment Conference) follow in May.

Thanks for reading.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History:

Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Following are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group

© CMG Capital Management Group