IN THIS ISSUE:

1. December Jobs Report Was Stronger Than Expected

2. Yet Some Bad News in the Very Good Jobs Report

3. US Stocks Plunge the Most on Record Last Week

4. China’s Massive $4 Trillion in Reserves is Dropping Fast

5. Crude Oil Price Hits 12-Year Low, Down 10% Last Week

Overview

In the first week of 2016, US stocks plunged by more than in any other first week of January since records have been kept (before 1900). The Dow Jones Industrial Index fell over 1,000 points from 17,591 at the close on December 31 to 16,519 at the close last Friday – a loss of over 6% in one week.

The S&P 500 Index shed over 100 points from 2043.7 at the close on December 31 to 1922.0 at the close last Friday – a loss of 6.0% in one week. The Nasdaq Composite lost 7.3% during the worst first week of January on record.

Most global stock markets were hit with similar losses or even worse in some cases. Investors around the world were stunned and are wondering what happened in the worst New Year’s week in history for share prices – and worry if more pain is to follow.

The financial media maintained that the carnage was caused primarily due to new economic data out of China, which was worse than expected. I will get into that as we go along today, but the rout was due to more than just disappointing Chinese data.

The collapse in crude oil prices since mid-2014 is also becoming a serious global concern for reasons I will outline below. The price of West Texas Intermediate Crude has collapsed over 70% since mid-2014 from near $105 per barrel to below $33 a barrel as of last Friday’s close. It fell 10% last week alone and is down so far this week.

While sharply lower gasoline and energy prices are a boon to consumers, there are now serious concerns about sovereign debt defaults in numerous oil producing countries. In addition, there are growing fears of global deflation as a result of collapsing oil and other commodity prices. I will tell you why below.

Yet before we get into the complicated issues raised above, let’s take a few moments to discuss last Friday’s stronger than expected unemployment report for December.

December Jobs Report Was Stronger Than Expected

The Bureau of Labor Statistics (BLS) released a significantly stronger than anticipated December jobs report Friday, making the final month of 2015 easily among the top three of the year in terms of jobs added.

Employment data out Friday showed employers in the United States added 292,000 net new jobs last month. Economists had been expecting only 211,000 payroll additions in December. The headline unemployment rate held steady at 5.0% for the third month in a row.

The BLS also revised payroll counts from October and November up by over 50,000 new jobs combined. November new jobs were revised up from 211,000 to 252,000 and October was revised up from 298,000 to 307,000. It was a great report on the surface, but let’s not forget that the December report always includes a large seasonal adjustment by the BLS.

Yet Some Bad News in the Very Good Jobs Report

For all of 2015, the nation added 2.65 million jobs. That sounds good, right? Not really. When measured against a year ago, last week’s jobs report doesn’t look nearly as good. In fact, job growth slowed in 2015, the first annual dip in new jobs since the Great Recession. As you can see in the chart below, for all of 2015 employers added 466,000 fewer jobs than in 2014, when employment increased by 3.1 million.

So, is the American economy slowing, or is the slowing job growth simply an indication that the job market has recovered and adding more jobs is getting tougher? After all, the unemployment rate hit 5% in October, down from 10% in late 2009, and it has stayed at that level ever since.

Eventually, job gains will slow down even if the economy is still healthy. Put another way, is the economy nearing full employment or are job gains once again falling short? To answer that question, you can compare the job gains of the current economic recovery to other recoveries.

Since the end of 2009, employment has increased by 13.6 million jobs. In the six years following the early 1980s recession, the number of new jobs rose by 18.1 million. The 1990s recovery saw a slower increase of 16.2 million jobs in the same period. Yet it was still a larger overall gain in new jobs than what we are currently experiencing.

The bottom line is: In 2015 the economy created fewer jobs than in 2014, the first yearly drop since the Great Recession. We should keep last Friday’s impressive jobs report in the context of an economy that is only growing at about 2% a year, which is still well below expectations.

Let’s now move on to our main topic today where the news is not nearly so good – what’s happening in the markets. I hope to be able to add some clarity to what was the most stunning start to a New Year on record.

US Stocks Plunge the Most on Record Last Week

As noted in the Overview above, the Dow plunged 6.1%, the S&P 500 6.0% and the Nasdaq 7.3% all in one week, making last week’s decline the worst on record for the start of a year. The catalyst once again was China. Adding to the China fears was the precipitous decline in crude oil which lost 10% in the first week of the New Year.

Let’s start with China. Before our markets opened on Monday, January 4 there was disappointing economic news out of China, and stocks tumbled worldwide. Then on Wednesday, January 6 we learned that China’s manufacturing index had dropped to a 17-month low. And on Thursday, the Chinese central bank devalued the yuan for the third time in less than a year.

And the news out of China only got worse as last week unfolded. Chinese stocks plunged over 10% last week, forcing authorities to suspend trading in its equity markets based on “circuit breakers” put in place at the end of last year.

But it quickly became apparent that the circuit breakers only made the panic worse, causing even more selling as Chinese investors worried that they could be locked into positions if trading was halted due to large losses.

On Thursday before the stock market opened, China’s central bank devalued the yuan (also known as the renminbi) to 6.5646 to the US dollar, its lowest point in almost six years. When stock trading started, investors dumped shares and the market was down 7% in less than a half-hour, at which point the circuit breakers again shut down the market.

Later that same day, Chinese authorities decided to abandon the circuit breakers starting on Friday, but the severe damage to share prices was already done. Fortunately, the Shanghai Composite Index (SCI) closed up almost 2% on Friday.

Equity markets around the world plummeted in lock-step with the decline in China’s stock markets last week. For most stock markets around the world, it was the worst New Year’s week in history. While the SCI fell another 5.3% on Monday, US stocks managed to post a modest gain. Today’s trading was mixed with a rally near the close. Yet volatility is likely to remain high in the weeks just ahead.

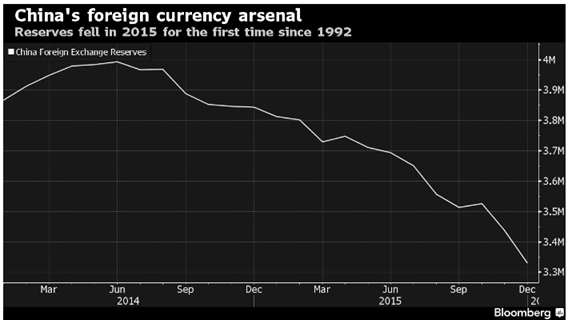

China’s Massive $4 Trillion in Reserves is Dropping Fast

At mid-2014, China’s vast holdings of foreign currency reserves (mostly US dollars) was estimated to be nearly $4 trillion, the largest such stockpile in the world. To many that seemed to be a gold-plated insurance policy against the country’s current market chaos, with a depreciating currency and a torrent of capital leaving the country.

The problem is the alarming “burn rate” of dollars at the People’s Bank of China. The nation’s stockpile of foreign exchange reserves plunged by $513 billion, or 13.4%, in 2015 to $3.33 trillion as the nation’s central bank coped with a weakening yuan and an estimated $843 billion in capital that left China between February and November of last year, the most recent tally available according to Bloomberg.

It is widely believed that trillions of dollars in reserves held by the Peoples Bank of China (PBOC) are invested in safe liquid securities, including Treasury bills and bonds. However, the US Treasury reported late last year that China’s direct holdings of Treasuries stood at only $1.25 trillion – although it cautioned that the figure may not reflect the true ownership of US securities, as some may be held in custodial accounts in other countries.

In China, like some other countries, the exact composition of its foreign exchange reserves is a state secret. But analysts worry the currency armory may not be as strong as it looks. That’s because some of the investments may not be liquid or easy to sell. Others may have suffered losses that haven’t been accounted for.

In addition, some Chinese reserves may have already been committed to fund pet government projects like the Silk Road Fund to build roads, ports and railroads across Asia or tens of billions in government-backed loans to countries such as Venezuela, much of which is repaid through oil shipments.

Then there are other liabilities that China needs to cover, such as the nation’s foreign currency debt to finance and manage imports denominated in overseas currencies. When those factors are taken into account, some $2.8 trillion in reserves may already be spoken for just to cover its liabilities, according to Hao Hong, chief China strategist at Bocom International Holdings Co.

This is yet another reason why the whole world is watching and worrying about China.

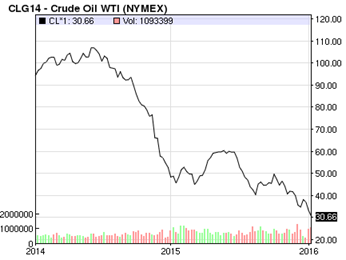

Crude Oil Price Hits 12-Year Low, Down 10% Last Week

US West Texas Intermediate (WTI) closed at $33.16 a barrel on Friday, down about 10% for the week. Brent crude closed Friday at $33.51 a barrel. It hit a trading session low of $32.16 on Thursday, the lowest since April 2004. Oil prices are plunging due to global oversupply and weak demand. Prices continued to plunge this week to below $31 a barrel for WTI.

Over the past year, the world has been producing more oil than it consumes by an average of 1.5 million barrels per day, according to the International Energy Agency. In the second half of last year, global daily production of crude topped 97 million barrels a day, versus daily demand of only about 95.5 million barrels, so there is literally a glut of oil on the market.

With the economic slowdown in China and elsewhere, OPEC and the International Energy Agency expect global oil demand to fall in 2016 – despite the lowest price in 12 years.

Normally, cheap oil prices are good for consumers, leaving them with more to spend on other goods and services. Yet with oil prices well below $35 per barrel, there are growing concerns about sovereign debt defaults in numerous oil producing countries – some even fear that Russia could be at risk if prices continue to fall.

So we’re at the point where falling oil prices are actually hurting the equity markets due to these growing concerns. With talk of $20 crude prices becoming more common, investors around the world are worried about sovereign debt defaults and widespread bankruptcies in the energy sector in 2016.

Finally, the plunge in energy prices, along with many other commodity prices, is increasing concerns about global deflation. Clearly, China is experiencing deflation as well as a host of other countries. This bears watching closely just ahead.

In conclusion, the wild markets we saw last week are likely to continue in the weeks and maybe months to come. For those who took my advice back in March and April of last year to cut your long-only equity exposure by at least 50%, I would remain in this defensive position for now. There may be an opportunity to reload just ahead.

Wishing you profits in the New Year,

Gary D. Halbert

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent. |