Recent economic data releases have been mixed. However, despite strong job figures, most have been on the soft side of expectations. Lower commodity prices are tough for producers of raw materials, but beneficial to the buyers of those materials. However, the bigger concern is why commodity prices are falling. Many view the drop in oil prices as signaling a more pronounced global slowdown and fear that the U.S. domestic economy may not be robust enough to escape that. The anecdotal data from the manufacturing sector is much worse than is suggested by the hard economic data reports.

Last week, we heard more talk of the possibility of a U.S. recession. Curiously, while the odds have gone up, a recession in 2016 is still viewed as unlikely. We are never “due” for a recession. The probability of recession does not depend on the length of the economic expansion preceding it.

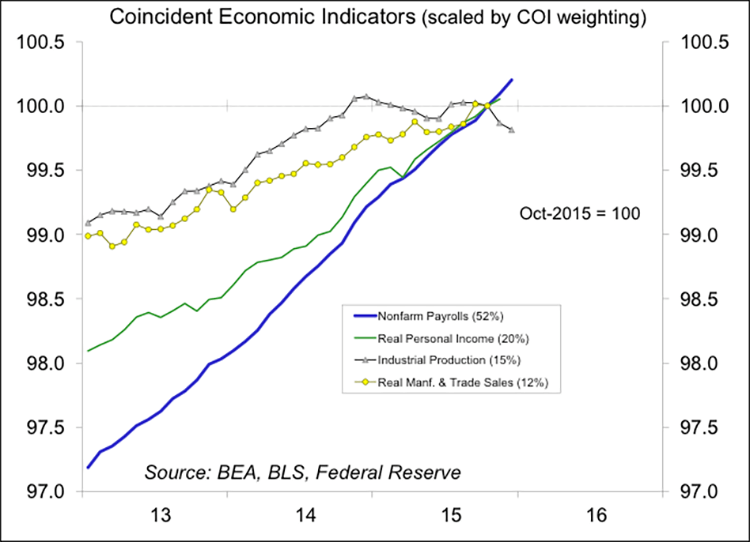

We’ve never had a sustained decline in industrial production without a recession in the overall economy, but that doesn’t mean much – as the manufacturing sector has accounted for an ever smaller share of the U.S. economy.

What do we mean by “recession?” The common definition is “two consecutive quarterly declines in real Gross Domestic Product.” However, for the U.S., that’s only a rule of thumb. The official call is made by the National Bureau of Economic Research’s Business Cycle Dating Committee (which sounds like a lonely hearts club for pedaling nerds). A recession is defined as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.” Nonfarm payrolls, a coincident indicator, have continued to improve at a strong pace. Industrial production is now trending a bit lower. Real personal income should be moving higher.

In recent months, the weakness in industrial production has been most pronounced in the output of utilities (unseasonably warm temperatures) and the contraction in energy exploration. Manufacturing output has softened, but not a lot. However, the Fed’s IP data measure real output (which doesn’t appear to be falling much and may be supported by quality adjustments). Nominal factory shipments fell 3.9% in the 12 months ending in November (durables +1.7%, nondurables -9.1%). Export prices are down over 10% since December 2013. Anecdotally, manufacturers generally report that things are tough all over, reflecting soft global demand and the impact of a strong dollar.

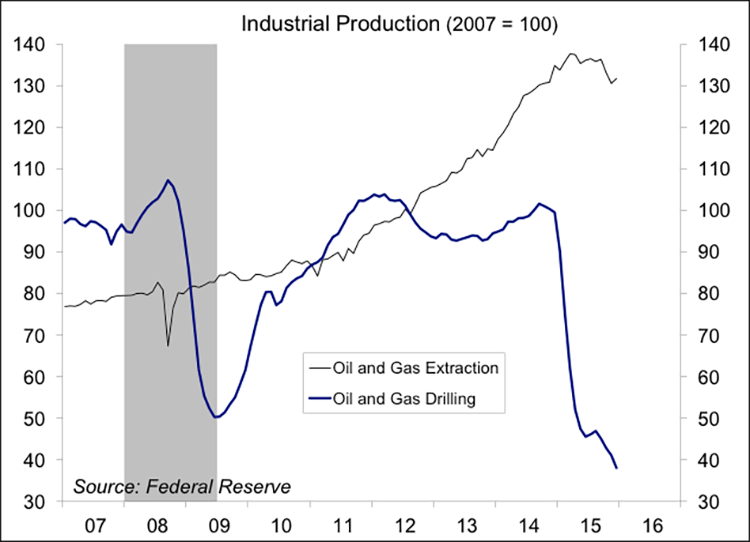

Energy has been an important component of the U.S. economic recovery. Up until the bust in oil prices, jobs in energy exploration were rising about five times faster than overall employment. However, the number of jobs is tiny compared to overall nonfarm payrolls (we’ve lost 129,000 mining jobs since the end of 2014, while nonfarm payrolls rose by more than 2.6 million). While this may be devastating for local communities (these tend to be high-paying jobs), it’s not much on a national level. On the other hand, energy exploration, which is capital intensive, has been a much bigger factor in business fixed investment. Much of the correction took place in the first half of 2015. However, the price of oil has now gone from $60 per barrel in late June, to below $30. Simply put, if $40 was “horrible” for most energy producers, $30 will be “impossible.”

The bigger concern is why oil prices have fallen further. Some of that is supply, but we are seeing global investors react to the day to day movements in the price of oils as if it were a gauge of global economic strength – hence, adding to the negative mood.

Can the U.S. economy withstand global weakness? Of course it can. Our economy is largely self-contained, with consumer spending (70% of GDP) being the key factor. However, 2016 GDP growth may be slower than what we had hoped to see.