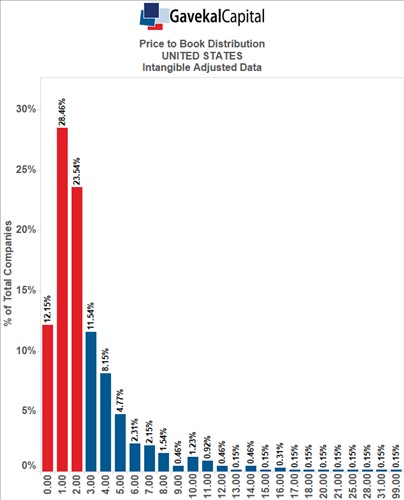

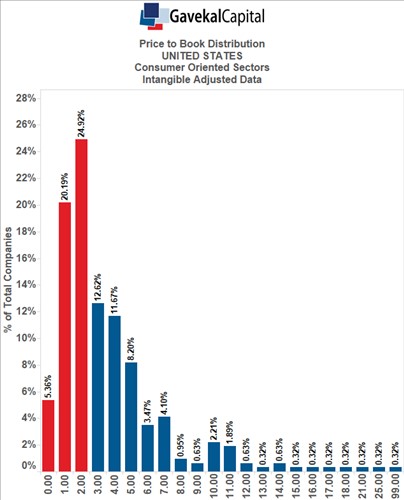

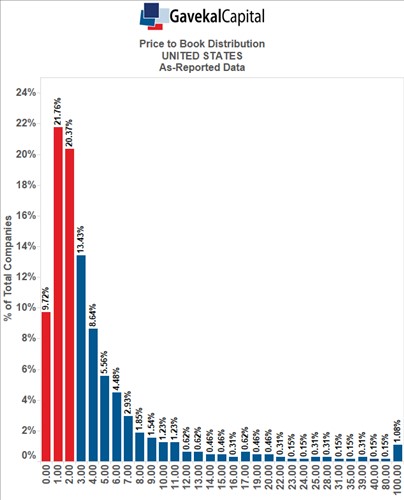

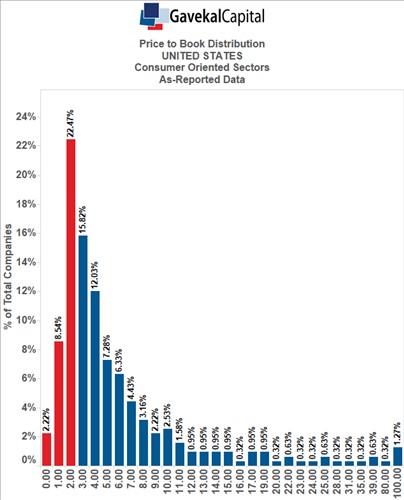

In the United States, nearly half of all companies (48.15%) trade over 3x book value. And if you break out valuations and look at just the more consumer oriented sectors (consumer discretionary, consumer staples, health care, and information technology) then the percentage of stocks that trade at a book value multiple of over three times increases to 66.77%. For those hardcore value investors that look for company’s trading below 1x book value, its very slim picking out there.

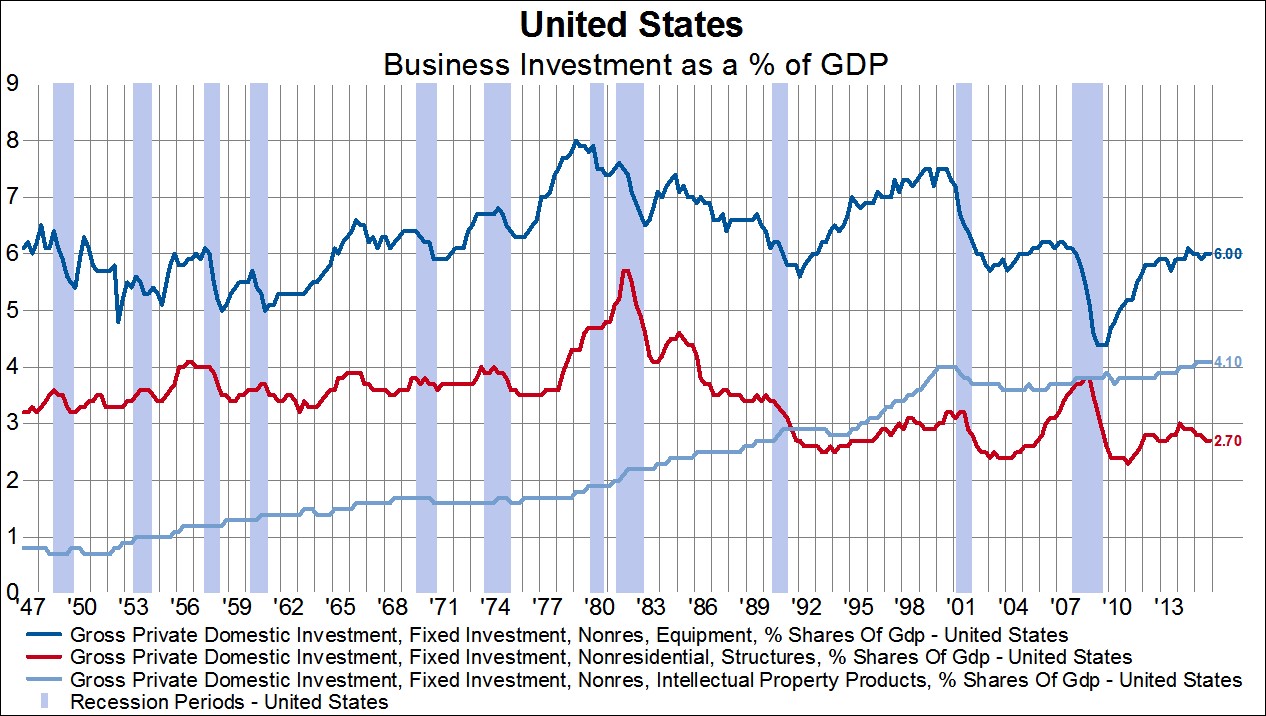

Since price to book value is a valuation metric, there are two possible reasons why so many companies currently trade at several multiples of book value. First, the numerator, price, could be inflated. Given that we have been in the longest running cyclical bull market in structural bear market, perhaps the market has gotten overly enthusiastic especially in regards to consumer oriented stocks. This is a reasonable assertion and an easy argument can be made that overall valuations in the stock market have become frothy. However, today we want to focus on the denominator, book value, since at Gavekal Capital we believe the book value of assets on company balance sheets is structurally underrepresented. The reason book value is underrepresented is because over the past forty years, corporations (and the economy as a whole) has shifted its asset base from a predominately tangible asset base to an evermore intangible asset base. In 1970, intangible investment only accounted for 14% of overall business investment in the US. Today, it accounts for 32% of overall business investment.

This shift has occurred because semiconductors have permeated throughout every industry and have changed the way companies accumulate capital. Prior to the release of the Intel 4004 in 1971, companies tended to purchase nearly all of its capital from a third party and this led to minimal differentiation among products since the capital stock companies were utilizing to create these products were all pretty similar. If you look around at any grocery store, you know that today we are in the age of massive differentiation. Companies continue to purchase a lot of its capital from third parties, however, now they add their own layer of internally created capital to the purchased piece of capital. This means that Pepsi’s Frito Lays still purchases the the bag Lays potato chips come in, but now they have 45 different variations of the Lays potato chip to meet all of its consumer’s taste demands instead of just one type of potato chip. Pepsi spends 1.2% of its sales on research and development in order to service the market with as many variations of potato chips as consumers want. In addition, Pepsi spends nearly 12% of its sales on other intangible investments, such as advertising and brand equity, to ensure that its consumers are knowledgeable that their favorite flavor profile can be found on a potato chip. This internally generated capital goes completely unaccounted on corporate financial statements because FASB created an accounting rule, SFAS #2, in 1974 that forced corporations to expense, instead of capitalize, intangible investments. This has led to a massive misinformation gap between investors and companies regarding what the true asset base of a company is composed of and this leads up back to our initial conversation on price to book value.

If one adjusts cooperate financial statements to include intangible investments on a company balance sheet, the number of companies that are trading at over 3x book value drops. Instead of about half of all companies trading over 3x book value, only about 35% trade over 3x book value once intangibles are taken into account. The change is even greater in the consumer oriented sectors. The percentage of companies that trade over 3x book value drops from 66.77% to 49.53%. We believe that if intangibles are properly accounted for, company valuation metrics, especially for the most innovative companies, make a lot more intuitive sense.