IN THIS ISSUE:

1. 4Q GDP Up Only 0.7% – Economy Started and Ended Weak

2. A Controversy Over GDP Growth Rate For All of 2015

3. Orders For Durable Goods Plunged Lower in December

4. Sub-3% GDP Growth: A Lost Decade For the US Economy

5. What We Could Do to Stimulate the Economy Now

Overview

Whew – January is finally over! Up until the last week or so, the downside carnage in January was the worst New Year’s stock market start in history. Thanks to last week’s rebound, it was only the worst New Year’s start since January of 2009 when the Great Recession was unfolding. Still, it was a hair-raising month for stock investors. And no one knows if the damage is over.

There are many theories as to why equity markets around the world suddenly plummeted in January. I have written about several of them in the last couple of weeks. Most market commentators, including yours truly, have pointed to concerns about China’s economy, the collapse in oil/commodity prices, the strong US dollar, Fed interest rate hikes, etc., etc. as the likely causes for the January implosion.

Rather than continue that discussion today, I want to point out a milestone that was reached with the end of 2015 and last Friday’s 4Q GDP report – and this milestone was not a good one. With 2015 behind us, it has been a decade since we have seen 3% yearly growth in the economy. The last year we had 3% growth was 2005. Call it America’s “Lost Decade.”

Near the end of today’s letter, I will make some suggestions on how we could stimulate our now moribund economy – starting with a significant corporate income tax cut for businesses large and small. Republicans complain that they can’t override President Obama’s veto, so they do nothing. Yet with the economy now growing by less than 1%, I think the GOP would be surprised at how much support they could get from Democrats, especially in an election year.

Before we get to that discussion, let’s take a look at last Friday’s GDP report for the 4Q. The advance report came in lower than expected with growth of only 0.7% for the final three months of last year. The sharply lower 4Q reading suggests yet another year of weak economic growth. And there is now a controversy over how much the economy expanded last year, which I will explain as we go along.

There’s a lot to cover in today’s E-Letter, so let’s get started.

4Q GDP Up Only 0.7% – Economy Started and Ended Weak

Let’s start today with the news from last Friday’s advance 4Q GDP report from the Commerce Department. The headline number was growth of only 0.7% (annual rate) in the final three months of last year. That number was weaker than the pre-report consensus of 0.9%, so it was yet another disappointment.

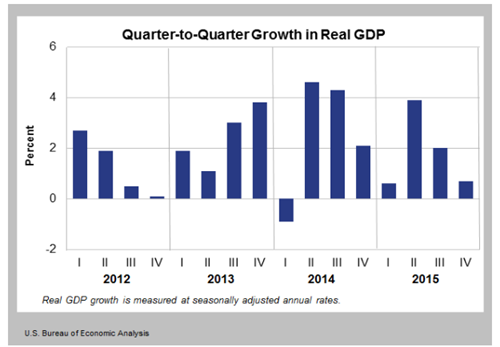

As you can see below, in 2015 US GDP rose by a very anemic 0.6% in the 1Q, due in large part to a very severe winter; by a strong 3.9% in the 2Q, largely attributed to “catch-up” from the 1Q; then 2.0% in the 3Q; and finally 0.7% in the 4Q. The economy started the year very weak, rebounded sharply in the 2Q and then ended the year almost as weak as it started.

The Commerce Department attributed the weak 4Q to a deceleration in consumer spending, a downturn in non-residential fixed investment, weaker exports and lower state and local government spending. Consumers continue to pocket most of their gasoline cost windfall to pay off debt and/or rebuild savings, rather than buying new goods and services.

The bottom line is that last Friday’s GDP report virtually assures a slow economic start for 2016 and raised the odds for a recession later this year. This 4Q GDP estimate will be revised two more times, near the end of this month and near the end of March. Early estimates suggest that the advance report number of 0.7% will be revised even lower later this month.

On the bright side (if you can call it that), the report sparked new discussion that the Fed will now be reluctant to move forward with the four interest rate hikes it has planned to implement this year starting in March. I’ll have more to say about that just ahead.

A Controversy Over GDP Growth Rate For All of 2015

In the Commerce Department’s GDP report last Friday, the official announcement stated that US economic growth for all of 2015 was 2.4%, the exact same as in 2014. That number immediately seemed high to me. Let’s go back to the quarterly GDP numbers for 2015: 0.6% for the 1Q, 3.9% for the 2Q, 2.0% for the 3Q and 0.7% for the 4Q.

If you add those four quarterly numbers up, you get 7.2%; if you divide that number by four, you get 1.8%, not 2.4%. So what gives, I wondered.

My immediate reaction was that the Commerce Department must have gone back and revised upward its GDP estimates for the 1Q, 2Q or 3Q. So I went to the Commerce Department’s Bureau of Economic Analysis (BEA) website to see if there were any revisions. There were none.

The quarterly GDP numbers for 2015 were exactly the same: 0.6%, 3.9%, 2.0% and the 0.7% advance estimate for the 4Q. Add ‘em up, divide by 4, and you get growth of 1.8%. So how did they come up with growth of 2.4% for last year? As of now, no one knows. Take a look.

On the left-hand side of the table, you can see that the BEA reported overall GDP growth of 1.5% in 2013, 2.4% growth in 2014 and 2015 growth of 2.4%. But if you go to the right-hand side of the chart, you see the official quarterly growth rates for 2015. Again, if you add them up and divide by four, you get 2015 growth of only 1.8%, not 2.4%.

I have to admit that at this point, I have no explanation. I have been watching these quarterly GDP reports for over 35 years, and I have never seen a discrepancy such as this.

While it is true that the 4Q advance GDP estimate will be revised two more times – at the end of February and at the end of March – I have no idea how the BEA will rectify this discrepancy. Maybe they will admit that it was just an error. I’ll keep you posted.

Before we move on to our main discussion today, I want to point out one other economic report from last week that was very disappointing. That would be the Durable Goods report for December which was released last Thursday.

Orders For Durable Goods Plunged Lower in December

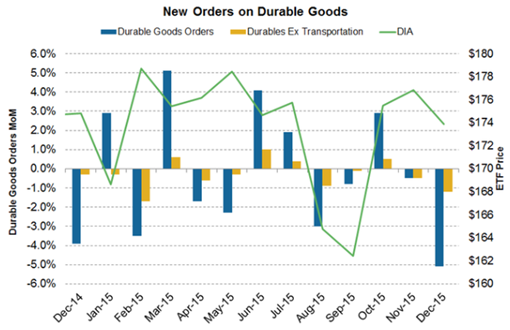

The Commerce Department/Census Bureau reported last Thursday that durable goods orders unexpectedly plunged in December by a whopping 5.1% versus the pre-report consensus estimate of only -0.5%. This was a big surprise. Durable goods represent consumer purchases that are likely to last 3-5 years or more. Think appliances, household goods, furniture, electronics, autos, etc. that are expected to last at least several years.

This key measure of US manufacturing health suffered its largest annual decline since the recession ended more than six years ago, showing how global headwinds are eroding this key pillar of the economy.

Demand for long-lasting manufactured products made in the US plunged 5.1% in December from a month earlier, and declined 3.5% for all of 2015, the Commerce Department reported last week. The annual decline in durable-goods orders last year was the largest outside of a recession in records dating back to 1992.

The figures add to mounting evidence that the manufacturing sector is contracting. And with the dollar strengthening further last month and financial-market tumult likely threatening business confidence, the factory slowdown could continue to worsen again this year.

Sub-3% GDP Growth: A Lost Decade For the US Economy

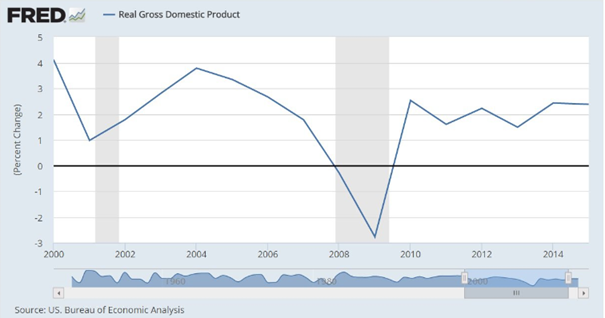

Whether you agree with me that the US economy grew by only 1.8% in 2015, or the Commerce Department that reported GDP growth of 2.4% last year, the last 10 years have been a “Lost Decade” for the American economy in one sense. Specifically, the US economy has not grown by over 3% a year since 2005.

From the end of World War II through 2005, the economy grew at an average annual rate of 3.5%. So 3+% growth was normal. Yet since 2005, the economy has not seen a single year of 3% growth.

Here are the numbers: 2015, 1.8% (or 2.4%); 2014, 2.4%; 2013, 1.5%; 2012,2.2%; 2011, 1.6%; 2010, 2.5%; 2009, -2.8%; 2008, -0.3%; 2007, 1.8%; and 2006, 2.7%.

Some economists argue that this is not unusual given that we had the worst recession since the Great Depression and the weakest recovery in the post-war era that followed it. Yet historically the economy has rebounded strongly following deep recessions. Not this time.

Obviously, the question is, why? Digging into the economic numbers, we find a combination of slowing labor force growth and weak productivity to blame. And it’s for those deeper structural reasons that many forecasters, such as the Congressional Budget Office, think the US is now a permanent 2% economy rather than a more vigorous 3% economy.

The difference between 2% and 3% may not seem like much, but it’s huge. Growth of 3% per year on average boosts the economy to $23 trillion over the next 10 years, whereas growth of 2% a year grows GDP to only $21 trillion over the same period. FYI, that $2 trillion difference is equal to the entire economy of Italy.

Most economists agree that getting growth back to 3% or above will be very difficult. Boosting productivity and labor force growth as America ages will be really hard, they tell us. But not impossible, especially with new leadership in the White House and economic and tax policies that can stimulate growth.

What We Could Do to Stimulate the Economy Now

For starters, the Fed should put its plans to raise short-term rates four times this year on indefinite hold. In its first policy statement of the year last week, the Fed acknowledged that the economy has slowed down in recent months – duh!

The rate hikes, should they occur, would only push the US dollar higher. While a strong dollar is generally a good thing, it is already up about 15% in the last year – enough is enough. The Fed should seek to stabilize the dollar so as not to hurt US exports any further.

Meanwhile, the Republican Congress should pass a significant corporate income tax cut for large and small businesses. For large corporations, slash the current 35% rate (the highest in the world) down to 20%. Push the rate down to 15% for small businesses such as C-corps and S-corps. And permit immediate tax write-offs for new-business-investment expenses.

Congress should also rewrite the rules governing the repatriation of US corporate profits from overseas. It is widely reported that US corporations have over $2 trillion in foreign accounts that would quickly return home if the rules are changed. That’s money which could fund new projects and create new jobs.

Congress should also push for reduced regulatory burdens, although it looks like there’s no stopping the Obama administration’s unconstitutional march toward even greater regulations. Even so, Congress should vote on such changes and make Obama veto them – before the election in November.

And speaking of the election, I believe that the weak economy is a large enough concern that many Democrats would go along with the Republicans in trying to force the changes I suggested above. Lots of Dems running for re-election would welcome the chance to do something to stimulate the economy.

Come on, Republicans, do what we sent you there to do – even if you may not have enough Dem support to override the president’s vetos! You might have more support than you think with the economy now growing at less than 1% and an election looming.

Very best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.