The story goes that tighter Fed policy has strengthened the dollar, the stronger dollar has led to lower prices of oil and other commodities, and the drop in oil prices contributed to stock market weakness in January and February. However, stock market movements cannot be attributed wholly to the price of oil, the price of oil cannot by tied completely to the dollar, and the dollar’s strength has not been due entirely to monetary policy. Examining these links more closely may provide some insight into where we are heading in the months ahead.

Exchange rates are determined by supply and demand. Currencies adjust to balance trade and capital flows. In the short run, relative central bank polices are an important factor. All else equal, the dollar should strengthen as the Federal Reserve moves to tighten and other central banks move to ease. The question is how much. The Fed has raised short-term interest rates by only 25 basis point and officials have signaled that policy normalization is expected to occur gradually.

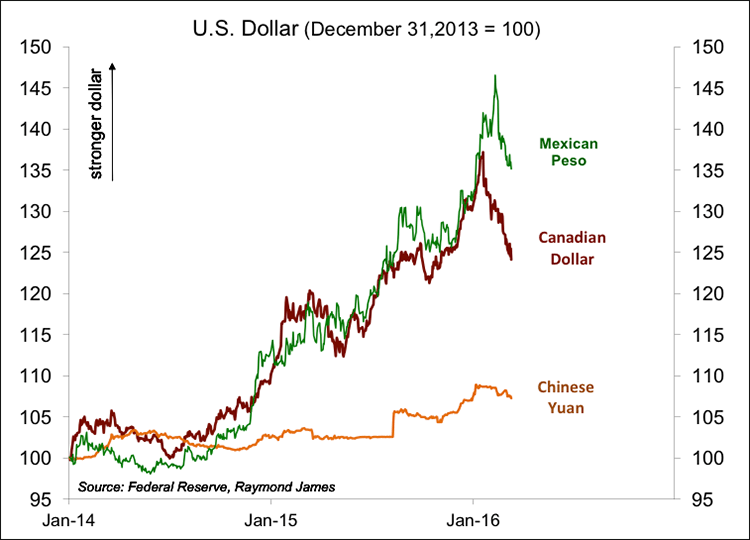

Much of the dollar strength has been reflective of global capital flows. Money has poured out of emerging economies. The U.S. has remained the safe haven. Such moves can be self-reinforcing and can go on for too long. Currency moves tend to overshoot. Consider the currencies of our two biggest trading partners, Canada and Mexico. From mid-2014, the Canadian dollar had depreciated 35% against the U.S. dollar and the Mexican peso had fallen 45%. These are huge moves and hard to justify by the fundamentals alone. Anecdotally, U.S. firms exporting to Canada and Mexico reported more serious restraints in January and February. The dollar has begun to reverse direction in recent weeks and may unwind further.

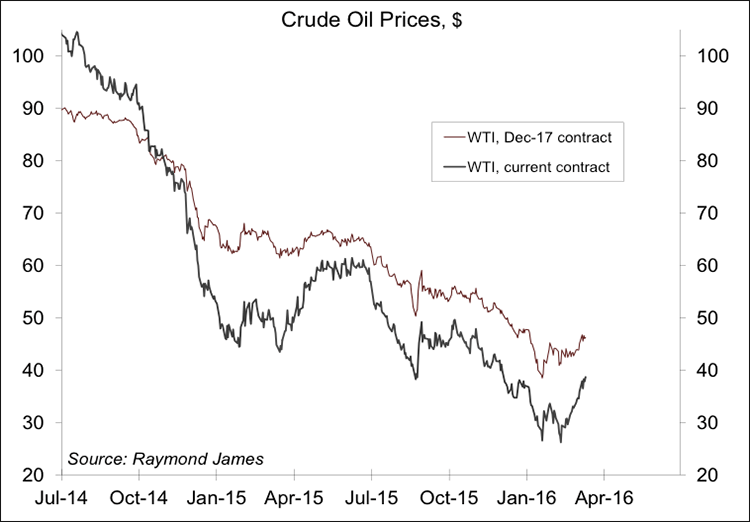

The dollar is only one factor in commodity prices (and no, it simply does not matter that commodities are priced in dollars). The trade-weighted dollar has risen about 20% since mid-2014. The price of oil fell by 70%. The price elasticities of the demand and supply of oil are very inelastic in the short term. That means that it doesn’t take much of a shift in supply or demand to have a very large impact on the price. Increased supply and decreased demand combined to send oil prices lower. The drop in oil prices should pave the way for an eventual rebound. Lower prices encourage more consumption and discourage oil exploration. In 2014, OPEC signaled that it wanted to put a lot of global fracking out of business. That means pushing oil prices lower and keeping them low for a long time. OPEC was clearly more successful than it intended to be, largely because the global economy was softer than anticipated.

The stock market and the price of oil are well correlated. That’s because they both react to common factors, including the overall strength of the economy. However, in recent weeks, the stock market and the price of oil have moved in tighter daily lockstep. What’s odd is that daily movements in the price of oil have been driven largely by supply issues (will there be cuts in production?) and not on demand news. That makes no sense. Perhaps a significant portion of programed trading has been built to recognize the long-term correlation between stock and oil, and that estimated correlation has now been hard-wired in.

The one common thread through this discussion is that the rest of the world economy is soft and the U.S. is relatively strong. Being more domestically oriented, the U.S. economy should be able to resist the pull of global softness. More importantly, the rest of the world should pick up at some point. There will be bottom fishing, of course, but emerging economies will begin to look a little more attractive at some point and capital flows are likely to turn (and may already have).

The U.S. consumer is in good shape. However, business caution is likely to continue, with perhaps some nervousness about the presidential election and what the thrust of the new administration will be in early 2017.