Fed Chair Janet Yellen will present her semi-annual monetary policy testimony to the House Financial Services Committee on Tuesday. She is expected to present a moderately upbeat economic outlook, but she should also note the abundance of downside risks to that outlook. This is an election year, so she is unlikely to receive a warm welcome. If fact, many are likely to criticize the Fed for raising rates in December. She will put up a credible defense, but that’s unlikely to appease the markets.

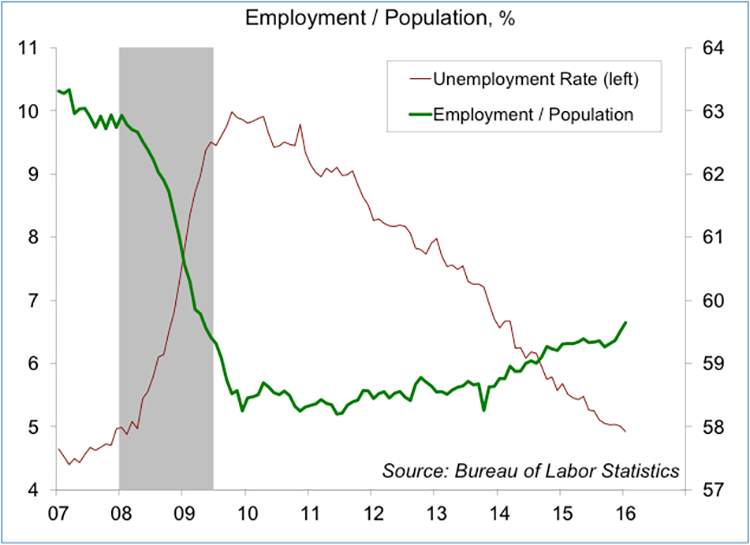

The Fed has two goals, maximum sustainable employment and stable prices (defined as 2% inflation in the PCE Price Index). It also has to keep an eye on financial stability. The job market has been the key driver of the Fed’s decision to begin raising rates. At 4.9%, the unemployment rate has dropped to a level that was once viewed as “full employment” (consistent with stable prices). The unemployment rate is a bit misleading, as many have dropped out of the labor force. Some of that decline reflects the demographics. However, the decline in labor force participation in recent years can’t be entirely attributed to an aging population. The employment/population ratio has begun to trend more noticeably higher over the last year (and especially in the last few months). Long-term unemployment and the number of people involuntarily working part time (preferring full-time employment) are still not back to “normal” levels, but they are getting close.

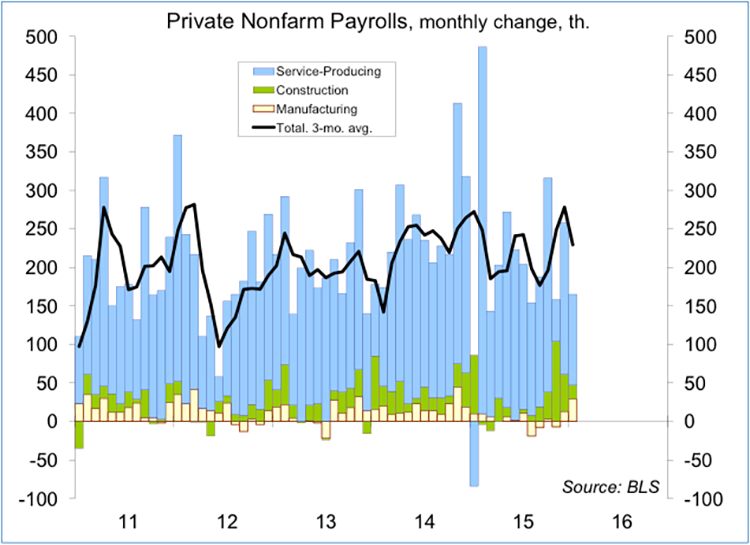

The economy added more than 5.7 million jobs in the last two years, nearly twice the pace that would be consistent with the growth in the working-age population. Strong job growth can continue for a while, as slack created in the downturn is taken up, but it will eventually slow to a more sustainable pace. Average hourly earnings rose 2.7% in 2015 (+2.5% over the 12 months ending in January), vs. a 1.9% average for the four previous years. This has caught the Fed’s attention.

The January Employment Report showed gains in manufacturing jobs in both December and January, which strikes many as unusual since other measures of factory sector activity have been soft. Most likely this is a seasonal adjustment issue. Less seasonal hiring in the summer and fall means that we are going to see fewer seasonal layoffs in the winter. Prior to seasonal adjustment, factory payrolls fell by 66,000 in January (+29,000 after seasonal adjustment). Similarly, retailers appear to have added fewer jobs in December – hence, fewer retail job losses in January (-584,000 before adjustment, +57,500 after adjustment). The financial markets are good at nuance, but this illustrates an important point. January data are generally unreliable. Take the numbers with a grain of salt.

Weather and seasonal adjustment make it difficult to judge the underlying strength in the economy in the first couple of months of the year. The data for March, April, and May will be much more critical. Fed policymakers know this.

Chair Yellen is likely to present an outlook that is close to the consensus view. That is, GDP is likely to rise by 2.0-2.5% over the course of this year. At the same time, the risks to that outlook are weighted predominately to the downside. The Fed has to balance the expectation (moderately strong growth) against the risks (slower growth) in setting monetary policy. Yellen should point out the policy is still very accommodative and that the Fed has to be forward-looking. Given the job market outlook, the central bank is still very much in tightening mode, but it is expected to proceed cautiously.

For most of the last few years, the stock market has been in the sweet spot. The economy was improving, but not so much that the Fed would take the punch bowl away. In recent weeks, the financial markets have over-reacted to the Fed, to oil markets, and to global developments, and we may not see investors come to their senses anytime soon.