Last week’s mention of the great Art Cashin sent a number of emails my way. The one that touched me most was from Richard who worked for Paine Webber from 1974 to 1987. Back then every broker had a small speaker on his or her desk. We in the industry know it as the “squawk” box.

That early technology made Art available to all the reps all day, every day. Richard wrote me that Art would close each day saying,

“You know the rules, take care of yourself, put some joy into your life and all those around you that you think deserve it, and never, NEVER pass up a chance to kiss someone you love!”

Richard added, “I look forward to his wisdom being accessible once again.” Pretty great.

I had dinner with Art several years ago, along with my good friend John Mauldin. Art is as humble and likeable as you see him on TV. I wonder if he has any idea how many people he has touched. Shoot me an email if you’d like me to forward your name and email address to Art.

The big news this week is Mario Draghi and the ECB. Let’s look at that, but first let’s see if we can take a 30,000 foot view at the problem and how the markets might behave going forward.

Collectively, the number one global problem is DEBT. Can we grow our collective incomes in a healthy way that we are able to cover our debts? For long periods of time, debt helps to fuel growth but at some point it becomes too big. Think in terms of what you earn and what you have to spend after you pay your bills. When you have too much debt and more of your income goes to pay off your debt, you have less to spend on other things. Your economy slows.

On a larger scale, this is what is happening to economies most everywhere – Japan, U.S., Europe and China. So, in steps the central banks to goose the system. Step one, central banks lower rates. However, when rates go to zero, central banks have lost the power so they move to step two. Step two is quantitative easing “QE”, also known as large scale asset purchases. The Fed did this in the last recession and again recently. The ECB is doing it now and Japan on and off since 1991.

Step two causes asset prices to rise, but they then reach a point when valuations grow too rich and forward return potential is low. Steps one and two hope to activate our collective animal spending spirits. We feel wealthier so we spend…so the theory goes. After you’ve done step two several times, subsequent moves are less powerful. As Ray Dailo says in a recent Bloomberg interview (link below), and I mentioned several months ago, the central banks reach a point where they are “pushing on a string”.

So what comes next? We are likely moving to step 3, or “helicopter money”. This amounts to direct government spending to stimulate the economy. The idea is to force spending since the private sector isn’t doing enough. Who does that spending? The government. Print and spend.

I share some bullet point notes from the Dalio interview. Cutting to the chase, like me, he sees a low return environment (see Stick With the Drill and Expect More Money Printing), slow growth, low inflation and choppier markets for a period of time. He also talks about step 3. But check out the interview and/or my notes (links below).

Steps 1, 2 and 3: The point is that there are a few “bazookas” yet to be fired. It was all about the European Central Bank this week. Janet Yellen and the Fed step to center stage next week. One giveth and one taketh away? We’ll see. How it plays out remains uncertain though I have my thoughts.

Front of mind is that debt on top of too much debt won’t work. Zero to negative interest rates destroy price discovery and it hurts retiree income (further slows the economy). If 75% of the investable assets are going to be in the hands of pre-retirees and retirees (per Blackrock) by 2020, I just don’t think they are looking to spend more. Animal spirits? Right. Their income is being squeezed. Pensions, significantly underfunded, need 7% to 8%. No chance unless they meaningfully overweight to non-constrained alternative strategies (and they are not).

Let’s recognize that we are in a long-term debt cycle. Be aware that this is different than anything you and I have experienced thus far in our lives.

Ok – grab a coffee and let’s dive in. This week’s piece is a quick read.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- The Draghi Bazooka

- Reaction to ECB Announcement

- Ray Dalio – Bloomberg Radio Interview

- Red Ink Rising – China Cannot Escape The Economic Reckoning That A Debt Binge Brings

- Trade Signals – Investor Sentiment Neutral, Bullish on Bonds and Gold

Draghi’s Bazooka

It was all about the European Central Bank this week. Mario Draghi and his ECB lowered rates to -0.40% from -0.30%, increased QE (asset purchases) to €80 billion euros worth of bond purchases each month, which is an increase from the €60 billion euros presently, extended the stimulus until at least March 2017 and announced they will also be buying corporate debt. Negative interest rates, additional QE and for an extended time period. The markets loved it… until they didn’t… until they did.

“Rates will stay low, very low, for a long period of time and well past the horizon of our purchases,” Draghi declared. Kaboom – markets are higher today.

Reaction to ECB Rate Cut

As one blogger put it: This is not capitalism, or a functioning market: this is the end-game of legalized looting and financialization. What’s the value of real estate? If interest rates are pushed negative, then that gooses housing demand, as the cost of interest on a mortgage declines to near-zero in real terms.

What would the value be at 5% mortgage rates? What would the interest rate be in a truly private mortgage market, one that wasn’t dominated by government agencies and central banks? Nobody knows.

Once you lower interest to zero, the market can no longer price the difference between a mal-investment and a sound investment. Price and risk discovery are dead.

Prop up asset bubbles with direct asset purchases, and markets abandon valuations in favor of following the manipulation. Price discovery is dead.

Ray Dalio, Bridgewater Associates – Bloomberg Radio Interview

Thinking back to the squawk box days vs. what we have at our finger tips today is reason to be really grateful. You and I have instant access to some of the brightest minds amongst us. A few key strokes and send.

Bridgewater stewards the world’s largest hedge fund (roughly $155 billion). I’ve always preferred to listen to investors with real money on the line over research providers. There were several things that stood out to me in the interview and I bullet point them for you:

- Over a period of time, productivity matters the most – what you earn and what you have to spend.

- There is a long-term debt cycle.

- When you have too much debt and you can’t service it anymore and when rates go to zero, we have run out of monetary policy #1 and we have to go to #2 (QE) –this happened in recession and again recently.

- QE causes the assets to rise in price and future returns are then low. Now when you’ve done that, the next move is less powerful… pushing on a string.

- Japan was in this spot first (pushing on a string)… rates at zero. Going nowhere and still trying to get 2% inflation.

- Europe is there… rates are slightly positive to negative. So there too interest rates are not going to work… we are pushing on a string in Europe.

- U.S. – we are close to pushing on a string.

- Forward equity returns of about 4%. Some returns, but not much.

- So risk reward is not asymmetric – the bigger risk is on the downside vs. reward on upside.

- We are moving to monetary policy or step #3 (“MP3”) or “helicopter money”. It will not be QE – QE was asset purchases that helped financial institutions but stays in the financial community.

- Going to move to a policy that puts money directly in the hands of spenders. Print and lend directly to spenders… helicopter money.

- The central bank has capacity, legally, to put directly in the hands of spenders. There are a range of ways it can be done.

- These long-term debt cycles come once a lifetime, but in history they have regularly happened.

- May see the Fed raise the Fed Funds Rate up 25 bps or so, but the very next big move is down… we are heading to MP3.

- He believes the Fed is not paying enough attention to the LT debt cycle

- Asset prices correct to a point where the risk premiums come back (SB here: that is when we want to get aggressive on equities).

- Let me be clear, I am not bearish on the stock market. Investors make a choice in investing, cash (0% return), bonds (2%) or stocks (4%).

- When stocks go down, it has a negative wealth effect which has a negative effect on the economy. Problem is the Fed, at zero, doesn’t have the ability to ease. They have to do something else.

- There was a great dialog near the end of the interview. Dalio added, “Are you going to create a good strategic asset allocation portfolio meaning you are not going to go to the betting table and bet against active investors like me? It is not easy to win in the markets. In fact, it is more difficult to win in the markets than competing in the Olympics.”

- Long-term debt cycle is what we need to look at – the Fed is not looking at it.

- Japan is more likely of what our outcome will be – unless we restructure our debt somehow.

- Overall debt is too large. We are at limits of debt relative to the income we produce. Look at individuals and corporations as a country, then as each separate country, then collectively as a world. There is a limitation to how much debt. We can’t borrow more to grow our way out of this. We can’t borrow more that will help us out of the slow growth, low inflation problem.

- We have a low return environment, slow growth, low inflation. Increased difficulty of monetary policy (central banks) working.

- Not expecting anything like 2008. That was a debt crisis. Debts couldn’t get paid. Don’t see a big bang crisis.

- Going to see low returns, relative stagnation.

- Choppier markets for a period of time.

- See more currency volatility.

- Globally there is a tightening of economic activity.

- No one knows exactly what the market range is.

“The way that we succeed is by having thoughtful disagreement” – I liked that quote…“try to find people who are smart and who disagree with your point of view – need independent thinkers. If you can work your way through to get at the right answer…” – amen brother.

Finally, I found this to be highly on point: Dalio doesn’t think it is more difficult for him (Bridgewater) to invest today. The reason is that he doesn’t make systematic investments (i.e., equities for the long-term where a market crash can cause great loss. They have the opportunity to go either way (bet both up and down).

A few days ago marked the 7th anniversary of the bull market. Now in its 84th month, it’s the third longest bull market on record. It’s aged, over-priced and central bank activity is pushing on that string. More that can be done? Sure. We are in the midst of an economic experiment that is, as my father used to say, “not for the faint of heart.”

Put your head phones in and head out for a walk – it’s 20 minutes well spent. Here is the link again: Bloomberg Radio Interview

Red Ink Rising – China Cannot Escape The Economic Reckoning That A Debt Binge Brings

While all eyes are on Mario, the PBOC pulled its own surprise this week. They are changing the way the banks will account for non-performing loans. This may free up billions for new lending.

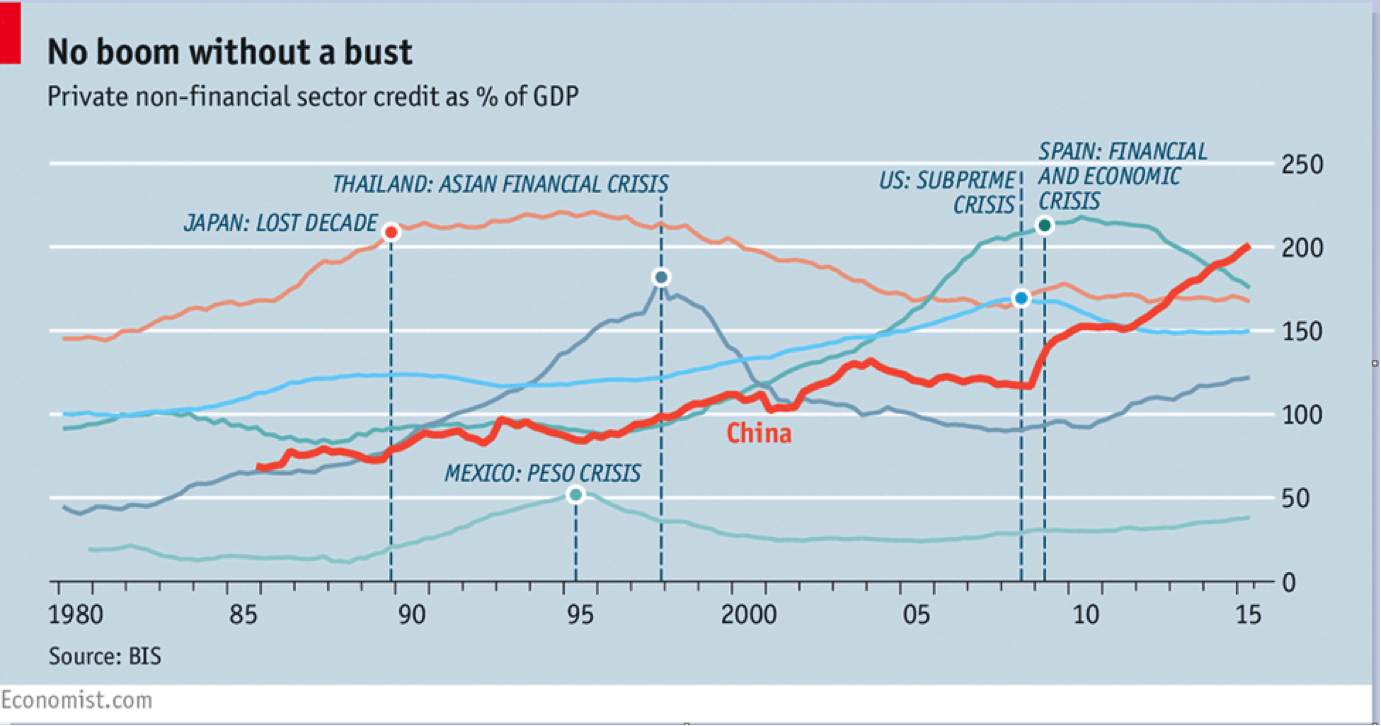

Get those quant goober goggles back out as you look at the next chart. Specifically, the dark orange China line which represents private non-financial sector credit as a % of GDP. Note Japan in 1989 (light orange line) and the U.S. in 2008 (blue line). Income can only grow so fast. Income can only cover so much debt. Is it any wonder we are seeing a global slowdown?

From the piece:

“HOW worrying are China’s debts? They are certainly enormous. At the end of 2015, the country’s total debt reached about 240% of GDP. Private debt, at 200% of GDP, is only slightly lower than it was in Japan at the onset of its lost decades, in 1991, and well above the level in America on the eve of the financial crisis of 2007-08 (see chart). Sooner or later China will have to reduce this pile of debt.

History suggests that the process of deleveraging will be painful, and not just for the Chinese.”

If you want to get a better sense for the headwinds that excess debt creates, this piece from The Economist does a great job. Here.

Trade Signals – Investor Sentiment Neutral, Bullish on Bonds and Gold

S&P 500® Index 1985

By Steve Blumenthal March 9, 2016

Included in this week’s Trade Signals:

Equity Trade Signals:

- CMG Ned Davis Research (NDR) Large Cap Momentum Index: Sell Signal – Bearish for Equities

- Long-term Trend (13/34-Week EMA) on the S&P 500®Index: Sell Signal – Bearish for Equities

- Volume Demand is greater than Volume Supply: Sell Signal – Bearish for Equities

- NDR Big Mo: See note below (active signal: buy signal on 3-4-16 at 1999.99).

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Neutral reading (short-term Bullish for Equities)

- Daily Trading Sentiment Composite: Neutral reading (short-term Neutral for Equities)

Fixed Income Trade Signals:

- Zweig Bond Model: Buy Signal

- High-Yield Model: Buy Signal

Economic Indicators:

- Don’t Fight the Tape or the Fed: Indicator Reading = +1 (Bullish for Equities)

- Global Recession Watch Indicator – High Global Recession Risk

- U.S. Recession Watch Indicator – Low U.S. Recession Risk

(S&P 500® Index monthly declines of -4.8% or greater below its five-month smoothing (MA) signaled recession 79% of the time: 1948 – Present). Data is updated each month end.)

Gold:

- 13-week vs. 34-week exponential moving average: Buy Signal – Bullish for Gold

Tactical — CMG Opportunistic All Asset Strategy (update):

- Relative Strength Leadership Trends: Utilities, Gold, Fixed Income, Muni Bonds and Telecom are showing strong relative strength. We’ve seen an increase in equity exposure with a trade this week out of Fixed Income and into Telecom (approximate 9% weighting).

Here is a link to the Trade Signals blog page.

Personal Note

“Downside hurts much more than upside might give benefit…clients get this.” – Neil Rue, CFA, Managing Director, Pension Consulting Alliance, LLC.

I’m not sure enough investors get this, though I’m sure you do.

To this end, motivated largely by a conversation I had with my Susan, I wrote an educational piece titled, The Merciless Math of Loss. Some time ago she asked me, “If there was one thing you should teach me about investing, what would that be?” I answered that the most important thing every investor should learn is how money compounds over time.

I then asked her, “If your investment account goes down 50% in value, how much do you have to earn to get back to even?” 50%, she answered. I told her that is what most people think. I said look at it this way, “if your account was worth $1,000,000 and you lost 50%, what is it worth?” $500,000, she answered. Then, after that decline, if you gain 50%, what would it be worth? She did the quick math then stopped and simply said, “oh” and added, “you have to tell everyone this”.

Susan is an extremely bright, Cornell University educated, human being. And beautiful! My point is we in the industry may get this, but it can be confusing to our clients who, like me with my electrician, really don’t get this business and further may have desire to know only so much. But they know if they made money over any period of time.

So I wrote the mathematics piece. Lose 20%, you needs a 25% gain to get back to even. Lose 50%, one needs 100% to get back to even. Lose 75%, you need a 300% gain. Again, here is the link to the piece. Please feel free to use the charts that show how devastating loss can be. And we need to teach this stuff to our kids. Ok – I’ll stop.

San Francisco is up next – March 23 and 24 for several meetings. Denver follows in late March and, so far, just Mauldin’s Dallas Conference is on the May calendar.

What a week of weather here in Philadelphia. The weekend looks equally great. A soccer tournament for kid number six and a ski event for kid number three will keep us on the road and I do see a small window to maybe sneak in some golf. My fingers are crossed.

Fire up your grill, grab your favorite drink and “kiss the ones you love the most!”

Wishing you a wonderful weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History:

Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Following are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group

© CMG Capital Management Group