“If zero or negative interest rates actually fixed what’s broken in the economy, we’d all be living in Paradise after seven years of zero interest rates.” – Charles Hugh Smith (blog)

I am up early, in my favorite chair and loving the coffee that Susan just made for me. It’s quiet and it’s Friday. Happy. I hope you are as well.

Ticking down the check list, following is my personal view on what is happening in the markets and what the road ahead may look like:

- The commodity bear market remains. Started in 2011, the average bear market lasts approximately 19 years.

- Oil is a mess (except for you and me and our wallets at the gas pump). Overall, still an economic drag as billions of dollars in projects are shelved and high-paying jobs are lost – though lower oil and gasoline prices are a positive for the consumer.

- The Fed – still leaning higher on rates, but I see them on their way to going lower. The talk of negative rate messaging is purposeful and, in my view, concerning (see quote above and see a link below to an important article by Ray Dalio).

- The equity bear market remains the dominant trend. As indicated by our CMG Ned Davis Research Large Cap Momentum Index and general price trend data (see Trade Signals below). The technical’s around the three day rally look weak.

- Equity valuations remain high. Probable forward 10-year returns remain low.

- The asset classes showing the strongest relative strength are Utilities, Government Bonds, Muni Bonds and Gold.

- Global recession – yes. S. Recession – not yet. Getting the timing right is critical to our collective wealth and future opportunity.

One of our advisor clients called me and asked for my thoughts on what the high-yield bond market may be telling us about recession. For what it’s worth, I shared the following:

My nearly 25 years of trading HY has taught me that the sector is a good leading indicator for the equity market and the economy. I believe that, in general, bond managers are really on top of their individually-held corporate credits (bonds). As you’ll see in the next chart, the major long-term trend for HY is down. This is concerning to me.

As prices decline, yields go higher and that spread relative to safer bonds like Treasurys is going up. That is a sign of potential trouble for companies. To this end, the overall default rate is rising and expected to reach a six-year high in 2016 and junk bond stress is spreading beyond energy (according to Moody’s).

In my view, severe stress will present when the money is due to be paid back. Post the great financial crisis, many companies found it easy to refinance and at lower interest rates. However, too many not-so-qualified borrowers found funding and at low rates. A number, including many in the energy space, are on life support and in need of refinancing. Nearly half of the $2 trillion total in the high-yield market is set to mature between 2016 and 2020. Refinancing will be impossible for some (defaults will spike) and be difficult for others. As investors, the probable sell-off will create our next investment opportunity!

Further concerns include the European and U.S. domestic banks that carry loan risk on their books. There is concentrated loan exposure to the oil and gas industry. Banks are highly leveraged businesses. We have reliable word that banks are marking down those loans on their books. These institutions are highly regulated. Once one starts, they all must get real. I expect we’ll see poor bank earnings numbers in April. One has to wonder why they waited until the first quarter of the 2016? 2015 incentive bonus’s anyone.

The behavior of bank stocks (such as SPDR S&P Bank ETF “KBE”) and iShares MSCI Europe Financials ETF (“EUFN”) relative to the S&P 500® (“SPY”) may be telling us something. Consider it a data point and let’s revisit this post come April’s earnings season.

Source: Yahoo! Finance

I conclude that recession holds the key to whether we see a short-term correction in the -15% to -20% range (maybe now behind us) or the -40% to -60% range. Either way, I believe valuations are high. Expect low forward returns from both equities and bonds.

Underweight equity exposure (and hedge that exposure), allocate to bonds (tactically) and overweight to tactical and other liquid alternative strategies and funds, such as managed futures, global macro and long/short equity.

I just can’t keep the opening quote out of my mind, “If zero or negative interest rates actually fixed what’s broken in the economy, we’d all be living in Paradise after seven years of zero interest rates.” Zero interest rates will hurt all of us.

Keep front of mind that we are living in a highly unusual central bank-influenced period in time. Untested and unknown.

I recommend you read Dalio’s piece below. He is the founder of Bridgewater Associates. Dalio and his team manage the world’s largest hedge fund ($154 billion in global investments). He looks forward to the next version of monetary policy. Helicopter money. As for John Hussman’s post, “Warning with a Capital ‘W”, drink something strong before you jump in. Don’t panic – just hedge, overweight to non-directionally dependent strategies and remain patient.

Patience and defense will pay off and hopefully keep your client firmly seated and on-plan through what may likely be a very bumpy ride.

To that end, ETF.com published an article I wrote entitled, “When Beating The Market Isn’t The Point”. Please feel free to share it with your clients. I hope you find it helpful.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- What Monetary Policy 3 Will Look Like, By Ray Dalio

- Hussman – “Warning with a Capital ‘W’”

- Trade Signals – Primary Trend is Bearish, Rally Target (S&P 500: 1950 Key Technical Level) – Blog post 02-17-2016

“What Monetary Policy 3 Will Look Like,” by Ray Dalio

Monetary Policy 1 was via interest rates. Monetary Policy 2 was via quantitative easing. It will be important for policy makers and us as investors to envision what Monetary Policy 3 (MP3) will look like.

While monetary policy in the US/dollar has not fully run its course and lowering interest rates and quantitative easing can still rally markets and boost the economy a bit, the Fed’s ability to stimulate via these tools is weaker than it has ever been. The BoJ’s and ECB’s abilities are even weaker. As a result, central banks will increasingly be “pushing on a string.” Let’s take just a moment to review the mechanics of why and then go on to see what MP3 will look like.

Why “Pushing on a String?”

Lending in order to finance spending requires both investors/savers and borrowers/spenders, who have very different objectives, to each operate in both their own interests and in a symbiotic way. For example, when a debt expansion that finances spending on goods and services takes place, both a) the investors/savers increase their debt holdings because they believe that they are increasing their assets, and b) the borrowers produce those borrowings (that investors/savers call an ‘asset’) to increase their spending. When both are going on in a big way (i.e., when debts, financial assets, and spending are rising fast), we have a boom. However, because both savers and borrowers often don’t do the calculations very well to determine whether the debt created will be used to produce more than enough income to service the debts, we also have busts. So, to understand how central banks’ monetary policies work, one has to see things through the eyes of both investors/savers and borrowers/spenders.

I will look at the process from the investment side, as that is now more important because central bank policies, especially quantitative easing, have their effects more by affecting the behavior of investors/savers than by affecting the behavior of borrowers/spenders. When the central bank buys a bond, it does so from a saver/investor who takes the cash to make an alternative investment decision. What they invest/save in makes all the difference in the world. When investing/saving is in the sort of assets that finance spending, that stimulates the economy. However, when investing in that sort of asset is unattractive, which is what happens when the “risk premiums” are low and/or investors are scared, it does not. To the extent that interest rates decline, that also has a positive effect on all asset prices because all investments are exchanges of lump sum payments for a stream of future cash flows, and the interest rate (i.e., the discount rate) is the rate that is used to calculate the present value of these cash flows. All else being equal, the more interest rates are pushed down, the more asset prices will be pushed up. That is how monetary policy now works.

So, Where Do Things Now Stand?

The discount rate is just about as compressed as it can be, so the potential present value effect of lowering it is nearly at its end. That’s a big thing. In terms of the risk premiums of “risky assets,” they’re now neither especially high nor low, so there is a bit more to be squeezed out of them, more so in the US than elsewhere. Put these two pieces together and it’s clear that the future returns of assets will be low, which will be a problem given what the returns need to be to meet our future obligations. Though not pressing, that issue is something that central banks will have to deal with, which helps to inform the picture of what MP3 will probably look like—i.e., they will need more “money printing.” From the perspective of an investor, if you look at the level of the returns relative to levels of volatility, the expected reward-risk could make those who are long a lot of assets view that terrible-returning asset called cash as appealing.

To clarify, take current bond yields (less than 2%) and cash (0%) and compare that to something like a 4% expected return on equities. Because of volatility, the 4% expected annual return pick up of equities over cash, or 2% over bonds, can be lost in a day or two. (For example, stocks fell by nearly 5% in a week earlier this month.) And then there is the feedback loop where a sell-off in the stock market in turn has a negative pass-through effect on the rate of economic activity. All that makes for asymmetric risks on the downside in the US—and the pictures in other countries are even more asymmetrical on the downside, as their interest rates are even lower and their risk premiums are nearly gone.

The mechanics of how currencies, interest rates, and economies work together is also important to understand at this time as they will have a big effect. Remember that all debt is a promise to deliver a specific currency, so when the currency gets more or less valuable, it affects people’s behaviors. That is true now more than ever because those who have money are exposed to alternative currencies to keep their wealth in (or to borrow in) and because the major currency systems are all in fiat currency. So more money than ever will move from one currency to another, or from currencies to other assets (e.g., gold), based on what people are thinking about how the values of currencies will change. Also we should expect currency volatility to be greater than normal because 1) when interest rates can’t be lowered and relative interest rates can’t be changed, currency movements must be larger, and 2) when both relative interest rates and relative currency movements are locked together (e.g., in European countries and wherever there are pegged exchange rates), relative economic movements must be larger. Said differently, to avoid economic volatility, currency movements must be larger. That reality creates “currency wars,” pegged exchange rate break-ups, and increased currency risk for investors. Because currency movements benefit one country at the expense of another (e.g., they’re beggar-thy-neighbor), if the world’s largest economies all face the difficulty of pushing on a string, exchange rate shifts won’t create a needed global easing. Nobody intends these wars to happen. That’s just how the economic machine works.

For these reasons investors should expect to experience lower than normal returns with greater than normal risk.

Asset prices have fallen largely as a result of this, together with the deflationary pressures brought about by most economies being in the later stages of their long term debt cycles.

So, how might the current decline in risky assets transpire? That depends on what levels risky assets need to decline to in order to raise their risk premiums enough to cause investors who have a long bias (which most all have) to take their cash holdings (or to borrow cash) to add to those assets. With the central banks’ abilities to be effective in easing to reverse a downturn weaker than before, the past may not be a good guide because the self-reinforcing cycle of falling asset prices having negative economic effects may not be as easily reversed as in more normal times. In other words, the downside risks are greater. That doesn’t mean that a downturn is likely—it’s just that the risks are asymmetrical if one does.

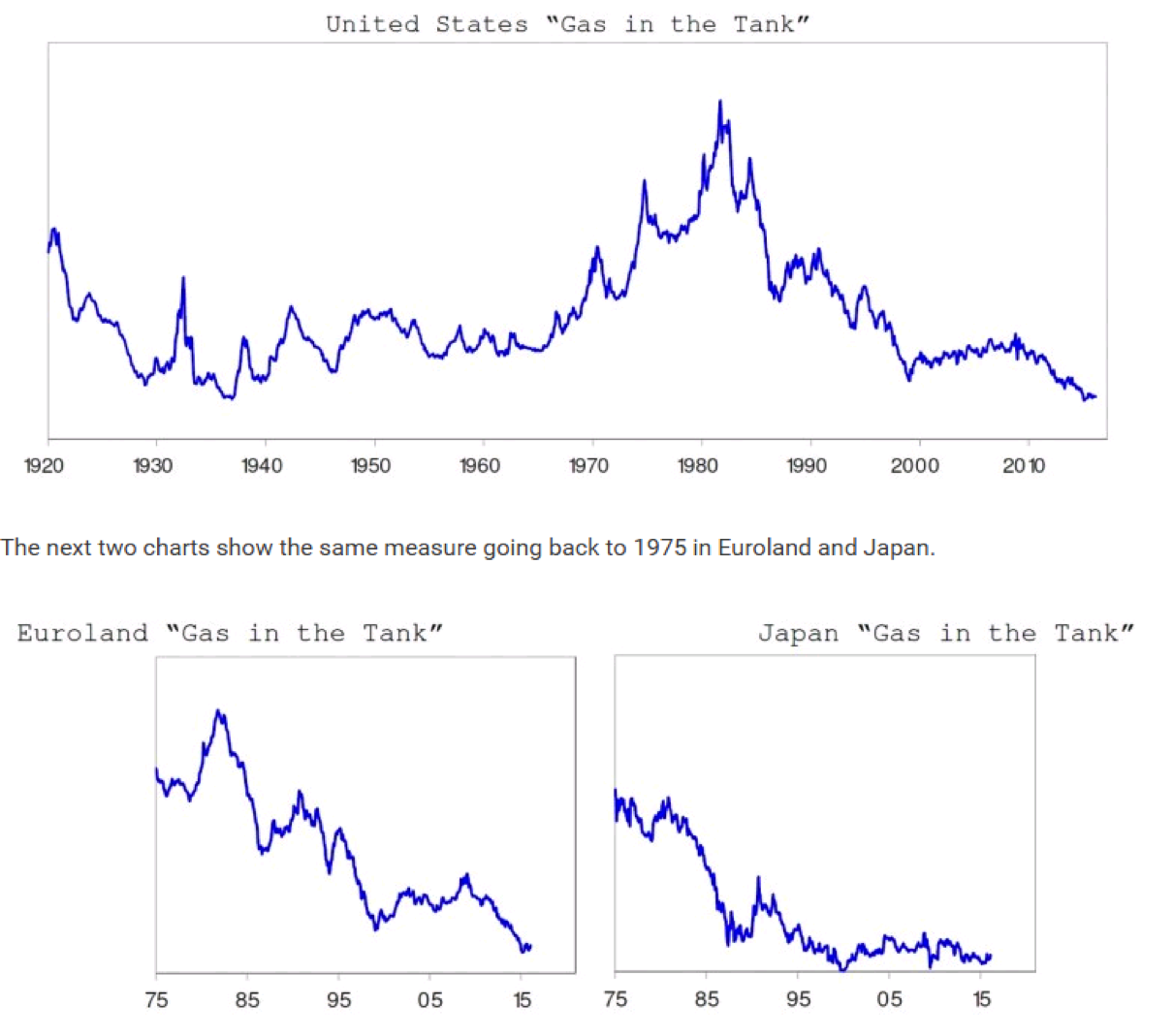

Most likely, as risk premiums increase, central banks will increasingly ease via more negative interest rates and more QE, and these moves will have a beneficial effect. However, I also believe that QE will be less and less effective because there is less “gas in the tank.” To convey how much gas they have left in the tank, we created an index based on the previously described drivers. It is shown below for the US since 1920 and for Euroland and Japan since 1975. As shown, for the US it is as low as ever and approximately the same as in 1937. Because of this, we think that the 1937-38 period, though not identical, is the most analogous period to look at when thinking about interest rates, currency rates, monetary policies, and global economic activity. It, and the mechanics behind it, are worth understanding.

Ray Dalio: What Will Monetary Policy 3 Look Like?

While negative interest rates will make cash a bit less attractive (but not much), it won’t drive investors/savers to buy the sort of assets that will finance spending. And while QE will push asset prices somewhat higher, investors/savers will still want to save, lenders will still be cautious lenders, and cautious borrowers will remain cautious, so we will still have “pushing on a string.” As a result, Monetary Policy 3 will have to be directed at spenders more than at investors/savers. In other words, it will provide money to spenders and incentives for them to spend it. How exactly that will work has to be determined. However, we can say that the range will extend from classic fiscal/monetary policy coordination (in which debt to finance government spending will be monetized) to sending people cash directly (i.e., helicopter money), and will likely fall somewhere between these two (i.e., sending people money tied to spending incentives).

To be clear, we are not describing what will happen tomorrow or what we are recommending, and we aren’t sure about what will happen over the near term. We are just describing a) how we believe the economic machine works, b) roughly where we believe that leaves us, and c) what these circumstances will probably drive policy makers to do—most importantly that central bankers need to put their thinking caps on.

As a quick aside: Jimmy Rogers was on CNN last week. He made his fortune several times over by investing where others feared to tread. He made a name for himself in the 1970s after co-founding a top-performing fund with George Soros.

He is sharp yet sometimes controversial. I’ve read several of his books and always find myself interested in what he has to say. Following is his two cents:

- “We’re all going to pay a horrible price for the incompetence of these central bankers,” Jim Rogers said Monday in a TV interview with CNNMoney’s Nina dos Santos. “We got a bunch of academics and bureaucrats who don’t have a clue what they’re doing.”

- He predicts their unconventional monetary strategies will lead to a stock market rally in the near future, but deep trouble later this year and into 2017.

- “It’s been over seven years since we’ve had a decent correction in the American stock market. That’s not normal … Markets are supposed to correct. We’re supposed to have economic slowdowns. That’s the way the world has always worked. But these guys think they’re smarter than the market. They’re not.”

- “You should be very worried and you should be prepared.” Source

“Warning with a Capital ‘W,’” by John Hussman

I know you may have or continue to have an allocation in one of John’s mutual funds. He missed getting long again in 2009. That stung both his investors and him. My advice is to not let that sour taste get in the way of some very sound research. No one is perfect in this game – thus we diversify to a number of different risks.

John begins, “We continue to classify the prospective equity market return/risk profile within the most negative climate we identify. The basis of this classification is fairly straightforward. Historically, once an extended speculative period of extreme overvalued, overbought, overbullish conditions gives way to increasing risk-aversion, as indicated by deterioration in market internals (and particularly in the presence of hostile yield trends in the form of widening credit spreads), the stock market has become vulnerable to vertical losses. Though not every instance of this syndrome has been followed by a market collapse, every notable panic and market crash across more than a century of data has featured that basic setup.”

Remove all sharp objects and click the link to read John’s latest piece titled, Warning with a Capital “W”.

We have created several educational pieces and white papers. We hope you find them helpful in your work with your clients.

- When Beating the Market Isn’t the Point

- Correlation, Diversification and Investment Success

- The Merciless Math of Loss (this is about how compound interest works for you)

- Here is a link to our Advisor Blog page

- Here is a link to our Advisor Resource page

Trade Signals – Primary Trend is Bearish, Rally Target (S&P 500: 1950 Key Technical Level) – Blog posted 02-17-2016

S&P 500® Index 1922

By Steve Blumenthal February 17, 2016

The trend remains negative for equities and is neutral for high yield. Investor sentiment remains extremely pessimistic. Such extreme readings are generally bullish for equites. We are finally seeing the oversold rally.

The S&P 500® Index is nearing its February high at 1947.20. The 50-day moving average line (trending lower) is currently at 1960. I favor establishing hedges on equity exposure in the 1925 to 1960 area.

Overall, the major trend remains bearish and the market remains expensively priced. In last week’s “On My Radar,” I shared some stats on past bear market corrections that may help put the current indigestion into perspective. They are pretty interesting. You can find them here.

Included in this week’s Trade Signals:

Equity Trade Signals:

- CMG Ned Davis Research (NDR) Large Cap Momentum Index: Sell Signal – Bearish for Equities

- Long-term Trend (13/34-Week EMA) on the S&P 500®Index: Sell Signal – Bearish for Equities

- Volume Demand is greater than Volume Supply: Sell Signal – Bearish for Equities

- NDR Big Mo: See note below (active signal: sell signal on 1-15-16).

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Extreme Pessimism (short-term Bullish for Equities)

- Daily Trading Sentiment Composite: Extreme Pessimism (short-term Bullish for Equities)

Fixed Income Trade Signals:

- The Zweig Bond Model: Sell Signal

- High-Yield Model: Neutral

Economic Indicators:

- Don’t Fight the Tape or the Fed: Indicator Reading = 0 (Neutral for Equities)

- Global Recession Watch Indicator – High Global Recession Risk (85.7% Probability)

- U.S. Recession Watch Indicator – Low U.S. Recession Risk

(S&P 500® Index monthly declines of -4.8% or greater below its 5-month smoothing (MA) signaled recession 79% of the time: 1948 – Present). Data is updated each month end.

Currently -4.1% below 5-month smoothed moving average.

Tactical — CMG Opportunistic All Asset Strategy:

- Relative Strength Leadership Trends: Utilities, Fixed Income, Muni Bonds and Gold are showing the strongest relative strength:

Personal note

Your portfolios probably have an allocation weighting to global equities. So I found it interesting and logically sound that bear markets, historically, were more severe when the global economy and U.S. were both in recession at the same time. The MSCI All Country World Index (ex – U.S. stocks) had an average drawdown of 48.6%. The MSCI ACWI (which includes a weighting to U.S. stocks) had an average drawdown of 45.2%.

My personal view is that we are currently in a global recession yet the U.S. is not yet in recession (though likely near). I sense that the confidence placed in global central bankers is waning. It feels to me much like it did in 2007. We are overdue for an economic recession. Likely this year or next. Recessions create moments of chaos. We will be called upon to bring peace in the next moment of chaos. That will be easier to do if the collective set of diverse risks set in place, in the portfolio creation process, do their job.

I believe that you and I will once again be called on to help others find peace. Going into the game prepared with game plan in hand, in my view, is critical. It will help with the finding peace part and should help with the seizing the opportunity part.

Naples, Florida is up next on February 29. I’m attending the CBOE Risk Management Conference. We do a lot of hedging within one of our equity funds and I’m looking forward to a spirited few days. We trade ETF-based options and have experienced first-hand the growth in liquidity, trading volume and the tightening in bid/ask spreads. I’m looking forward to learning more.

Dallas follows in the first week of March for a mutual fund gathering of key platform decision-makers. I will travel to Indianapolis in mid-March for an advisor’s client event and to San Francisco on March 23 and 24 for several meetings. I just booked three nights in Vail. It is just me and my boys. Though I’m going to try to twist Brianna’s arm. From there we drive to Denver for several advisor meetings and an afternoon touring the University of Colorado – Boulder. My Matthew is a high school junior and crazy about skiing… so CU is on his mind. Though I’m doing my best to brainwash him on Penn State.

Wishing you an outstanding weekend! It is supposed to be 55 degrees and sunny here in Philadelphia!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal Chairman & CEO CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History:

Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Following are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group

© CMG Capital Management Group