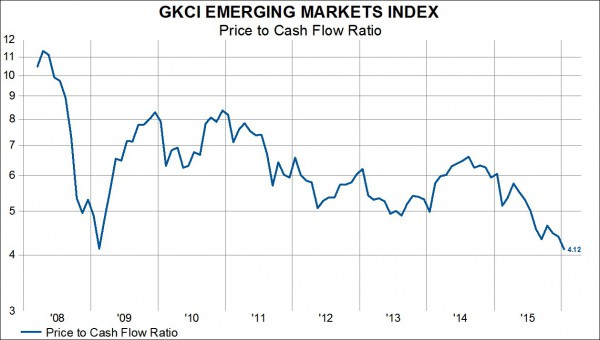

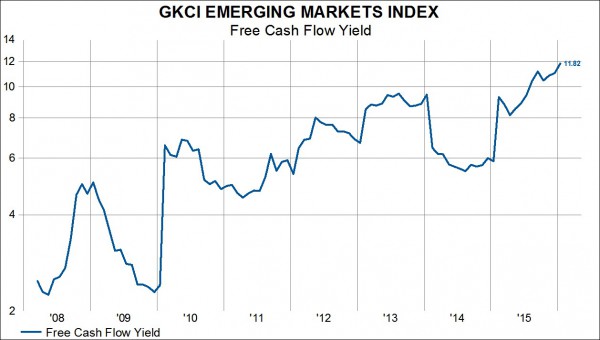

Regardless of the valuation metric one chooses to look at it, the story is the same: EM stocks are cheap. EM stocks have fallen so far that 2009 valuation lows are starting to be challenged. Case in point, on a price to cash flow basis EM stocks are trading at lower multiple today than they were in 2009 (granted just a hair lower). This is important because EM stocks are doing a better job than ever in creating free cash flow. The GKCI EM Index is currently trading at a juicy 11.82% free cash flow yield.

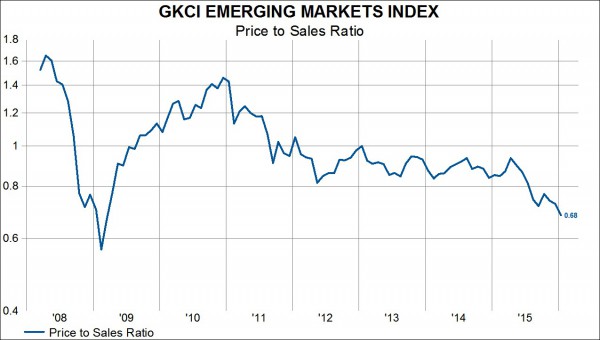

On a price to sales, price to book value, and price to earnings basis, 2009 valuation lows are still in place but current valuation multiples aren’t too far off. In 2009, EM stocks hit a price to book value level of 0.89x, currently its trading at 0.91x book value. In 2009, EM stocks were trading at 0.56x sales. Today, it trades at 0.68x sales. Finally, in 2009 price to earnings multiples hit a low of 5.99x. Today, EM stocks trade at 7.95x earnings.

EM stocks understandably remain out of favor for most investors. However, they have been out of favor for so long that finally a valuation argument can be made for dipping back into EM equities.