Introduction

One of the greatest challenges that authors face when posting articles on financial blogs is how much information they should include and how much they should exclude. Space is limited, and many readers prefer a short write-up over long dissertations. Therefore, most authors (yours truly included) attempt to summarize their positions in the fewest words possible. However, this approach implies that readers will fill in the blanks between what is said and what is left out. Unfortunately, that is not what always happens.

In my own personal experience, the best example I can offer to illustrate what I’m talking about relates to comprehensive research and due diligence. I am a firm believer that all investing in common stocks requires comprehensive research and due diligence before your money is invested. As a result, I often provide articles on what I refer to as research candidates. Most of the time I am presenting candidates that I believe appear sound or attractively valued.

Therefore, my position is that a research candidate is offered as a suggestion to the reader that the company in question may be worthy of conducting a comprehensive research and due diligence effort. Because, and to paraphrase a comment Warren Buffett once made, “Investing without research is like playing stud poker and never looking at the cards."

In this respect, I lay out the ingredients but expect the reader to do their own cooking. As I previously stated, I try to offer research candidates that might be worthy of the reader’s time and effort for conducting a comprehensive research and due diligence procedure. Nevertheless, I will often receive comments from readers pointing out important facts or considerations that I failed to mention about a given company. Even though I often stress the importance of comprehensive research and due diligence, I don’t do it in every article I write. Consequently, I understand why readers who are not familiar with my work might get the wrong or incomplete impression about what I’m suggesting or discussing.

Researching United Technologies: Here’s How I Do It

But even more relevant to the thesis of this article is another comment or question that I often receive asking how to conduct research and due diligence. On October 9, 2013 I published an article found here titled “What Is Due Diligence? Here's How I Do It.” In that article I presented my general approach to how I personally perform research and due diligence, and utilized the company Medtronic (MDT) as a representative example to illustrate my process and procedure. However, several years have passed since I published that article, and in the comment thread of my most recent article I was asked the following questions as follows:

“Everyone talks about performing due diligence. Could someone give advice on what is entailed in that? Are there articles/web sites anyone recommends? Maybe this could be a good topic for Mr. Valuation?”

This reader’s questions inspired me to repost my approach to research and due diligence. However, in this article I will be sharing the due diligence I recently conducted on United Technologies Corporation (UTX), a company I have owned since late July 2010, and one that I consider attractively valued today. Also with this article I will be reposting excerpts from what I wrote in the previous article, however, I will not be applying quotations because the original work was mine.

The first step in my due diligence process is the determination of whether or not I believe a given business (stock) is worthy of the time and effort required for further scrutiny. Since my approach relates to investing in the business behind the stock, my initial investigation relates to the fundamental strength and health of the business in question. In other words, do I believe the fundamentals underpinning the business are strong enough and therefore worthy of my continued efforts? (Note: I purposely make it a point to ignore price or valuation with this first step).

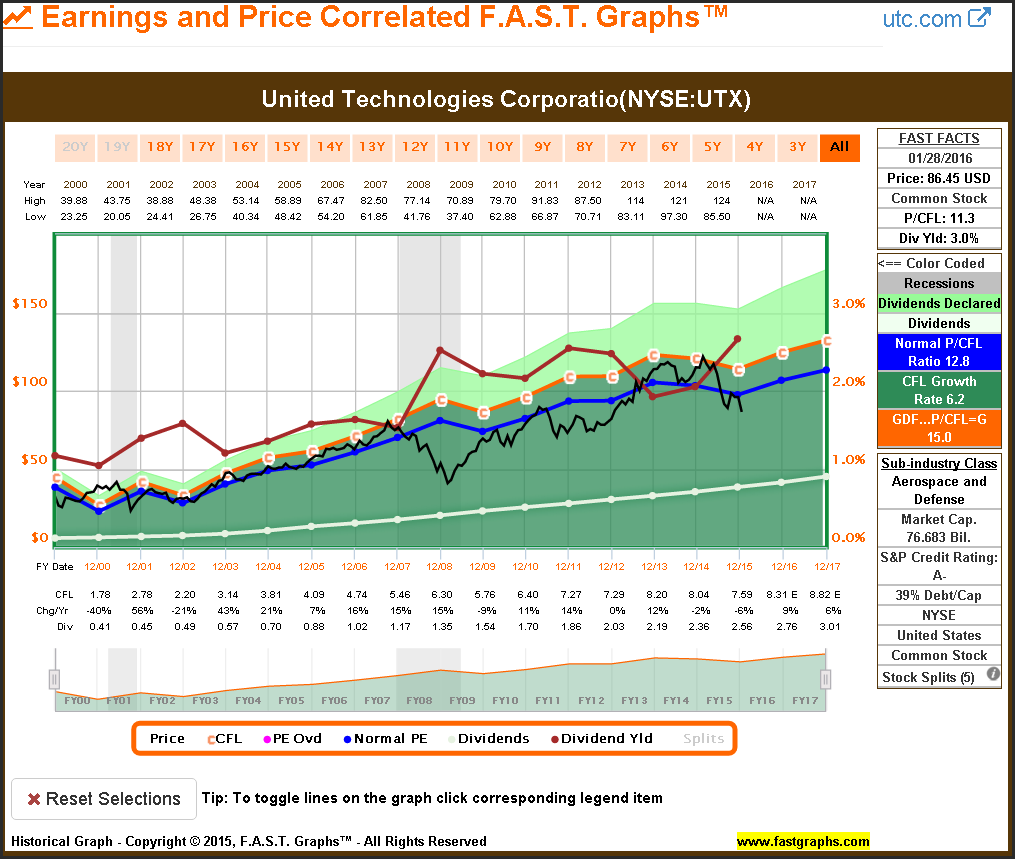

As most regular readers of mine know, I developed F.A.S.T. Graphs™, the fundamentals analyzer software tool, in order to assist me in researching stocks deeper, faster and more efficiently. The following earnings and dividend graph on United Technologies since 1996 tells me a lot about the historical operating performance of this blue-chip dividend growth stock and provides insights into the quality and skills of its management team.

United Technologies is an industrial company in the subsector Aerospace and Defense. Both the Industrial sector and the Aerospace and Defense subsector are generally thought of as cyclical industries. In truth, many companies operating in this sector and subsector possess deep cyclical characteristics comprised of significant periods where earnings rise and fall from one timeframe to the next.

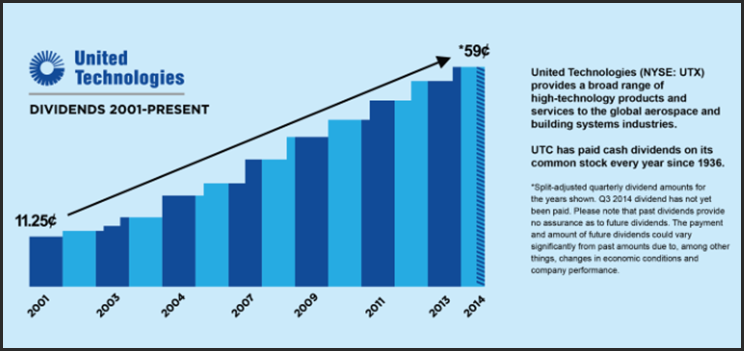

However, a careful review of United Technologies’ historical earnings and dividend achievements paints a different picture. Earnings growth has been very consistent with only the occasional drops or flattening of earnings results from one year to the next. Importantly, this blue-chip dividend growth stock remained very profitable during our last two recessions of 2001 and 2008. But best of all, the company has increased its dividend for 22 consecutive years and has paid a dividend every year since 1936. Therefore, this first step in my due diligence process suggests that this is the kind of company that I would like to be a long-term shareholder owner of.

Now that I am comfortable that this is the type of company I would like to be a long-term holder of, the next step is to check the company’s current valuation or price relative to its intrinsic value reference line. Therefore, I add monthly closing stock prices (the black line) to the above graph in order to check its current valuation, but also to analyze how the market has historically valued the company’s operating results.

The first thing that strikes me on the United Technologies’ graph after I bring price into the equation is how the market has had a long-term tendency to price this blue-chip at a premium to its orange earnings justified valuation reference line. However, I also noticed that its current price has fallen below its historical normal P/E ratio (the dark blue line) and its orange earnings justified valuation reference line as well. Additionally, I observe that reported earnings for fiscal 2015 fell approximately 8%, which perhaps partially explains the market’s current negativity towards the company.

For additional insights into my observation of the market’s penchant to apply a premium valuation, I next remove earnings and dividends from the graph leaving only price in relation to its historical normal P/E ratio. The most striking observation from this exercise is to notice how price has inevitably moved back to the normal P/E ratio range every time it fell below it in the past. At this level of my due diligence process, this gives me a modicum of confidence that it is a real possibility that this could happen again in the future.

An integral part of my personal research and due diligence process is to take full advantage of all the analytical power available from the research tools at my disposal. Since I have conducted comprehensive research and due diligence on many blue-chip dividend growth stocks in the past, I have also learned that premium valuations relative to earnings can look differently when evaluated based on cash flows.

Therefore, I routinely switch from evaluating the company’s earnings and price relationship to taking a look at price as it relates to cash flow. Also, on the following price and cash flow graph on United Technologies I also add an additional valuation reference based on historical dividend yields. Here I discovered that United Technologies is trading at a discount to its historical price and cash flow relationship, and I further notice that its current dividend yield is at its highest historical level which further indicates attractive valuation.

What Businesses is the Company in?

Once I have determined that valuation appears sound, and in this case attractive, my next step is to click on the link to the company's website provided at the top of the graph. Once I am in the company’s website, my objective is to learn as much about the company and the businesses it is in as I possibly can. I typically spend a great deal of time moving around the company’s website in order to get a feel about what the company does and how it makes its money.

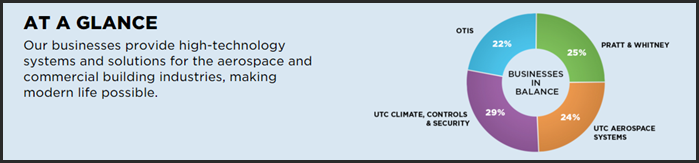

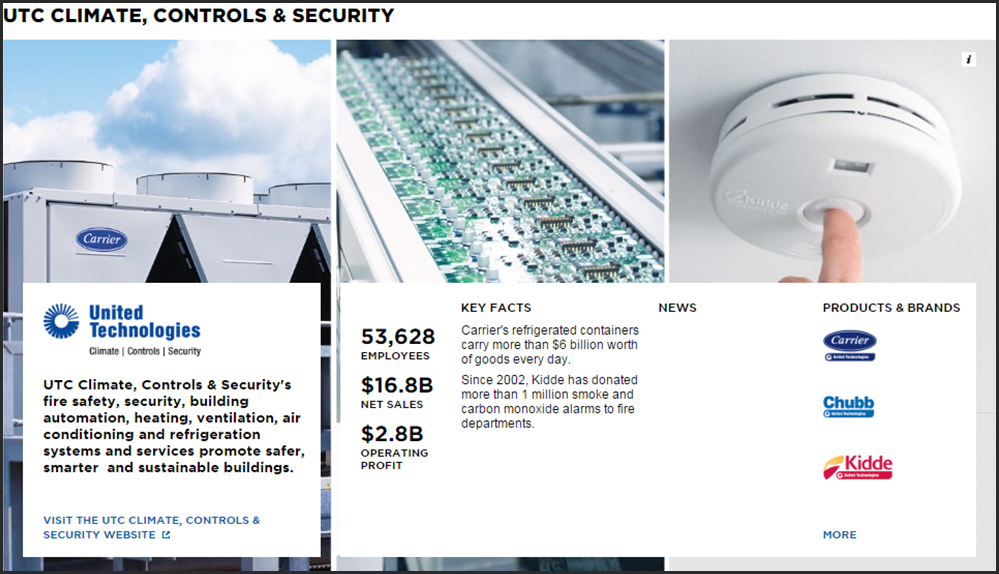

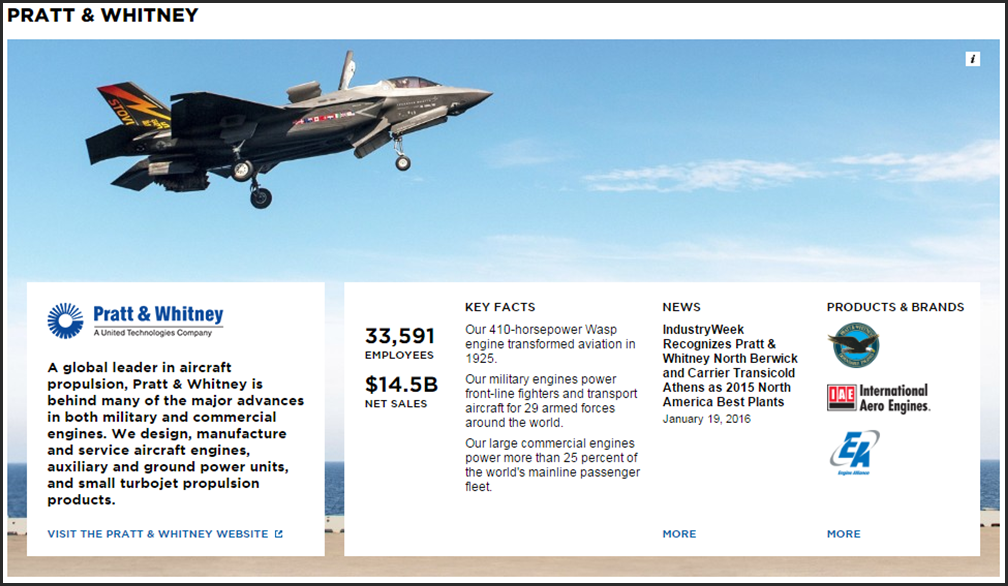

As an example of what you can find by doing this, United Technologies has a section titled “Our Businesses” and in that section they present their company “At a Glance.” For the reader’s convenience, I’ve included a few screenshots from that section. The first thing that struck me was how balanced United Technologies’ businesses are. This industrial company is very well-diversified across four important businesses, and each contributes almost equally to the whole.

In addition to the balance I saw in this section, the company provided an excellent summary full of important facts and insights into each of their four primary businesses. After spending just a few moments reviewing each of their four businesses, I received a great feel about what businesses they are in, their brands, their sales, and many other interesting insights into the company. However, I also followed the provided links to each of their respective businesses and spent time learning more about each of them.

After I got a general feel about what the company does, and while I’m still in the website, I will next look for the investor relations section. Although I can also find a company’s financial reports here, I save that tedious task for later. What I look for instead are any presentations that the company has provided. I am especially interested in presentations made at investor conferences or analyst days.

Later in this article I will be moving on to generating feasible forecasts or future performance estimates. I often start that process by examining consensus analyst estimates. However, before I do that I like to review presentations that the company made to analysts, because I recognize that the analysts making their forecasts are significantly impacted by sitting through the same presentations I’m about to review. Therefore, I can begin to make my own forecasts prior to examining what the analysts are forecasting.

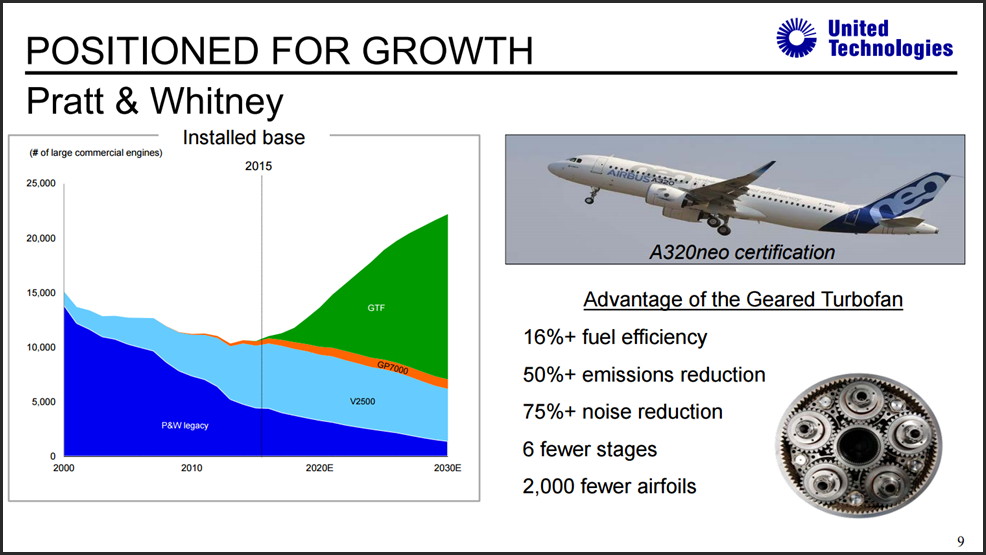

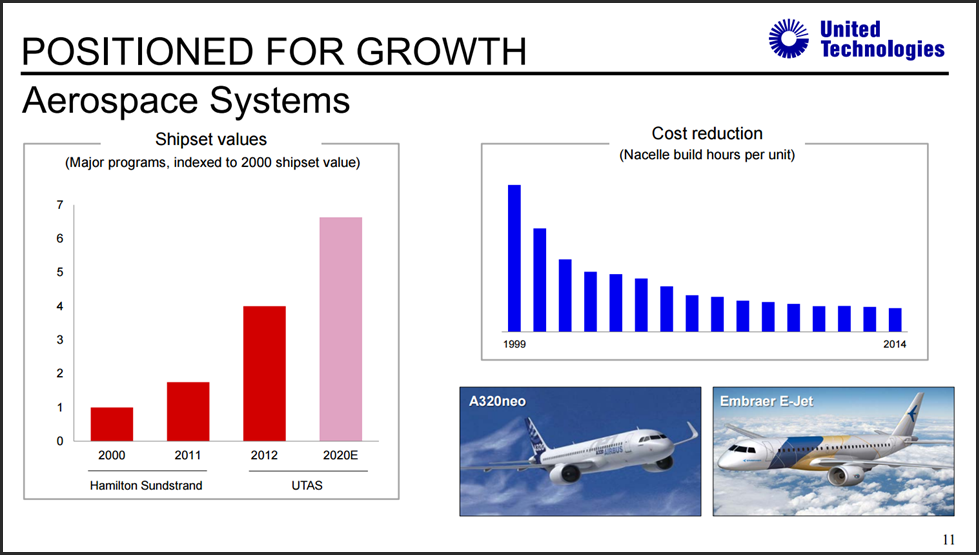

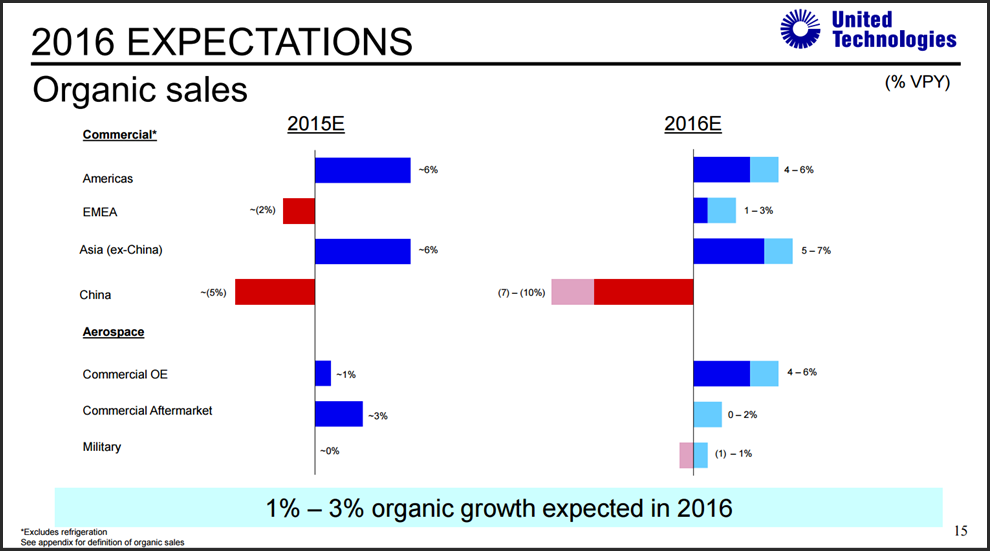

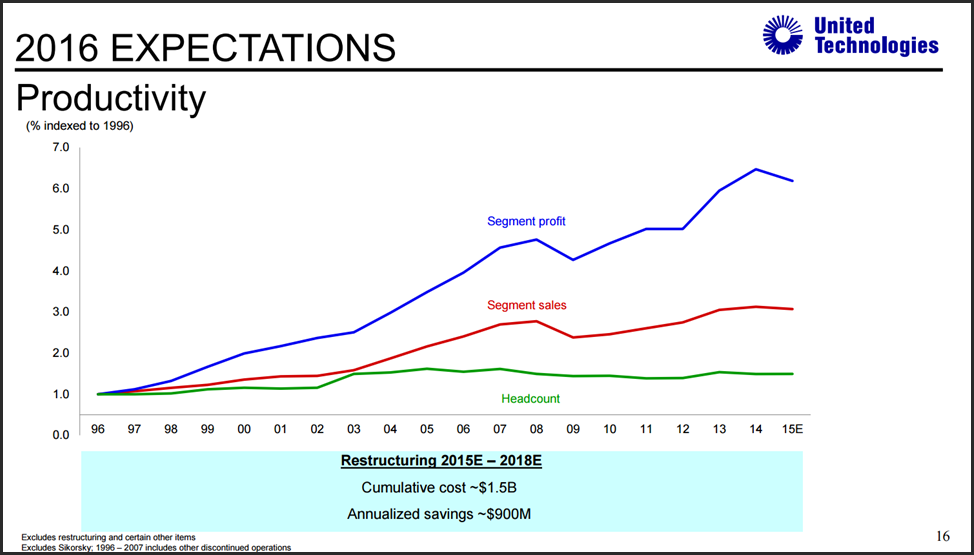

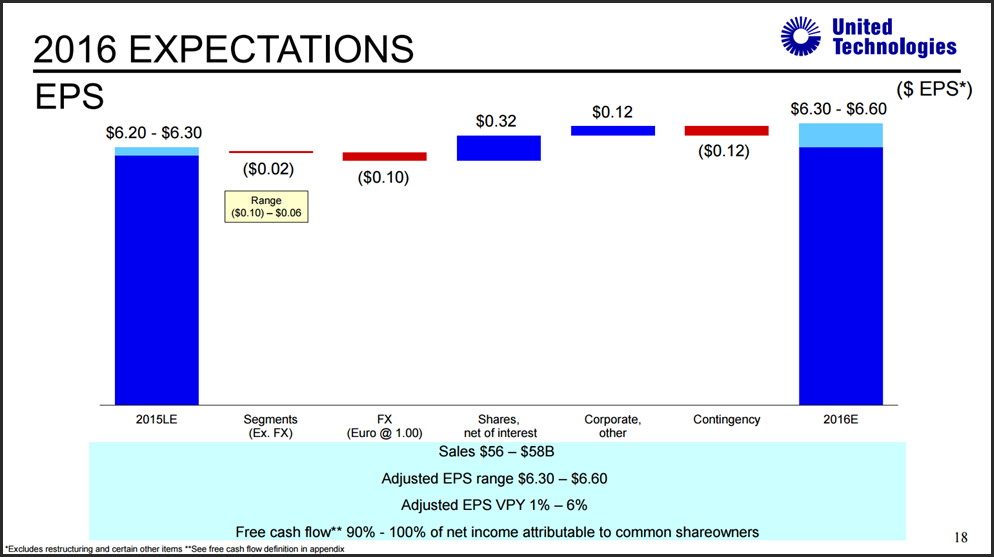

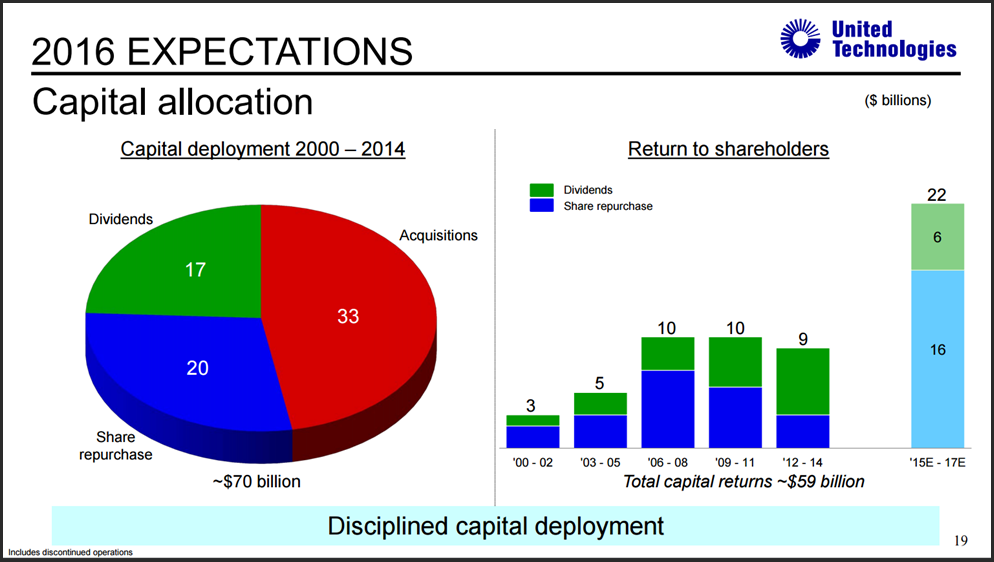

Here is a link to United Technologies’ Investor and Analyst Meeting held on December 10, 2015, followed by a few slide excerpts from the presentation. Remember that at this point in my process I am striving to get a perspective about the company’s future prospects and growth potential. At the same time, I also recognize two important things about these types of presentations.

First of all, every company attempts to put their best foot forward and paint as optimistic a view of their company as possible. However, I also recognize that it is not in the company’s best interest to guide investors above what they are capable of accomplishing. It’s always better to exceed expectations than it is to disappoint.

Next, and after reviewing any other presentations I found interesting, I will spend time reviewing other sections of the company's website in order to better familiarize myself with the company. In addition to trying to learn more about the company, I will always include a review of the company's management team. Here is a link to the leadership team of United Technologies.

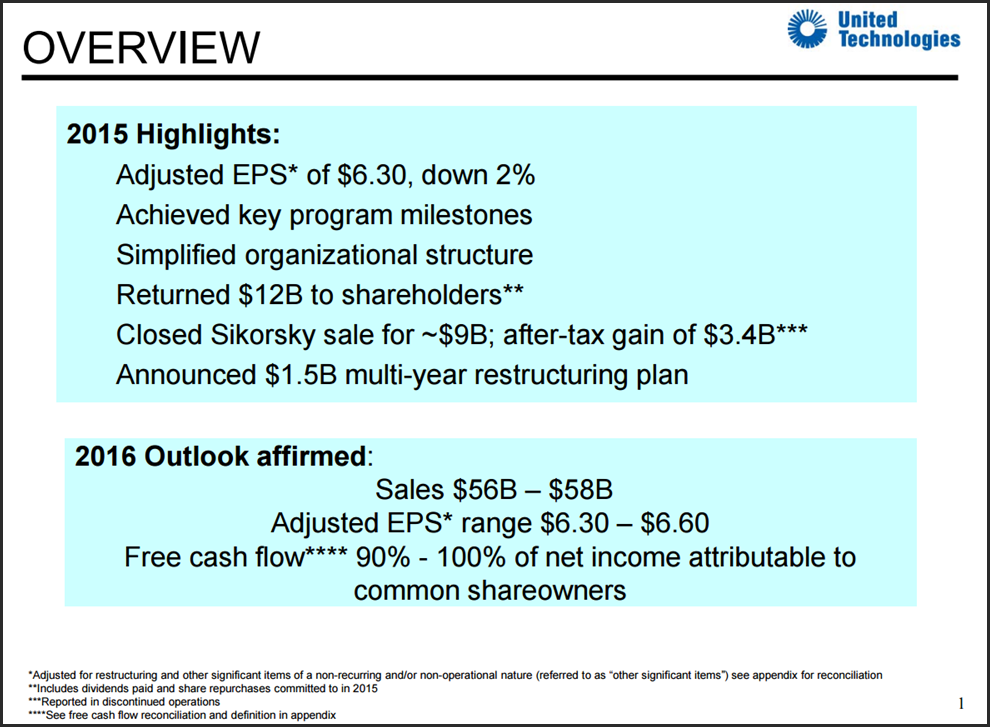

I will also look for press releases where the company will announce important actions such as divestitures, acquisitions, and of course their most recent quarterly filings. What follows is an excerpt of their most recent financial report and a few associated slides:

“UTC Reports Full Year 2015 Results, Affirms 2016 Outlook

Wed January 27, 2016 6:58 AM|PR Newswire

"I'm pleased to report UTC's 2015 earnings reached the top end of expectations we set months ago," said UTC President and Chief Executive Officer Gregory Hayes. "Solid execution on our strategic priorities has set a strong foundation for future growth.

"In line with our 2015 strategic priorities, we took decisive actions to streamline our portfolio with the divestiture of Sikorsky and return over $12 billion to shareowners. Returning cash to shareowners continues to be a top priority and we are still targeting $22 billion of total shareowner returns through share repurchases and dividends from 2015 through 2017," Hayes said. "We also streamlined UTC's organizational structure and initiated a $1.5 billion multi-year restructuring plan to improve competitiveness.

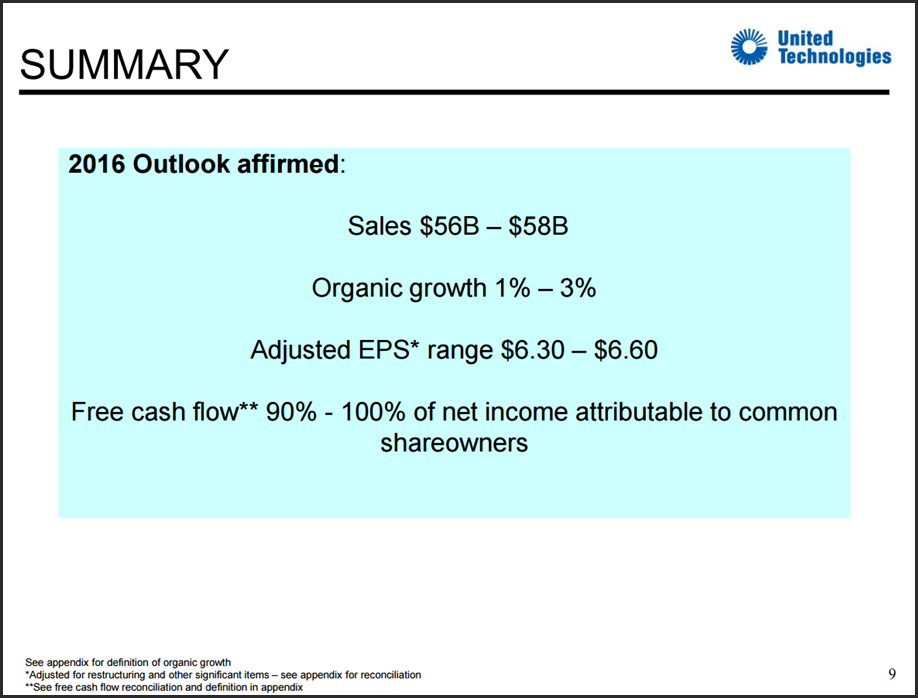

"As we enter 2016, the tough actions that we've taken, and will continue to take, put us in position to achieve our financial objectives. We remain confident in our full year 2016 Adjusted EPS expectations of $6.30 to $6.60 on sales of $56 billion to $58 billion, despite a difficult macro environment," Hayes added.

“UTC continues to anticipate 2016 free cash flow in the range of 90 to 100 percent of net income attributable to common shareowners. The company also continues to expect share repurchase of $3 billion in 2016, beyond the repurchases that will be completed in 2016 under the previously announced $6 billion accelerated share repurchase program. UTC continues to assume a $1 billion to $2 billion placeholder for acquisitions in 2016.”

Diving Deeper into the Financials

Moreover, since it is facts that I am after, I will attempt to organize and gather all of the financial and fundamental information that is available to me. Of course, as regular readers of my work would expect, I personally rely on F.A.S.T. Graphs and FUN Graphs (fundamental underlying numbers) to organize and reveal essential financial information that cumulatively will be vital regarding my ability to make a sound investing decision. Of course, it is only fair for me to recognize and disclose that there are many other fine research tools available.

At this point in my due diligence process, my focus is on ascertaining the financial health and strength of the company. Therefore, I now turn to a review of the company's balance sheet, cash flow statement and income statement. Of course, this can only be accomplished through a review of the company's financial statements found in their annual and quarterly reports. Since this can be a tedious and time-consuming task comprised of digging through and pouring over financial reports and spreadsheets, I developed FUN Graphs to make the task easier, more efficient and fun (pun intended).

United Technologies Corporation: The Balance Sheet

In my opinion, United Technologies has a pristine balance sheet. This is consistent with the company’s S&P credit rating of A- .

United Technologies Corporation: The Cash Flow Statement

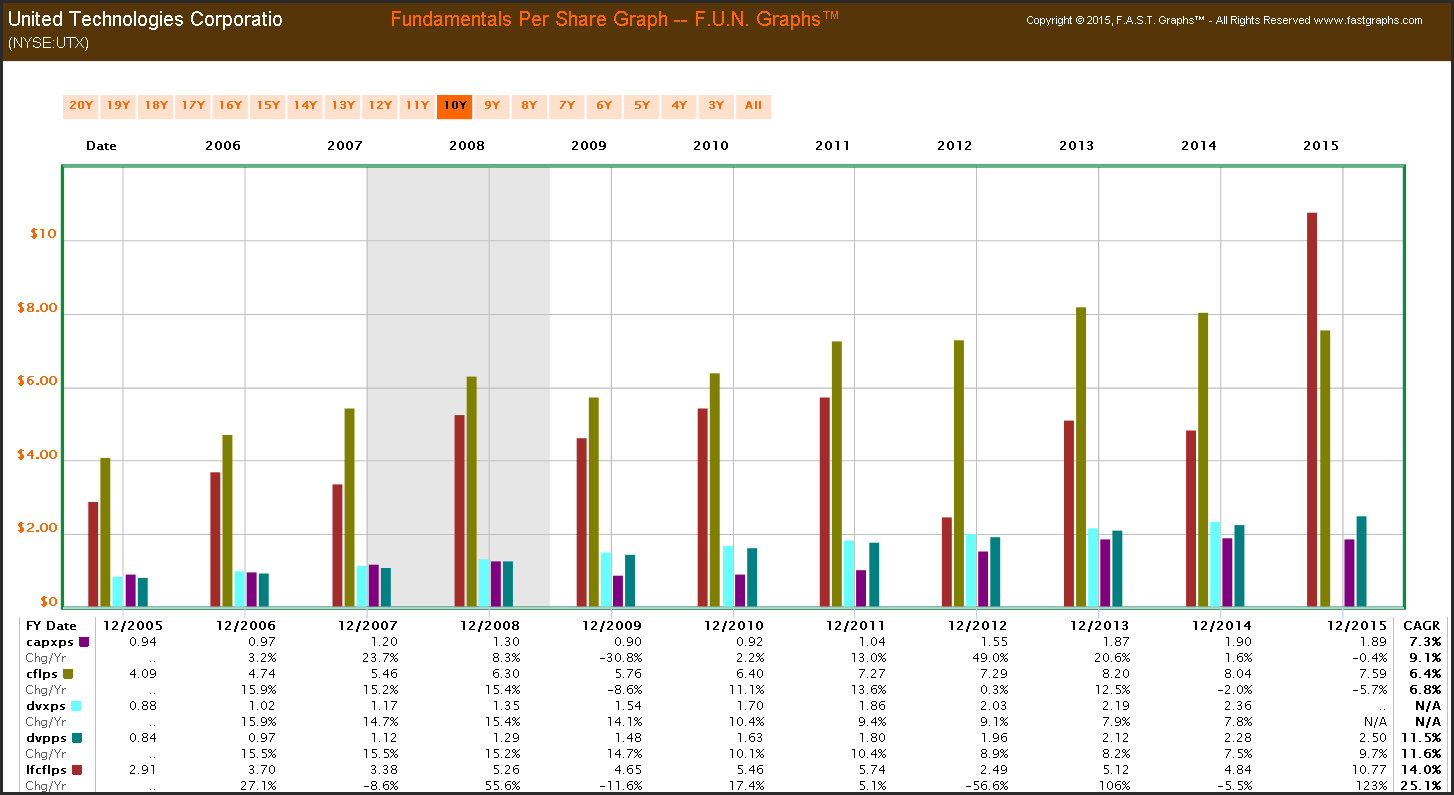

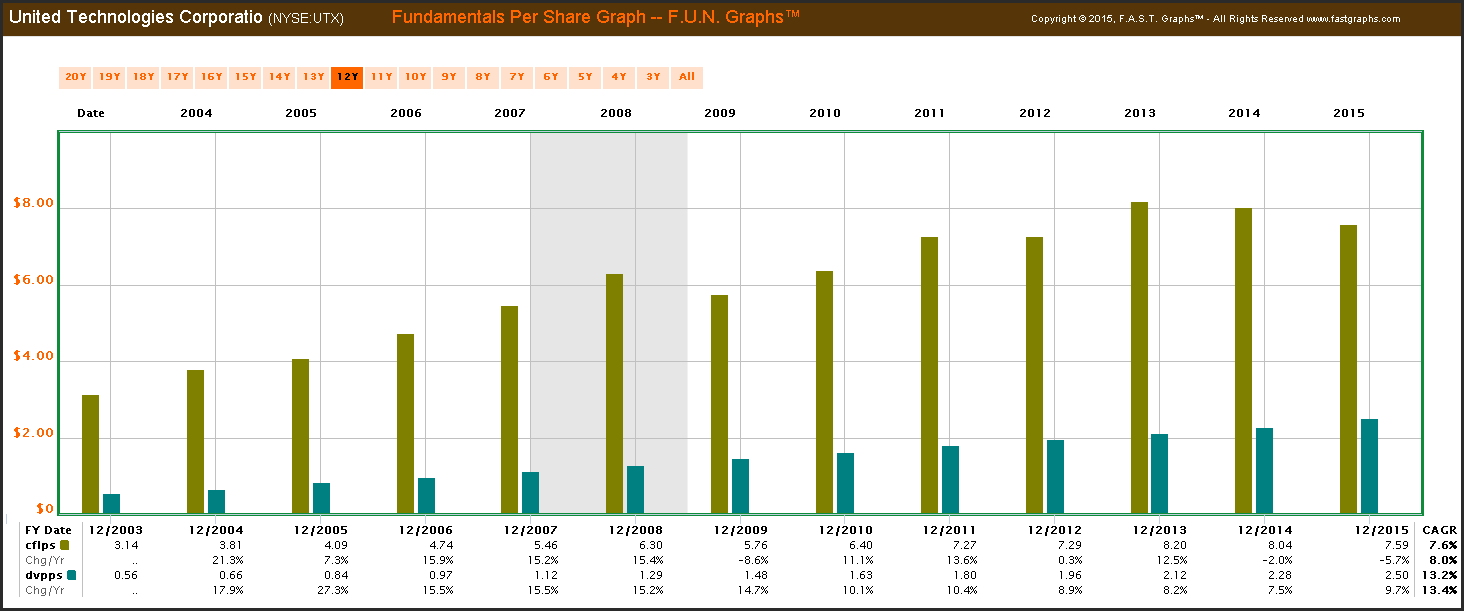

United Technologies Corporation produces prodigious levels of cash flow fully capable of supporting their growth needs with plenty left over for dividends.

United Technologies Corporation: Key Items from the Income Statement

United Technologies Corporation produces strong revenues and their cost of goods sold was reduced in 2015.

United Technologies Corporation: Revenues (rev)

Although United Technologies Corporation’s revenues were down in 2015, they remained at healthy levels.

United Technologies Corporation: Gross and Net Profit Margins (annual and quarterly)

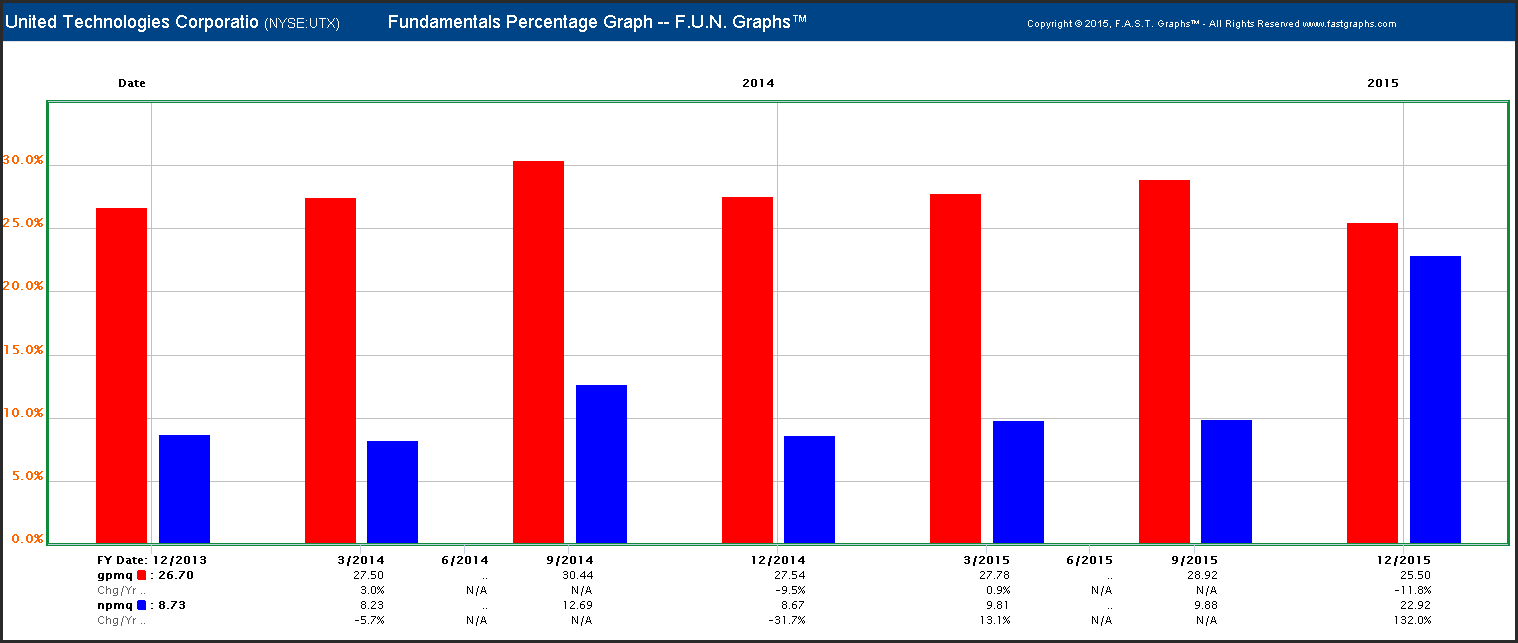

United Technologies Corporation produces steady and strong gross (gpm) and net profit margins (npm). I find it encouraging that even though revenues were down in 2015, both gross and net profit margins increased. I attribute this to management’s focus on cost controls.

2014-2015 Quarterly Gross (gpmq) and Net Margins (npmq)

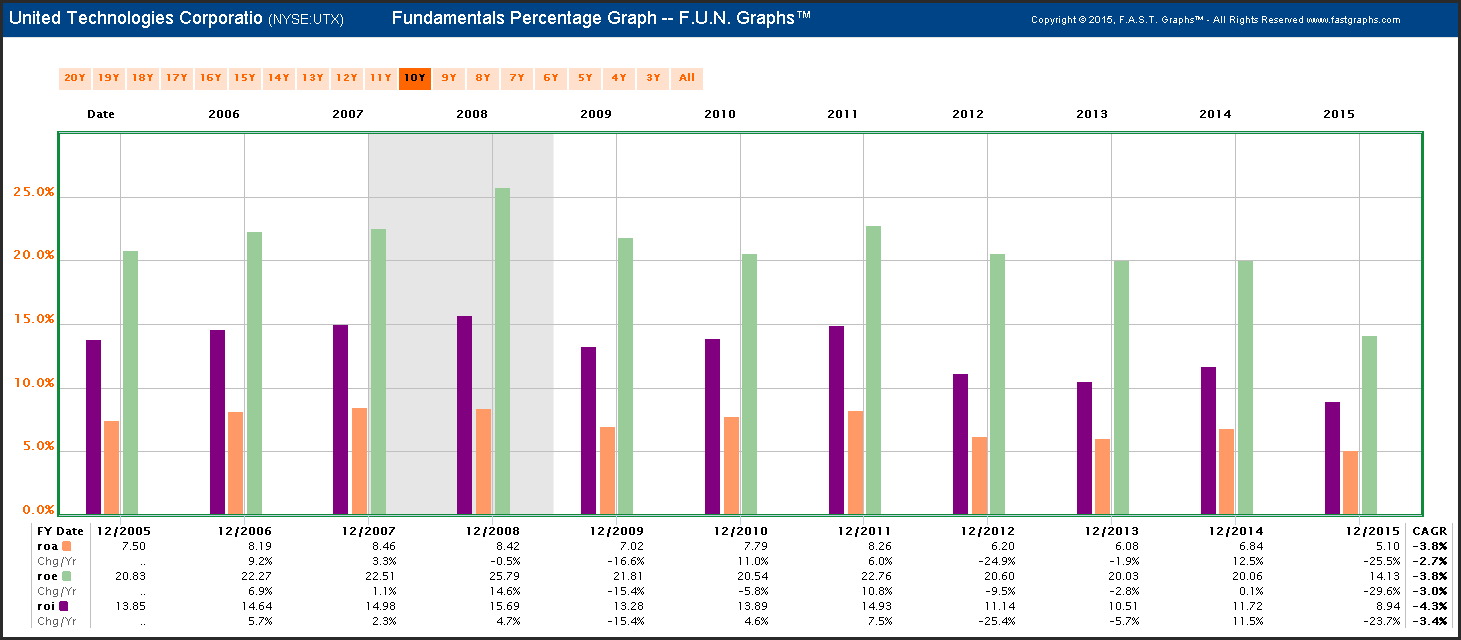

United Technologies Corporation: Returns on Assets, Equity and Invested Capital

United Technologies Corporation produces solid returns on assets (roa), returns on equity (roe) and returns on invested capital (roi). Although each of these metrics were down in 2015, they remain at healthy levels.

United Technologies Corporation: Forecasting the Future (Earnings, Dividends and Returns)

Now that I’ve gone through my research and due diligence process, it’s time to make some reasonable forecasts about what the future might hold for United Technologies Corporation. I will base my forecasts on earnings expectations and then calculate the potential future returns I could reasonably expect from a combination of dividends and capital appreciation.

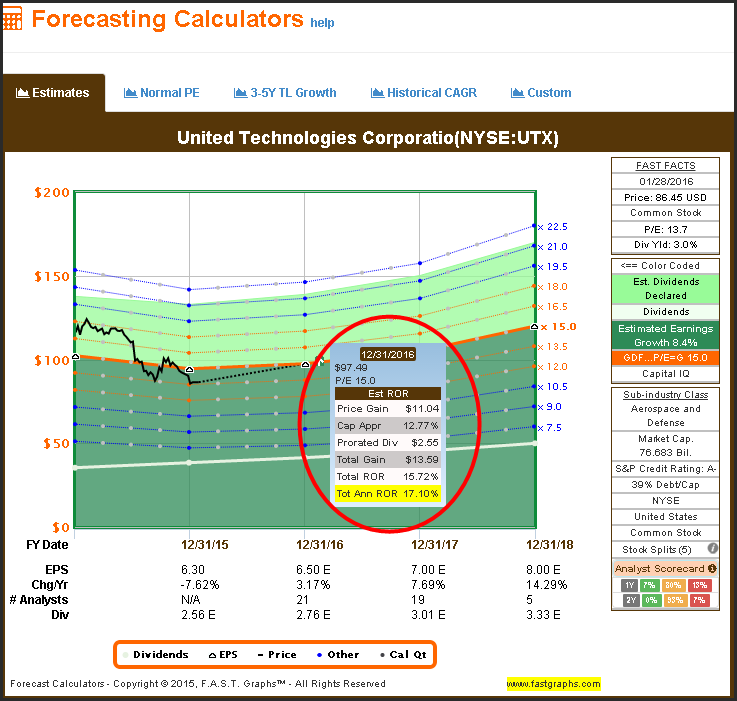

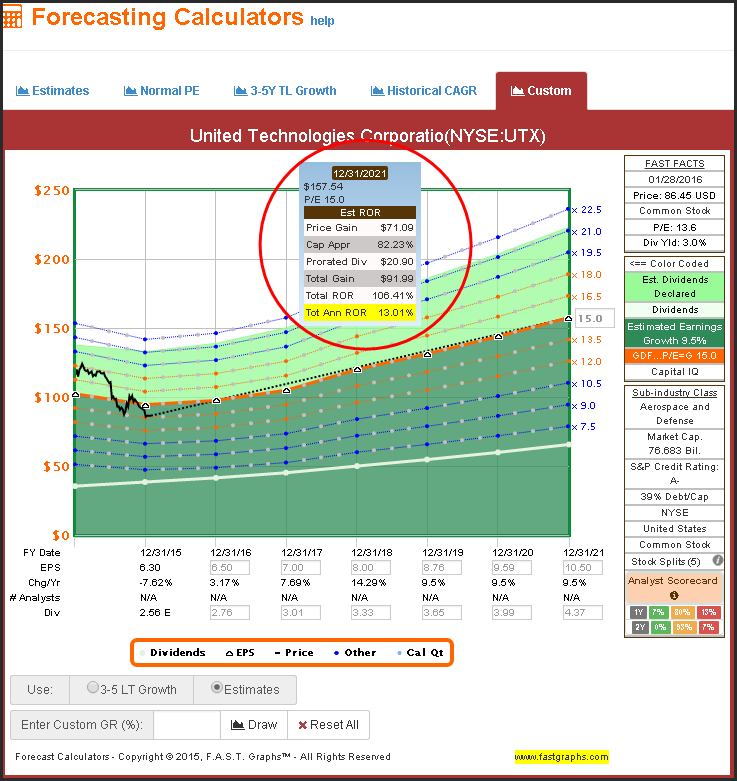

I will start by focusing on consensus analyst estimates for fiscal year-end December 2017. As previously discussed, I have done my own analysis and recognize that these consensus estimates are in line with company guidance. The median consensus estimate for 2016 earnings is $6.50, which is within management’s guidance range of $6.30-$6.60. If I apply a reasonable P/E ratio of 15 to that estimate, I can expect a total annual rate of return in excess of 17% over the next year. I consider this a reasonable case and possibility.

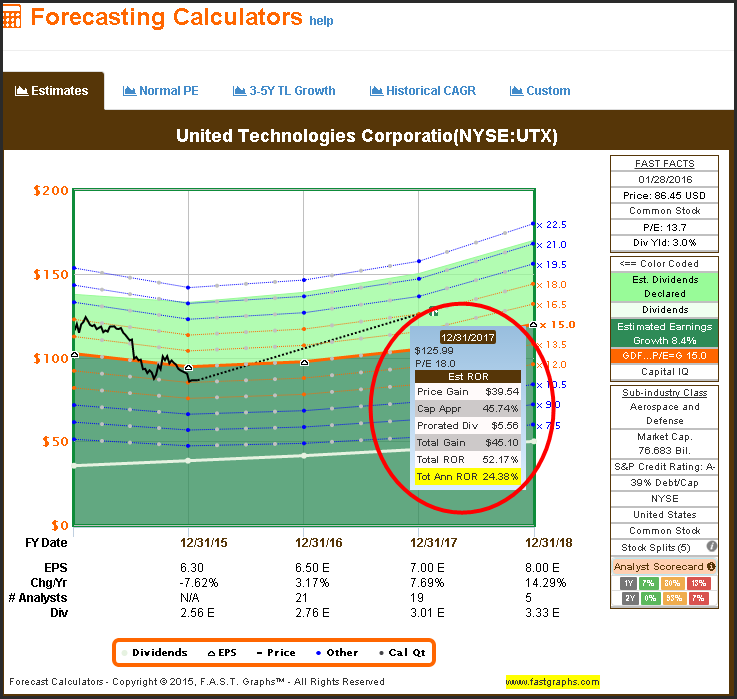

For a more optimistic view, I ran a second “what if” scenario based on consensus earnings estimates through 2017. However, in this more optimistic case, I ran a calculation based on the historical normal premium P/E ratio of approximately 18 that the market has applied. Under these calculations, my total annualized rate of return would be in excess of 24%. I consider either my previous calculation or this more optimistic calculation both potentially reasonable and achievable. But more importantly, I like both numbers.

I also looked at the analyst scorecard for United Technologies Corporation based on both 1-year forward and 2-year forward estimates. Although this does not guarantee that the estimates will be correct, it does engender confidence that the probabilities are high that they will be within a reasonable range of error. Analyst estimates have been within a reasonable range of accuracy 87% of the time with 1-year forward forecasts, and 93% of the time with a 2-year forward forecast.

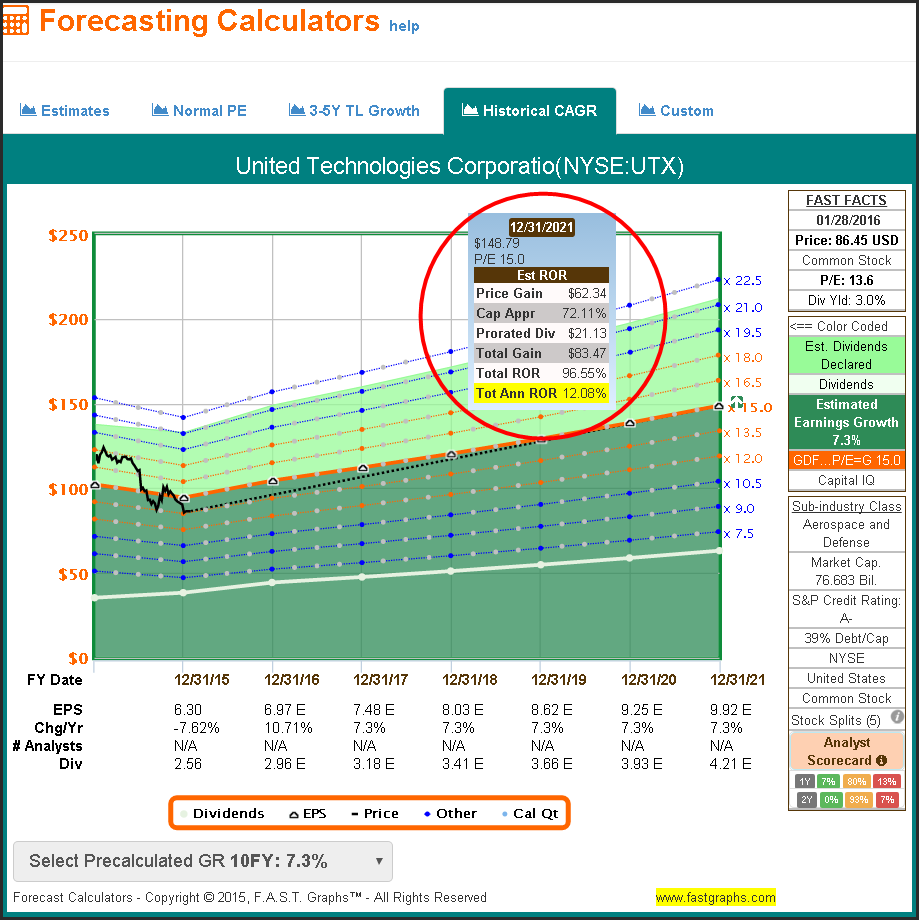

When I am making forecasts and return calculations, I prefer to run numerous “what if” scenarios. These would include best case, worst case and my most reasonable expectation. In addition to the analyst’s estimates and company guidance, I also like to run calculations based on the company’s normal historical growth achievements. The following calculations are based on the earnings growth rate of 7.3% that the company has achieved over the past completed 6 years. Once again, I like the number this would produce if this were to occur.

Finally, in addition to near-term consensus analyst estimates, I also like to evaluate the long-term (3 to 5 year) growth estimates that analysts also provide. The following Forecasting Calculator blends near-term specific estimates with analyst’s long-term expectations. Once again, I like the numbers even after applying a conservative P/E ratio multiple of 15.

United Technologies Corporation: WHY INVEST IN UTC

United Technologies Corporation has a section in their website titled “Why Invest in UTC” where management presents their case for investing in their business. Since my personal motivations for investing in this company are quality, a current high yield and dividend growth with moderate to above-average and predictable capital appreciation potential, I especially liked what I saw in the following slide. This tells me the company and its management is committed to its dividend policy.

My confidence in the company’s willingness and capability of continuing to pay and grow their dividend is also enhanced when I look at how well their dividend is covered by cash flows. My own conclusions are that this company is fully capable of and committed to continuing to grow their dividend.

I admire this company’s management team and the good work they have done growing the business historically. I also like their focus on growth, controlling costs and willingness to adapt and change when they feel it’s necessary. But most importantly, the following excerpt suggests to me that the company has a well thought-out plan and perspective on their business and its future potential.

“POSITIONED FOR GROWTH

By focusing on our core aerospace and building systems businesses, investing in game-changing technologies and continuing to expand our presence in emerging markets, we are uniquely positioned to capitalize on two megatrends that are shaping modern life — mass urbanization and rapid growth in commercial aviation.

Across emerging markets, tens of millions of people a year are migrating to urban centers, leading to enormous growth in the commercial building industry. As the world urbanizes, increased air travel follows. According to industry estimates, airlines will add 30,000 new commercial aircraft over the next 20 years to replace aging fleets with more fuel-efficient planes and expand capacity across Asia.

In addition to being well positioned in growth markets, we also maintain a relentless focus on cost reduction, enabling us to continuously target industry-leading margins. Using our ACE (Achieving Competitive Excellence) operating system, we leverage our global scale to drive efficiency, productivity and a commitment to perfect quality throughout the organization. This “One UTC” approach enables us to delight our customers every day, across the product portfolio, functions and geographies.

A relentless focus on growth markets, cost reduction and industry-leading margins: This is UTC.

FOCUSED ON INNOVATION

To grow, a company also needs to develop great products. At UTC, we focus our research and development investments on products that address local market needs, deliver value to customers and lead to revenue growth. Recent examples include Carrier Transicold’s launch of the Citimax™ line of small truck refrigeration units for the market in India. In 2013, Otis introduced the Gen2® Switch elevator, which uses 81 percent less power than traditional systems and is capable of operating on battery, solar or wind power — ideal for areas with frequent power outages.

We are using innovative technologies to design and build the next generation of jet engines and aerospace systems, including additive manufacturing to produce complex, precision engine components. Pratt & Whitney’s PurePower® engine with Geared Turbofan technology is transforming the industry with significant reductions in fuel burn, emissions and noise. We are also leaders in the development of advanced new composites — stronger and lighter weight than conventional materials — for use in a broad range of components, including nacelles, drive shafts, wheels and brakes, and fuel lines.

UTC was ranked among the world’s most innovative companies for the second consecutive year in 2013 by Thomason Reuters.”

Many investors have strong views about whether share buybacks are beneficial or harmful. My personal view is that they can be either, depending on the company’s valuation. When a company’s price valuation is high, I consider buybacks harmful. In contrast, when a company’s price valuation is low, I consider them beneficial. United Technologies Corporation: Shareholder Friendly Stock Buybacks

I found United Technologies Corporation’s historical record on buybacks instructive regarding the quality and capabilities of the company’s management. In 2004 and again in 2011, 2012 and 2013 United Technologies Corporation was actually issuing stock during times when the valuation was high. In contrast, they have recently announced an aggressive buyback plan (partially funded by their divestiture of Sikorsky helicopters) during this timeframe when their valuation is low. See the corresponding circles on the two graphs below.

United Technologies Corporation: Confidence from My Personal Experience with the Company

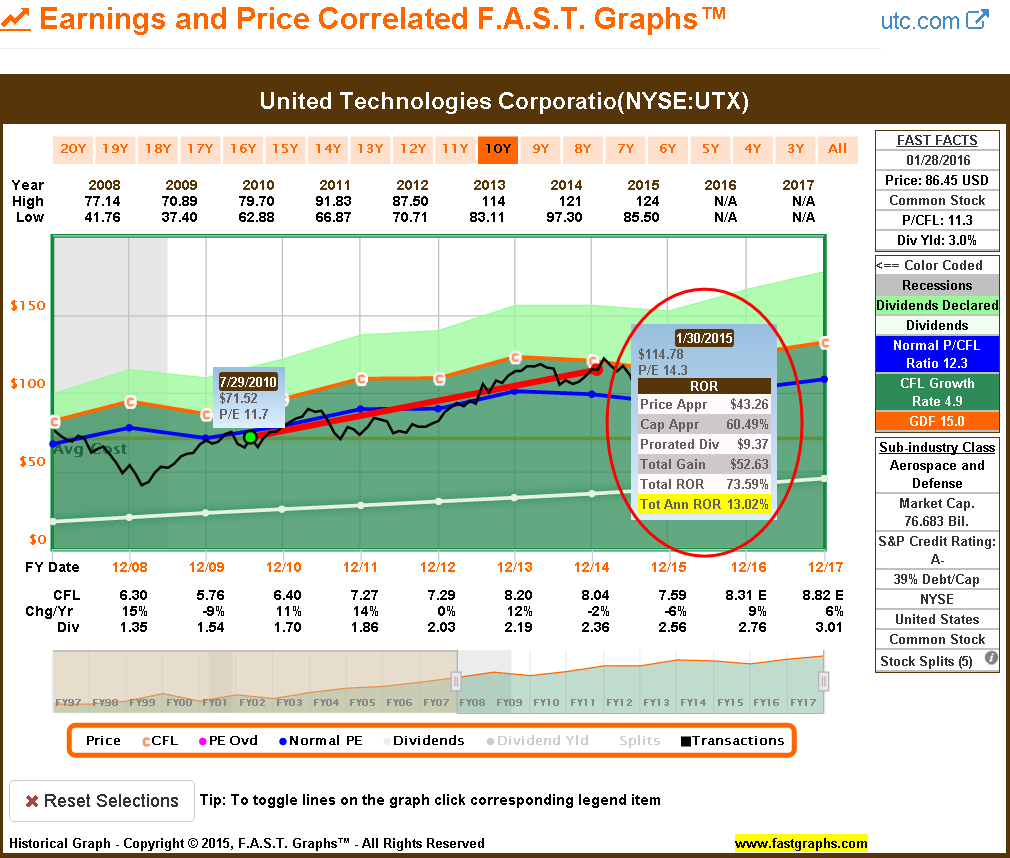

As I previously mentioned, I have been long United Technologies Corporation since July 2010. The following two price and cash flow correlated graphs have a green dot when I purchased United Technologies Corporation. On the first graph, I use the calculating function of F.A.S.T. Graphs™ and run a calculation based on buying a stock when the price was at a discount to its cash flows and measuring its performance when it went back into alignment with fair value based on cash flows in 2015. This timeframe generated a healthy total return in excess of 14% per annum and a healthy amount of dividend income paid along the way.

On this next graph, I again run a calculation only this time it is based on the company stock price currently trading again at a discount to its cash flow justified valuation. In this case, I still have a total annual rate of return approaching 6% per annum which I regard as attractive considering the current low valuation. But what I find most intriguing after running this calculation is the power and importance of a growing dividend income stream.

United Technologies Corporation’s stock price fell precipitously over most of 2015 but their dividend continued to grow each year after my original purchase. I do this as a classic example of how a dividend can buffer poor performance during a down market.

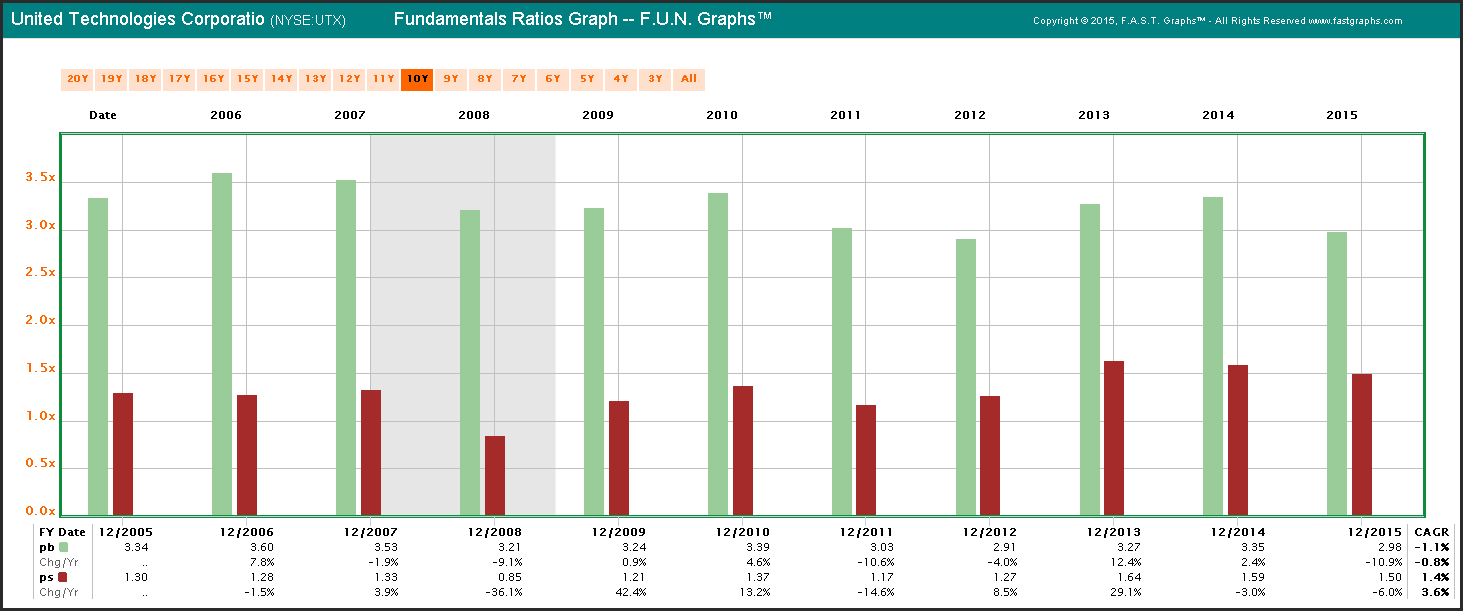

United Technologies Corporation: Valuation Ratios

In addition to the basic price to earnings and price to cash flow valuation metrics, I like to run the company through several other valuation ratios. The following FUN Graph shows that United Technologies Corporation is attractive based on price-to-book (pb) and price to sales (ps). These are not the only valuation measurements I run, but are offered simply as an example. You might recall that I also valued this company based on its historical dividend yield earlier.

Summary and Conclusions

What I have attempted to do in this article is simply share my own personal approach to conducting research and due diligence on stocks I am interested in. I cannot stress enough how important I believe it is to thoroughly research any company you are interested in investing in. Admittedly, it can be a rather complex and time-consuming process. However, like any job, if you have the right tools the task can be completed without a lot of stress or strain. This is one reason why I personally prefer relatively concentrated portfolios. The fewer stocks you own, the easier it is to know what you need to know about each of your holdings.

On the other hand, conducting research and due diligence on a common stock can actually be fun. Personally, I enjoy learning about companies, their management teams and their future prospects. And of course, I especially enjoy the process when I believe I have found a bargain. I get excited when I see what appears to be a great business on sale. Consequently, I am willing to perform the necessary research and due diligence with great enthusiasm. But perhaps most importantly, I do not let short-term price action contaminate my thinking. Company management teams have some capacity to control the operating results of their business. However, they have no control of how the market might price them, especially in the short run.

Disclosure: Long UTX and MDT.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.