Simplify Your Research Process and K.I.S.S. Your Worries Goodbye

Introduction

Most everything I write about is based on my belief in value investing as a sound, prudent and profitable long-term investing strategy. At its core, value investing relates to getting value on your money with investing just as it would to getting value for anything you would purchase. I feel safe in saying that no one wants to pay more than they should for anything that they purchase. This would apply to the basic necessities of food, clothing and shelter, and everything else that we would want to buy. Consequently, I don’t think it should be any different when we are buying stocks.

In this regard, most people execute a rather sane and simple strategy when purchasing most things. Intelligent shoppers are always on-the-lookout for bargains or sales. Moreover, most intelligent shoppers have a general idea of what the merchandise they are desirous of purchasing is worth. As a result, they are excited and appreciative when they see merchandise they want selling at a bargain price. Ironically, this seems to hold true for most every shopper except most common stock shoppers. I have long found it curious that common stock investors seem to hate it when their stocks go on sale.

Many times in the past I have utilized the following metaphor to illustrate my frustration with many common stock shoppers that I have personally talked to. Imagine for a moment that you pulled up to your favorite retail store and noticed that the parking lot was full. As a result, you had to circle the lot many times just to find a place to park. When you finally entered the store, you noticed that every aisle was jam-packed with people with full shopping carts feverishly pulling merchandise off the shelves. It could only be described as a shopping frenzy.

At that moment, something odd happened. The manager of the store got on the intercom and announced to all the customers in the store that the store wanted to reward their loyal shoppers. For the next hour the manager said everything in the store is going to be marked down 50% off. Before the store manager’s words were barely out of his mouth, you noticed something remarkable. Every shopper in the store instantly abandoned their already-full shopping carts and ran out to their cars and into the parking lot.

Fortunately, the store manager immediately came to his senses and made another announcement through speakers located in the parking lot area. He apologized profusely, rescinded his half off sale, and further announced that if the shoppers would come back the price of everything in the store would be marked up 50% above what the price was when the shoppers were in their shopping frenzy. With this announcement, the shoppers jumped out of their cars and stormed the doors of the store and once again engaged in a buying frenzy that was even more intense than it was just before they left.

If you think about it, the stock market is the only market on earth where shoppers routinely behave this way. When stock prices are high and inflated, people can’t seem to get enough overvalued securities to add to their portfolios. However, when those same companies go on sale at significant discounts to true value, it’s as if investors are saying they will not by that cheap stuff.

I can only surmise that common stock shoppers behave this way for two important reasons. First of all, they are heavily influenced, and even emotionally traumatized when the price of the stock they own is dropping. Consequently, they must believe that someone knows more than they do about the stock and this engenders fear and anxiety. In my opinion, the second reason might be that they are over-complicating and/or over-thinking their analysis. My experience gives me great confidence that the first reason is valid, and anecdotal experience from talking with numerous investors also suggests that my second reason plays a major role.

With this in mind, this article will present my approach on how investors can simplify their research and due diligence process on common stocks. When I was in the Army, they taught me the “K.I.S.S.” principle: Keep It Simple Stupid. I’m sure most of you have heard that expression before, and this article will present my views on how it can be applied to researching and assessing the fair value of common stocks. To be clear, I will be sharing my personal approach to simplifying how I research and analyze the fair value of any stock I’m interested in.

How Do You Simplify the Research Process: Start by Asking the Big Questions?

Big Question Number 1: Will the company remain an ongoing concern?

Since value investing implies the long-term ownership of good businesses, the most important thing I want to be comfortable with before I invest is whether or not I believe the business is viable longer term. Stated more simply, am I comfortable that the company I am examining is in no danger of going bankrupt or out of business in the near future? I’m not looking for precise growth forecasts at this point; I’m simply asking myself whether or not I believe the business will be around long enough to make me some money.

This greatly simplifies the research process and simultaneously engenders confidence in the investment decision. The simple knowledge that my business is strong enough to survive reduces the anxiety that short-term stock price volatility engenders. Furthermore, this helps me realize that I own a valuable asset regardless of whether other people are currently buying or selling it. Since I’m not worried about the survival of the business, I can have the confidence to let stock price volatility run its course.

Furthermore, true value investors buy the business, not the stock. This is not a trivial statement and represents one of the most important keys to implementing a successful value investment strategy. Almost by definition, investing in a business implies the desire to hold the investment for a long period of time. In the real world, people do not trade businesses. However, in the real world, there are many people that do trade stocks. Since business owners are not planning on selling in the near future, daily price fluctuations can and should be ignored. On the other hand, short-term price volatility can and often does create a lot of anxiety in the minds of active traders.

Big Question Number 2: Do I anticipate that the business will grow long-term or shrink?

I believe that many investors complicate their stock research process through attempting to be too precise, especially with their future forecasts. For example, investors can find specific analyst estimates on most every significant publicly-traded company on the major stock exchanges. These estimates will often include specific earnings numbers for the next few years, and additionally a longer-term forecast for earnings growth rates.

Although I think it’s rational to attempt to have some idea of how fast the company you’re investing can grow, this does not need to be as precise as many investors want or need it to be. To me, it’s significantly easier and more relevant to hold a more general view of the future prospects of a business. In other words, before I stress too much about attempting to forecast precise future growth rates, I simplify the process by evaluating whether I believe the business can grow or will it shrink. If I invested in a sound business at a reasonable or attractive valuation, I don’t need a lot of growth in the future to make money. This is especially true when the company pays a dividend and has a long history of increasing its dividend.

Additionally, I further contend it would be naïve to think that estimates could be perfect. As we all know, the future always contains elements of uncertainty. Therefore, no matter how thorough, dedicated or even capable an analyst might be, none of them have crystal balls. Moreover, as the future unfolds, things change. This can be related to the prospects of an individual company, or perhaps related to dynamic macroeconomic changes.

Therefore, I have always suggested continuous monitoring of each position invested in with a special focus on estimates and guidance. Which brings me to another point, it is my contention that most analyst estimates are heavily impacted and derived from company guidance. As a general statement, it is in a company’s best interest to lowball guidance. Nevertheless, as previously stated, both guidance and estimates can change as time passes.

In summary, I believe it’s more important to hold a general view of whether a company is capable of growing at any rate than it is to attempt to worry and fuss about trying to make a precise calculation of growth. As previously indicated, if I was careful to invest at sound or attractive valuation, any future growth will do. Of course, the more future growth the company generates, the better. However, when valuation is low enough, even the slightest little bit of growth can be long-term profitable.

Big Question Number 3: What am I investing for?

Knowing precisely what you’re investing for also simplifies the research process while simultaneously eliminates much of the worry and anxiety. Therefore, the clear answer to this question can empower you to focus on what’s important and eliminate worrying about things that are not important. Some of the more common choices could be investing for growth, income, or some combination of both. There is no better or worse answer to this question, there is only the answer that is right for you.

For example, if you are truly investing for income and perhaps future income growth, then the most important thing to focus on would be the dividends your companies are paying. Dividend income is a function of the number of shares you own and not subject to the fluctuating price of the stock. In other words, whether your stock price is rising or falling, your dividend income will be unaffected. In this regard, you should be most concerned with what dividend the company is paying on a per-share basis, and additionally whether they will pay more or less in the future. If you can discipline yourself to do this, you will worry much less about stock price volatility. Consequently, you will be more prone to make intelligent decisions rather than emotional ones.

Wal-Mart Stores (WMT)

To more clearly illustrate what I’ve written thus far, I offer the following analysis on Wal-Mart Stores in the context of the three big questions presented above.

Big Question Number 1: Will Wal-Mart Stores continue to be a going concern?

I would find it hard to believe that Wal-Mart won’t be around long after I am no longer visiting this planet. In other words, I have absolutely zero concern that Wal-Mart will not continue to remain in business for a long time to come. A quick glance at some important fundamental financial metrics should clearly validate that belief.

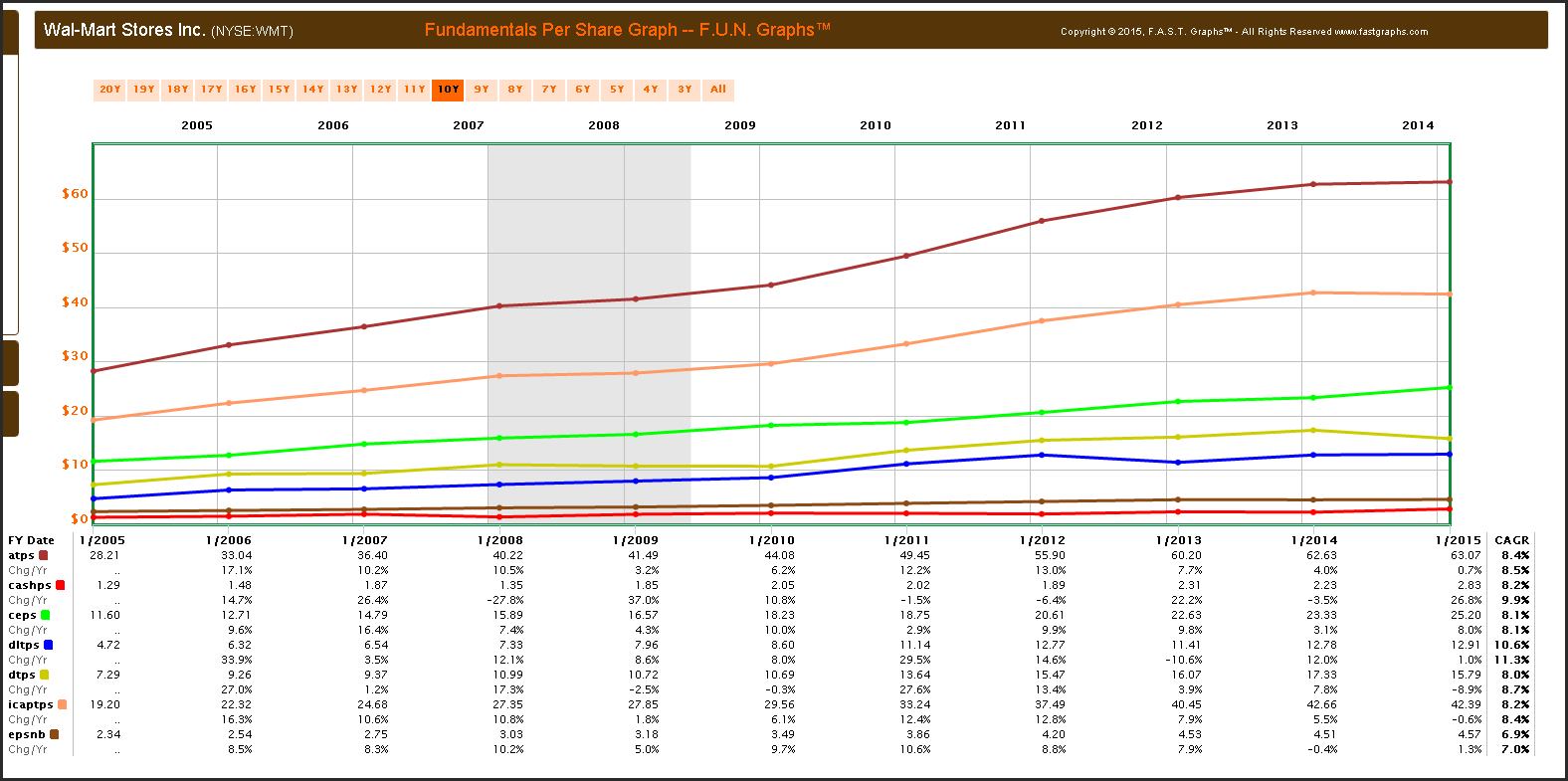

Wal-Mart’s Balance Sheet

Wal-Mart has a healthy balance sheet. A quick glance at Wal-Mart’s balance sheet shows improvement in almost every category. Assets per share are growing (atps), cash per share (cashps) is growing, common equity per share or book value is growing (ceps), long-term debt per share (dltps) and total debt per share (dtps) are growing but remain at reasonable levels, and invested capital per share (icaptps) is growing consistently in alignment with the other metrics.

Wal-Mart’s Income Statement

Although, as we will see later, Wal-Mart’s earnings per share have recently been in a downtrend, revenues per share (revps) continue to advance at a healthy but moderately slowing clip.

Wal-Mart’s Cash Flow Statement

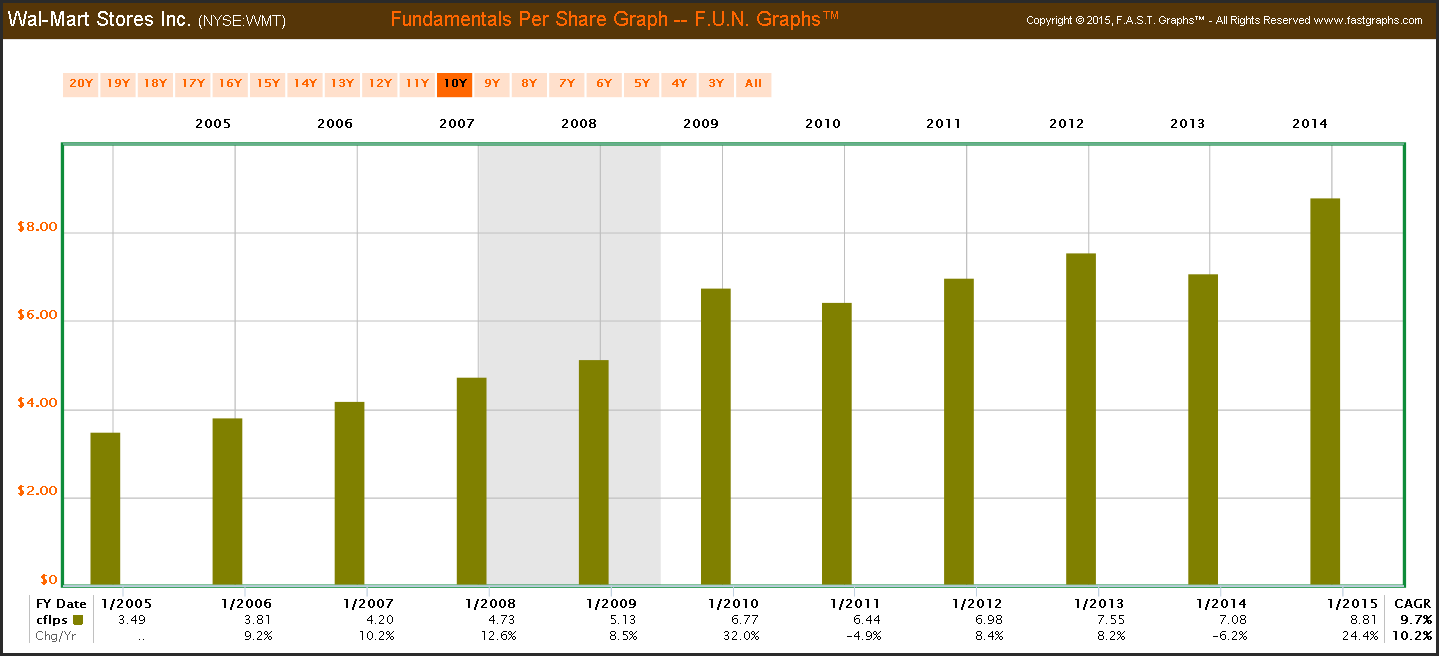

Wal-Mart’s annual cash flows continue to remain strong and healthy.

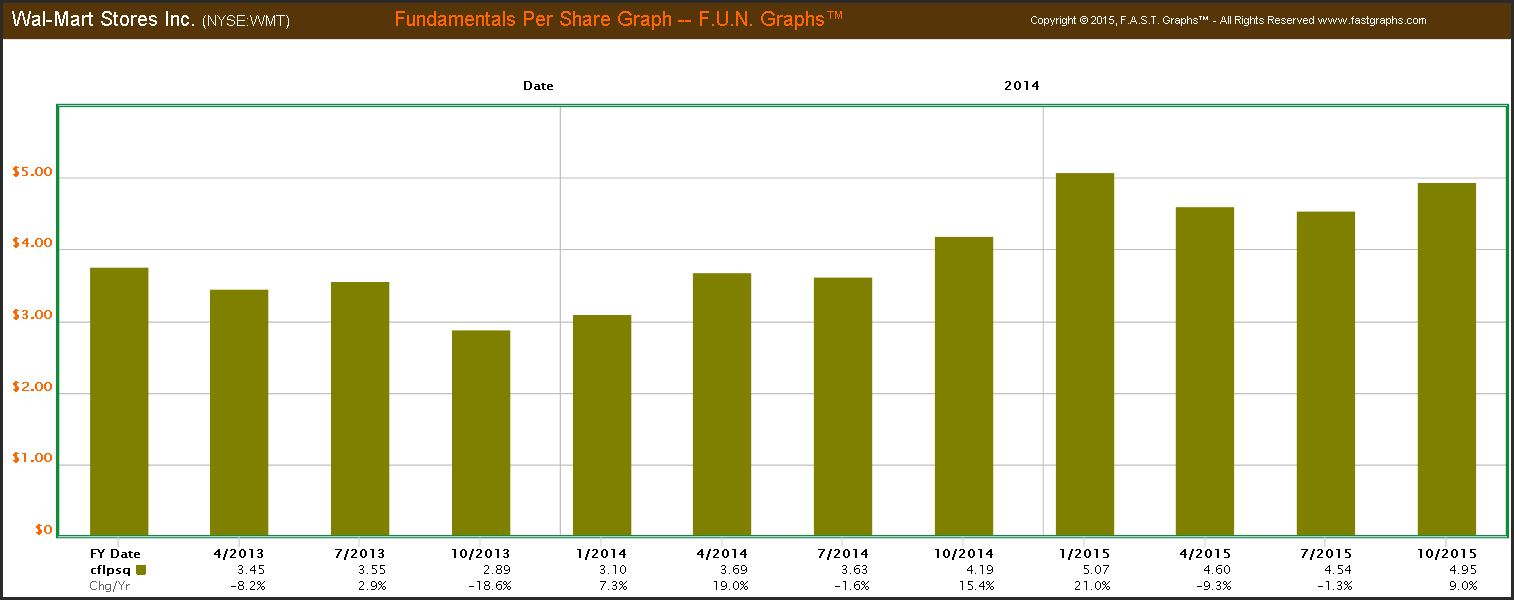

Wal-Mart’s cash flows per share on a quarterly basis (cflpsq), have improved in 2015 over 2014 and 2013.

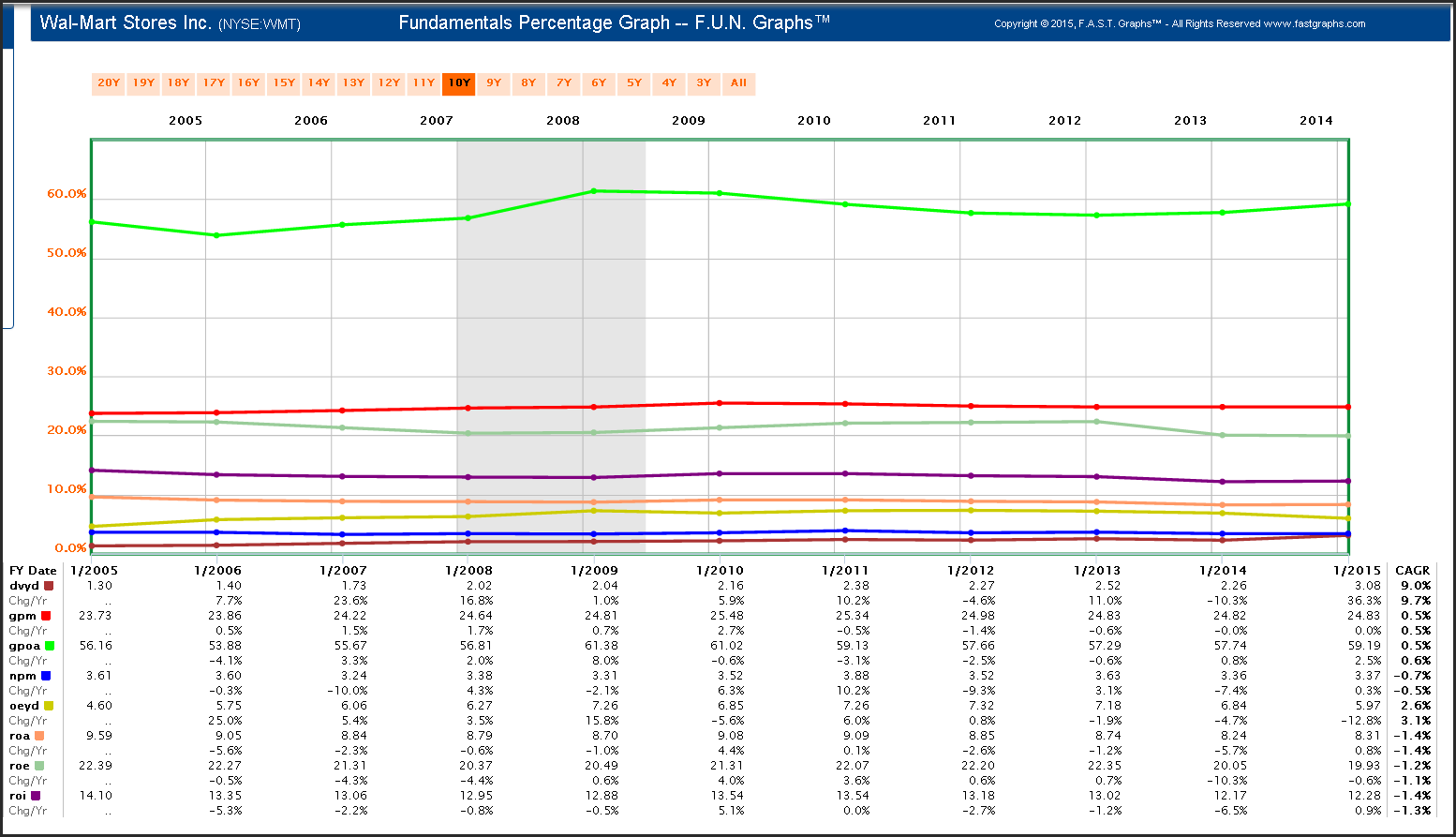

Wal-Mart’s Margins and Returns

I consider Wal-Mart a well-managed company as evidenced by the consistent generation of important metrics such as:

Dividend yield (dvyd), gross profit margin (gpm), gross profitability (gpoa), net profit margin (npm), operating earnings yield (oeyd), return on assets (roa), return on equity (roe) and return on invested capital (roi).

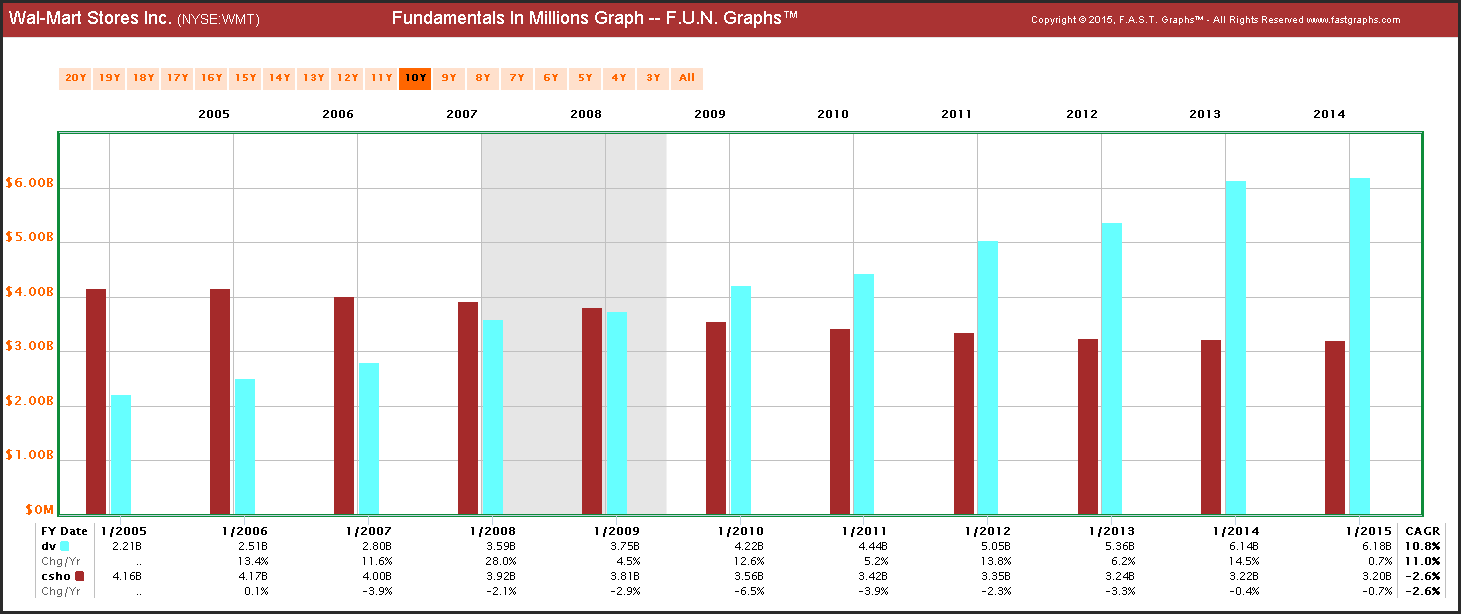

Wal-Mart’s Share Buybacks and Dividends

During this recent period when Wal-Mart’s stock price has been weak, they have been buying back shares (common shares outstanding (csho) and growing their dividends (dv).

Big Question Number 2: Will Wal-Mart grow or shrink?

Considering Wal-Mart’s enormous size, it would be a stretch to believe that the company would continue to grow at past historical rates. However, it would not be a stretch to believe that Wal-Mart will grow. The only question would be – how fast? Nevertheless, considering its quality and current valuation based on depressed earnings, just knowing that it can grow at all could be enough. The following excerpts from their most recent earnings transcript present management’s view of their future growth:

“Even if the percentage doesn't sound high because we have such a large denominator, not many companies grow by this amount in a quarter. I call this out because I don't want the currency impacts to obscure the strength of our business. We are a growth company and we're growing.”

This next excerpt provides some insight into why their earnings have been recently weak, emphasis added is mine:

“As we expected, operating income continued to be pressured by our decision to invest in our frontline associates. To improve the store experience for our customers and create a bridge to our future where digital capabilities will play an increasing role in our stores, we're making a $1.2 billion planned investment in our people this year that we understood would impact near-term operating income. This is by far the biggest driver of the decline in consolidated operating income.

Before going into the details, I want to take a step back to talk about our strategy. At our investor meeting last month, we shared more detail than usual about the next three years of our growth plan. We’ve never been a company that manages only for the short term, and that’s certainly true during this period of change. Although investments in our people and technology impact near term earnings, they will help us deliver sustainable growth and returns to shareholders over time.

We’re confident these are the right steps because we know where and how we’re going to win. We will be the first to deliver a seamless shopping experience at scale. No matter how you choose to shop with us - through your mobile device, online, in a store or a combination - it will be fast and easy. Online retailers are testing physical store experiences because they recognize the same customer desire that we do. There’s a race to do this right, but only Wal-Mart can bring together a dense network of stores, supported by a supply chain and systems like ours, with an emerging set of digital capabilities to win with customers.”

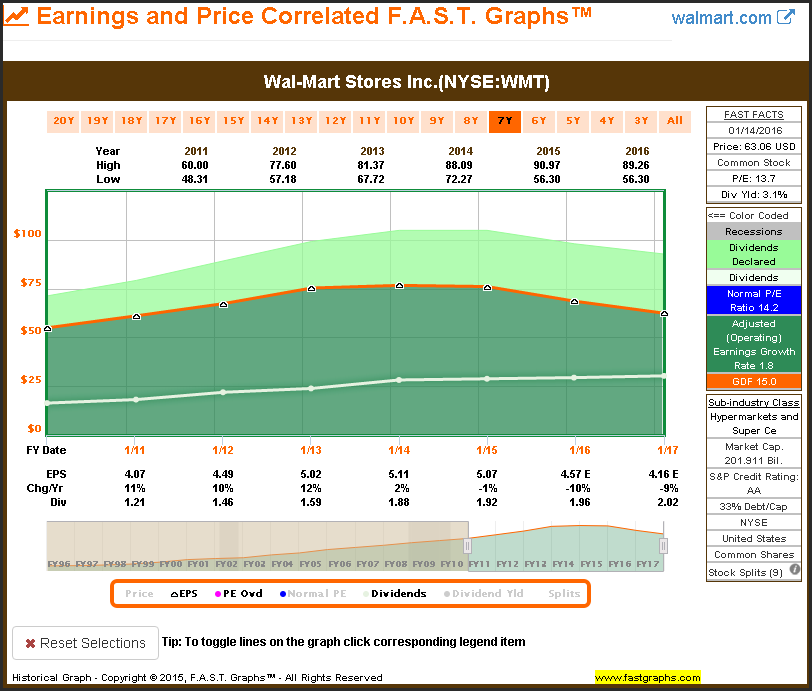

As previously stated, the second excerpt provides some color on management’s position regarding the justification and reasons why recent earnings have been weak, as depicted in the earnings and dividends only FAST Graph below.

“As we create this seamless experience, we’re positioning for growth in five key areas:

• First, we’ll continue to win on value. We’ve won on value in the past and that won’t change.

• Second, convenience is increasingly important as customers want to save both money and time.

• Third, we will always work to be great merchants - whether in stores or online.

• Fourth, we’re focused on the key geographies for customer growth, which are North America and China.

• Finally, we want to appeal to a blend of income levels. The way we’re approaching e-commerce, Neighborhood Markets, Sam's Club, grocery pickup, and other areas will appeal to value conscious customers of all demographics. We already serve customers from all income levels around the world but we have an opportunity to get even stronger.

By taking these steps, we will grow the company faster. We will add between $45 - 60 billion dollars of revenue to the company in the next three years. That’s a lot of growth; it just happens to be on a big base.”

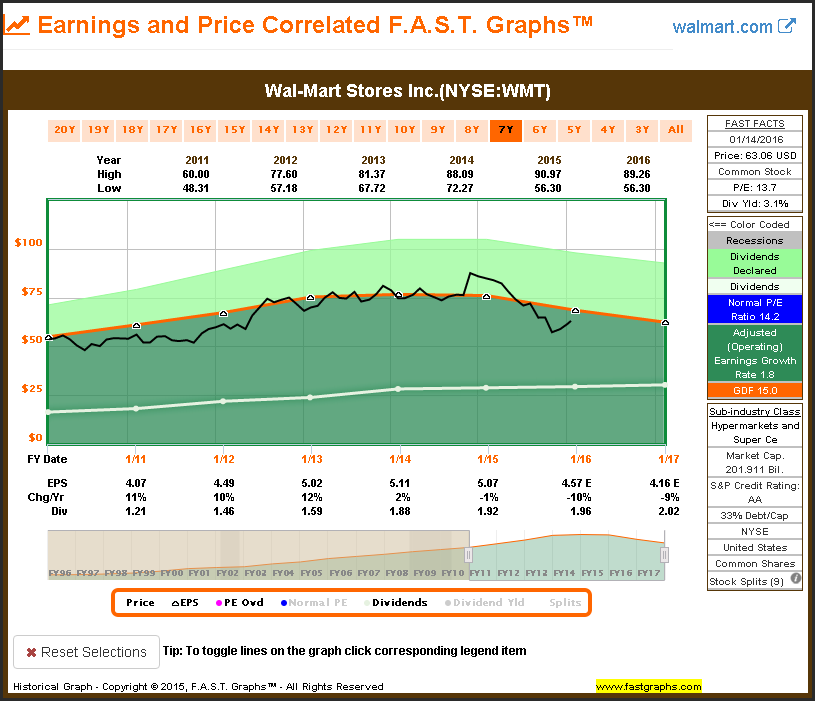

Moreover, when we add monthly closing stock prices to the above graph, we discover two important things. First of all, we see a high correlation to Wal-Mart’s stock price and its operating earnings per share. In this regard, the recent drop in stock price in 2015 is justified based on falling earnings. Additionally, since earnings are also expected to be weak in fiscal year 2017, it is possible that Wal-Mart’s stock price could drop farther over the short run.

However, since we’ve already indicated that Wal-Mart is virtually certain to continue to be an ongoing concern, it seems prudent to take a longer-term view and perspective. The following Growth “Infographic” taken directly from their website provides management’s perspective on future growth.

Wal-Mart is planning a $20 billion dollar share repurchase program over the next two years and estimates growth at between 3% - 4%. This may not be substantial, but if they are successful, it does perhaps answer the question that Wal-Mart will grow. The following outlines management’s position in more detail:

“Financial Outlook

The company also indicated that as a result of a stronger than anticipated impact from currency exchange rate fluctuations, it now expects net sales growth for the current fiscal year to be relatively flat. Excluding the impact of currency exchange fluctuations, net sales growth would be approximately 3 percent for fiscal year 2016. In February, the company indicated that it expected net sales growth of between 1 and 2 percent.

Charles Holley, Wal-Mart’s executive vice president and chief financial officer, outlined the company’s financial priorities for growth and detailed the investment and expansion plans for fiscal year 2017.

Our sales growth over the next three years is estimated to range between 3 to 4 percent annually, which will add approximately $45 to $60 billion in sales. Within the last year, we have experienced traffic and comp sales improvements in our Walmart U.S. business, and our plan reflects that positive momentum continuing,” said Holley.

McMillon said Walmart is bringing a disciplined approach to managing the company’s financial resources and portfolio. “We are actively reviewing our portfolio to ensure our assets are aligned with our strategy. But we will be thoughtful in our approach, recognizing our responsibility to drive shareholder value,” he said.

Holley also discussed the company’s profitability over the long-term and provided more insight into certain financial metrics.

“Fiscal year 2017 will represent our heaviest investment period. Operating income is expected to be impacted by approximately $1.5 billion from the second phase of our previously announced investments in wages and training as well as our commitment to further developing a seamless customer experience,” said Holley. “As a result of these investments, we expect earnings per share to decline between 6 and 12 percent in fiscal year 2017, however by fiscal year 2019 we would expect earnings per share to increase by approximately 5 to 10 percent compared to the prior year.”

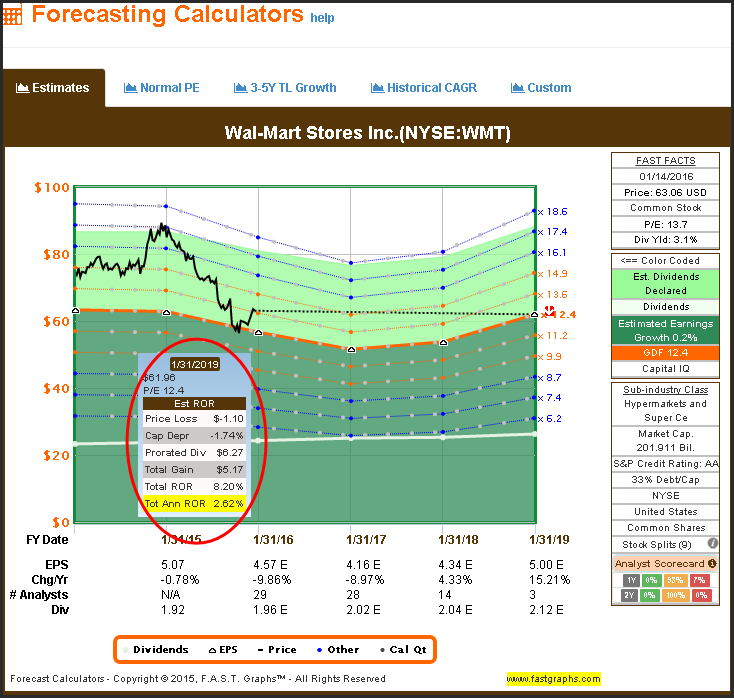

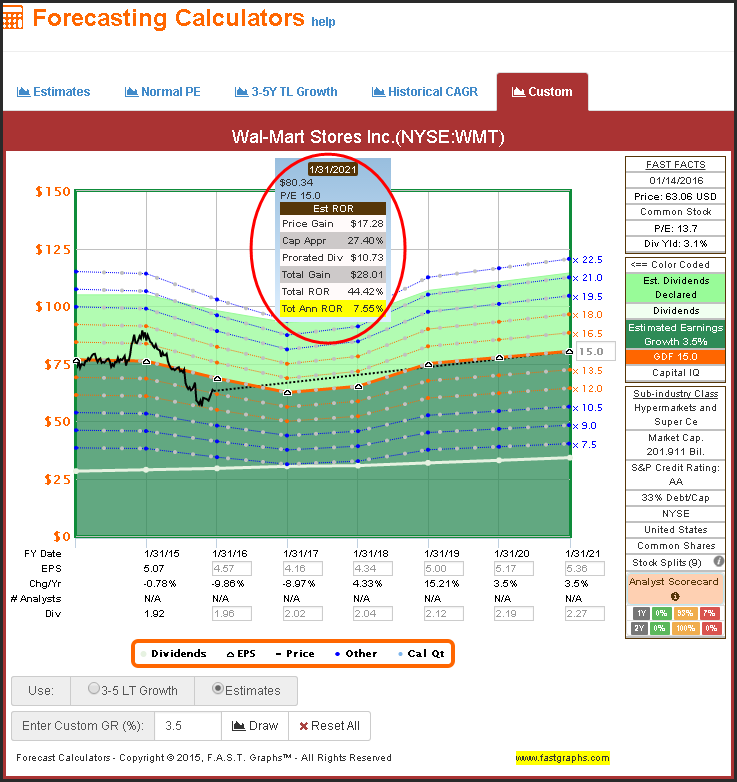

Consensus analyst estimates over the next couple of years indicate rather tepid growth for Wal-Mart. More importantly, although Wal-Mart’s current blended P/E ratio of 13.5 is below my 15 P/E ratio threshold, it should be noted that it is based on expected weak near-term earnings. Consequently, Wal-Mart investors should not expect significant capital appreciation over the next year or two. However, income-seeking investors might be attracted to its 3.2% current dividend yield and its AA credit rating. In other words, as I will discuss when answering the third big question, Wal-Mart is attractive today for safety and yield, not high short-term returns.

Longer-term, assuming management’s forecasts are reasonably accurate, Wal-Mart does appear to offer the potential for a reasonable total return of close to 8% per annum. I have used the mid-point growth rate of 3.5% (between management’s guidance of 3% - 4%) to run these calculations.

Big Question Number 3: What are you investing in Wal-Mart for?

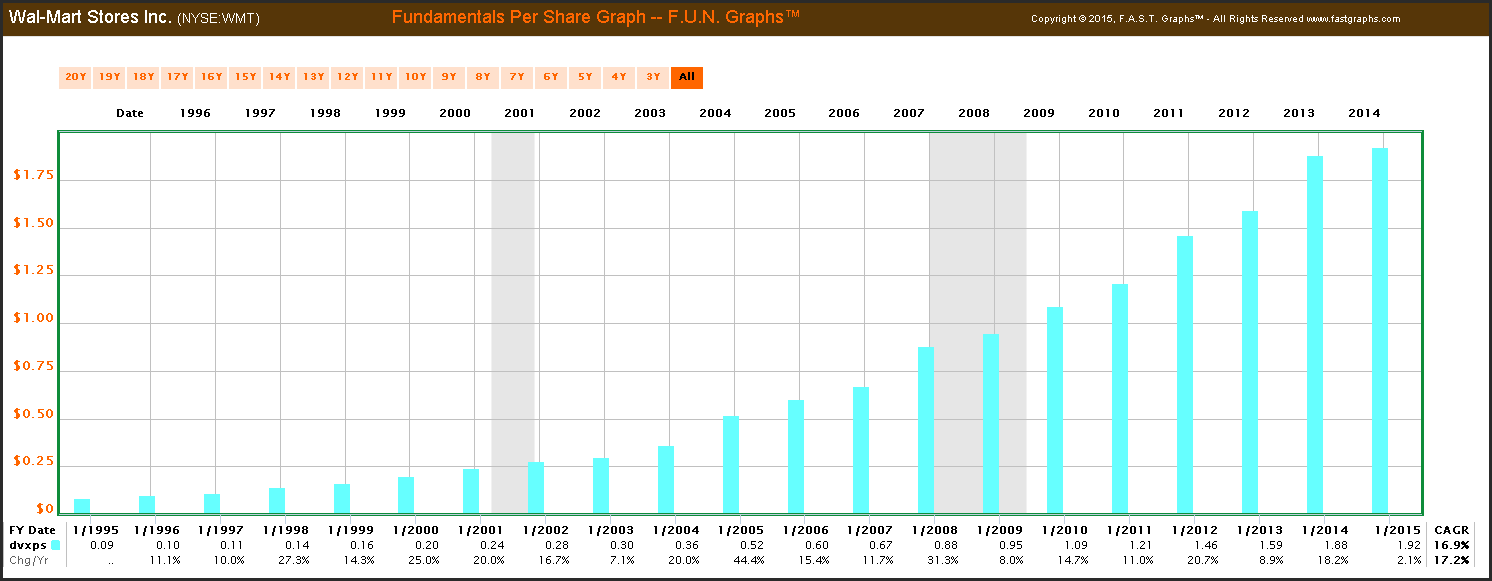

From what I’ve described above regarding Wal-Mart’s growth potential, it is certainly not the most exciting total return stock available. However, considering its high yield, impeccable quality and reasonable valuation based on depressed earnings, it might appeal to income-seeking investors concerned with safety and quality. The following illustrates Wal-Mart’s consistent dividend growth since 1996:

Over the long run, Wal-Mart has outperformed the S&P 500 on both a total cumulative dividend income and annual capital appreciation basis. However, future capital appreciation and dividend growth may not duplicate the past. Nevertheless, Wal-Mart appears to be a sound and high-yielding long-term investment.

Summary and Conclusions

Whether most common stock investors will admit it or not, investing in stocks carries a deep-rooted primal fear of losing all of your money. Therefore, during a bad market many people will project a bear market to the extreme of total loss. Although this does happen on occasion, it is very rare to see a stock drop 100% or go out of business. This is especially true when you are invested in blue-chip dividend paying stocks. Consequently, focusing on the big question of whether you believe your company will continue as a going concern can be enough to alleviate the extreme fear of total loss. Once you come to grips with the likely reality that your company will most likely outlive you, it becomes easier to fight those panicky feelings.

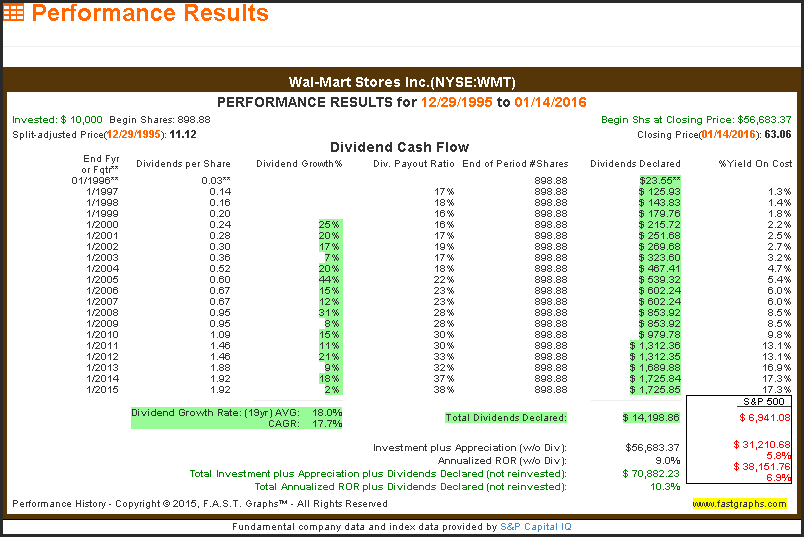

Whether we like it or not, the undeniable reality of investing in the stock market is that there will always be bear and bull markets. But most importantly, each bear market inevitably ends by turning into a bull market, and vice versa. If we learned anything from our last “Great Recession” it should be that. Although it may be hard for many people to wrap their heads around this, our last recession created one of the best investment opportunities in modern times. And equally as important, all of the Dividend Champions and Aristocrats raised their dividends prior to, during and after the Great Recession - Wal-Mart included. If you were investing for income, and knew what you were investing for, it was quite calming to realize you were receiving a raise in pay each year. Those that did, were able to K.I.S.S. their worries away.

Disclosure: Long WMT.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.