Suffering Stock Market Stress?

Consider This Market with Negligible Volatility and Consistently Rising Values Instead!

Introduction

It would be an understatement to call the recent stock market activity turbulent. High stock price volatility makes investors anxious and some people even become downright frightened. These emotional responses are often exaggerated for people in or near retirement. Therefore, I contend that all investors need to find ways to keep their emotions in check in order to avoid panicking, which typically leads to the making of a devastating financial mistake.

I believe there is a viable antidote that is capable of calming investors down by empowering them to focus on one of the least volatile markets in all of finance. The market I’m referring to possesses only a small fraction of the volatility found in stock prices. Additionally, this market is predictable, consistent and produces significant levels of income. Even better, this market represents a primary source of long-term returns, and consistently rises over time.

Unfortunately, this market is hardly acknowledged or recognized by most people. Therefore, this article is offered and dedicated to enlighten investors about this powerful yet often ignored market. This is especially important during stock market times like we are experiencing today.

Stock Market Turbulence

Before I divulge the amazing constantly rising, low volatile market I discussed in the introduction, I would like to share a few excerpts from an article I recently read by Safal Niveshak titled “How to Deal with Stock Market Turbulence.” I felt Safal’s post contained a lot of wisdom and sound advice about handling a turbulent market like we have today. His article started out with the following allegory:

“Ladies and gentlemen, please fasten your seatbelts; the captain has just announced that we will be encountering some unexpected turbulence.

I hate hearing this phrase whenever I am flying, but there is no way an airplane can completely avoid turbulence (unless it is standing still in a hangar). When flying, captains don’t choose the route where there will be fewer clouds or less turbulence. Instead, they choose the safest, fastest way to get their passengers where they need to be. This, more often than not, means hitting a bit of unexpected turbulence.

Now, not unlike a flight, any journey you embark on is undoubtedly going to be a bumpy one. And investing in the stock market is not any different.”

Then Safal went on to offer the following sage advice, which I cannot agree with more:

“A lot of people fear stock market crashes and ‘unexpected’ turbulence like we are seeing now. But if your investment plan will only succeed if there is no turbulence at any time, it’s probably not a very good plan. If you follow a sound process, you need to embrace the turbulence, which I believe is a better option than avoiding it, if you actually want to get somewhere in your investment journey.

Successful investors are not those who tend to avoid all turbulence, crashes, and declines in their stock portfolios. Instead, they are the ones who know that turbulence might come and look forward to it, brace for it and embrace it at the same time.”

Later in the article Safal shared a thought from George F. Baker from the book “100 to 1 in the Stock Market” by Thomas Phelps that I found especially wise based on my own investing experiences and perspectives:

“To make money in stocks you must have “the vision to see them, the courage to buy them and the patience to hold them.”

From there Safal added his views on the importance of patience (a concept that I prefer to modify as intelligent patience) as follows:

“Patience – or the ability to keep on with your investment process despite the occasional periods of turbulence or euphoria – is the rarest of the three, but it pays off in the long run.”

I highly recommend you follow the link above and read Safal’s entire post, it is a very short article that I believe is chock-full of wisdom, and well worth your time, and extremely relevant regarding how to deal with how the market has been acting recently.

Dividend Income: The Primary Source of Long-Term Returns?

There is additional important information that I would like to share before I reveal the fantastic market that constantly increases in value with negligible volatility. As investors, I believe it is imperative that we all recognize and understand where the primary sources of long-term returns come from. This is critical knowledge that can empower investors to navigate through troubled waters.

In the comment thread of one of my recent articles a reader shared a link to a research report titled “Income as the Source of Long-Term Returns” produced by The Brandes Institute, an arm of Brandes Investment Partners, a highly regarded value investing firm. The following are a few excerpts from that research report that I felt were relevant to the thesis of this article:

“During the last two decades of the twentieth century, the investing world saw declining dividend and bond yields, with prices generally moving higher for both equities and bonds. In the early years of this century, investors seemed to belittle the importance of income as a component of returns, focusing primarily on the potential for capital gains.”

This next excerpt emphasized the importance of taking a long-term view with your investments:

“II. Taking a Long-Term View

One factor that has historically led some investors to underestimate the impact of income has been a reluctance to consider a true long-term horizon. References to long-term investment performance often tend to cite 3-or 5-year asset class returns. We challenge this definition of long-term horizon for two reasons. First, individuals and institutions may be investing for retirement purposes or with liability needs that have a horizon of 20 years or more. Second, the characteristics of investment returns may change significantly if long-term is redefined from 5 years to 20 years or more. While our data would allow even longer horizons than 20 years, we consider that length of period to be a reasonable practical maximum for most institutional and individual investors.”

But most relevant to this article of mine, was a discussion of the importance of income:

“III. The Importance of Income: the Historical Perspective

The debate over the relative importance of income versus capital price changes is a classic case of “tortoise versus hare.” In today’s information saturated world, investors tend to focus on financial items that tend to change rapidly (i.e., prices) rather than those that may be more stable, such as dividends. But our earlier study showed clearly that over the long term, income dominated Price movements as a source of returns, even for equities. For fixed income, income accounted for substantially all of returns over the long term.”

Finally, Brandes provided a summary of which I mostly agree with in concept, but as I will later illustrate, I do challenge parts of their conclusions:

“VII. Summary and Conclusion

Based on our review of 89 years of US investment returns across equity and fixed income, the importance of incomes contribution to total return is clear.

Fixed income returns were dominated by their income component for all time horizons longer than 5 years.

For U.S. equities, the income component was significant for time horizons as short as 5 years, and dominant for horizons of 20 years longer.

We believe this research illustrates that the industry acceptance of 5 years as a long-term investment horizon underestimates the potential of reinvesting and compounding income. By reinvesting the income contribution of investment returns, investors can leverage the power of compound interest. Investors should not let recent market experience distort their perspective, and particularly should avoid preconceptions that income is less important than capital gains in its contribution to total equity returns. Income has served as a significant component of returns, and the combination of reinvested income and capital appreciation has presented the best option for long-term investors to realize optimal terms.”

Before I go on, I think it is only fair that I acknowledge that I have been on record in the past of eschewing academic studies in the general sense. The Brandes study I cited above would be no exception. However, my position is not that academic studies have no value, because I would readily acknowledge that they do. However, my primary concern is that their over-generalized nature often leads to conclusions that can be misleading to investors.

For example, the Brandes study suggests or alludes to the fact that dividend income was the “dominant” contributor to returns for time horizons of 20 years or longer. I would certainly acknowledge that dividend income is an important contributor to total return, but not necessarily dominant, even over periods of 20 years. In the aggregate of all common stocks that the study purported to cover, it may be true. However, for the majority of US blue-chip Dividend Aristocrats or Dividend Champions that most US investors gravitate towards, I challenge that conclusion and will provide supporting evidence below.

The reason I feel it’s important to mention this is because achieving long-term capital appreciation through the ownership of blue-chip dividend paying stocks is also a significant benefit to investors. And as I will soon demonstrate, most best-of-breed blue-chip dividend paying stocks will in truth generate more capital appreciation than dividend income over a long-term horizon such as 20 years.

On the other hand, that in no way disparages the important contribution that dividends make. Additionally, I will add that this is a truth regardless of whether dividends are reinvested or not. The reason is simple and straightforward. Best-of-breed blue-chip dividend paying stocks grow over time, and that growth represents an important source of capital appreciation as well as dividend income growth.

Furthermore, since I am known in certain circles as MisterValuation, I feel compelled to point out that fair valuation plays an important role regarding how much capital appreciation an investor will receive from the ownership of a stock. Later in this article I will elaborate more fully on the contributions of both capital appreciation and dividend income to total return relative to valuation.

The Dividend Income Market

This final excerpt from the above report corroborates and introduces my assertion that there is a consistently rising market with negligible volatility that I believe it would be wise for investors to consider, especially those in retirement.

“Volatility of the dividend income streams themselves was a very small fraction (under one-twentieth) of the volatility of stock price movements.”

The constantly rising market with low volatility that I referenced in the introduction is what I call the “Dividend Income Market.” What differentiates this market from the stock market relates to what the investor focuses on. When people think of or refer to the stock market, they are primarily referring to and focused on stock price action. The headlines will always be something on the order of: The Market Is Up So Many Points or Down So Many Points Today Because of X. Clearly, this represents not only a focus on price, but also an obsession with price movements.

However, in my opinion there are important fallacies associated with the stock price focus and/or obsession. For starters, short-term price activity is the cost of the liquidity that publicly traded stocks provide. This liquidity is in stark contrast to less liquid investments such as real estate (of course REITs not included). Illiquid investments such as real estate also constantly rise and fall in value over time. However, there is no publicized quotation service reporting daily bids or asks. Therefore, when the time or occasion comes to sell a piece of real estate, it often takes an extended period of time to close the sale. In contrast, publicly traded stocks can be liquidated virtually instantly.

Nevertheless, both illiquid investments such as real estate, and highly liquid investments such as publicly traded stocks do possess an intrinsic value. In both cases, intrinsic value is ultimately a function of the amount of cash flow that the investment is capable of producing over time on its owner’s behalf. On the other hand, it is not always a given that current owners are capable of harvesting the full extent of their assets’ intrinsic value at any specific moment in time.

With illiquid investments like real estate, it may take an extended period of time before a sell can be closed at an attractive valuation (intrinsic value). With liquid investments such as stocks, a sell can be executed almost instantly, but not always at a valuation that represents the true worth of the business. Therefore, when I own a great business where the market is pricing it below my calculation of its intrinsic value, I never think of it as losing money. Instead, I simply recognize and accept the fact that my stock representing ownership of the business has become temporarily illiquid.

Temporary illiquidity will never stress me very much on a business that I have no intention of selling for many years to come. Since I am not interested in selling it currently, I have neither concern nor interest in what someone else might be willing to pay me for it today. On the other hand, I am keenly interested in the amount of income the investment is generating on my behalf, which is also where my focus lies. Of course, this specifically applies to dividend paying stocks, which currently represent the bulk of my portfolio. Therefore, I do not consider myself invested in the stock market, I consider myself invested in the “Dividend Income Market.”

20 Dividend Aristocrats: The Stock Market Perspective VS the Dividend Income Market Perspective

This brings me to the core thesis of this article. When most investors think about the stock market, they are primarily focused on what the prices of stocks and the stock market are doing. As the Brandes study cited above so aptly put it:

“In today’s information saturated world, investors tend to focus on financial items that tend to change rapidly (i.e., prices) rather than those that may be more stable, such as dividends.”

The primary thesis of this article is to point out that there is a different, albeit generally ignored, market that long-term oriented investors can, and I contend should, focus on. I am dubbing this the “Dividend Income Market” and in doing so, suggesting that long-term investors in this market focus on dividends instead of stock prices. By doing this, you will discover a market that does continuously increase where volatility is extremely low or even nonexistent.

As usual, I will utilize F.A.S.T. Graphs™, the fundamentals analyzer software tool in order to present my case. To accomplish this, I have chosen 20 prominent blue-chip Dividend Aristocrats that I will present from the perspective of the stock market based on stock prices versus the Dividend Income Market with a focus on dividends. In doing this, I will be presenting a litany of 60 graphs in all. Twenty of these graphs will present stocks through the volatile lens of stock price action. Twenty of these graphs will present stocks through the lens of consistently rising dividends with negligible volatility.

The final set of twenty graphs will present comprehensive performance reports where I will suggest that the reader analyzes the contribution that capital appreciation makes and the relative contributions that dividend bring to total return on each of these 20 blue chips. Dividend growth rates and payout ratios should also prove interesting to examine.

Finally, I acknowledge that there is a level of redundancy with this exercise. However, I would also suggest that there are specific lessons about investing in general, as well as the contributions of capital growth and dividend income that are unique to each of these examples. And of course, there is the important role that valuation plays regarding the creation of long-term performance. Therefore, I will also provide very brief commentary to elaborate and illuminate on some of the uniqueness found with some of these examples.

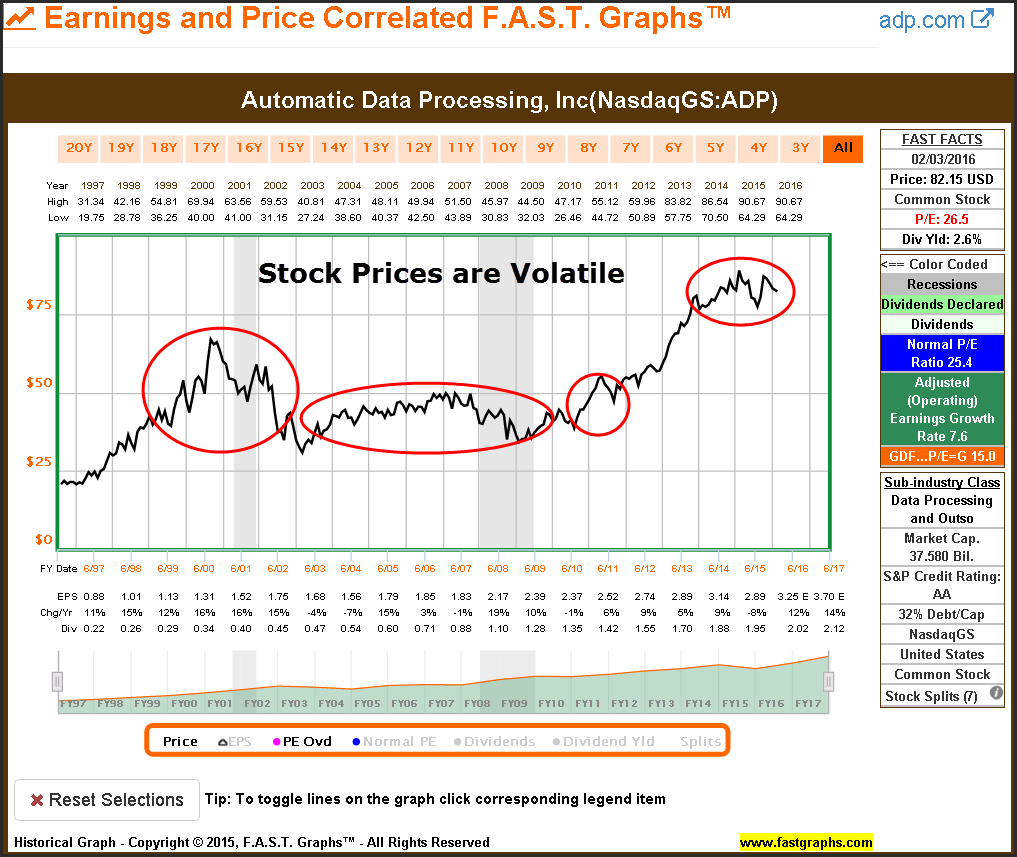

The Stock Market: Automatic Data Processing, Inc. (ADP)

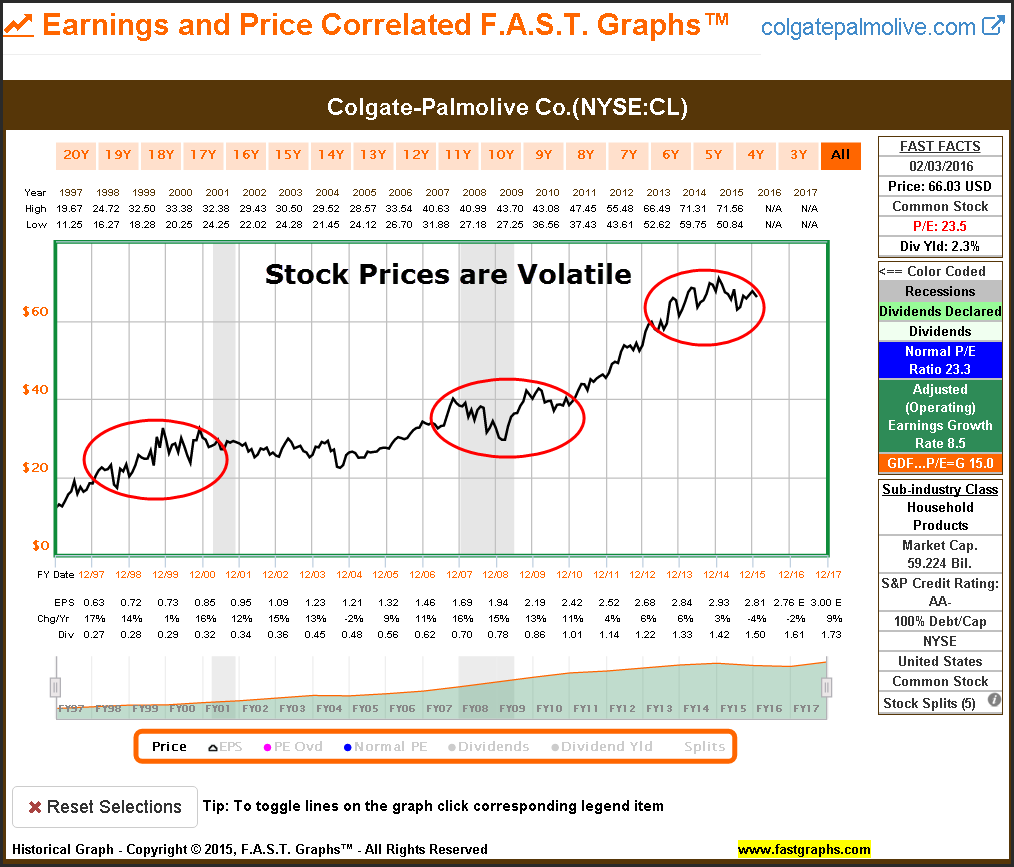

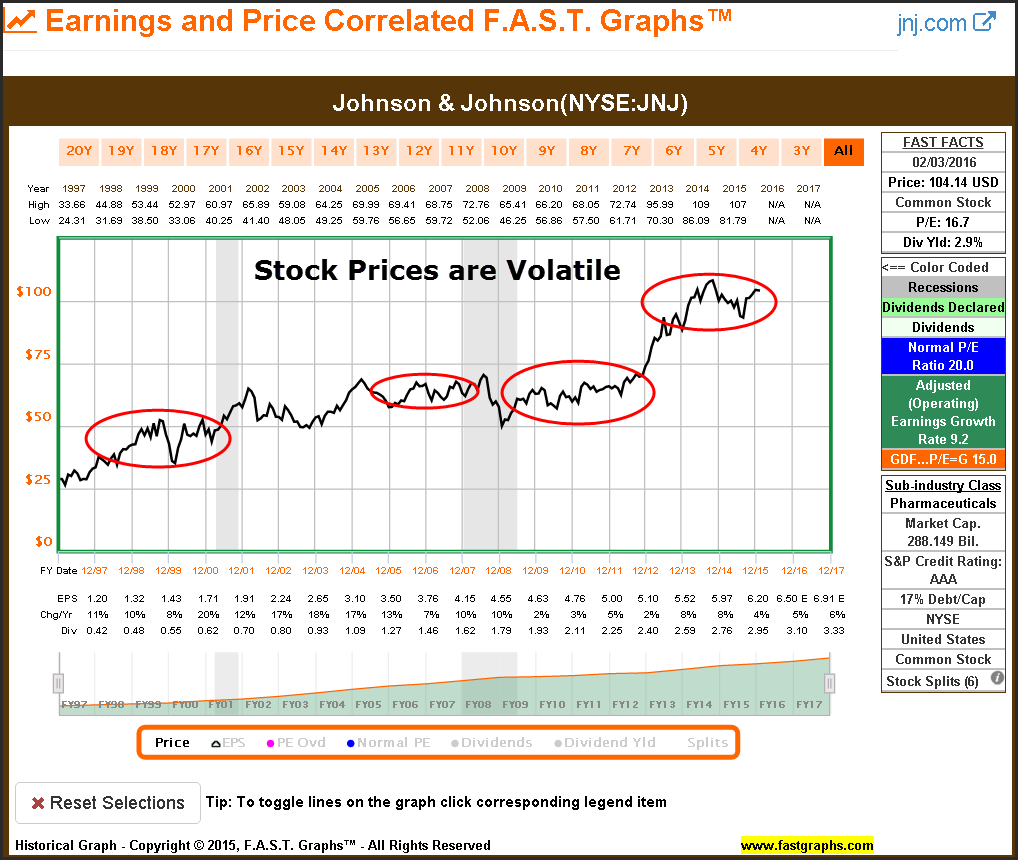

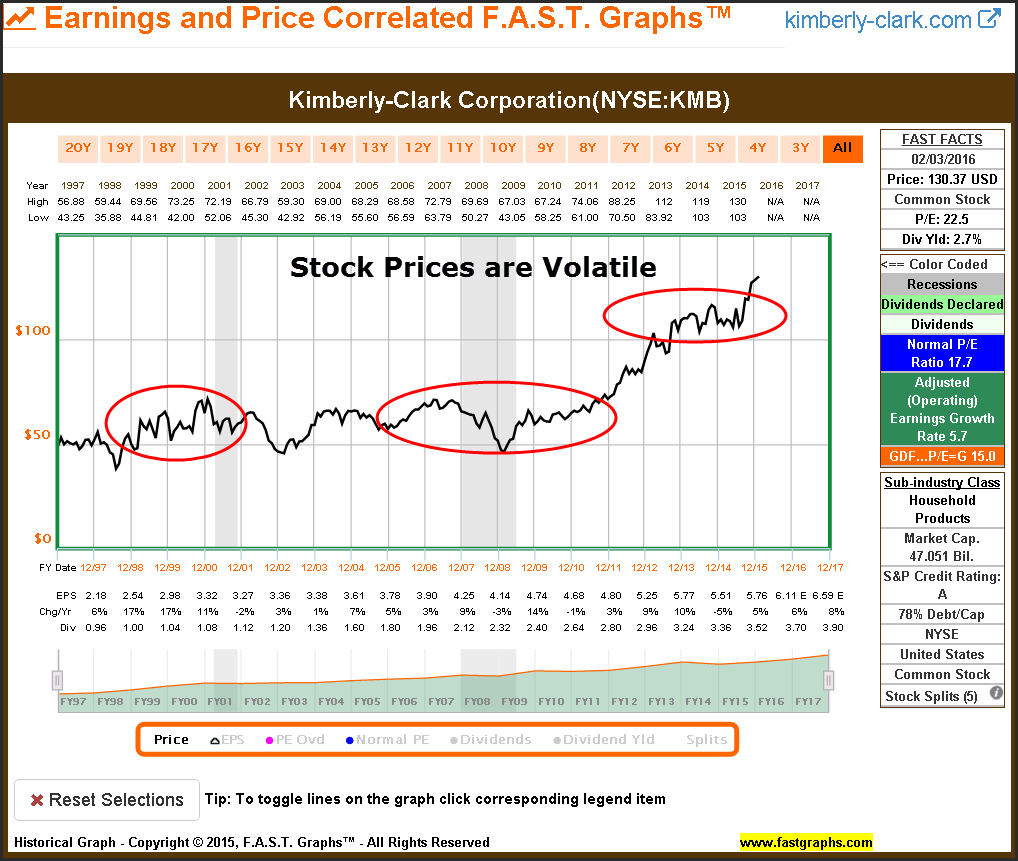

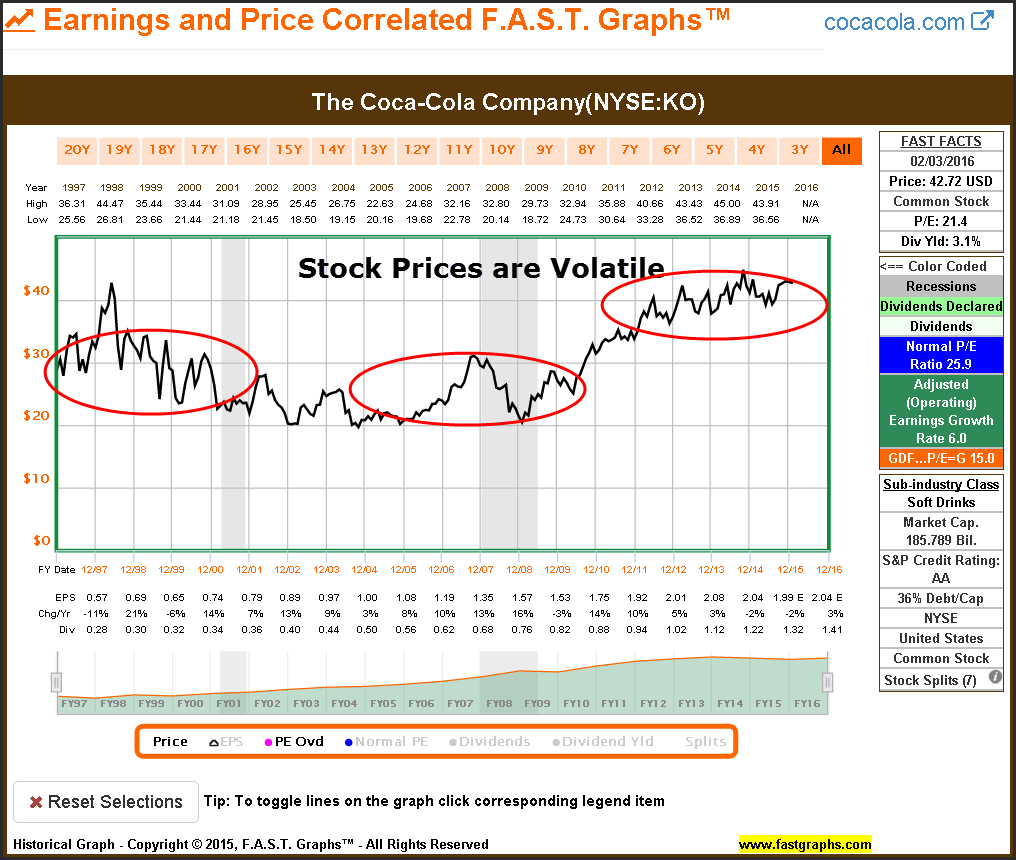

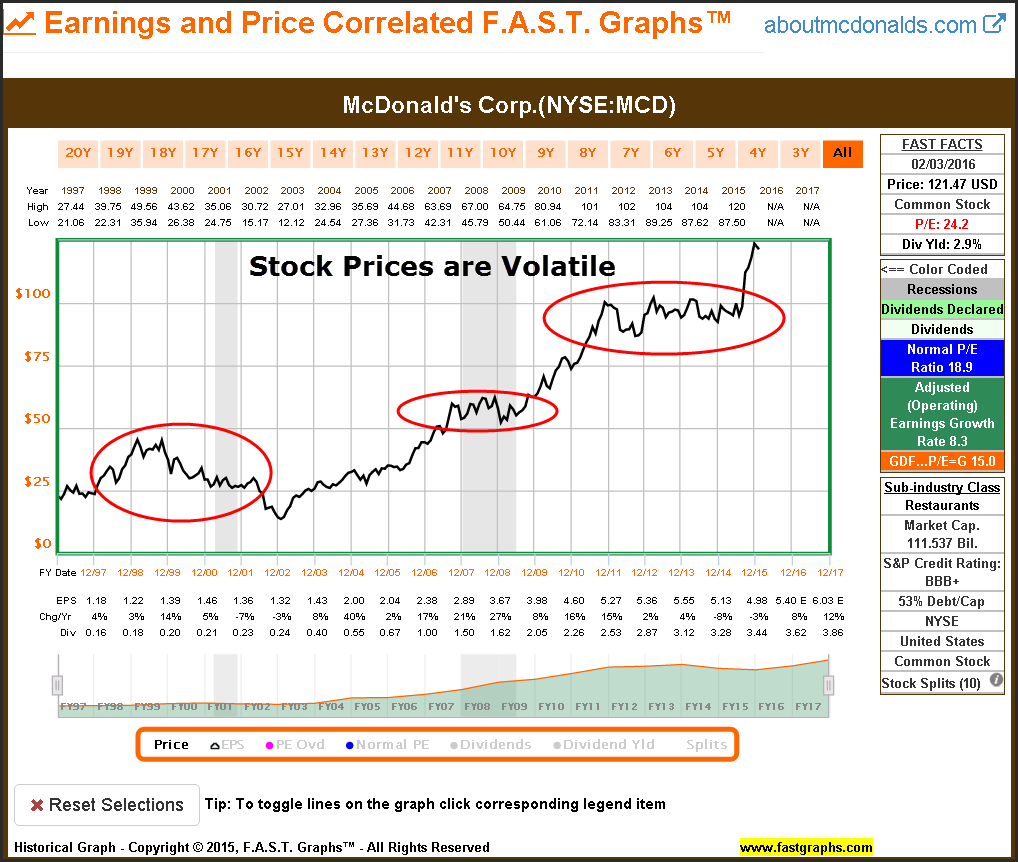

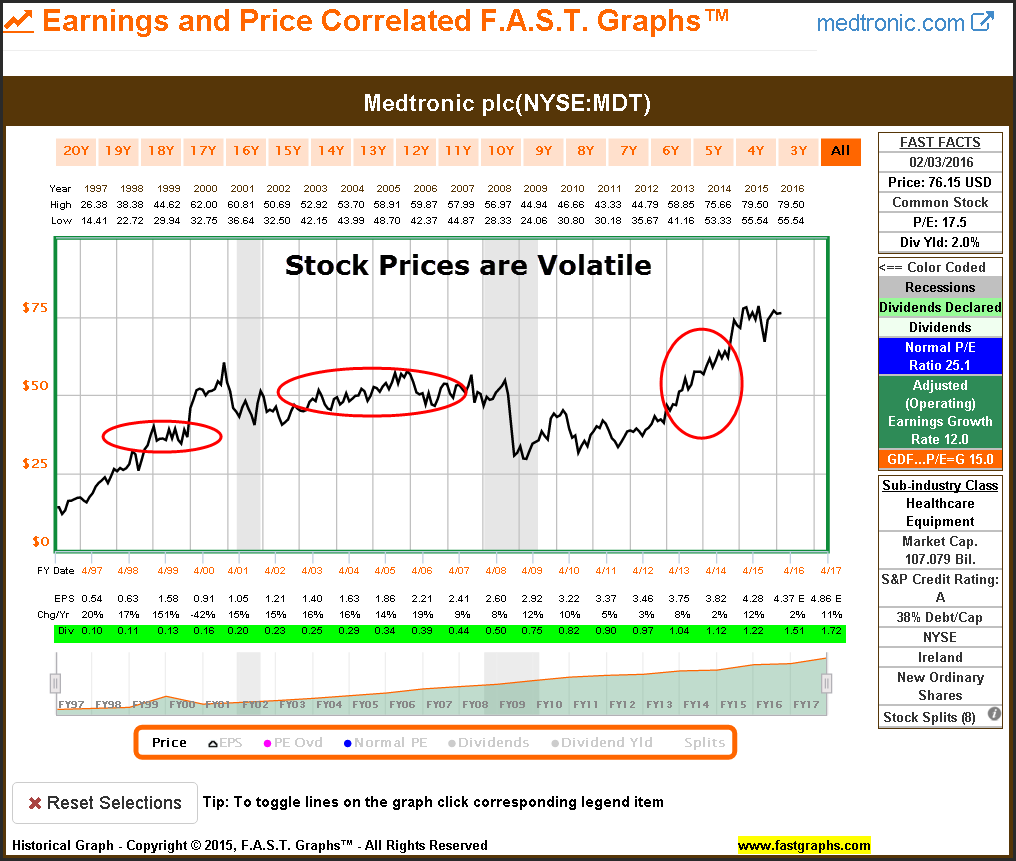

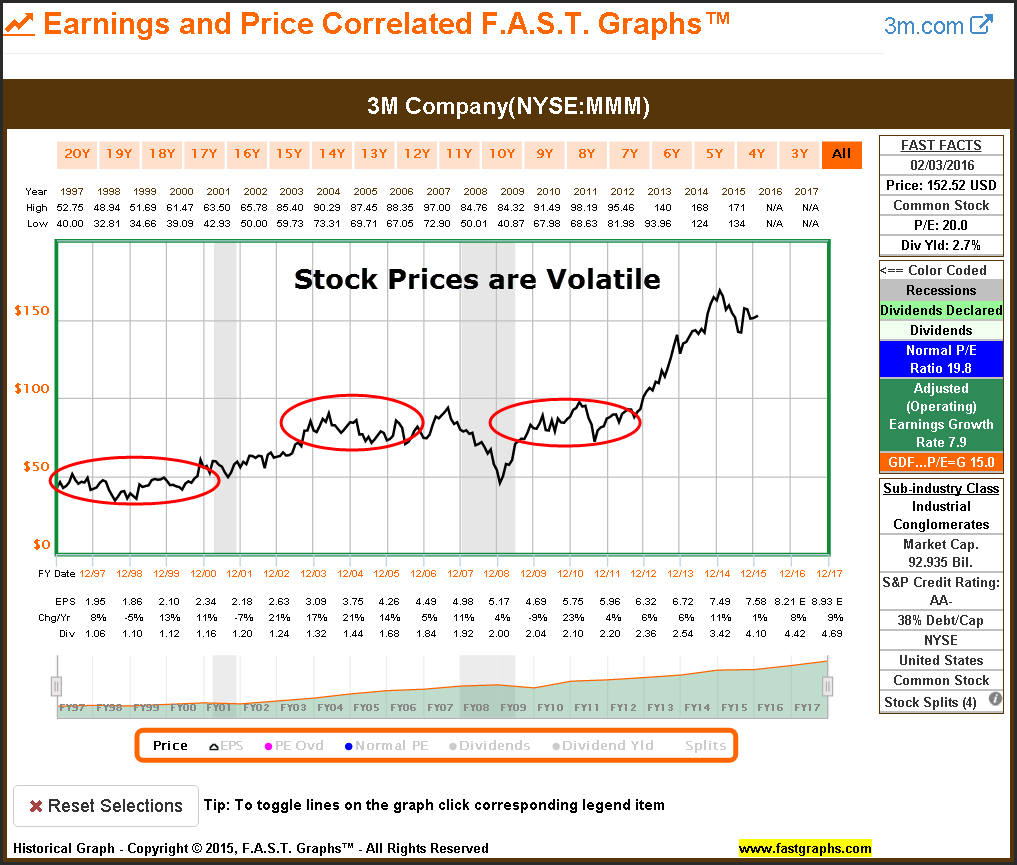

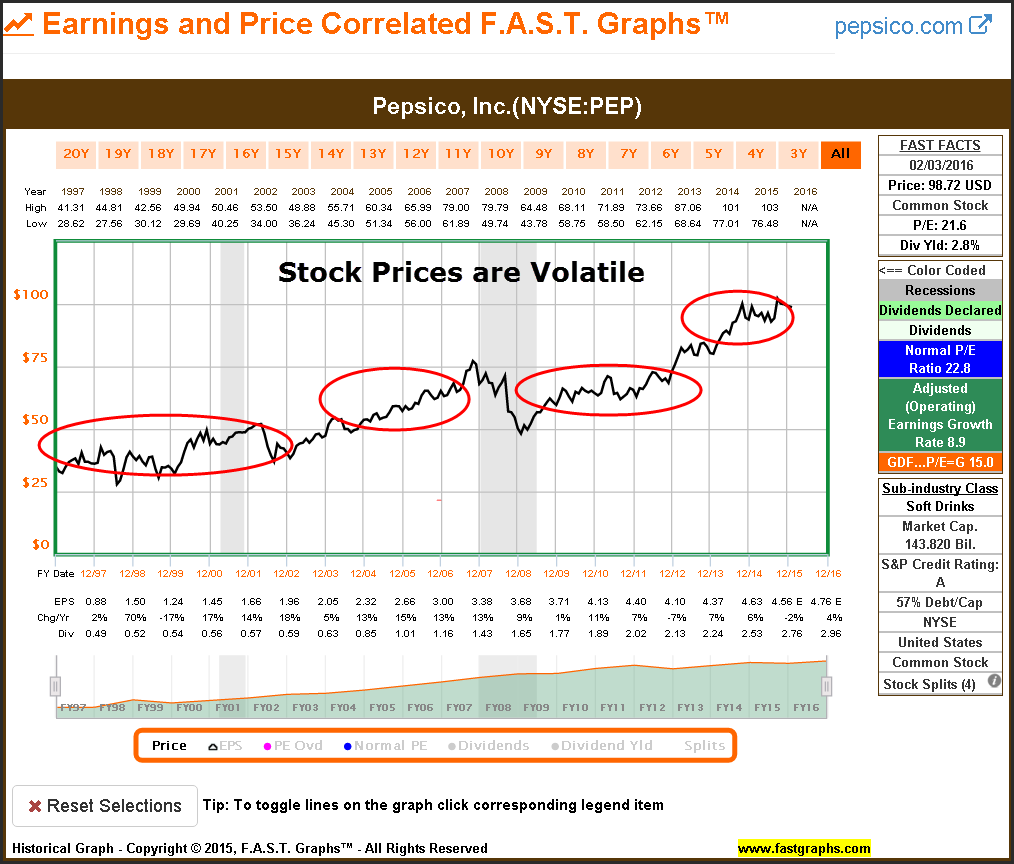

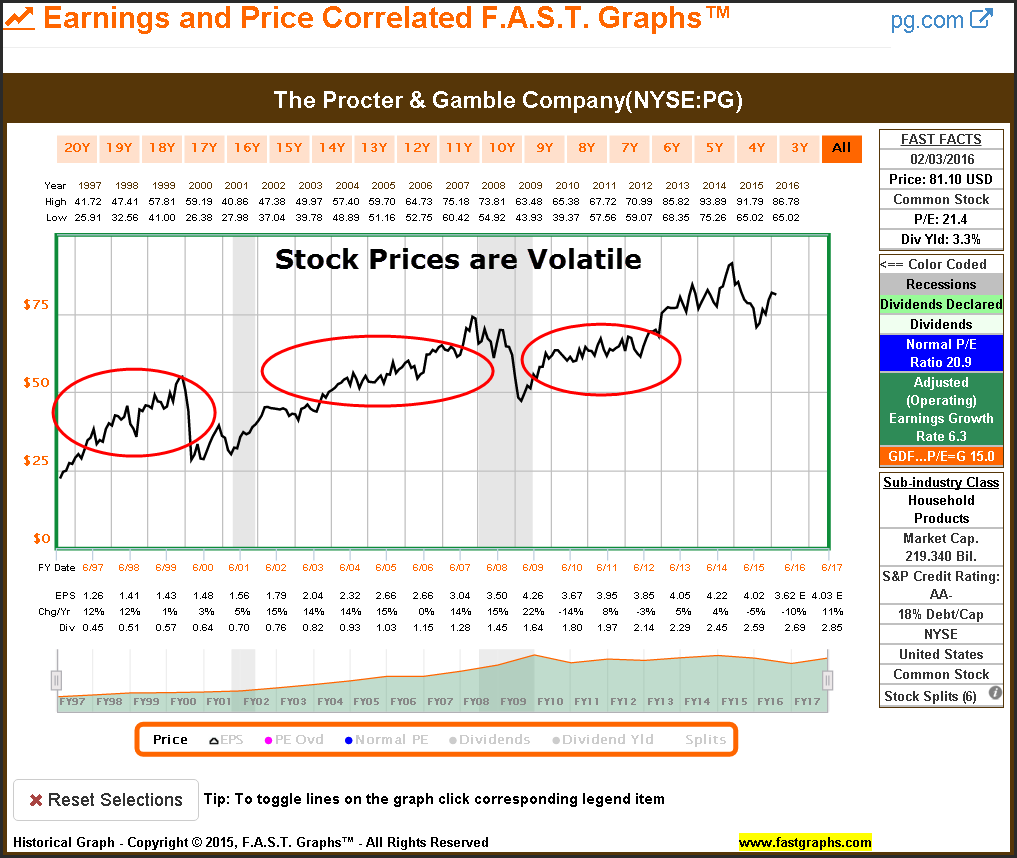

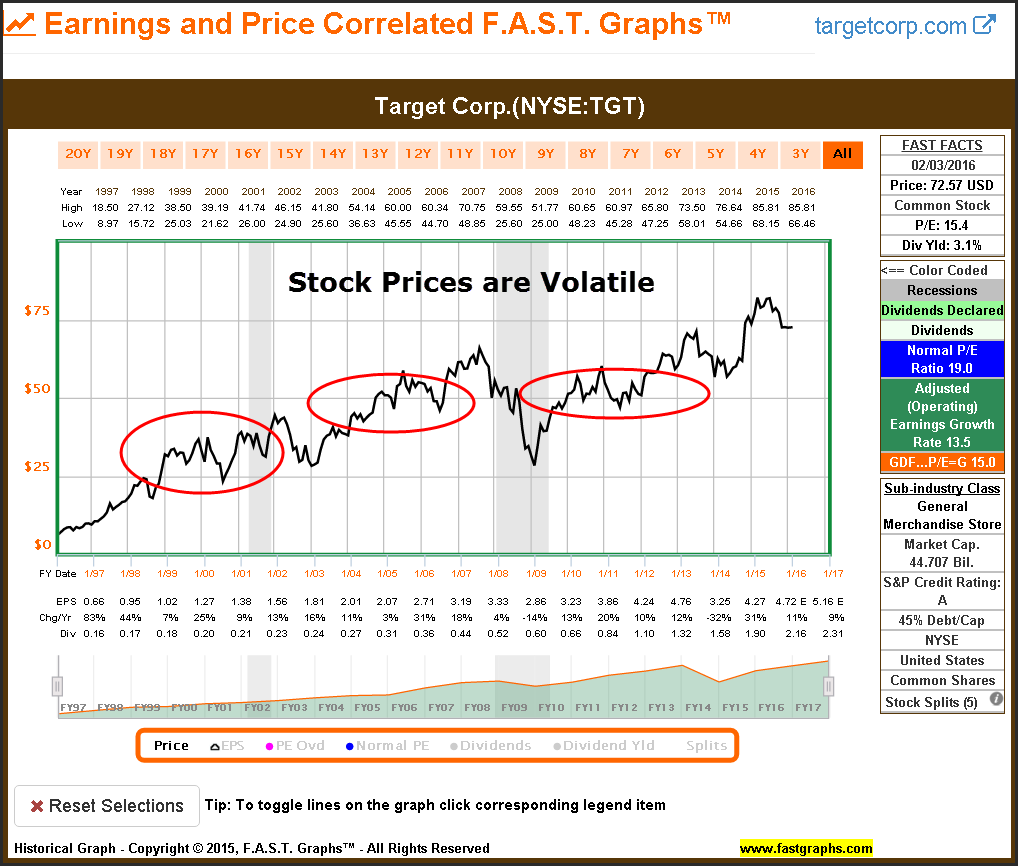

When Automatic Data Processing is looked at from the perspective of the stock market we discover several timeframes with troubling bouts of price volatility. When looked at solely from this perspective, it is easy to see how stock price movements can cause anxieties.

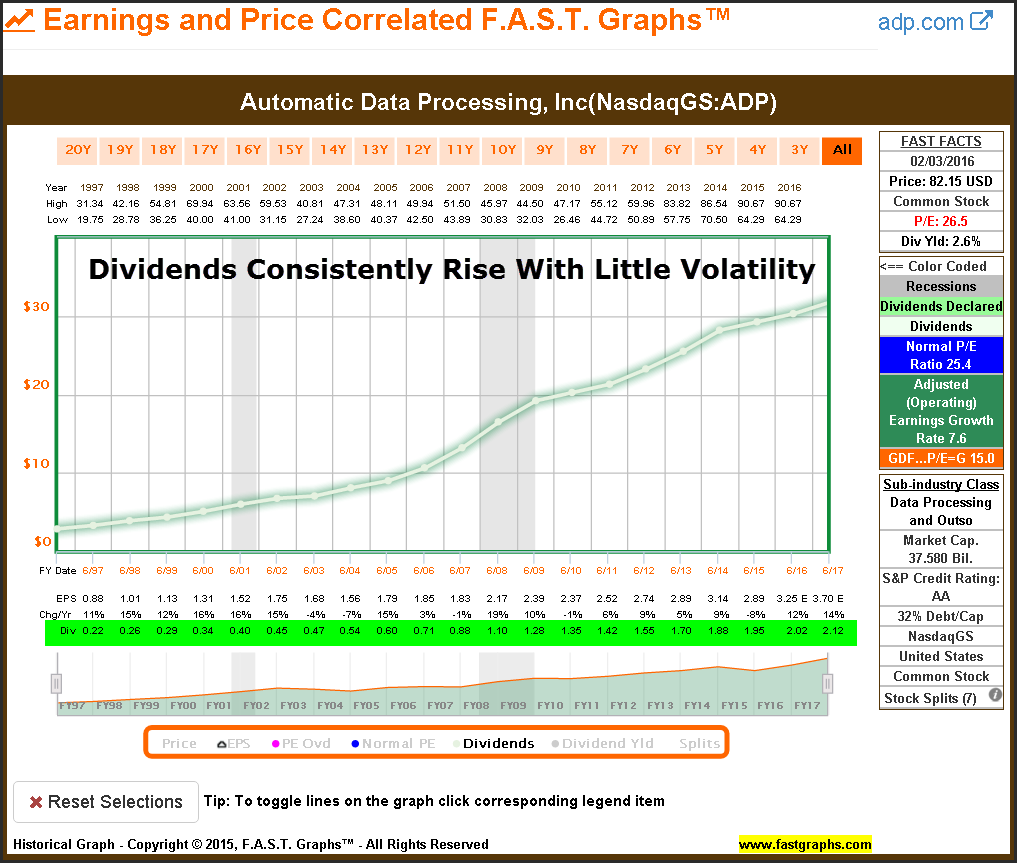

The Dividend Income Market: Automatic Data Processing, Inc.

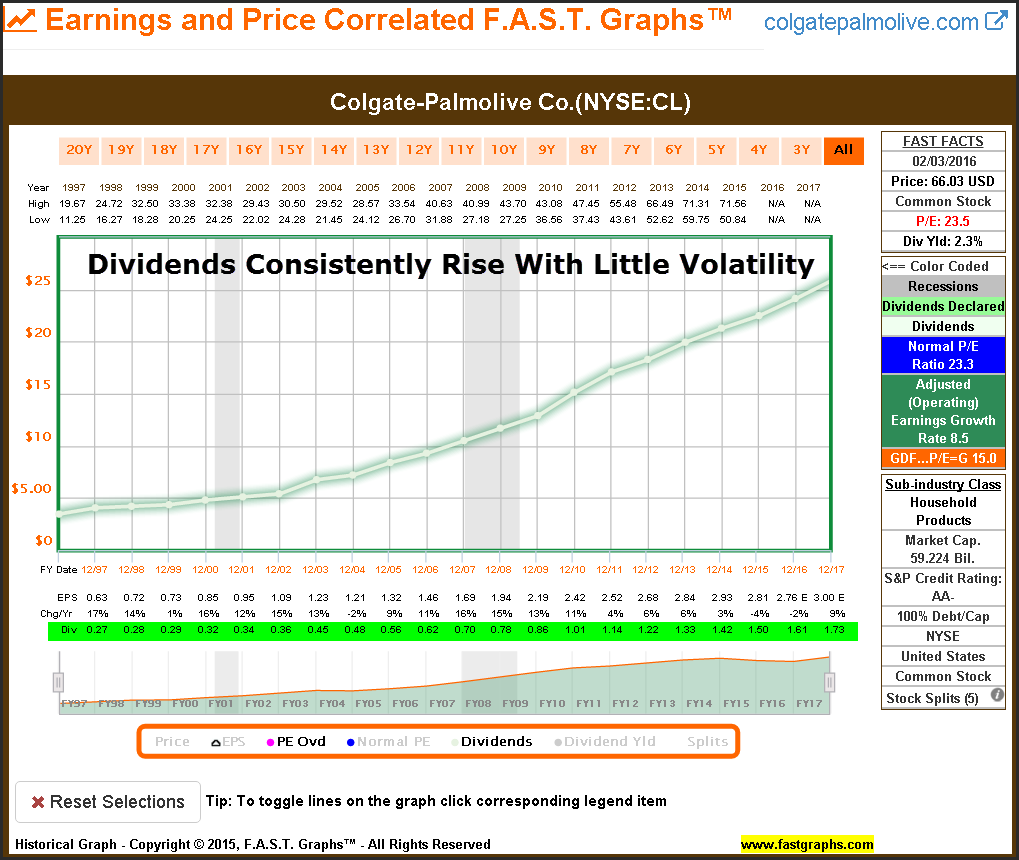

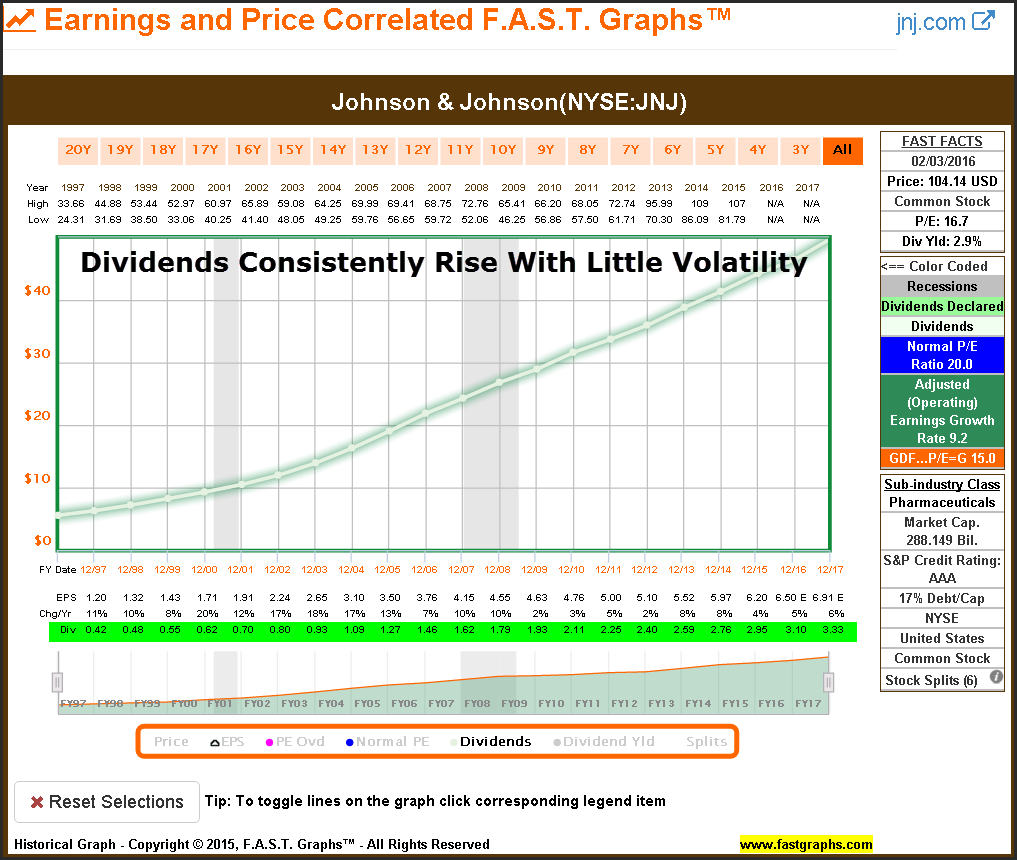

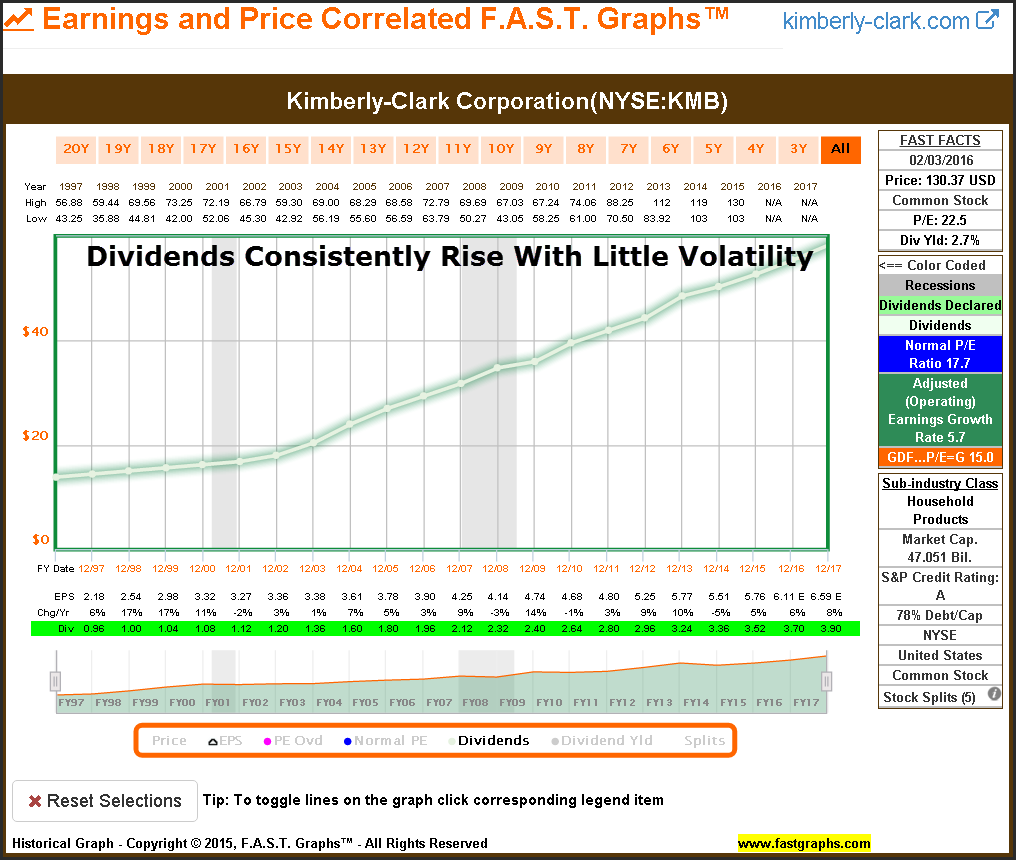

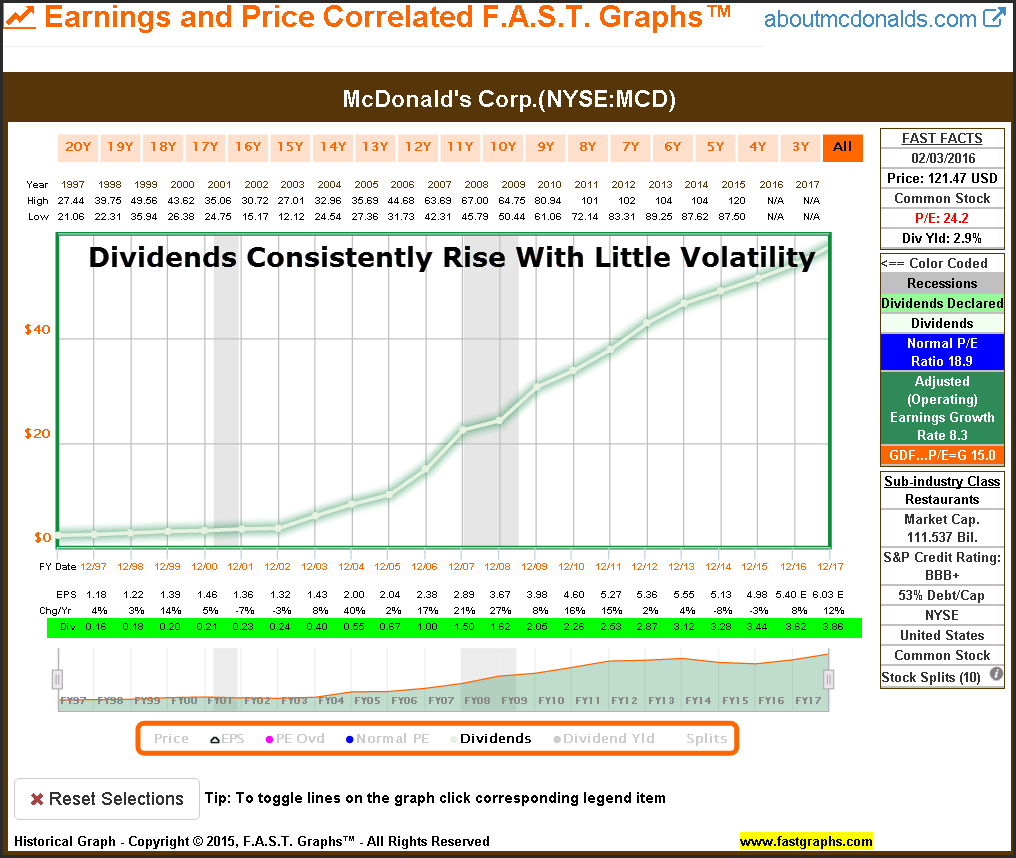

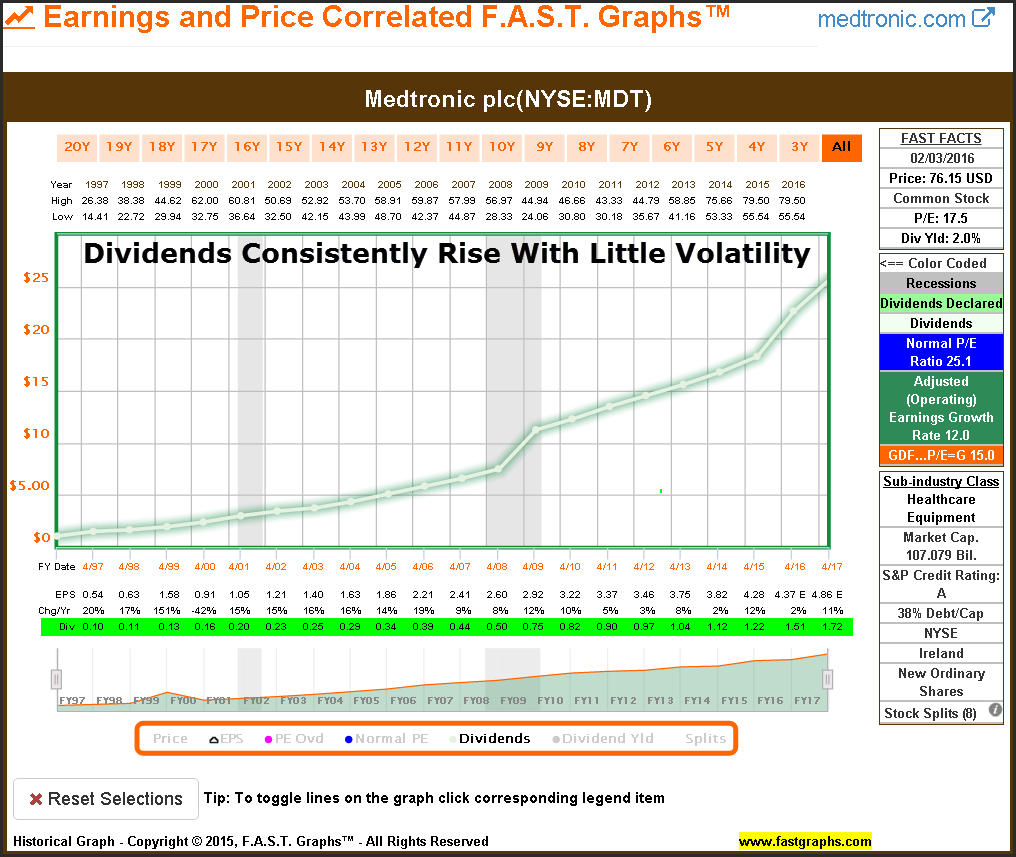

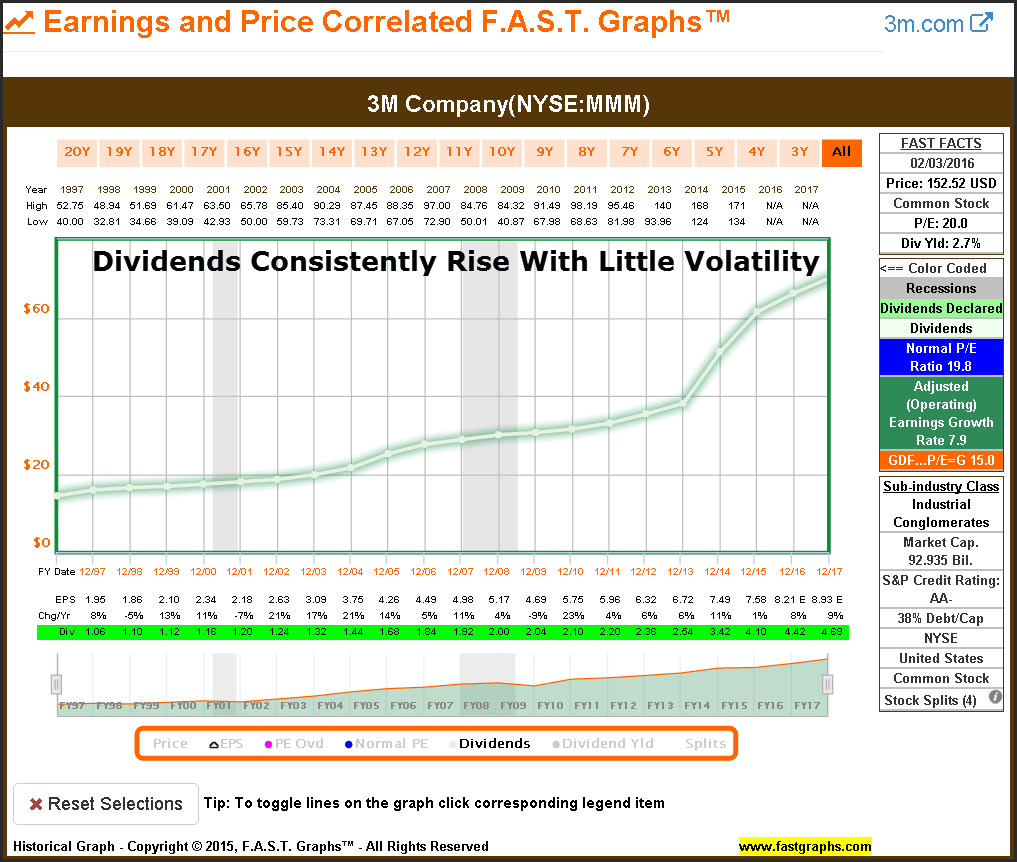

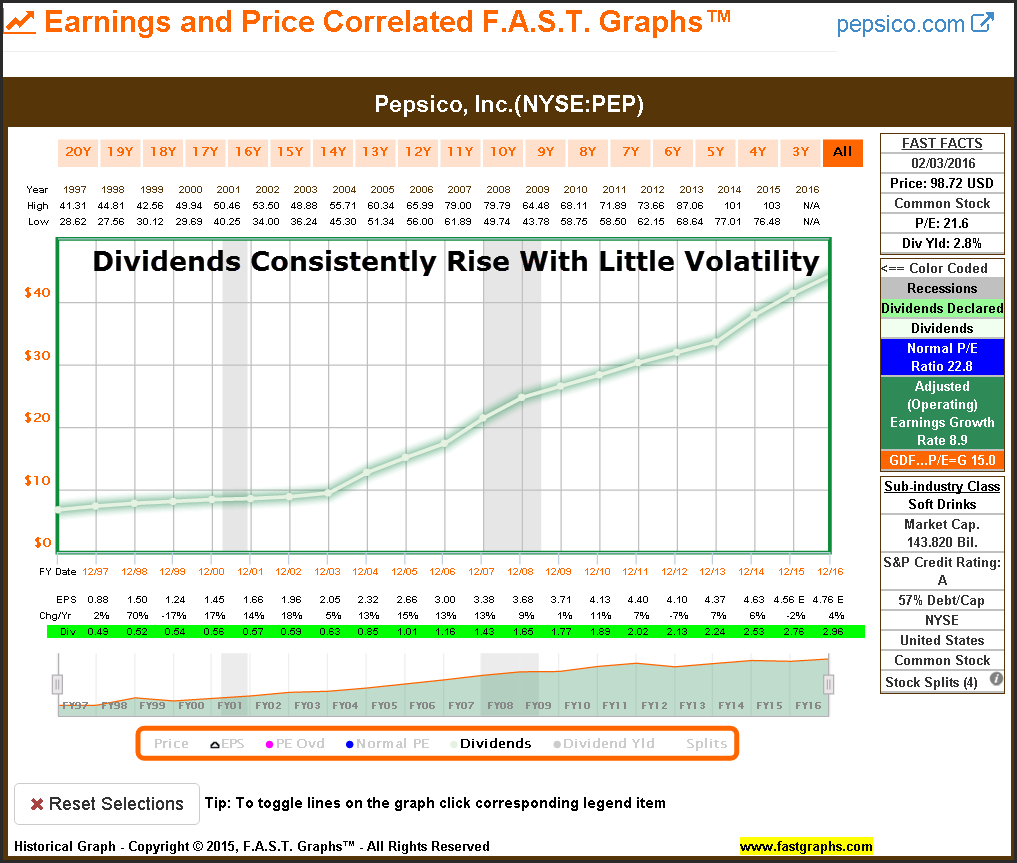

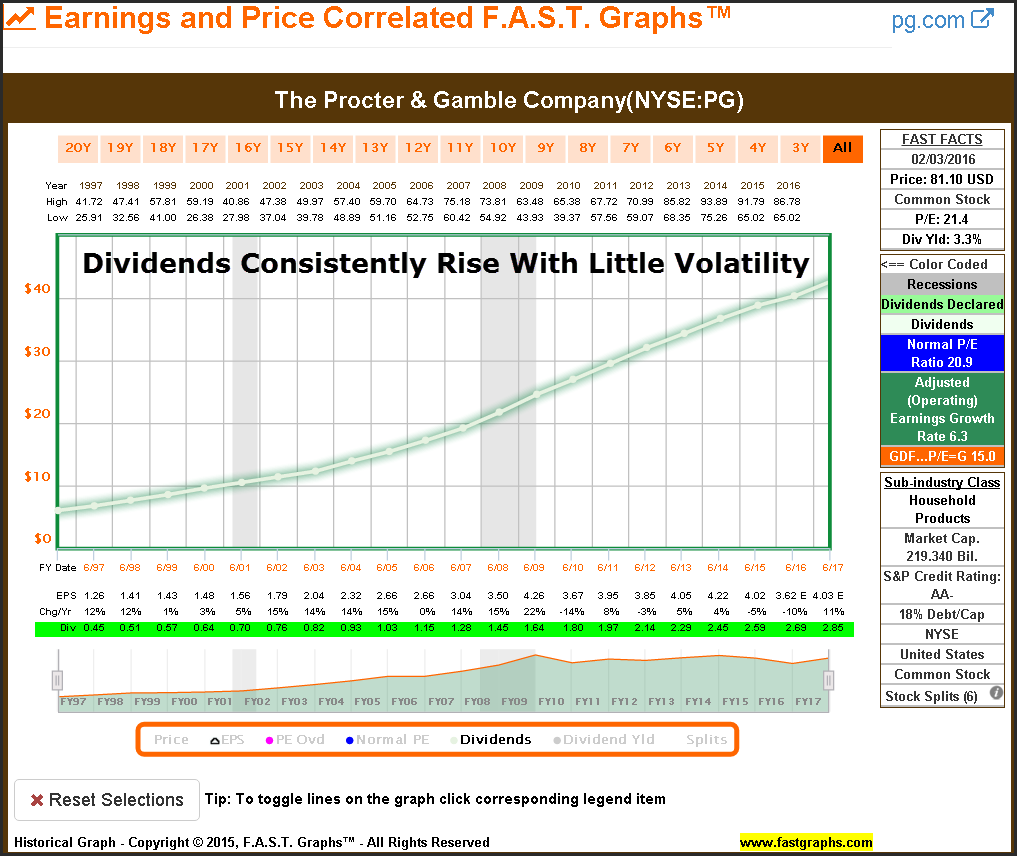

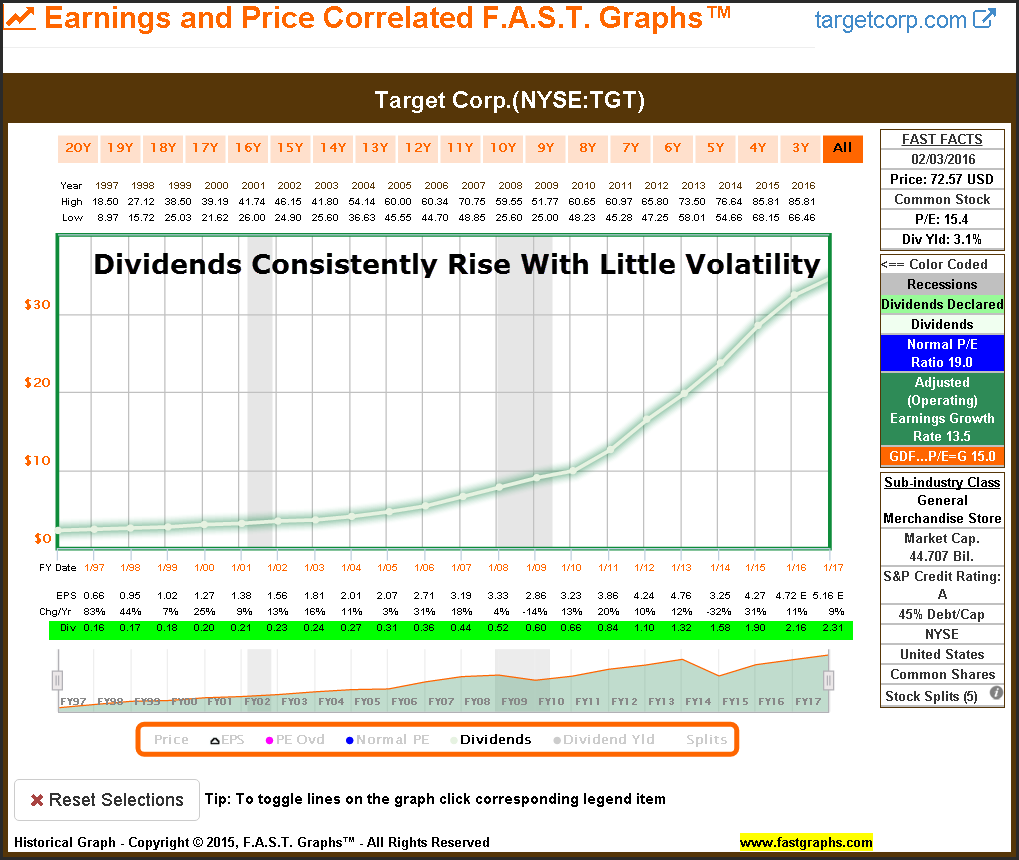

In contrast, when Automatic Data Processing is looked at through the lens of the “Dividend Income Market” we see the steadily increasing dividend value with very little volatility involved. Just as it will apply to all future examples, this is where the money comes from to pay the bills on an ongoing basis. I contend that this market is much more important to the long-term oriented investor, and therefore, where their focus should rest.

Maintain the same perspectives with each of the other examples that follow. Notice how nervous stock prices are over time and consider how much anxiety this volatility might bring in the short run when examining each company via the stock market. Then notice how much more consistent the dividend income is over time, how it continuously increases, and how calming it would be if that is where your focus was more appropriately placed.

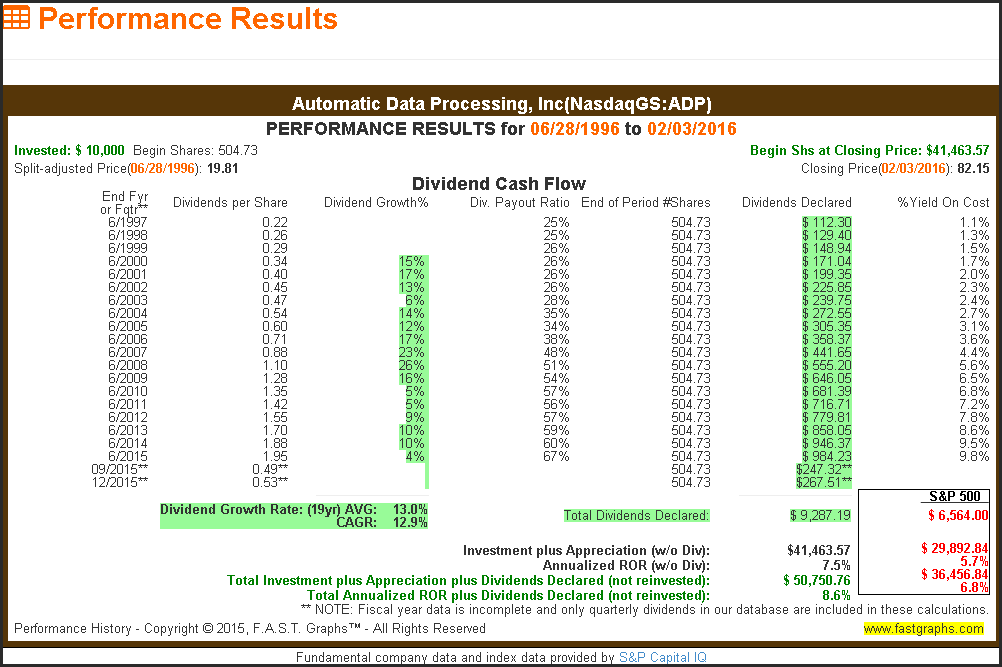

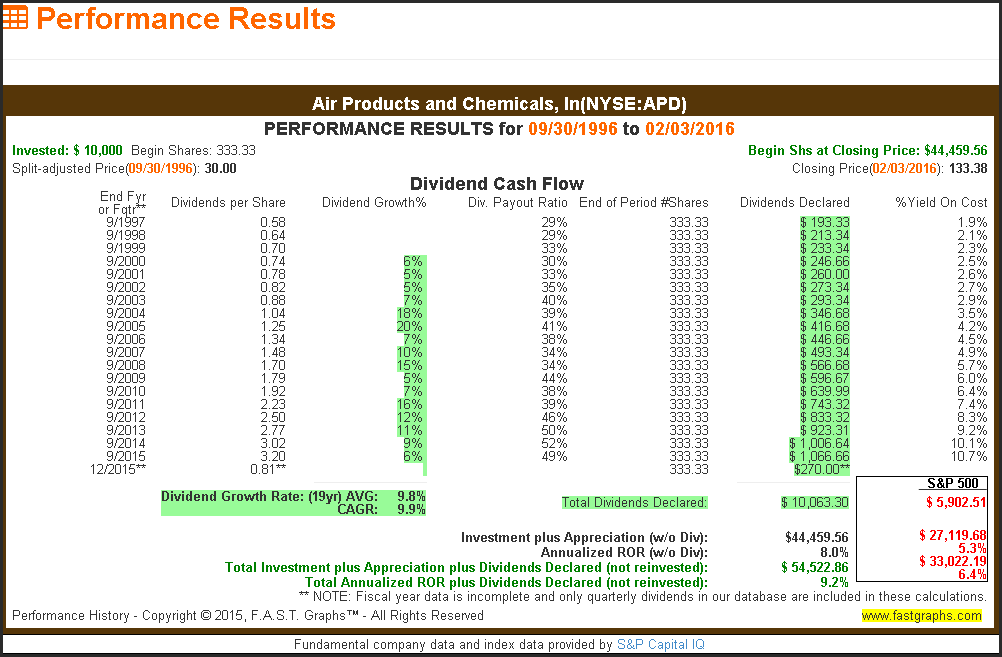

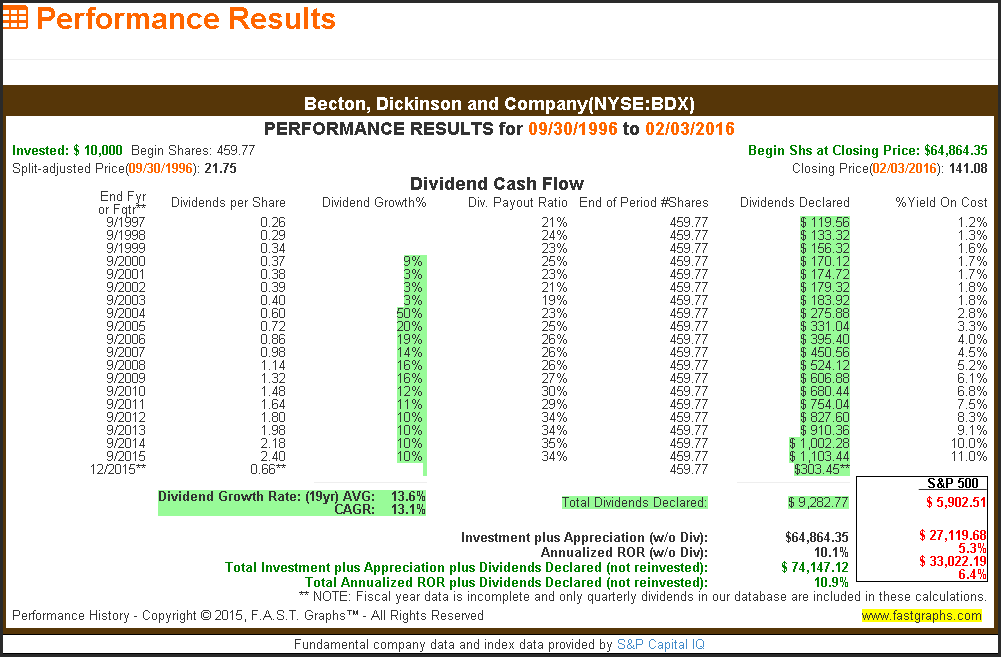

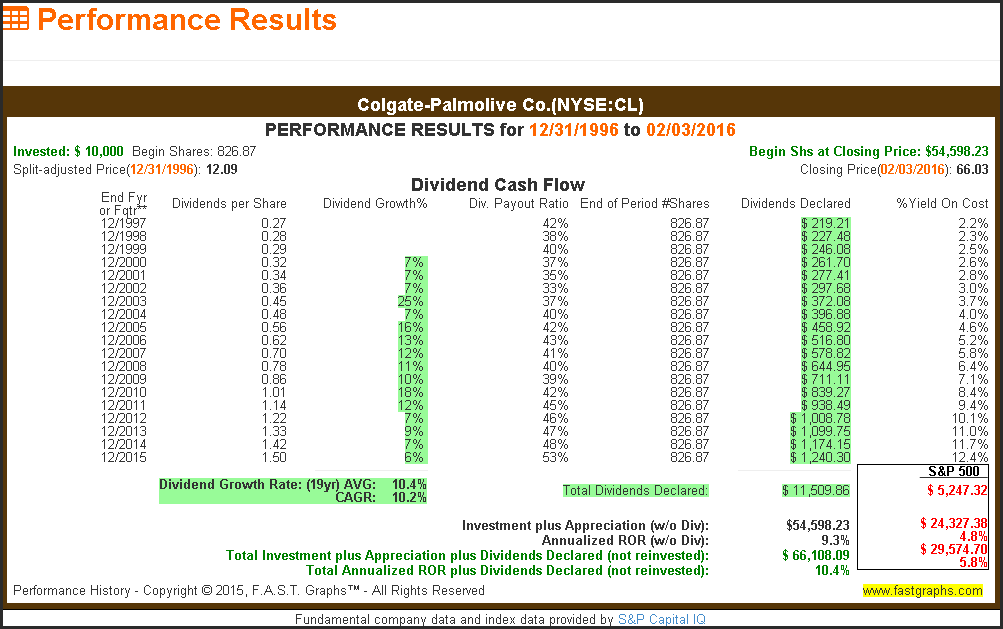

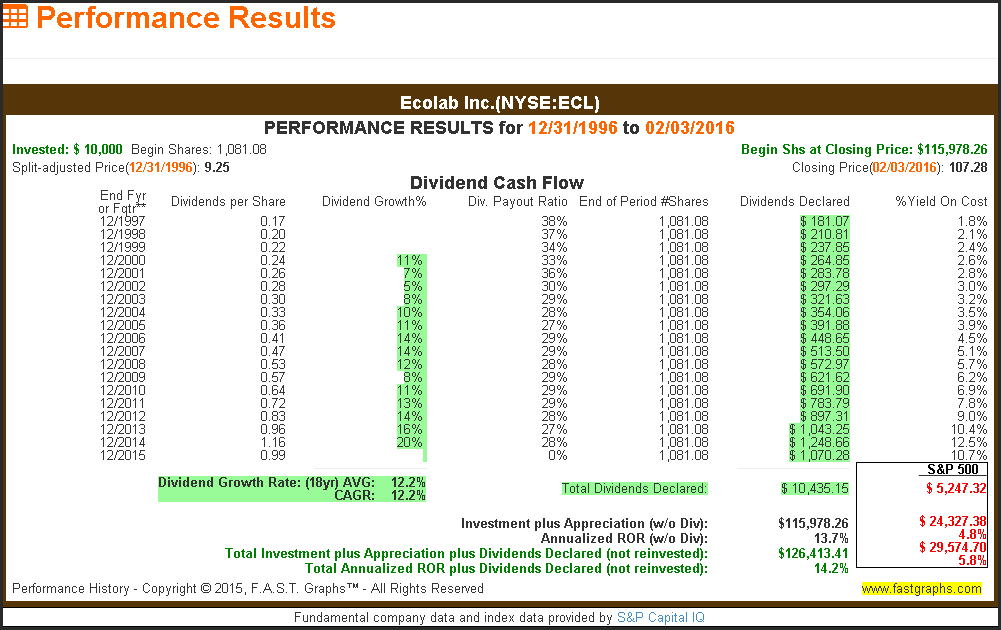

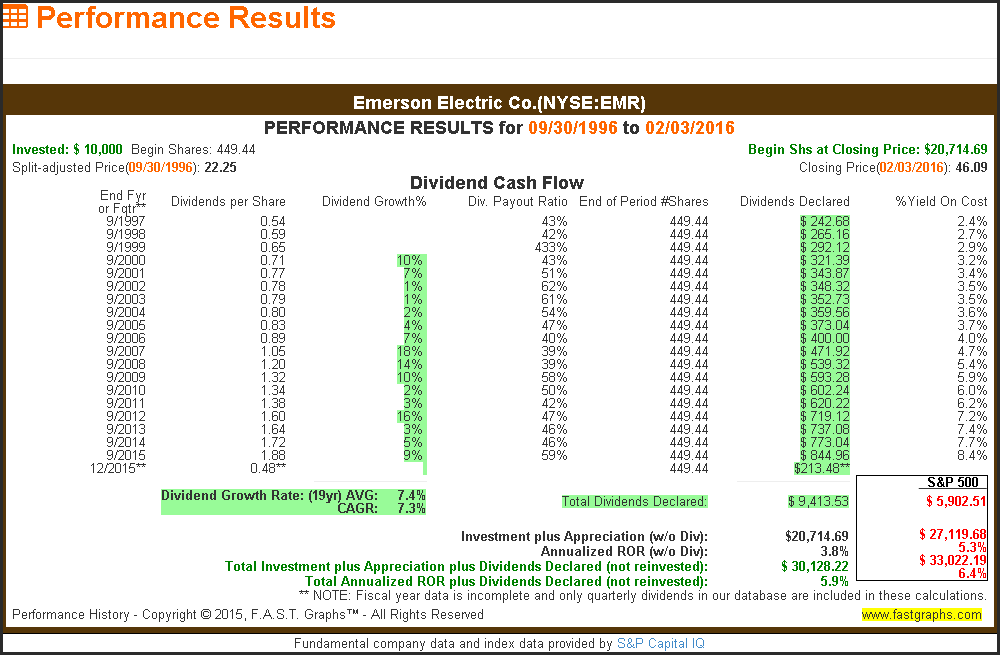

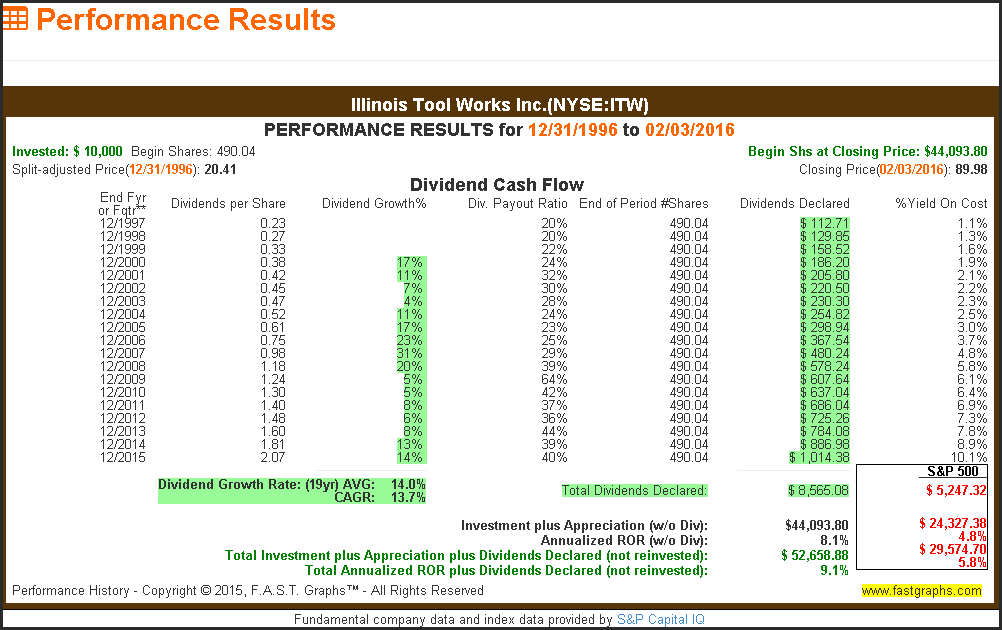

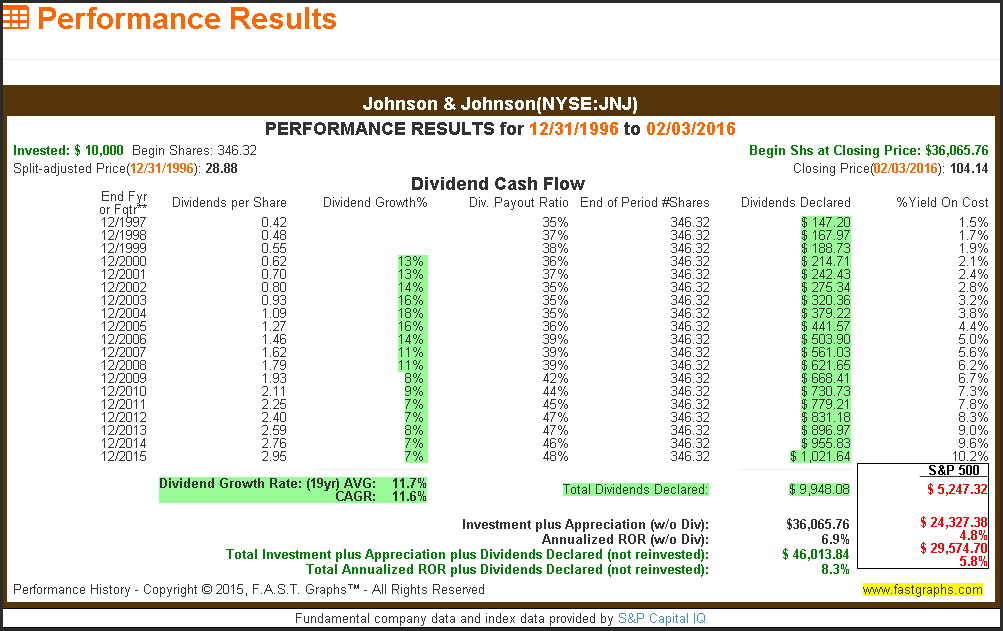

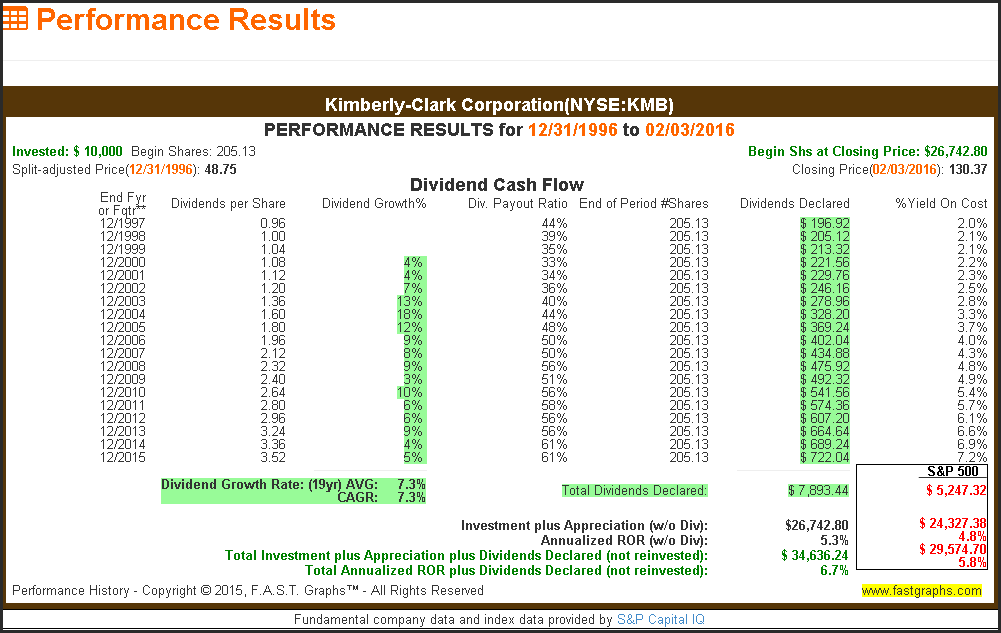

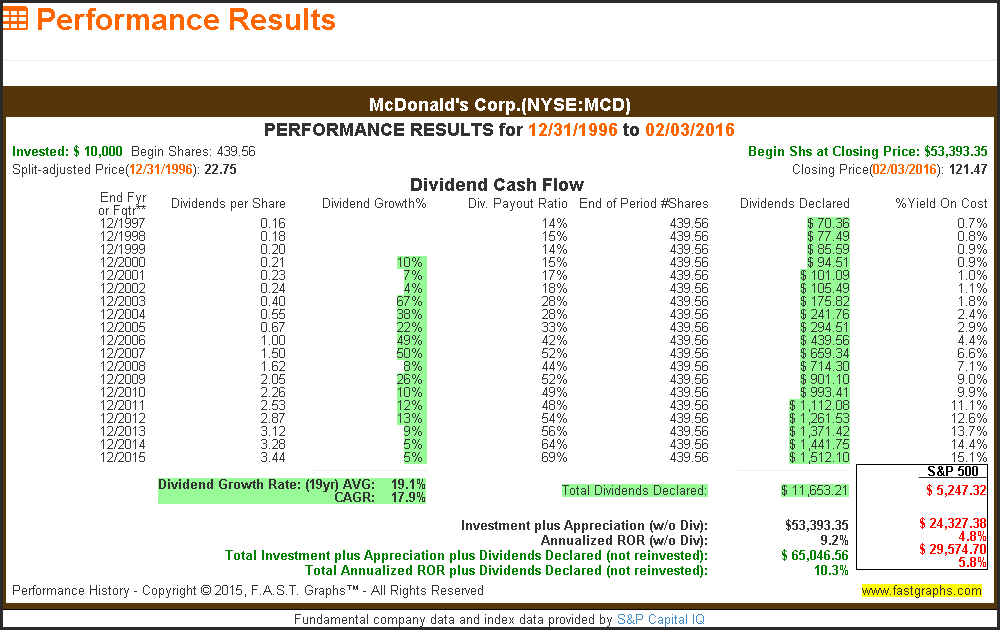

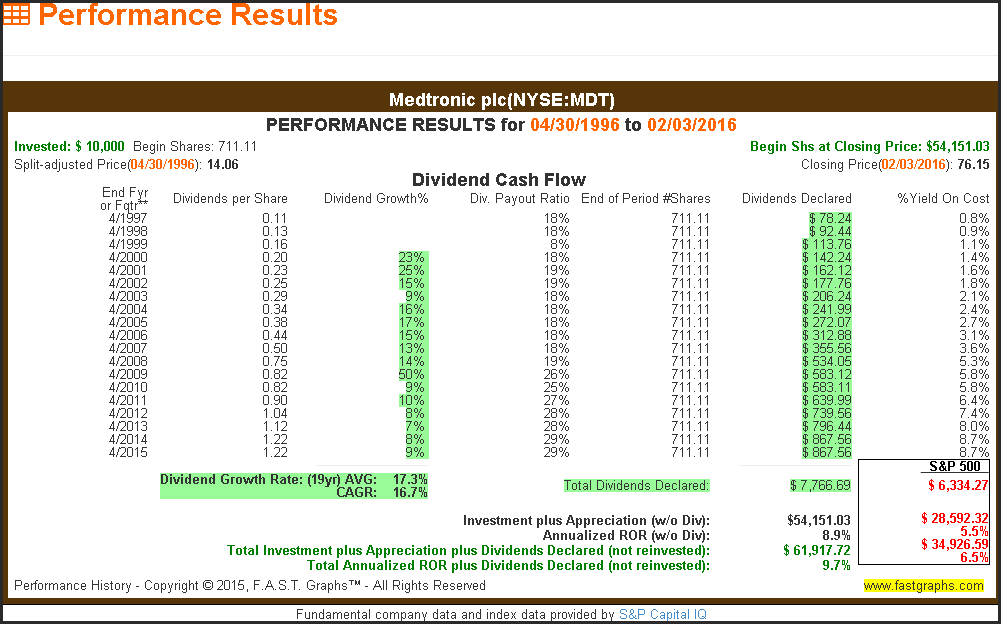

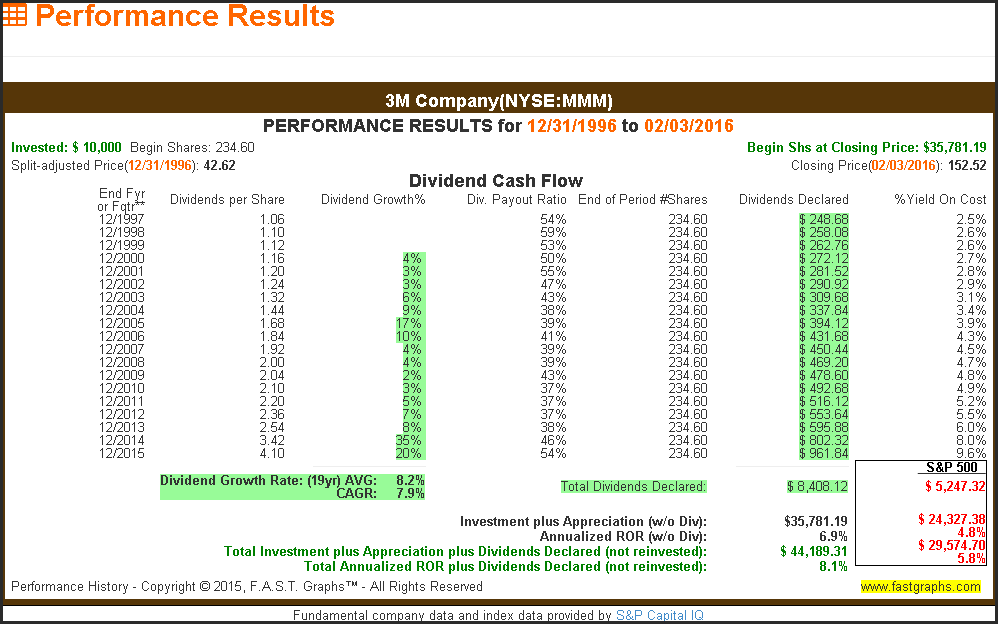

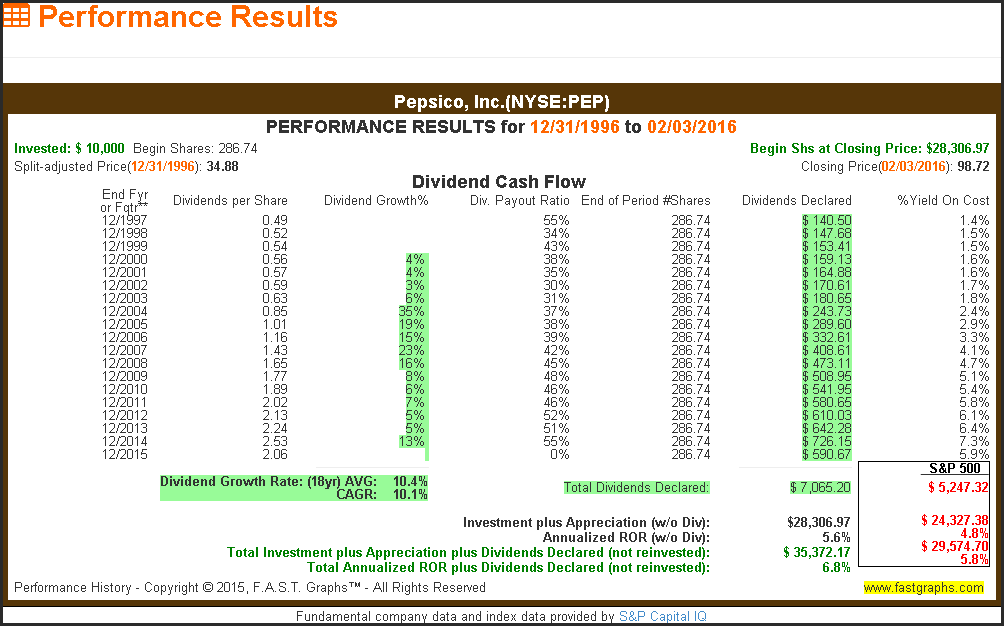

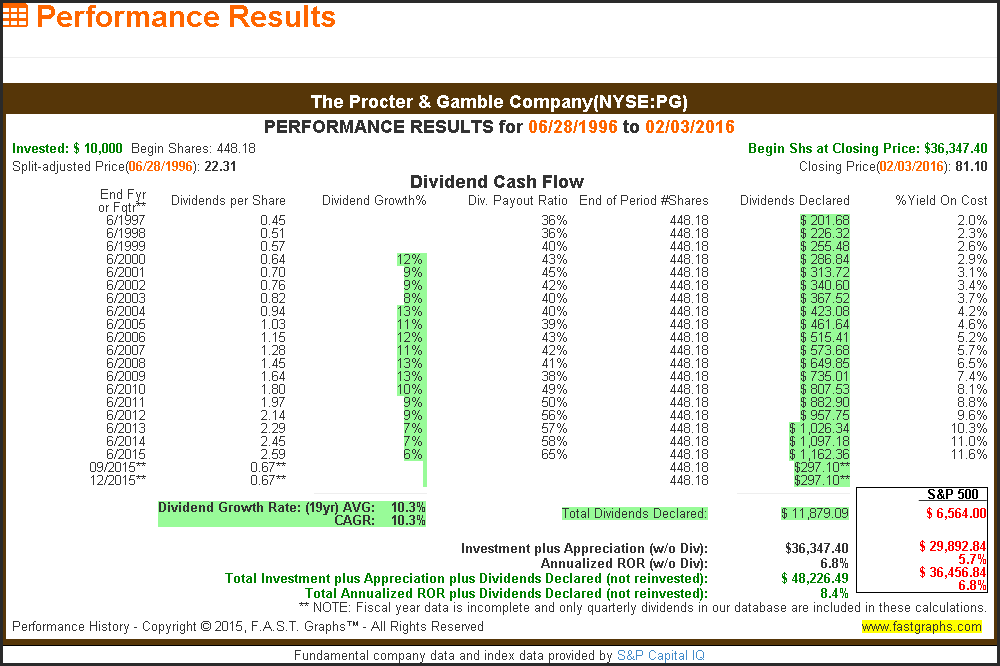

When reviewing the long-term performance of Automatic Data Processing, we discover some important and interesting facts. This performance (and all performance reports that follow) are based on a one-time $10,000 investment at the beginning of the timeframe measured. With this first example we see $9,287.19 of cumulative dividend income and $31,463.57 of capital gain. Therefore, dividends represented approximately a third of the return, but capital appreciation was the dominant contributor.

To save the reader from excessive additional verbiage, I suggest that the performance of each of the following examples be evaluated in the same manner. Note how much return came from dividends versus how much return came from capital appreciation. When calculating capital appreciation, remember to deduct the original $10,000 investment from the total.

Going through this exercise on each of the following examples will provide a clear perspective of the contributions from dividends versus capital appreciation. However, I will add some additional commentary on a few of the following examples that I believe warrant special considerations.

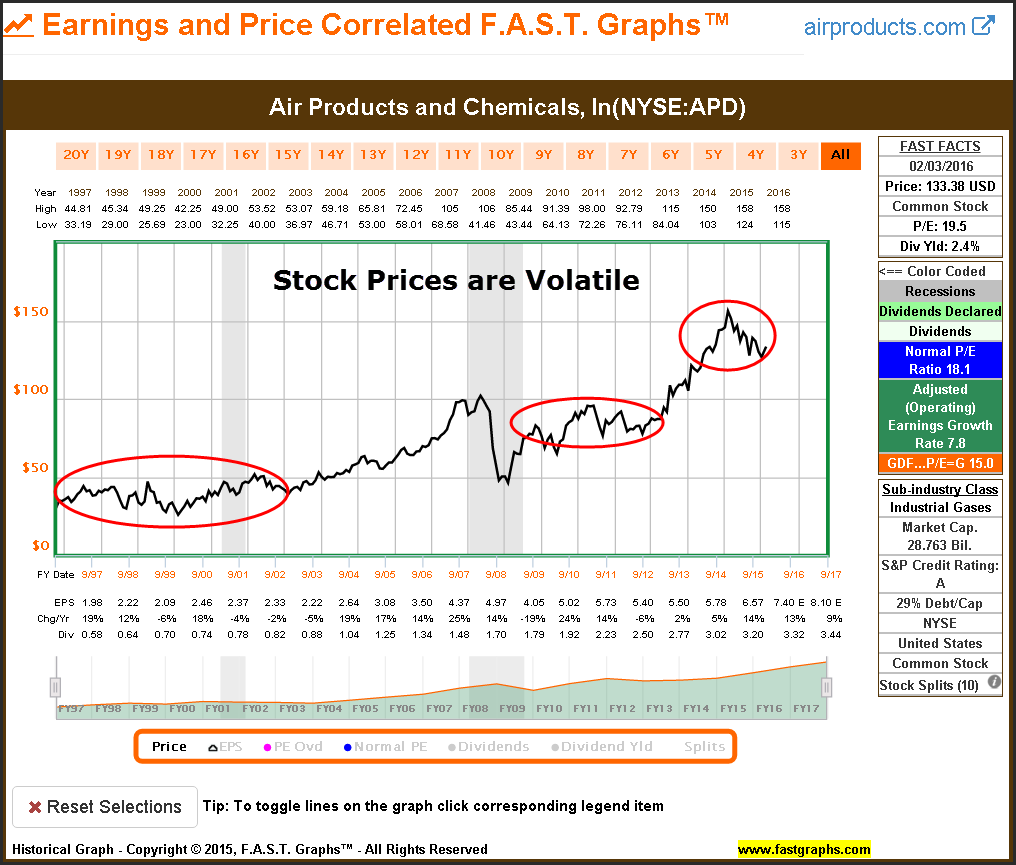

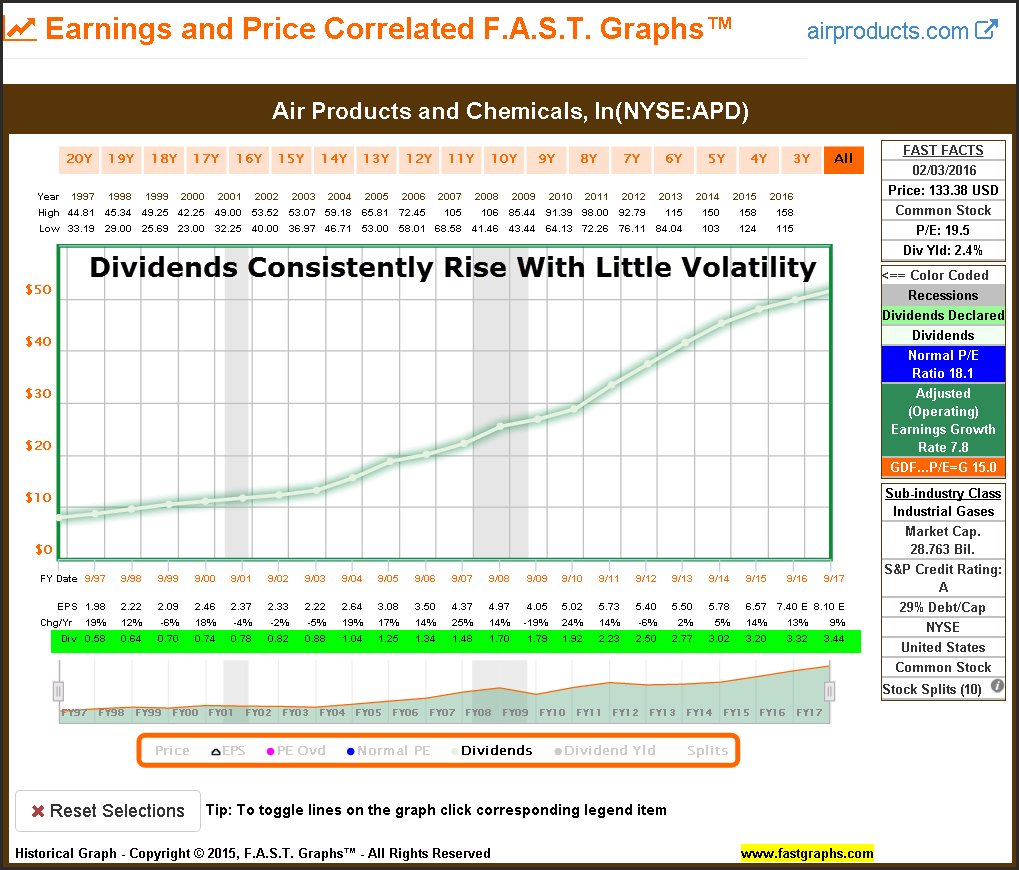

The Stock Market: Air Products and Chemicals, Inc. (APD)

The Dividend Income Market: Air Products and Chemicals, Inc.

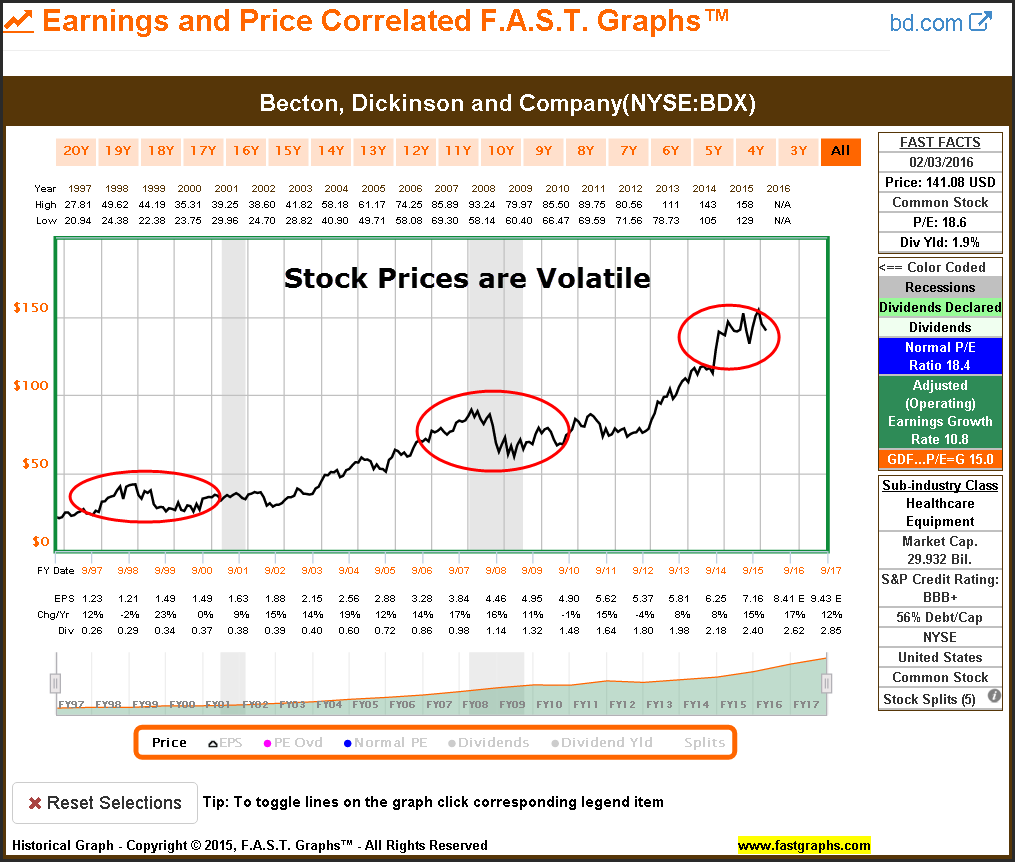

The Stock Market: Becton Dickinson and Company (BDX)

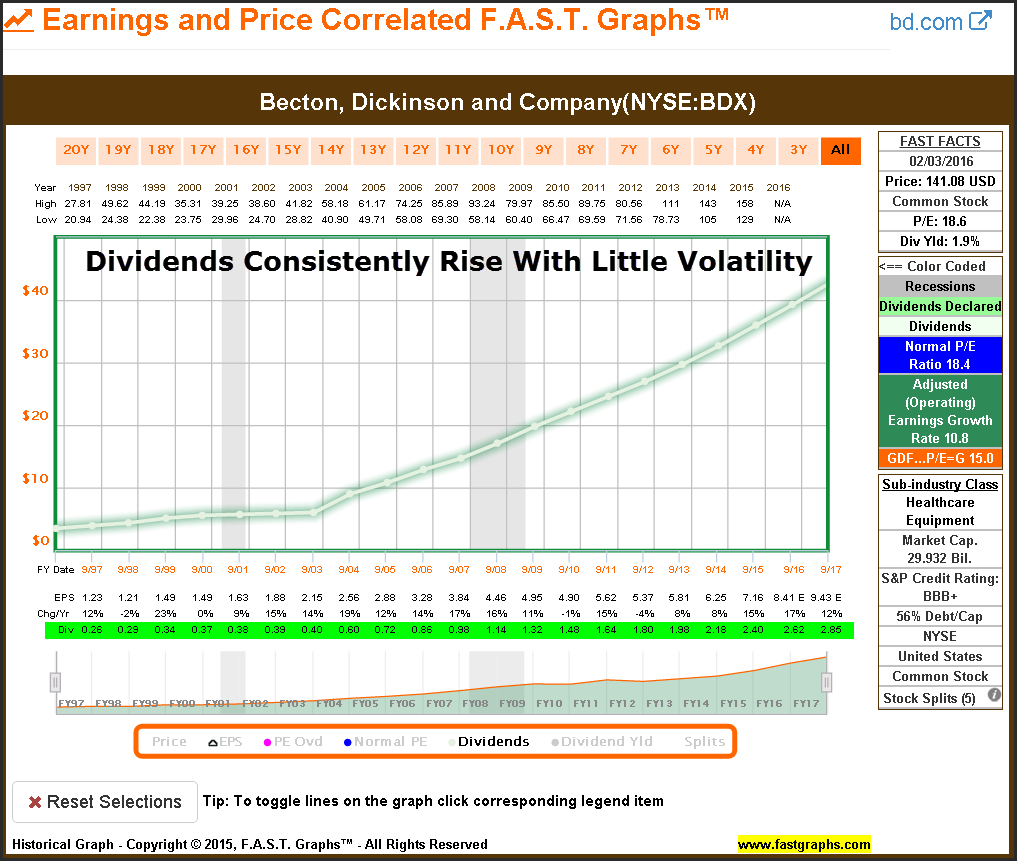

The Dividend Income Market: Becton, Dickinson and Company

The Stock Market: Colgate-Palmolive Company (CL)

The Dividend Income Market: Colgate-Palmolive Inc.

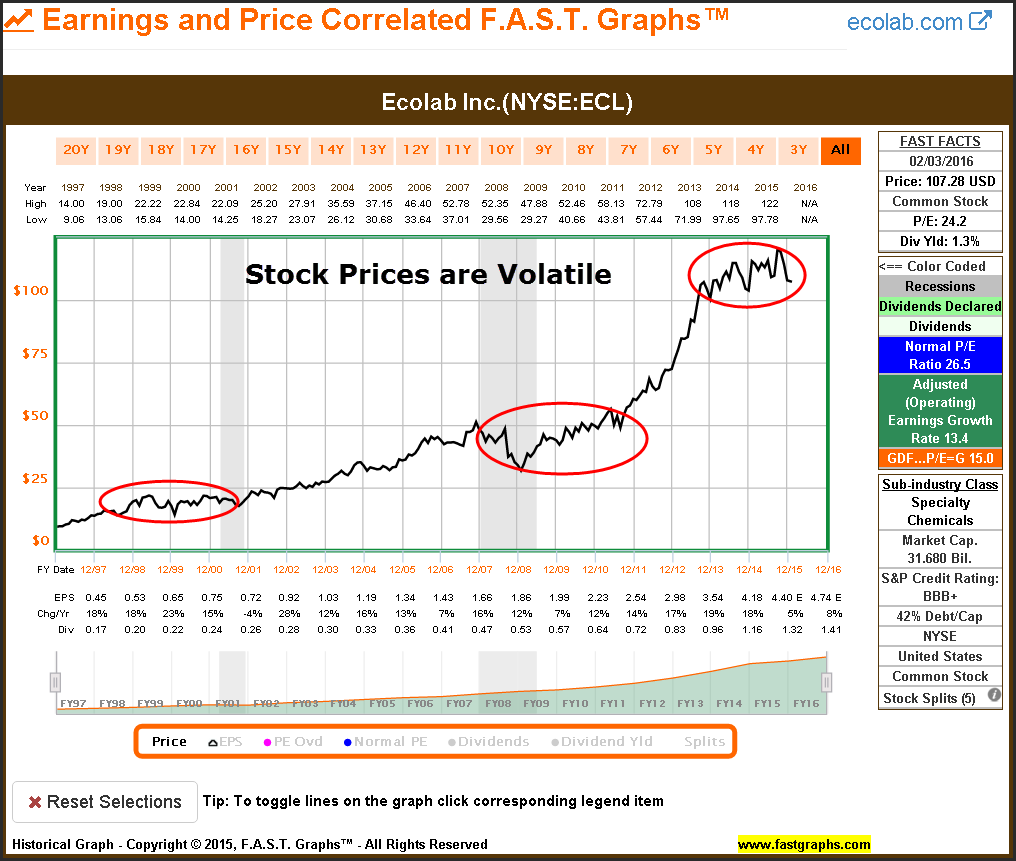

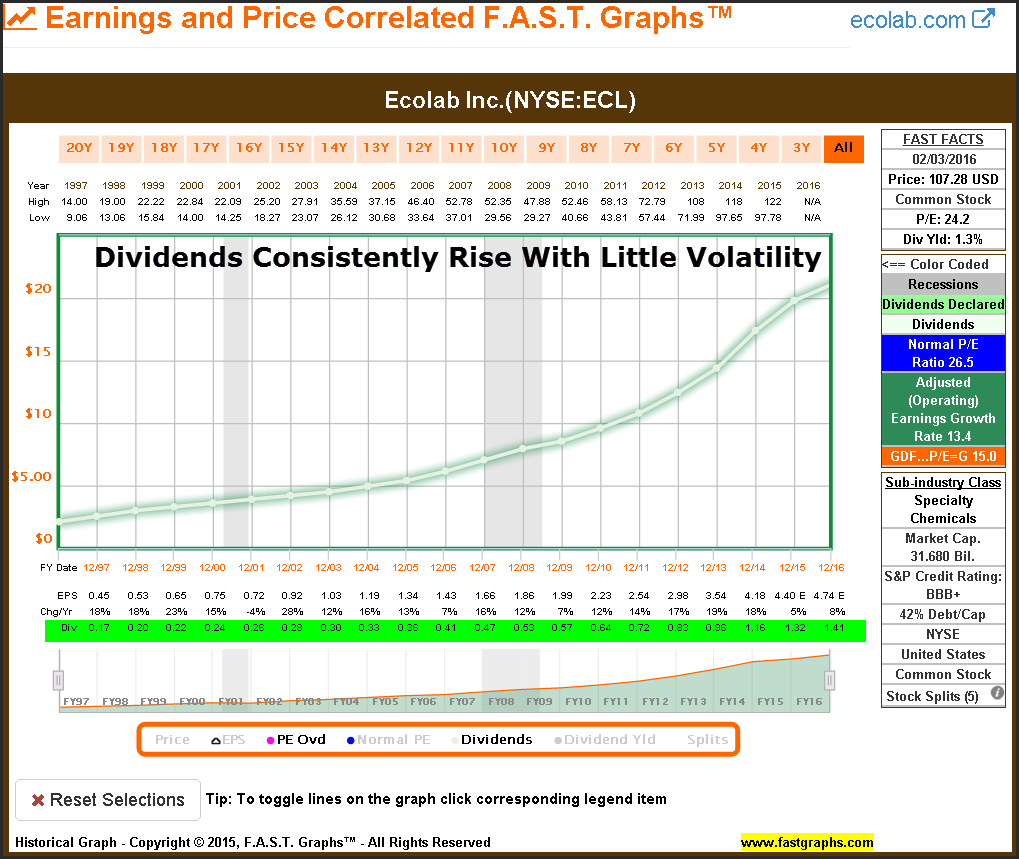

The Stock Market: Echo lab Inc. (ECL)

The Dividend Income Market: Ecolab Inc.

Ecolab has been one of the most consistent and fastest-growing companies in this group. Consequently, it is no surprise to see the significant amount of capital appreciation generated on shareholder’s behalf. Dividends made an important contribution, but capital appreciation was more than 10 times dividends.

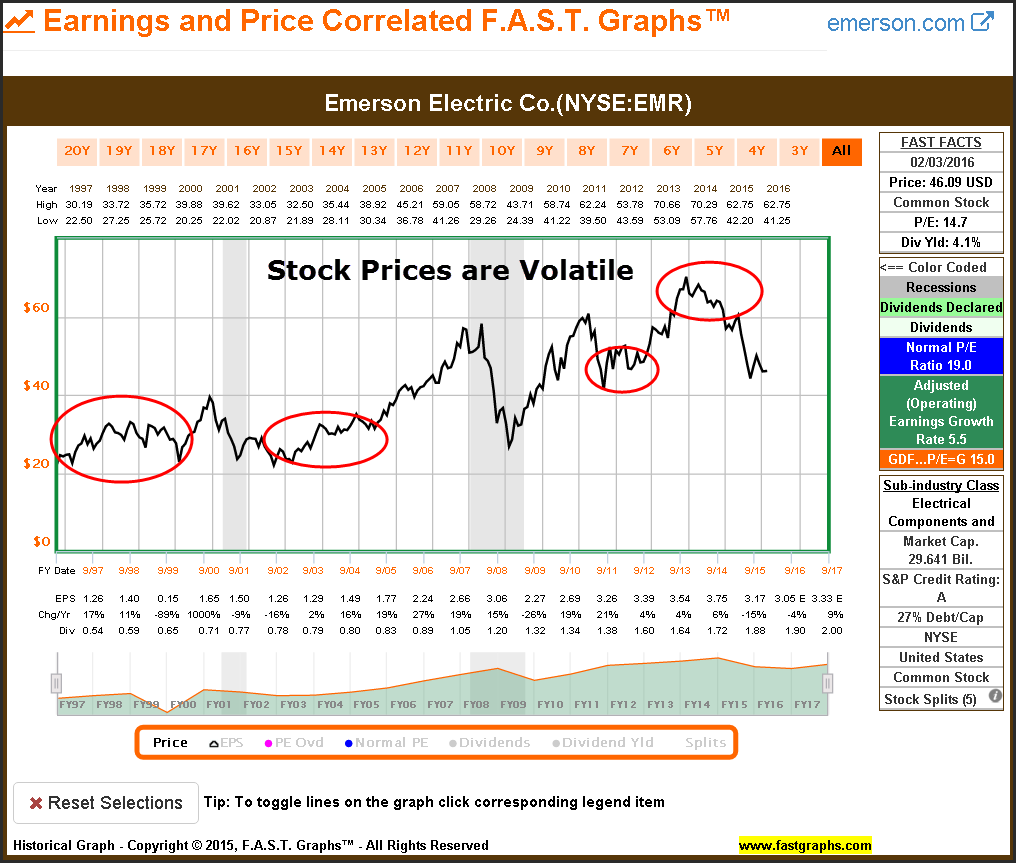

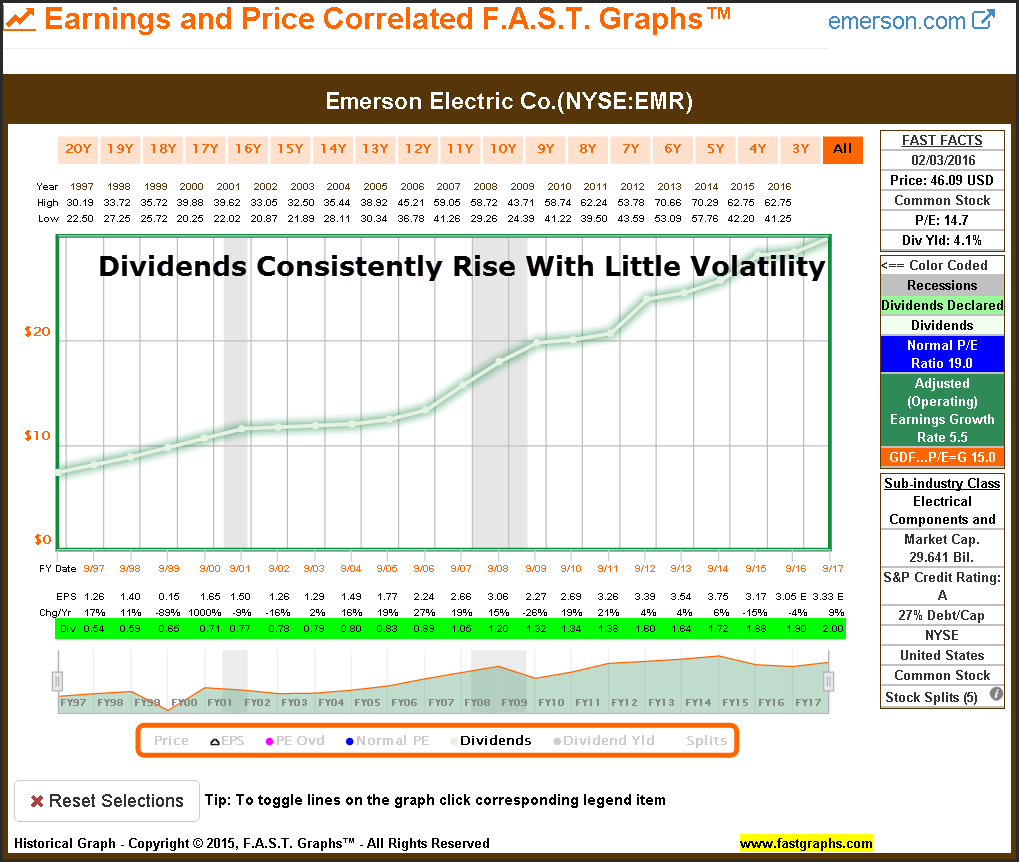

The Stock Market: Emerson Electric Company (EMR)

The Dividend Income Market: Emerson Electric Company

Emerson Electric is one of the most cyclical companies in this group. Therefore, it is not surprising to notice that dividend income represented approximately half the total return since 1997. I will also add that Emerson Electric is experiencing a down cycle in both price and earnings currently. Consequently, this has a meaningful impact on the capital appreciation side.

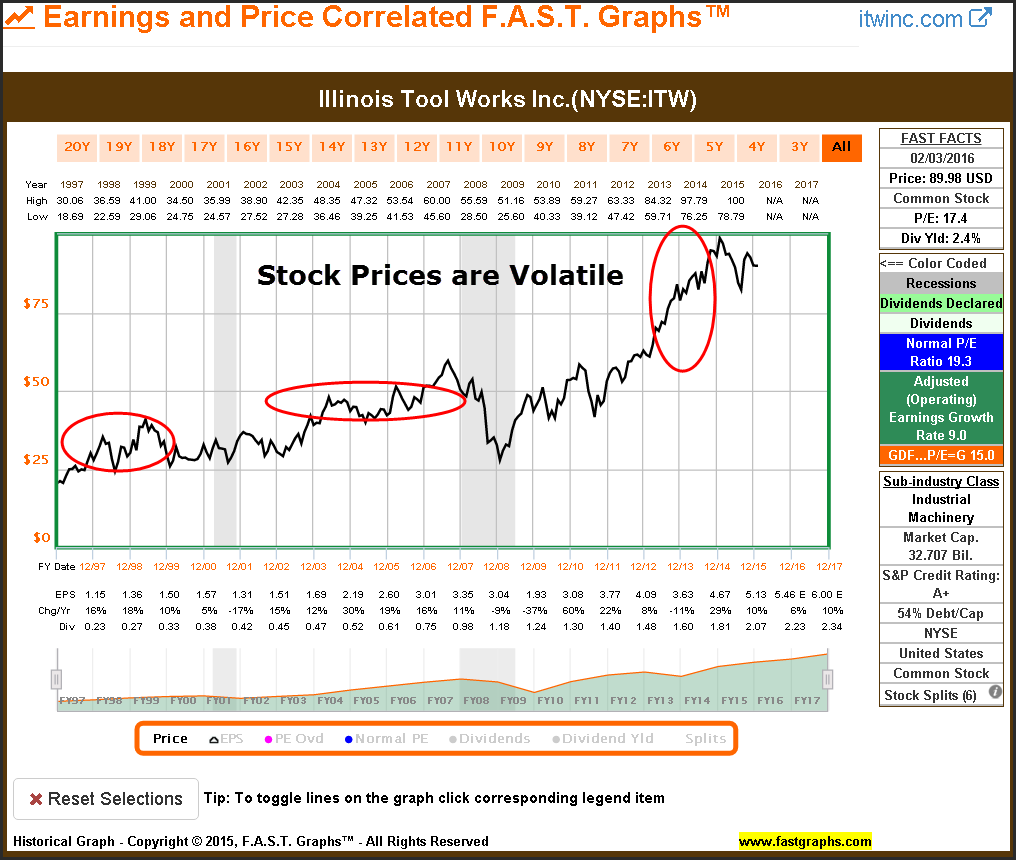

The Stock Market: Illinois Tool Works Inc. (ITW)

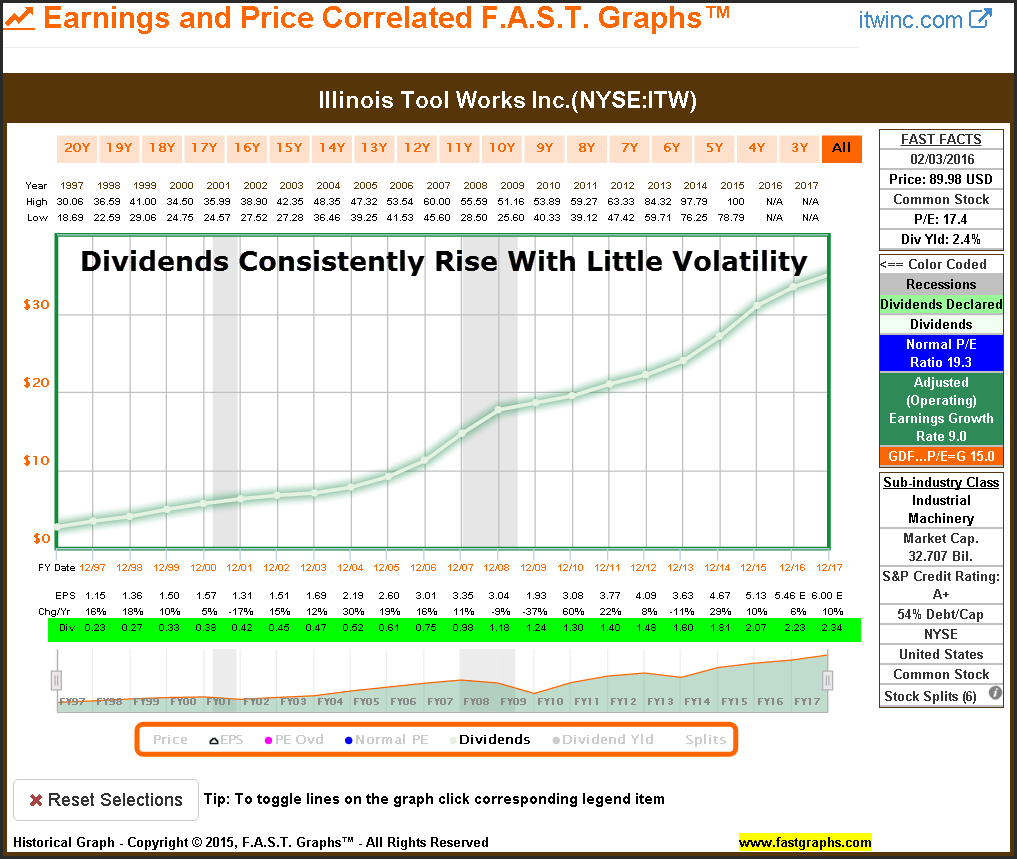

The Dividend Income Market: Illinois Tool Works Inc.

The Stock Market: Johnson & Johnson (JNJ)

The Dividend Income Market: Johnson & Johnson

The Stock Market: Kimberly-Clark Corporation (KMB)

The Dividend Income Market: Kimberly-Clark Corporation

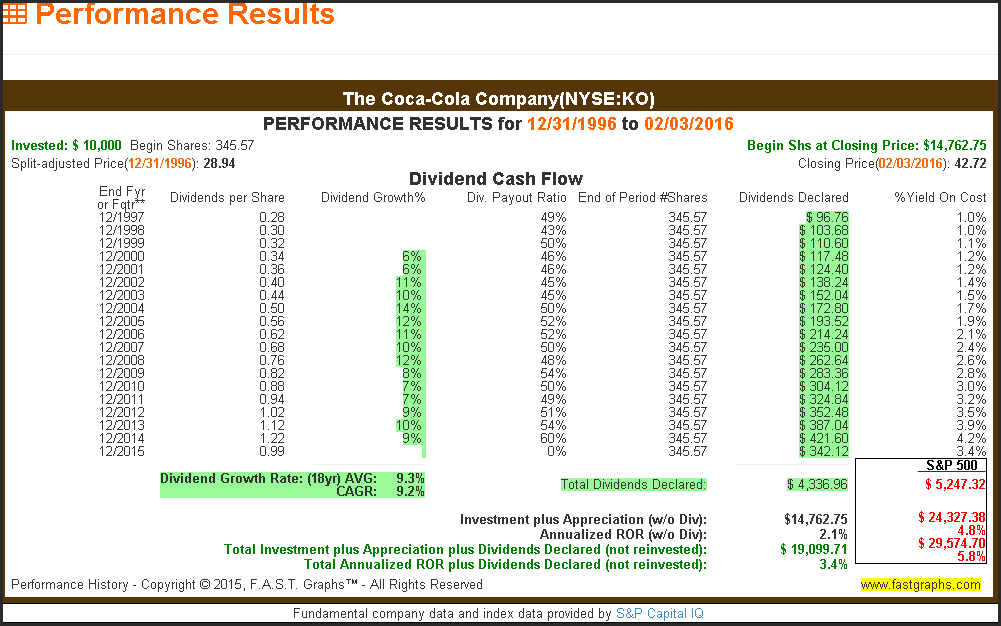

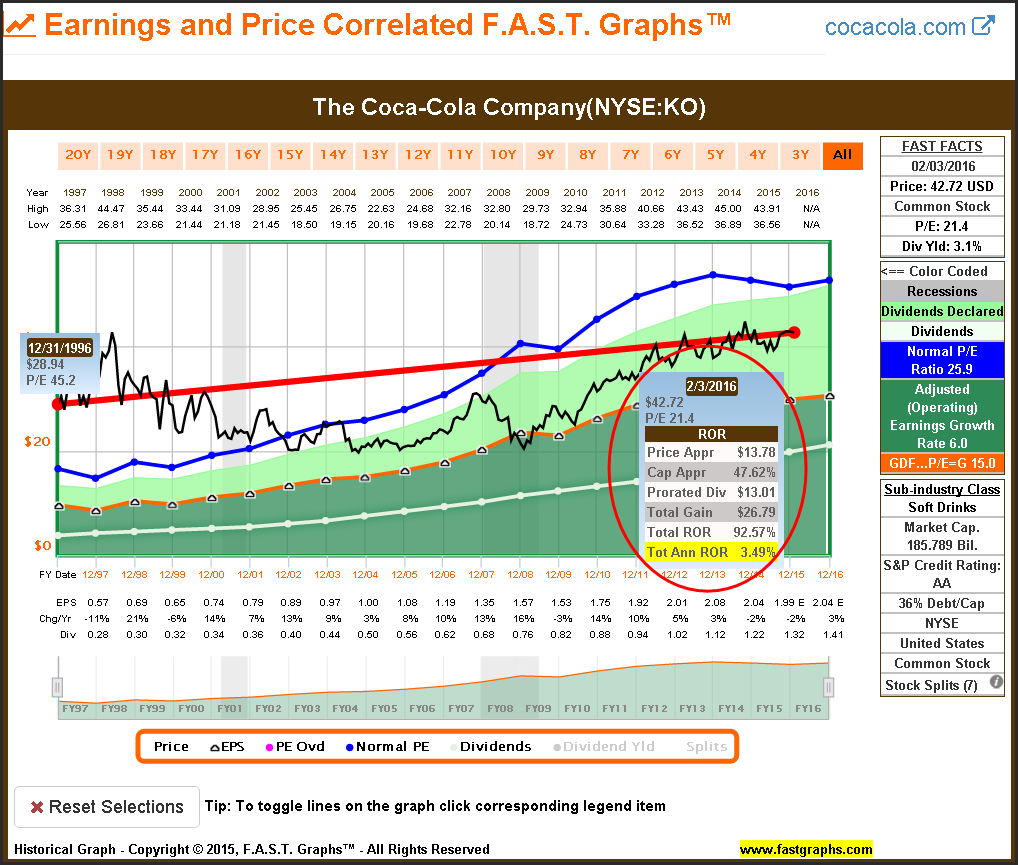

The Stock Market: The Coca-Cola Company (KO)

The Dividend Income Market: The Coca-Cola Company

The Coca-Cola Company: Bonus Valuation Graph

As I alluded to earlier in the article, in addition to dividend income, valuation plays an important role in the long-term generation of total return. At the beginning of 1997 (December 31, 1996) Coca-Cola was trading at a P/E ratio of 45.2. This represented significant overvaluation, which created a significant headwind against capital gain. However, as seen above, the dividend record has been impeccable.

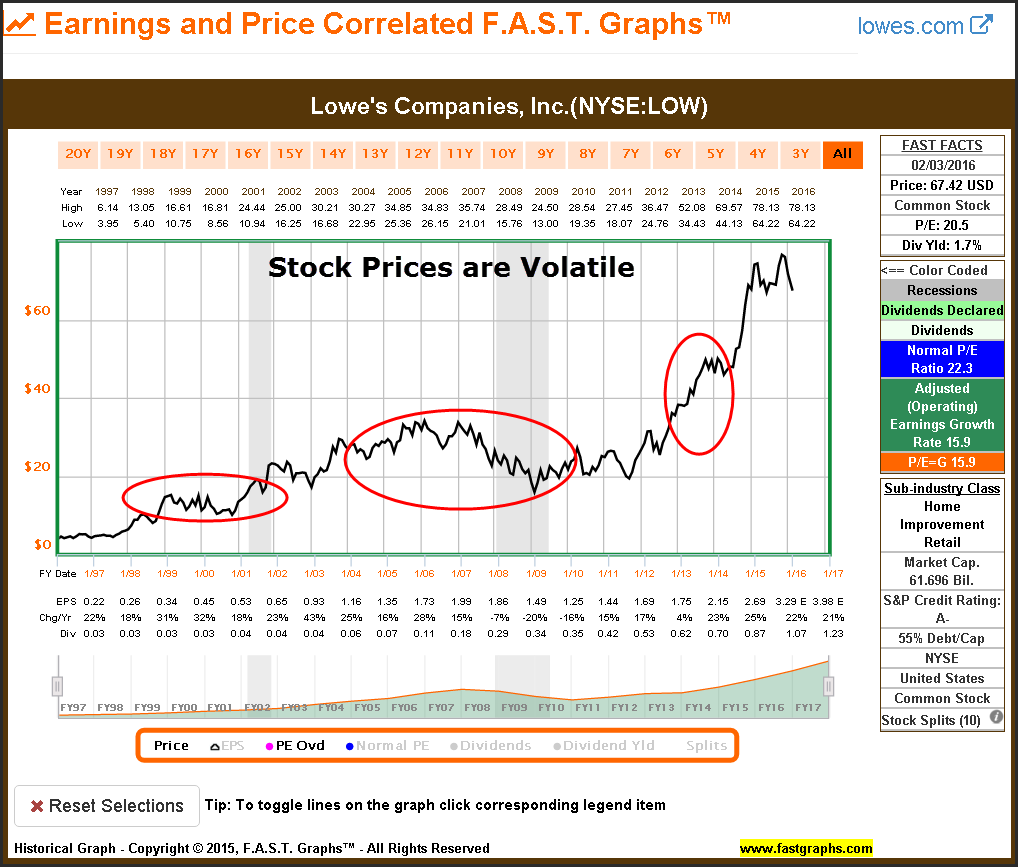

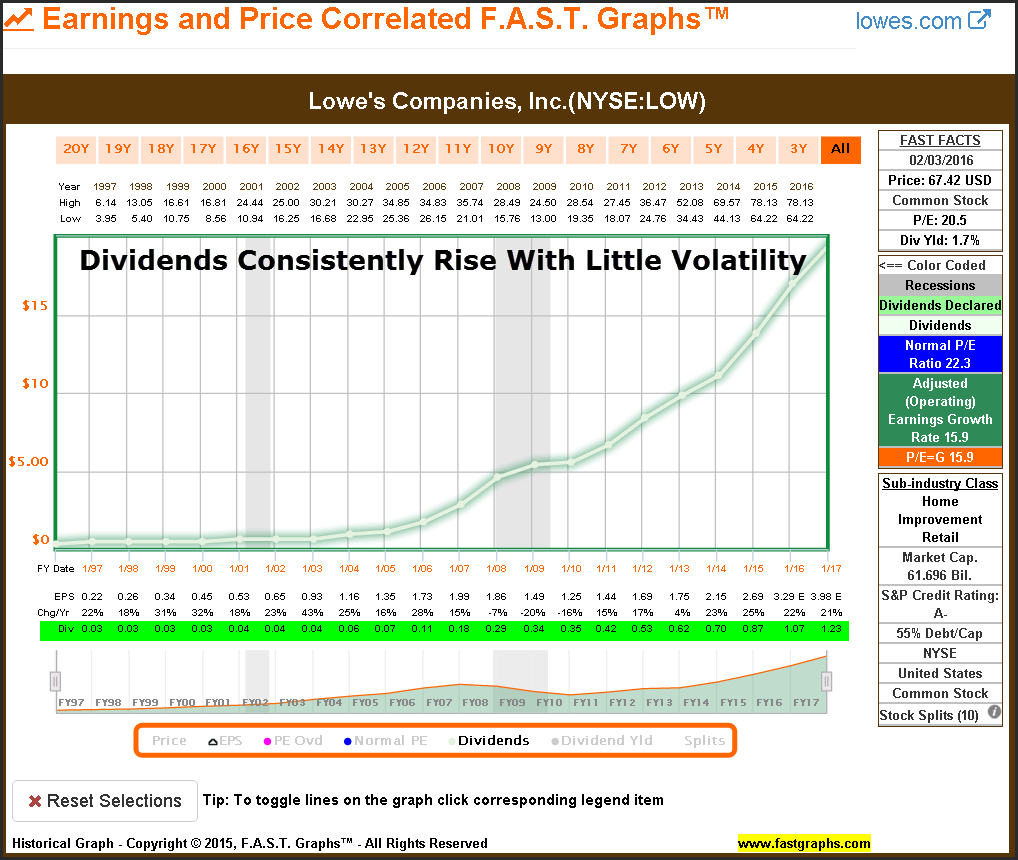

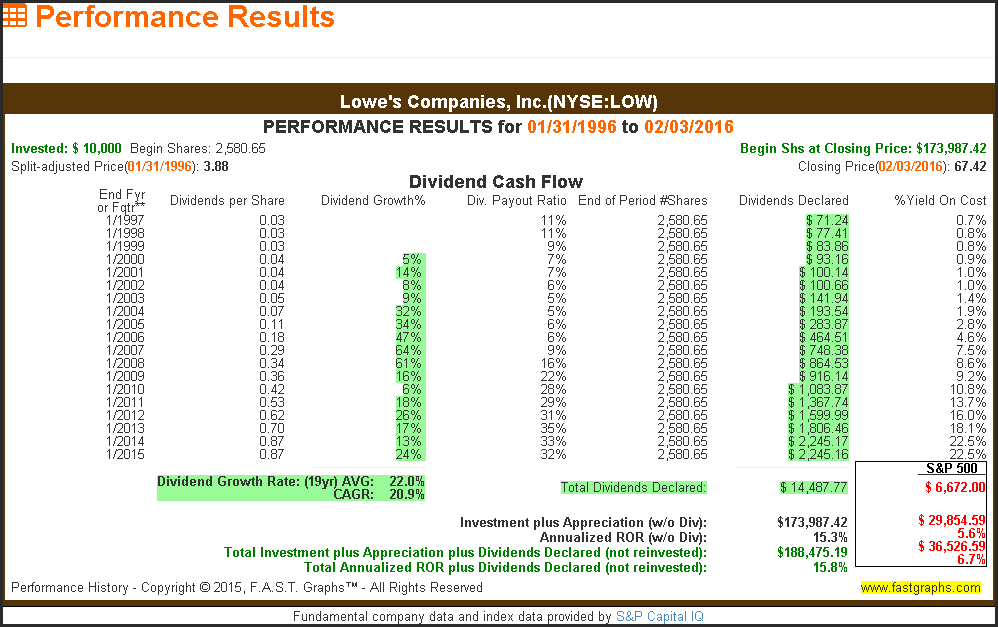

The Stock Market: Lowe’s Companies, Inc. (LOW)

The Dividend Income Market: Lowe’s Companies, Inc.

In a similar fashion to Ecolab, Lowe’s generated significantly more growth than most of these other examples. Consequently, here is another example where capital appreciation made a significantly greater contribution to total return than dividend income. In other words, capital appreciation was the dominant source of return in this example.

The Stock Market: McDonald’s Corp. (MCD)

The Dividend Income Market: McDonald’s Corp.

The Stock Market: Medtronic plc (MDT)

The Dividend Income Market: Medtronic plc

The Stock Market: 3M Company (MMM)

The Dividend Income Market: 3M Company

The Stock Market: PepsiCo, Inc. (PEP)

The Dividend Income Market: PepsiCo, Inc.

The Stock Market: The Procter & Gamble Company (PG)

The Dividend Income Market: The Procter & Gamble Company

The Stock Market: Target Corp. (TGT)

The Dividend Income Market: Target Corp.

The Stock Market: V.F. Corporation (VFC)

The Dividend Income Market: V.F. Corporation

The Stock Market: Wal-Mart Stores Inc. (WMT)

The Dividend Income Market: Wal-Mart Stores Inc.

The Stock Market: Exxon Mobil Corporation (XOM)

The Dividend Income Market: Exxon Mobil Corporation

Exxon Mobil Corporation: Bonus Earnings and Price Correlated Graph

I felt it was appropriate to cast a spotlight on Exxon regarding the recent troubles going on in the energy sector. S&P Corporation recently put this AAA rated company on credit watch. In the same context, S&P recently downgraded 10 U.S. oil companies and suggested they will decide whether to downgrade Exxon within the next 90 days. However, it has been suggested that it would only be by a single notch.

The reason I highlight this is to point out that in addition to focusing on dividends over stock prices, it’s also important to focus on other important fundamental metrics such as earnings and cash flows. At the end of the day, future dividends will be sourced from the company’s ability to generate operating results.

Summary and Conclusions

Before I conclude this article, I want it to be clear to the reader that I am not recommending any of the examples utilized in this article for current investment. That is not the intent or purpose of what I’ve written. Instead, I chose these 20 prominent blue-chip Dividend Aristocrats in order to illustrate how focusing on dividends and their consistency and growth can empower investors to avoid the anxiety that comes with volatility in stock prices.

If you are a long-term oriented investor, and if your investment objective is a current and growing income stream, I believe it makes more sense to keep your focus on your income and how it consistently grows over time. Stock-price volatility is unavoidable and will inevitably change from rising to falling several times over a long investing horizon. The key is to ignore the volatility of stock prices and the anxiety it brings, and focus your attention instead on the consistency and predictability of your growing dividends. Not only will that calm you down, it’s what matters most in the long run anyway.

Disclosure: Long ADP,JNJ,MCD,KO,PG,MDT,WMT,PEP,TGT,CL,EMR,ITW,KMB

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.