The recent economic data reports have continued to reflect the mix of global softness and domestic strength. The economy has continued to add jobs at a relatively strong pace in early 2016, although the real test for the job market will come over the next few months. The job market is getting tighter and, despite a dip in hourly earnings, wage trends are higher. January trade data, overshadowed by the employment report, suggest a larger drag on GDP growth in 1Q16, but the consumer should carry us through into the second half of the year.

The headline payroll figure is subject to statistical noise and seasonal adjustment uncertainty. Numbers can bounce around from month to month. The impact of noise can be reduced by focusing on the three-month average (for February: +228,000 overall and +224,000 for the private sector). We need to add about 100,000 jobs each month to be consistent with the growth in the working-age population. We can run well beyond that pace currently because we are taking up the slack that was generated during the recession. However, the pace of job growth should slow as the labor market tightens. Many firms are currently reporting difficulties in finding skilled labor.

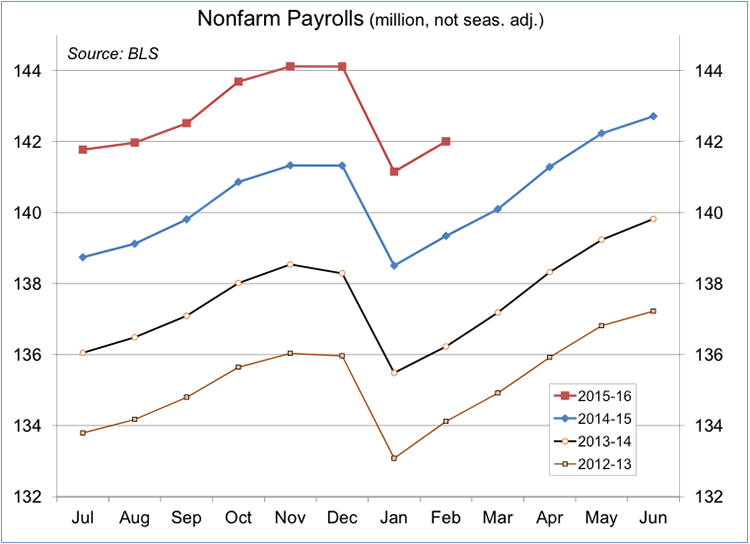

We added 850,000 jobs last month before adjustment (vs. 832,000 in February 2015). We can expect to add about three million jobs (unadjusted) over the next three months.

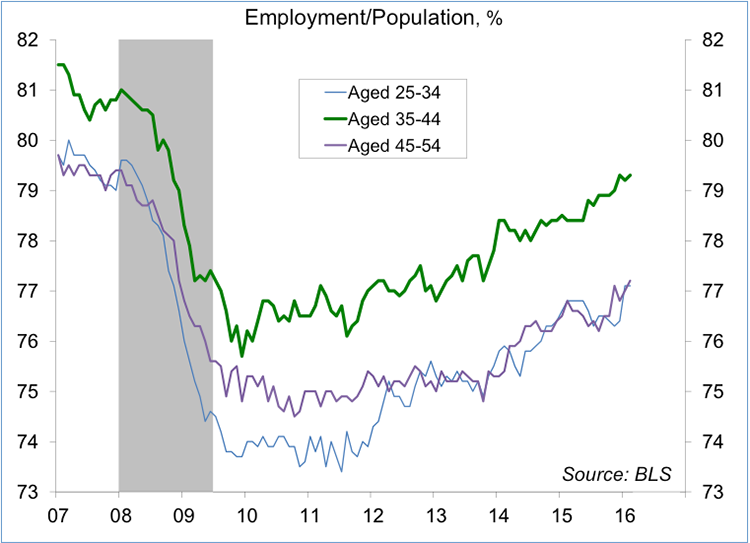

The unemployment rate held steady at 4.9% in February, but would have fallen further if not for an increase in labor force participation. The emp/pop ratio is trending higher, with solid gains in the key age cohort ( those aged 25-54 ). The broad range of labor market indicators suggests that there is still slack in the job market, but that slack is being reduced. Fed officials will differ in their assessments of slack in the job market, but there should be general agreement that monetary policy will need to be normalized over time. The question is one of timing.

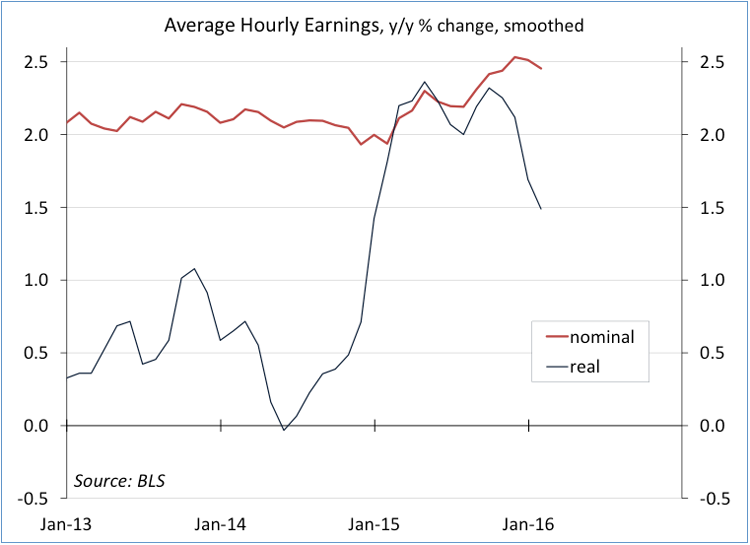

Average hourly earnings jumped 0.5% in January, but edged back 0.1% in February. That brought the year-over-year change down to 2.2%, vs. 2.5% in January. However, the wage data are often revised. The three-month average was up a little less than 2.5% from a year ago. So, the choppiness of the last two months aside, the underlying trend still appears to be higher.

Monthly trade figures tend to be choppy, but the initial figures for January point to a sharper impact from soft global growth and the strong dollar. Adjusted for inflation, declines were relatively broad-based. This is consistent with much of the anecdotal evidence suggesting that exporters are having a tougher time, particularly in regard to our key trading partners. Trade decisions don’t turn on a dime and the strength of the dollar appears to be having a significant lagged effect.

Still, the U.S. economy is largely self-contained. The household sector fundamentals are in good shape, but businesses may remain cautious due to fears of “recession,” worries about global growth, and election-year uncertainty.