Retired Dividend Growth Investors: Sleep Soundly by Embracing Survivorship Bias

Introduction

Before investing in any common stock I believe it’s imperative to know as much about the business behind the stock as you possibly can. However, there are only so many businesses that an individual investor can know anything about. On the US stock exchanges alone, there are approximately 20,000 individual companies to choose from. Therefore, logic would dictate that every individual investor needs a process or system for separating the wheat from the chaff.

The first logical step towards implementing a process that is appropriate for you is to clearly identify your investment goals and objectives. For example, if dividend income is your goal, it would logically follow that you would exclude all or any company that doesn’t pay a dividend. In other words, it would make no sense to spend time learning about a company that doesn’t support your primary goal. This principle would apply to any investment goal or objective that an investor could have. Of course, the opposite is also true. When searching for a common stock investment that meets your goal, you are best served by only searching among and/or screening the universe of companies that can potentially support your objectives.

This article is directed towards those investors primarily interested in achieving a growing income stream. Since the world seems to love to label things, this article is directed to the so-called “dividend growth investor.” Retired investors are one of the primary practitioners of this particular strategy because they are living off of the income their investment portfolios produce.

On the other hand, I am not yet retired and have no immediate plans of doing so, yet I also personally embrace investing in dividend growth stocks as the primary constituents of my portfolio. Even though I am not yet living off the income my portfolio produces, I like the idea of generating additional discretionary income that I can spend if I choose, or reinvest if I don’t need it currently.

Therefore, when looking for suitable stocks to invest in, I appreciate the work of fellow Seeking Alpha Author David Fish and his CCC lists of Dividend Champions, Contenders and Challengers. I also appreciate the legwork provided by S&P Capital IQ with their Dividend Aristocrats list. The combination of these two suppliers of dividend growth stock opportunities provide an approximate listing of 750 dividend growth stocks that I can choose among. Consequently, I have already whittled the list of approximately 20,000 individual stocks down to a more manageable level. This is the true value that lists like these cited above offer.

However, and this is critical as it relates to the intent of this article, that doesn’t mean that I would be willing to invest in every company on those lists, nor does it mean that I would only invest in a dividend paying stock if it did. Furthermore, not every dividend paying stock is on those lists, but they certainly represent an elite grouping of dividend paying stocks with a history of increasing their dividend. Consequently, they provide a fertile field of stocks for me to investigate that almost by definition would support my primary goal of income growth.

Survivorship Bias Is Irrelevant To Me--And I Believe Should Be To You Also

This article was inspired by a recent article titled “These 26 Dividend Aristocrats Won’t Let You Sleep Well At Night” by fellow Seeking Alpha author Psycho Analyst that introduced his article by referencing a recent offering of mine. Apparently, his article was offered as a counterpoint to my article titled “Consider This Strategy To Reduce Stock Market Anxiety.” Unfortunately, in my opinion his article had little or nothing to do with what I wrote about, and even more unfortunately, he insinuated that I was taking a position about the S&P’s Dividend Aristocrats list that was simply not true. To clarify the record, here are two direct quotes from Psycho Analyst’s article (emphasis added is mine):

“DGI Investors have bought into the idea that most companies with long records of raising dividends will continue to raise them. This concept was illustrated compellingly in Chuck Carnevale's recent article, "Consider This Strategy to Reduce Stock Market Anxiety." In that article, he suggested that investors need not worry about stock market volatility when invested in twenty stocks selected from the list of S&P Dividend Aristocrats.”

In truth, I suggested no such thing. My article was not about not worrying about stock market volatility simply because you are invested in Dividend Aristocrats. Instead, my article presented the views that stock price volatility is unpredictable, where in contrast dividend growth is more consistent and predictable. Therefore, I suggested that income investors would be better served to focus on the steady and rising dividend income they were receiving over being anxious about short-term price volatility. More to the point, a steadily rising dividend is a fundamental metric where short-term stock price is simply driven by the laws of supply and demand between buyers and sellers. Stock price is not a fundamental metric. I will elaborate more on this important point later.

Before I go on, I want it on the record that I respect Psycho Analyst’s work, and wholeheartedly support his right to express his views on investing. However, I am objecting to the misrepresentation of my work used to serve as a counterpoint backdrop to his thesis. His article was essentially a discussion of “survivor bias” which I emphatically contend has no relevance or relationship to what I was writing about. The following is an excerpt that I also argue misrepresented what I had truly written about:

“Since the trademarked term "Dividend Aristocrat" was devised by S&P to describe a list of stocks that have raised their dividends for 25 years or more, it should have come as no surprise to readers that the graphs Chuck displayed in his article showed a steady increase in dividends year after placid year. Unfortunately, investors who found this soothing at a time when market volatility is rising to unparalleled heights, may be falling prey to one of the classic mental errors that lead to poor investing decisions: survivor bias.”

“The term "survival bias" refers to what happens when we draw conclusions from a set of data from which all elements which have not lived up to some criteria for success have been excluded.”

For statisticians, the concept of survivorship bias may be relevant when evaluating the validity of studies that are presented to support a conclusion. However, my work that was cited was not a study designed to lead readers to the conclusion that Psycho Analyst insinuated I was drawing. Yes, I did include 20 examples, and each of them was in fact a Dividend Aristocrat. However, I was not taking the position that that you could ignore price volatility simply because my examples were Dividend Aristocrats.

Instead, and I repeat, I was suggesting that focusing on a steadily rising dividend income stream that was not being affected by price volatility was a rational approach that could help investors navigate troubled waters. Dividend income is not affected by price volatility, because dividends are paid based on the number of shares you own. Once you own the shares, price changes have no effect on the income that you receive.

In this same vein, here is why I contend that survivorship bias has no relevance to either my article that was cited, or to dividend growth investors in general. As I stated in the introduction of this article, investors should know as much about any company they are interested in investing in as they possibly can. However, this implies solely focusing on either the companies you already own, or are interested in possibly purchasing. Any companies outside of that universe are irrelevant.

In other words, I could care less about any company that was in the Dividend Aristocrats and fell from grace, unless I owned it at the time. The only companies I am interested in are the ones I own now or ones I am interested in possibly investing in. Moreover, the dividends of my companies are what I am most concerned about. Therefore, what I suggested in my previous article was that investors should focus on the fundamental metric called dividends on each of their actual portfolio holdings.

There were many other important and salient principles that I was writing about in my original article. For those readers that are interested in what I truly wrote about, you can follow the link presented above. However, and most importantly, my article was not suggesting complacency - and it certainly wasn’t suggesting ignoring your portfolio holdings simply because they were Dividend Aristocrats.

Although I am flattered that Psycho Analyst or any other credible author would reference my work in theirs, I do object when words are put into my mouth or implications are made about what I was suggesting when I wasn’t suggesting it. On the other hand, there is much that Psycho Analyst and I are in 100% agreement on. As a case in point, I am in complete agreement with many important contributions presented in Psycho Analyst’s article. For example, I wholeheartedly support most of the following excerpts where he wrote:

“Conclusion: Dividend Growth Portfolios Will Always Require Careful and Continuous Monitoring

The data you just reviewed should be enough to convince you that the only way to maintain a dividend growth portfolio that continues to pay dividends is to continually monitor your stocks, because there is no guarantee any dividend growth stock will continue to be a dividend growth stock, or even, for that matter, keep paying a dividend.”

“So Dividend Growth investors can't just buy and hold. They must monitor earnings closely, listen to conference calls, pay attention to critiques that point out problems with their stocks, keep alert to changes throughout the economy, and act swiftly when detecting black swans. If they wait until a company's earnings decline to where they have to cut or eliminate their dividend, the crumbling share price can make it impossible to replace the income lost from those dividends.”

Johnson & Johnson (JNJ): A Strong Survivor

Johnson & Johnson is a survivor. Furthermore, it is on the Dividend Aristocrats and Dividend Champions lists, and has increased its dividend for 53 consecutive years. I am long Johnson & Johnson, and a significant part of my attraction is the company’s long and illustrious record of dividend growth. However, I have not chosen to invest in Johnson & Johnson simply because it is on Aristocrats or Champions lists.

Instead, I have chosen to invest in Johnson & Johnson because it is an extremely high-quality blue-chip dividend growth stock that I have researched thoroughly, and I have continuously monitored its results each and every quarter for many years. Therefore, I could care less about any non-surviving Dividend Aristocrat or Champion because I am not invested in them.

I Suggest Focusing On Fundamentals, Not Short-Term Price Action

I articulated the core theme of my previous article as follows: The Stock Market Perspective Vs. The Dividend Income Market Perspective. What I was metaphorically illustrating was that those investors that are price focused expose themselves to a lot of anxiety. For starters, price focused investors tend to check the prices of their stocks daily, and quite often several times a day. The volatility associated with stock prices can create an enormous amount of stress and worry on both sides.

When the price of their stocks is rising, they tend to worry about the potential of losing gains they might have achieved. In contrast, when the price of their stocks is falling, they worry that they might fall further, or even worse, lose all of their money. In my experience, most human beings are not capable of enduring that much constant stress. Therefore, their investment actions are all too often reactionary rather than rationale.

In my previous article, I presented 20 examples where I was illustrating the consistency of a steadily rising dividend in contrast to the volatile and inconsistent movements of short-term stock price. For the most part, I utilized blue-chip dividend growth stocks that I was also long in (I am long 13 of the 20 examples I utilized). The remaining 7 where companies that I considered extremely high-quality blue-chip dividend growth stocks. And yes, all 20 were Dividend Aristocrats and Champions, and all 20 were survivors.

However, some of my examples are currently overvalued, meaning that I would not suggest investing in them at this time. Nevertheless, I chose these examples to illustrate the consistency of the steadily rising dividend income stream in contrast to volatile stock prices. In this article I will offer only Johnson & Johnson with the intention of clarifying the true message I wanted to deliver.

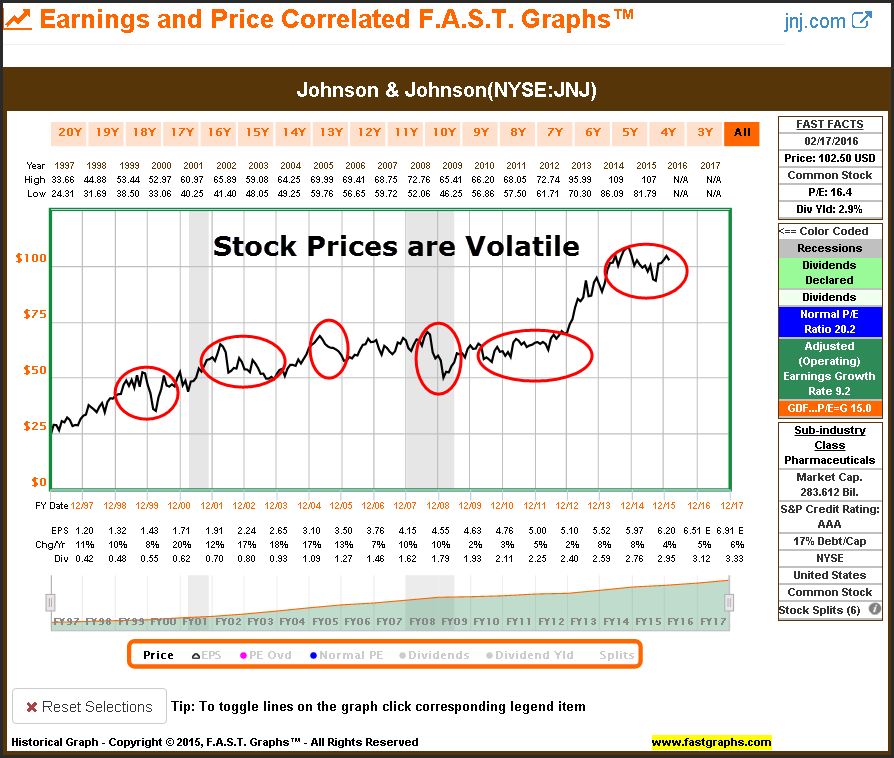

The following price only F.A.S.T. Graphs™ on Johnson & Johnson illustrates the volatility of short-term price action over a long timeframe. The major point of looking at Johnson & Johnson from this perspective is to simultaneously illustrate that stock price action is not always directly reflective of fundamental value. In other words, Mr. Market will often overvalue or undervalue a given stock at any point in time without any direct relationship to the fundamentals of the business. Consequently, I contend that there is very little intelligence to be gleaned from price movement alone. In other words, fundamentals are not involved.

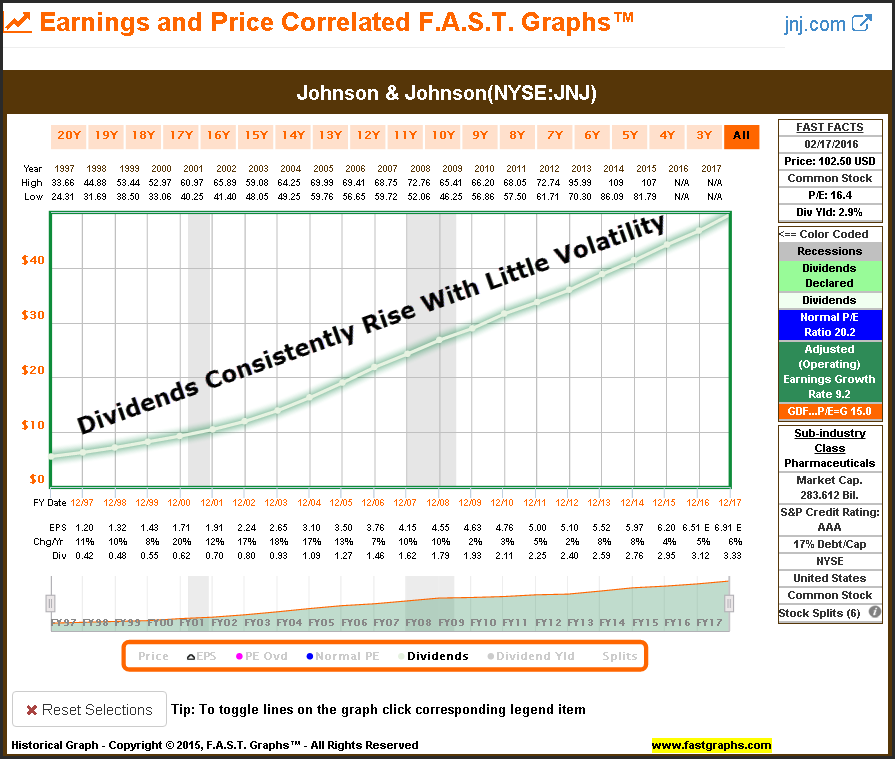

In my previous article, I presented a price only graph on each of my 20 examples followed by the associated long term performance to include dividends and capital appreciation. However, more to the point of my core thesis, I also presented a dividends only graph on each of the 20 examples. Therefore, I offer the following historical dividend record of Johnson & Johnson since 1997 just as I did in my previous article.

However, here is the point that I feel Psycho Analyst appears to have missed regarding what I was truly writing about. In all fairness, I may not have been clear enough in my first article; therefore, I hope to rectify that here and now. The primary reason for my suggesting that investors focus on dividends over short-term stock price movement is because dividends are directly associated with important fundamentals. Dividends are paid out of earnings and/or cash flows, which I believe are two of the most important fundamental metrics that investors should focus on, especially dividend growth investors. To be clear, all fundamental metrics are important, but earnings and cash flows are some of the most important metrics to the dividend growth investor.

Therefore, dividend growth investors who are more concerned with and focused on “The Dividend Income Market” are simultaneously also examining a proxy, if you will, of the important fundamentals. Steadily increasing dividends are functionally-related to strong earnings and cash flows. Consequently, there is intelligence associated with focusing on dividends. Simply stated, strong fundamentals support and represent the primary source of dividends and dividend growth. As a result, the company that has achieved a long and consistent record of dividend growth is typically a company with strong fundamental strengths.

As I previously stated, one area that Psycho Analyst and I are in complete agreement on is the importance of continuous monitoring of your portfolio holdings. However, I do not favor the continuous almost obsessive daily monitoring of stock prices. Instead, I favor continuous monitoring of fundamentals. The advantage of this approach is that you are only required to do it four times a year.

In other words, only when the company reports its financial statements are you given hard factual information. Therefore, prudent dividend growth investors are in effect only required to perform true research and due diligence on their company once each quarter. As a result, they are spared the daily stress and anxiety that comes with focusing on stock prices.

Consequently, they can intelligently manage their portfolios in a rather relaxed manner. Between each quarter they can spend their time with their families, or simply doing the things they enjoy. Portfolio management does require the commitment of a certain amount of the investor’s time. However, it does not need to consume all of their time if they are focused on the more relevant issues such as fundamentals.

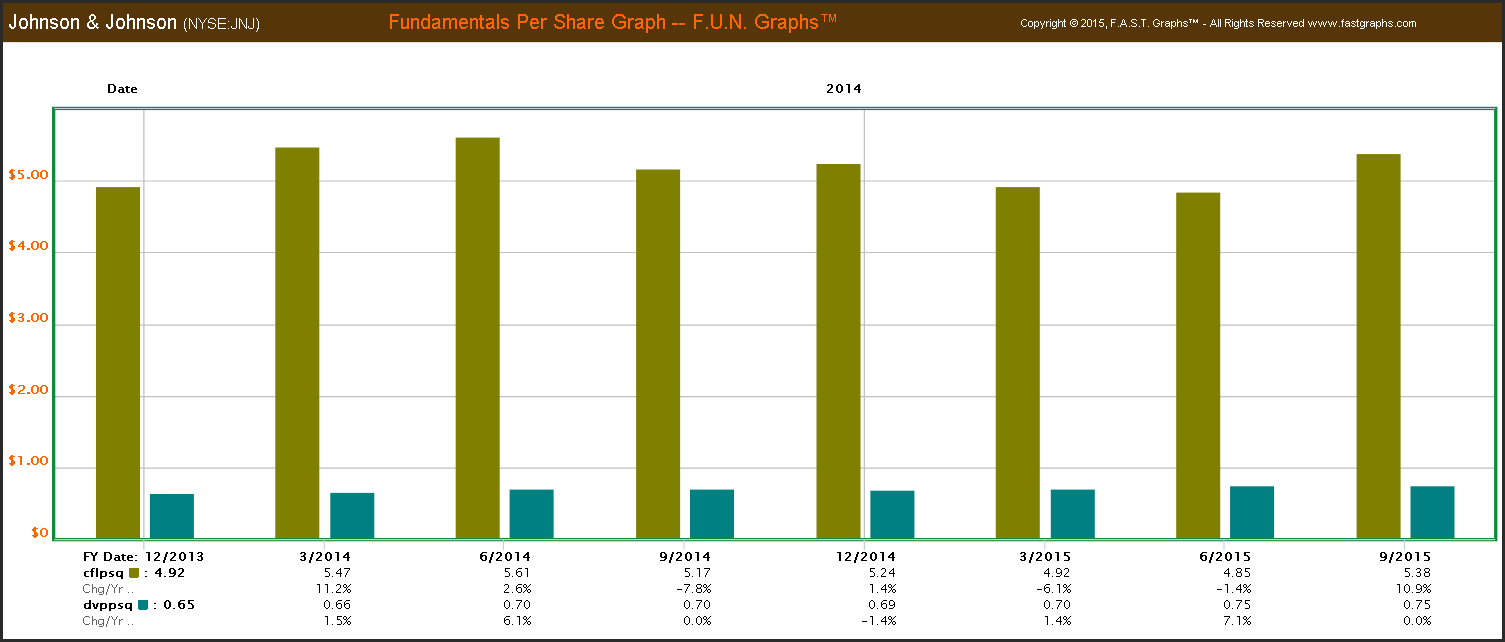

To illustrate my point, here are Johnson & Johnson’s quarterly cash flows and dividends paid for the last 8 reported quarters through September 2015. S&P Capital IQ has not posted actual year-end cash flows as of yet, but they are estimating them at $6.27 versus $5.38 for the fiscal quarter ending September 2015. Interestingly, they have already announced a dividend of $.75 payable on March 8, 2016 bringing their 2015 dividend in at $2.95 versus $2.76 in 2014. Therefore, from my perspective, all is well in Johnson & Johnson land relative to the sustainability of their dividend.

Summary and Conclusions

I wrote this article in order to respond to what I considered a misrepresentation of my previous work based on fellow Seeking Alpha author Psycho Analyst’s reference to it in his most recent article. I want to be clear that my attention was not to denigrate his fine article. He made a lot of valuable and interesting points in what he wrote. I am primarily objecting to his comments suggesting that I was taking a position that I, in fact, was not. Precisely, I objected to the innuendo that I was suggesting investing in Dividend Aristocrats or Champions as a worry-free strategy.

With that said, I am also not a devotee of survivorship bias in regards to analyzing individual stocks. If someone is conducting a study, then I can understand how excluding certain data could lead to misleading conclusions. However, regarding the management of an individual stock portfolio, I believe it only makes sense to focus on the stocks that are relevant to the portfolio.

However, I do believe that there is a bias regarding dividend growth investing that I consider unfair. This notion that dividend growth investors are members of a cult, or that they are complacent with their investing processes is categorically a falsehood, at least with the ones that I have a personal relationship with. Most dividend growth investors that I know are committed to comprehensive research and due diligence and they monitor their portfolio holdings on a continuous basis.

But perhaps most importantly, a dividend growth investing strategy, when conducted prudently, is a proven and sound strategy. It may not outperform the market on a total return basis over every timeframe. However, in my experience, a well-executed dividend growth strategy will outperform the market on the basis of total income generated over time. Furthermore, and once again in my own personal experience, the total dividend income generated consistently grows with each passing year.

Finally, the real reason I suggest focusing on dividends instead of stock prices is because dividends are a fundamental metric. Stated more directly, dividends come from earnings and cash flows. Therefore, as a general rule, if a company is raising its dividend every year it is also generating strong earnings and cash flows as well. The bottom line is that I favor focusing on fundamentals over obsessing over short-term stock prices and the associated volatility that goes with it.

Disclosure: Long JNJ.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.