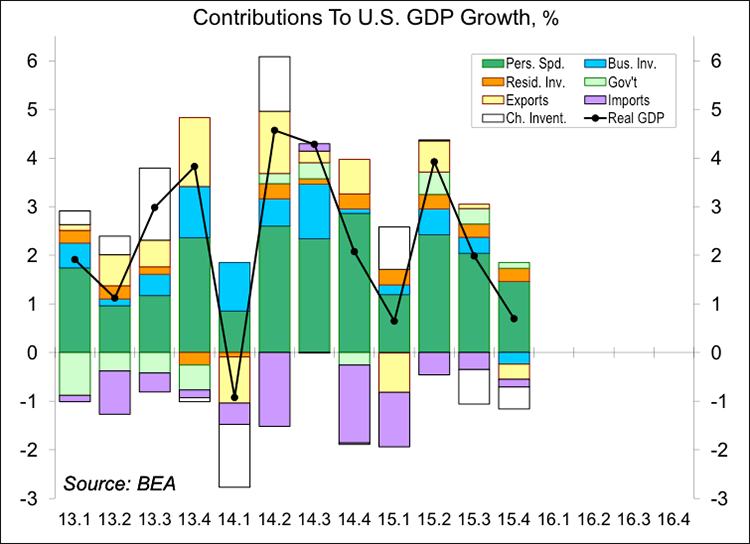

Real GDP rose at a 0.7% annual rate in the advance estimate for 4Q15, roughly what was expected before the release, but a lot lower than was anticipated at the start of the quarter. It’s not as bad as it looks. Growth was held back by foreign trade and slower inventory growth. Domestic demand was mixed, but moderate. The fourth quarter numbers don’t tell us much about the important question: what’s growth likely to be over the course of this year. More troublesome, there are more important concerns about the economy’s long-term prospects.

Net exports subtracted 0.47 percentage point from fourth quarter GDP growth, according to the advance estimate. Slower inventory growth subtracted 0.45. Private Domestic Final Purchases (consumer spending, business fixed investment, and residential homebuilding) rose at a 1.8% annual rate, vs. a 3.2% increase over the four previous quarters – so we can’t pin fourth quarter softness on the rest of the world alone. Consumer spending slowed. Business fixed investment turned down, with weakness concentrated in structures (mostly energy exploration) and transportation equipment (no detail available).

While GDP growth slowed in the fourth quarter, monthly figures suggest a sharp loss of momentum in November and December. Durable goods orders fell sharply. Consumer spending was disappointing. One possibility is that consumers and businesses may have been reacting to the news. Fear of a slowdown can become self-fulfilling. This is a greater concern for the rest of the world than it is for the U.S., where business can make adjustments as demand picks back up (if the fear is contained and unwarranted). However, it bears watching closely. One of the key elements in the financial crisis was panic. Panic made the housing correction and deleveraging much more sinister. A panic is difficult to predict. Bad news can feed on itself, but it’s hard to gauge the timing and magnitude.

Many point to the data as evidence that the Fed made a mistake by raising rates in December. Hindsight is a wonderful thing. However, the Fed would likely have faced greater market adjustments if it waited. Postponing a rate hike in September led to further undue risk-taking. The Fed’s focus is on the job market (slack still being reduced) and the inflation outlook (likely to move back toward the 2% goal as oil prices stabilize). The Fed did not cause January’s stock market weakness (which was more sentiment than fundamentally driven). Investors were disappointed with the January 27 policy statement. The Fed simply signaled that it was keeping its options open. Investors were hoping for a strong signal that rate hikes would be on hold for the foreseeable future. By stressing the job market in the policy statement, the Fed implied that a March rate hike was still on the table (although widely seen as not very likely).

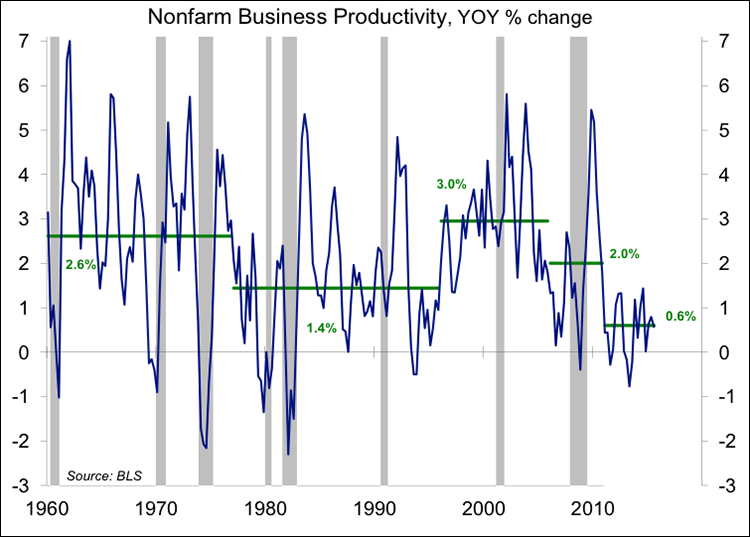

While investors have been fearful that the U.S. economy will not escape the pull of slower global growth, there are more important long-term concerns. Slow fourth quarter growth, combined with strong job market improvement, means that productivity (output per work-hour) likely fell in 4Q15. These figures are erratic (large quarterly swings and sizable revisions), but the trend over the last few years has been poor (about a 0.6% annual rate). The weak trend adds support to the view that we’ve entered a period of secular stagnation.

Labor costs are an important part of the inflation outlook, but you need to account for what you’re getting for that added labor expense. That’s were productivity comes in. Unit Labor Costs (labor expense per unit of output) are trending at a higher rate. This could show up as higher inflation if firms can pass the higher costs along, or it could show up as a squeeze on corporate profits if they can’t. Nobody knows if the productivity slowdown will be temporary or longer lasting. However, a more permanent slowdown would have far reaching implications for the longer-term economic outlook.