This article is directed to the individual investor concerned with achieving the highest possible total return. The highest total return will typically come from a true growth stock simply because a faster growing company is worth more than a slower growing company past, present and future. On the other hand, for that statement to be true, a high rate of earnings growth must be consistently achieved. Generating and sustaining a high rate of earnings growth is the tricky part, because although there are a few companies capable of generating higher earnings growth rates, they are rare.

Additionally, there is one undeniable fact about true growth stocks that is nevertheless hotly debated and argued about. In truth and fact, a pure unadulterated growth stock under the strictest definition is capable of dramatically outperforming most blue-chip dividend paying stocks. The total return differences are not subtle, they are significant and profound. However, I contend it is also an undeniable fact that the risk differential between investing in true growth stocks and blue-chip dividend paying stocks is equally as significant and profound. More simply stated, investing for high growth is risky.

As a result, it logically follows that high-growth stocks are much more research, due diligence and continuous monitoring intensive. Consequently, when investing in growth stocks I suggest you be prepared to put in the necessary work and effort to keep up with the company, its industry and the competition. In a free market, competitors won't let a high-growth company keep the market to itself. Therefore, if the investor is not willing to put in that effort, then investing in growth stocks may not be appropriate.

Nevertheless, even though I readily acknowledge that investing in high-growth stocks is undoubtedly riskier than investing in blue-chip dividend growth stocks, their rapid growth can effectively mitigate some of the risk. Thanks to the power of compounding, the company that is growing its earnings very fast can bail investors out even if they overpay for the stock at purchase. Of course, this assumes that the company continues growing earnings at above-average rates. And more importantly, assumes that the investor stays the course, which admittedly is an aggressive assumption.

The Power and Protection Of Higher Earnings Growth

With the above said, this article is primarily about the power, protection and return potential that can occur when investing in growth stocks. Although I will be referencing Facebook as a quintessential example of a true unadulterated growth stock, I contend that an analysis of Facebook, past, present and future also offers important investing lessons about growth stock investing in general.

Moreover, I consider myself a dedicated value investor. Regular readers of my work will attest to the fact that I consider fair valuation the most important metric to consider before investing in any stock. Not only do I write about the importance of valuation in virtually every article I publish, I have even been given the name MisterValuation and also operate a website under that name.

In the same vein, I consider fair valuation a critical metric to consider and evaluate when selecting high growth stocks just as I do any other stock. However, as I previously alluded to, you can be more liberal with valuation when a company’s earnings growth rate is as high as Facebook (FB) has achieved. In other words, as I will later illustrate, you can actually overpay when initially investing in a high-growth stock and still make an above-average long-term total return. You do take on more risk by doing that, but due to the power of compounding, a high rate of earnings growth can still generate a significant and above-average total rate of return.

This is possible because thanks to the power of compounding, investing in growth stocks can in effect compress time. In other words, instead of taking a decade or more to double your earnings in a slower growing blue-chip dividend growth stock, you can double your earnings much quicker in a true growth stock.

To illustrate my point I will turn to the widely recognized Rule of 72. This rule states that you can calculate the number of years it takes to double your earnings (or your money) at a given compound return by dividing it into the number 72. I have often utilized the following illustration to demonstrate the point I am making about the power of compounding and how it compresses time.

First I will make the assumption that the average person has a working lifespan of 36 years. In modern times this may be a conservative assumption, but as I will soon illustrate, it facilitates the math. Next I will assume two different compound rates of earnings growth as they apply to the average dividend growth stock, and then to the pure growth stock. For the dividend growth stock I will assume a generous and above- average rate of earnings growth of 10% per annum. For the pure growth stock I will assume the appropriately higher rate of earnings growth of 20% per annum. The math then looks like this:

With the dividend growth stock, If I divide 10% into 72, I calculate that it will take 7.2 years to double my earnings (72/10% = 7.2 years).

With the pure growth stock, if I divide 20% into 72, I calculate it will take only 3.6 years to double my earnings (72/20%=3.6 years). In other words, earnings will double in half the time.

If I apply this math to my assumed average working life of 36 years, I get the following results:

If my earnings double every 7.2 years at a 10% rate of growth, I will get 5 doubles in 36 years (36/7.2=5).

If my earnings double every 3.6 years at a 20% rate of earnings growth, I will get 10 doubles in 36 years (36/3.6=10).

The net effect is that by doubling my average rate of earnings growth from 10% to 20% per annum, I do not generate two times the earnings by growing at twice the rate. Instead, I get double the doubles. Looked at from the perspective of the first $1 (dollar) of earnings, the power of compounding (compressing time) becomes vividly clear.

Doubling my first dollar’s worth of earnings 5 times at the 10% growth rate results in the following: $1 doubles 5 times to $2, $4, $8, $16, and finally to $32. However, at the 20% growth rate I get 5 additional doubles over the same 36 year timeframe as follows: $64, $128, $256, $512, $1024.

To put this into perspective, over my assumed 36 year working lifetime I generate 32 times more earnings by growing at 20% than I would have if my earnings grew at 10% (1024/32=32). Doubling the number of doubles over the same timeframe shows the incredible power of compounding that true growth stocks are capable of offering.

However, it should be noted that successfully growing earnings at the rate of 20% per annum over a working lifetime is a rare and difficult feat. Eventually the law of large numbers comes into play and a company’s earnings growth rate will surely slow down as a result. Nevertheless, the above exercise is valuable for the insights it provides into the power of compounding.

Additionally, this knowledge about compounding also ties in nicely to rate of return expectations. I have evaluated and analyzed thousands of companies in my lifetime. This experience has led me to what I consider an undeniable conclusion. In the long run, earnings determine market price. Moreover, as this relates to achieving a high total return, when a stock is purchased at a sound valuation, your total return will be highly correlated to a company’s earnings growth achievement. To be more precise, your capital appreciation component specifically will be generated based on earnings growth. Additionally, this is also true for dividend paying stocks. Capital appreciation will relate to earnings growth, and so will the income component from dividends. In other words, a dividend paying stock’s rate of dividend growth will also highly correlate to its earnings growth.

The Power of Diversification When Investing In Growth Stocks

Regardless of your investing strategy, diversification should always play an important role. Nevertheless, diversifying a growth stock portfolio offers a different dynamic than is found with more conservative investing strategies. Due to the power of compounding at a high growth rate, a diversified growth stock portfolio can produce strong results even when the portfolio contains a significant percentage of failures.

The following table presented for illustration purposes assumes a $1 million portfolio invested in 15 high-growth stocks with approximately $660,667 invested in each. The assumptions presented in the table are extreme. For example, the first column assumes that 80% (12 out of 15) of the growth stocks go completely bankrupt and only 3 (20%) achieve the 20% return objective over 10 years. Even under this extreme and highly unlikely circumstance, the portfolio would still achieve a positive total return of 2.16% annualized. Of course, if you batted 100%, the portfolio would generate a total return of 20% per annum.

The point of this exercise is to illustrate that you only need a few successful growth stocks in a portfolio to make an attractive rate of return. This is what I meant when I stated earlier that a high rate of earnings growth can mitigate risk, especially when the growth stock portfolio is even moderately diversified.

Facebook is a Quintessential Example of a Growth Stock

Note: Before I continue on, I want it to be clear that this article is not intended to provide a comprehensive analysis of the business or fundamentals supporting Facebook. Instead, this article is presented on the thesis that that analysis and due diligence had already been completed. The primary premise and objective of this article is to present, evaluate and discuss the mathematics behind what drives long-term returns and how to calculate them. However, here are two articles here and here that provide interesting insights into Facebook’s future growth potential.

Therefore, the above discussion about the mathematics behind investing in growth stocks was offered to provide a clear perspective towards answering the question posed in the title of this article. Is Facebook a screaming buy or sell? The answer to this question is debatable, and I am certain there will be readers that take both sides. Nevertheless, the correct answer for each individual investor will be related to their own personal risk tolerances and typical investing behaviors.

My definition of a growth stock is straightforward and precise. First of all, a growth stock represents the common stock of a company whose business is consistently growing earnings and cash flow at a significantly above-average rate. More precisely, my definition of a growth stock is a company whose earnings are consistently increasing at a minimum rate of change of earnings growth of 15% or better.

However, a hyper growth stock is one that I define as growing earnings at a rate of change of 25% or better. Admittedly, although both categories are rare, there are more 15% growers than there are companies growing earnings at 25% or higher. In between these broader gradations of growth are additional growth categories such as a high grower at 20%, etc. Consequently, as I will next illustrate, Facebook represents a quintessential example of a hyper growth stock.

The Math Supporting Facebook’s Historical Performance

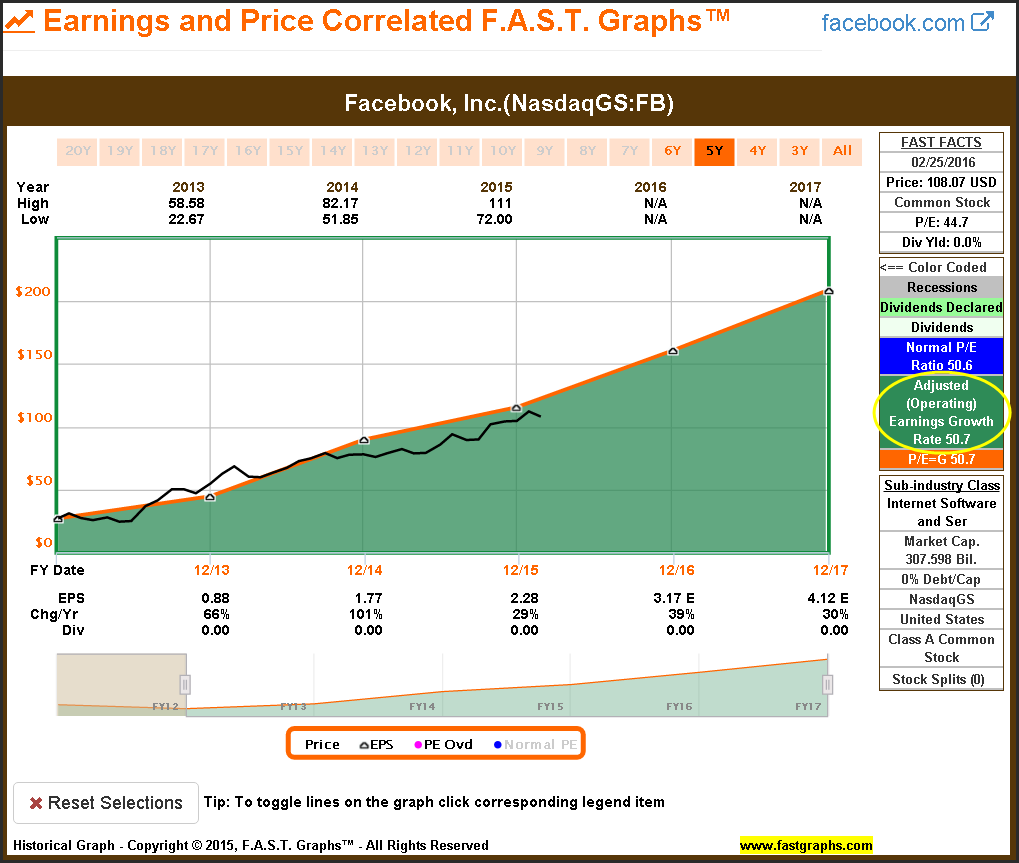

Additionally, the above discussion was also offered to illustrate that all investing is ultimately about the math. To be clear, historical performance will be a function of how fast the company has grown its business, which is a precisely-measurable set of historical facts. The following earnings and price correlated F.A.S.T. Graphs™ clearly illustrates how Facebook’s stock price (the black line) has tracked its earnings (the orange line) since 2013.

The graph also illustrates that Facebook has grown its earnings at the incredible rate of 50.7% per year. Since Facebook has grown earnings above 15%, the formula utilized to draw the orange valuation reference line is P/E ratio = to earnings growth rate (Note: the formula is depicted in the orange rectangle in the FAST FACTS box as P/E=G). Therefore, the orange line on the graph represents a P/E ratio or earnings multiple of 50.7.

The following historical performance results for Facebook over this timeframe clearly validate my thesis that earnings drive market price. Had you invested $10,000 in Facebook on December 31, 2012 that investment would now be worth $40,597.58. That calculates to an annual rate of return of 55.9% which closely correlates to the company’s earnings growth rate of 50.7%. At the end of the day, investing in common stocks is all about the mathematics behind the company’s operating achievements.

Estimating Facebook’s Future Performance Is Also All About the Math

Thus far I have illustrated how long-term Facebook shareholders have been rewarded in almost direct proportion to its business results. However, as I alluded to earlier, historical performance is measurable because it has already occurred. On the other hand, the future performance of Facebook remains an unknown. Nevertheless, my argument is that Facebook’s future performance will also be a function of the math behind its future earnings growth.

Additionally, at least over the intermediate-term, I continue to believe that Facebook will not be paying a dividend anytime soon. Therefore, Facebook’s future total return will also be a direct function of capital appreciation generated by future earnings growth. Of course, since the future is always unknown, it can only be forecast or estimated.

My suggestion is that investors should run numerous forecasts based on reasonable assumptions regarding Facebook’s future growth. In other words, several “what if” scenarios should be calculated with the objective of running conservative, optimistic, moderate, or even worst case scenarios. But most importantly, current or prospective investors should do the math based on each of those scenarios in order to calculate specific future return possibilities. As previously stated, the endgame of all successful investing is always about the math.

Doing the math does not need to be hard if you have the right tools at your disposal. Spreadsheets or financial calculators can do the trick. Regardless, I believe it is imperative that investors do the math in order to have reasonably precise calculations about what their future returns might be. Therefore, I offer the following video utilizing the various F.A.S.T. Graphs™ “Forecasting Calculators” where I will run various “what if” scenarios and calculations on Facebook’s potential future returns over the next 3 to 5 years.

The key benefit behind this process is to gain as clear of a view and understanding of Facebook’s future return possibilities based on various scenarios. In my opinion, this is far superior to simply investing in a stock with the hope that it will go up, or that you will make money. Moreover, this exercise is designed to provide a reasonable range of probabilities and possibilities regarding future returns. I consider this analogous to investing with your eyes wide open.

Summary and Conclusions

Facebook is clearly one of the most dominant (hyper) growth stocks of modern times. Its historical earnings growth achievements have been nothing short of spectacular. Consequently, the company has already grown to a market cap in excess of $300 billion over a very short period of time. This may be the biggest challenge the company faces regarding its future growth potential. Nevertheless, the company continues to exceed consensus analyst earnings estimates almost like clockwork.

Based on historical earnings achievements, Facebook appears fairly valued in spite of its lofty current blended P/E ratio over 44. When looking to the future, it appears that Facebook might continue to grow earnings at 30%-plus rates, at least for the next few years. Therefore, due to the power of compounding, Facebook could be a rewarding future investment even if the stock experiences P/E ratio contraction. The key of course is future earnings growth. At current valuations the company will have to continue to grow very fast to support its stock price. Is Facebook a screaming buy or sell? I leave that decision up to you.

Disclosure: No position.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.