“The greatest obstacle to being heroic is the doubt whether one may not be going to prove one’s self a fool; the truest heroism is to resist the doubt; and the profoundest wisdom, to know when it ought to be resisted, and when to be obeyed.”

Nathaniel Hawthorne, 1804-1864

American novelist

When it comes to the stock market, it is clearly a time for much doubt, but perhaps also heroism. As we write, the market is in the midst of a nasty sell-off, the worst start to a year in U.S. stock market history, with every sector down for the year with the exception of utilities. Global stocks have fared even worse, losing $14 trillion since peaking last May1 and more than $2 trillion during the first week of January alone. The beginning of the year is an especially inauspicious time for a stock market plunge as markets often trend in the direction of the year’s first week. The 24 other years since 1950 in which the S&P 500 Index declined during the first week averaged a paltry 0.7% return for the year in total. But do not despair, there are many good reasons to remain positive, not least of which being we came into the year holding a near 20% cash position, which has helped cushion against the market declines. Additionally, there are indeed bright spots in the economy and despite legitimate economic disturbances this is certainly no 2008.

What is going on here? First there are a number of macro trends that continue to shake confidence. The first is continued economic weakness in China, where the vulnerability of their economy, and now their currency2 , is garnering greater attention. Next is the deepening oil price route, which is starting to dominate attention as investors are finally waking up to the idea that a low oil price will impair the ability of oil companies to pay back the massive debts they have incurred in the last few years. And finally there is the tremendous strength of the U.S. dollar, driven by the tightening Fed being out of step with the loosening Rest-ofthe-World. As an aside, this is a great time to take that foreign vacation you’ve been thinking about; to take just one example, the dollar has recently hit a historic high against the Mexican Peso, rising by a quarter this past year.

Meanwhile we are also starting to see a number of ominous signs of a potential U.S. recession:

• The yield curve is flattening, meaning that longer-term rates are not as far above short-term rates as they used to be. An inverted yield curve (short-term rates above long-term rates) is one of the classic signs of a recession, and a flatter curve brings us one step closer.

• The Dow Jones Transportataion average has declined more than 24% from its December 2014 high. A 20%+ decline in this economically sensitive index has, in 22 of the 29 cases since 1940, signaled a forthcoming 20%+ bear market for the broader S&P 500 Index.

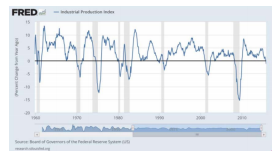

• U.S. Industrial Production declined over the last year for the first time since 2009. Annual declines have consistently flagged recessions in the past (gray bars on the chart on the next page).

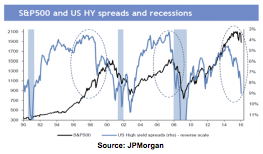

• Finally, high yield spreads are widening, meaning low-quality companies are finding it more difficult to get financing vis-à- vis their high quality, more stable bretheren. This has some investors particularly worried as high yield spreads have been known to lead equity returns in the past.

• Finally, high yield spreads are widening, meaning low-quality companies are finding it more difficult to get financing vis-à- vis their high quality, more stable bretheren. This has some investors particularly worried as high yield spreads have been known to lead equity returns in the past.

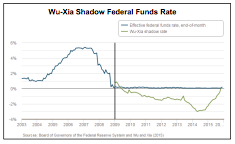

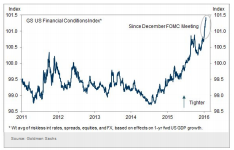

On the supposedly positive side of the ledger, some bulls have asserted that we can’t be in the start of a recession-driven bear market because recessions usually don’t begin until the Fed has been tightening for 3+ years. Our rejoinder is to question: when did the Fed tightening start? In normal times, the first rate increase (which we got in December) would be the beginning of a tightening cycle, but considering the amount of quantitative easing (a.k.a. Q.E.; a.k.a. money printing) this cycle is anything but typical. A very compelling argument can be made that the beginning of the tightening cycle should date back to the “tapering” of Q.E, which was in the beginning of 2014. Under this interpretation, we are already two years into the tightening cycle, and so a bear market and/or a recession would be more or less on schedule. The idea that we are substantially far along in the tightening cycle is backed up by the graph found on the bottom of the prior page one showing the “shadow” federal funds rate3 has been rising since 2014 and the chart to the right showing the effect this shadow tightening has had on financial conditions.

So what does all this mean for the markets going forward? In the broadest scope, that depends on whether or not we have a recession. Absent a recession, a full 20% bear market drop is unlikely. Though rare, bear markets unaccompanied by recessions have produced declines of 26% on average. Importantly, these declines are recovered quickly (under six months on average). (So far, the S&P 500 has “only” fallen 12% from its May peak, though the typical stock is down more than the index.) However, if a recession is in the cards, we may expect something closer to the historical average peak to trough decline of 44%, and a much longer durational average of 20 months.

Our position is that the U.S. is not likely to have a recession and if we do it will be a relatively mild one, nothing like the Great Recession of 2008, which included a financial crisis that will not be soon repeated (at least not in the U.S.). While China is someday headed towards a financial comeuppance due to rising debt levels and scores of unprofitable mega-projects, the direct financial linkages to the U.S. are few and, despite all the bashing of Dodd-Frank bank regulations from both the Left and Right, the American financial system is now in pretty good shape with banks holding much more capital to shore up their assets than was the case in 2007. Consumers too have repaired their balance sheets by paying down debt (this is actually one reason the recovery has been anemic, though not necessarily a bad thing because while consumer debt fuels growth, it brings instability). Finally, despite much hand-wringing about the Fed having no room to lower rates if the economy does stumble, there is nothing to stop it from easing via another round of Q.E.4

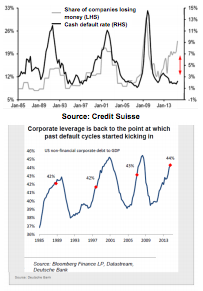

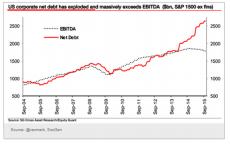

Despite not seeing a full blown financial crisis, we do expect to see increased financial turmoil, just not turmoil that spirals out of control. Until very recently the financial seas have been calm indeed, with record low bond defaults occuring, despite a non-recessionary high number of companies actually losing money as the chart at right shows. So far this situation has been allowed to persist as the financial markets were generously financing unprofitable companies. With the trouble abroad, and narrative of Fed tightening out there, we expect banks and credit markets to pull back a bit, sparking defaults, and sparking further pulling back. We suggest that now would not be a good time to put oneself in a position of being at the mercy of the credit markets... and yet this is exactly what companies have been doing, as the charts on the bottom right and atop the next page highlight.5 If financial conditions tighten as we expect, some air will likely come out of all stock prices. However, for the last few quarters we have endeavored to buy stocks whose valuations rest on current earnings, current cash flows, and current bank accounts; a lot less air should be let out of these valuations as opposed to those whose lofty heights are built on the hope and promise of successes not yet achieved.

Given the potential for financial tightening and corporate defaults, why wouldn’t we expect a recession? The short answer is we will be looking for the U.S. consumer to bail everyone out. The drop in oil prices might be bad for international financial stability but it is hugely stimulative for the average American shopper. So far the expected spending boost has largely yet to materialize, but this is likely due in large part to the decline in gasoline prices being viewed as a temporary blip of cheap gas in an era of increasingly expensive gas... and it is slowly becoming more and more apparent every day that lower prices are here to stay. In addition to oil, grains (and therefore food), raw materials, and foreign labor (due to the rising dollar) have all dropped in price, and inflation has otherwise remained low. So far, consumers have largely opted to pay down their debt and save more as opposed to hitting the mall. However, the improving labor market should only increase the confidence to spend, and this spending should do much to offset the weakness in energy and manufacturing. These industries matter but are overshadowed by consumer spending which makes up 71% of U.S. GDP. With this in mind, our most recent purchases have been companies that should benefit from increased consumer spending.

In summary, we expect the U.S. economy to trudge forward though the overall stock market may be more challenged in 2016. Market downturns and economic uncertainty are permanent features of what have been and we expect will continue to be rising stock market values over time. In fact, market pullbacks are just the sort of occurrences for which we have prepared, and are actually necessary to produce the kind of bargains that allow us to put your cash to work.

As always, we appreciate the trust you place in us.

Sincerely,

John G. Prichard

Miles E. Yourman

1 To be fair, a substantial portion of these losses come from stating them in dollar terms because the greenback has appreciated by some 12.5% since May against a tradeweighted basket of foreign currencies.

2 We expect the Chinese Yuan to ultimately have perhaps another 30% to fall before it is through. As we have discussed, these “devaluations” are being caused by market forces, not the machinations of the Mandarins.

3 This is a measure of what the federal funds rate would be if it could go below zero and is derived from the term structure of interest rates.

4 At least one prominent investor, Ray Dalio of Bridgewater, the world’s largest hedge fund firm, has suggested that another round of Q.E. is more likely than a substantial round of rate tightening. When it comes to macroeconomics, Mr. Dalio is one figure worth listening to.

5 Incidentally this is part of the reason why we believe “rates are never going up, ever”. The low interest rates that prevailed in the wake of the financial crisis encouraged companies to take on more debt as the lower interest payments meant companies could service more debt with the same cash flow. If the Fed were now to aggressively raise rates, they would risk putting many of these companies in danger of default. The Fed will need an outlook stronger than today’s to be able to safely crank rates back up.

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

© Knightsbridge Asset Management, LLC