Considering the historically bad start to the year, it is worth asking whether US stocks are in a consolidation mode or are about to break down significantly? To help get us closer to an answer we wanted to run through a variety of our market internal charts.

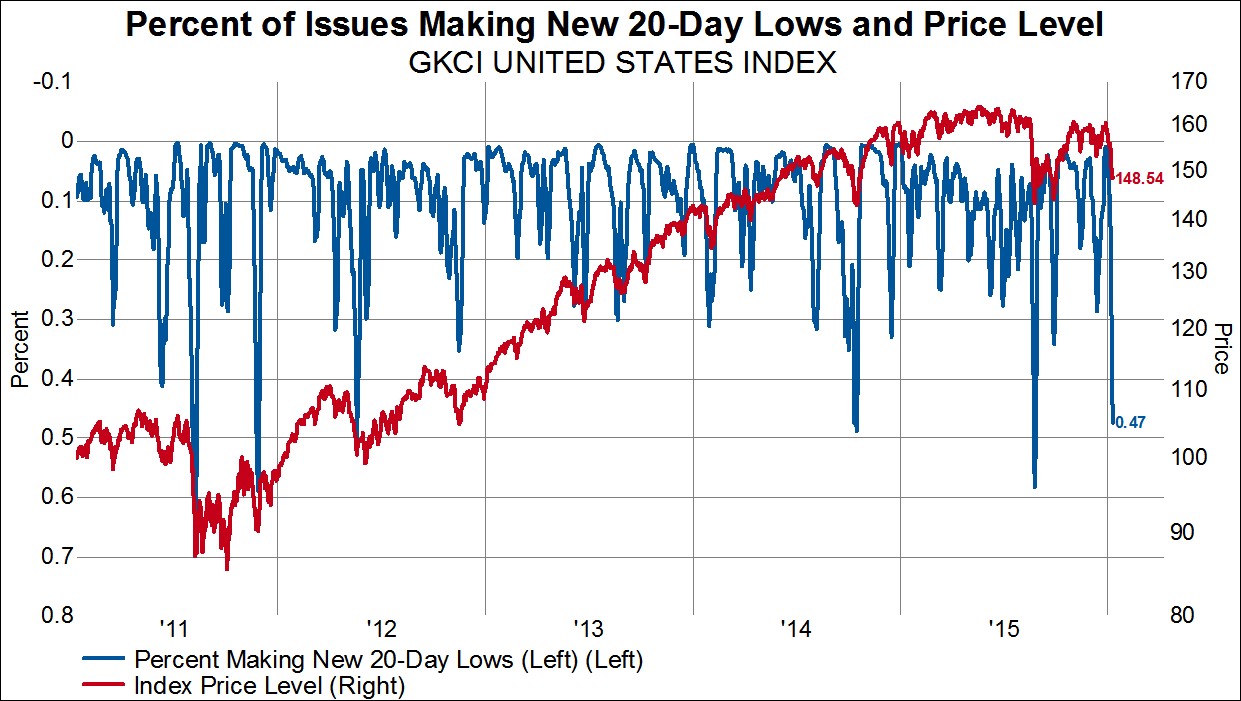

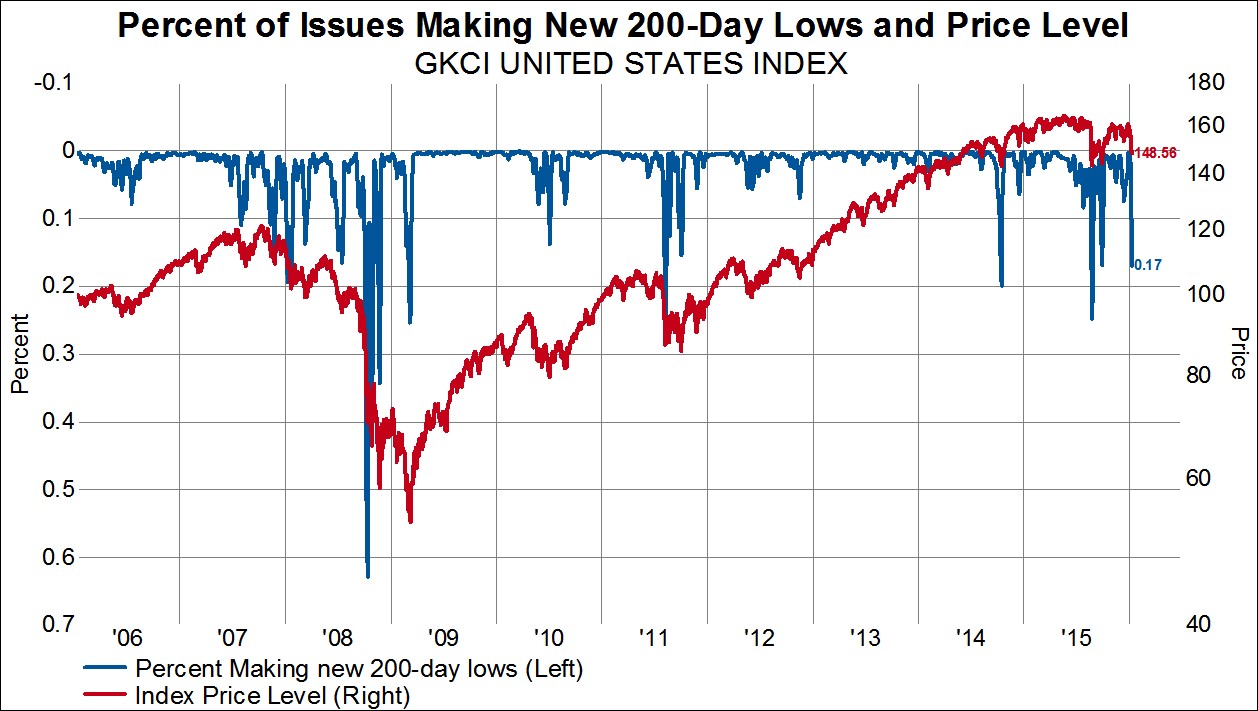

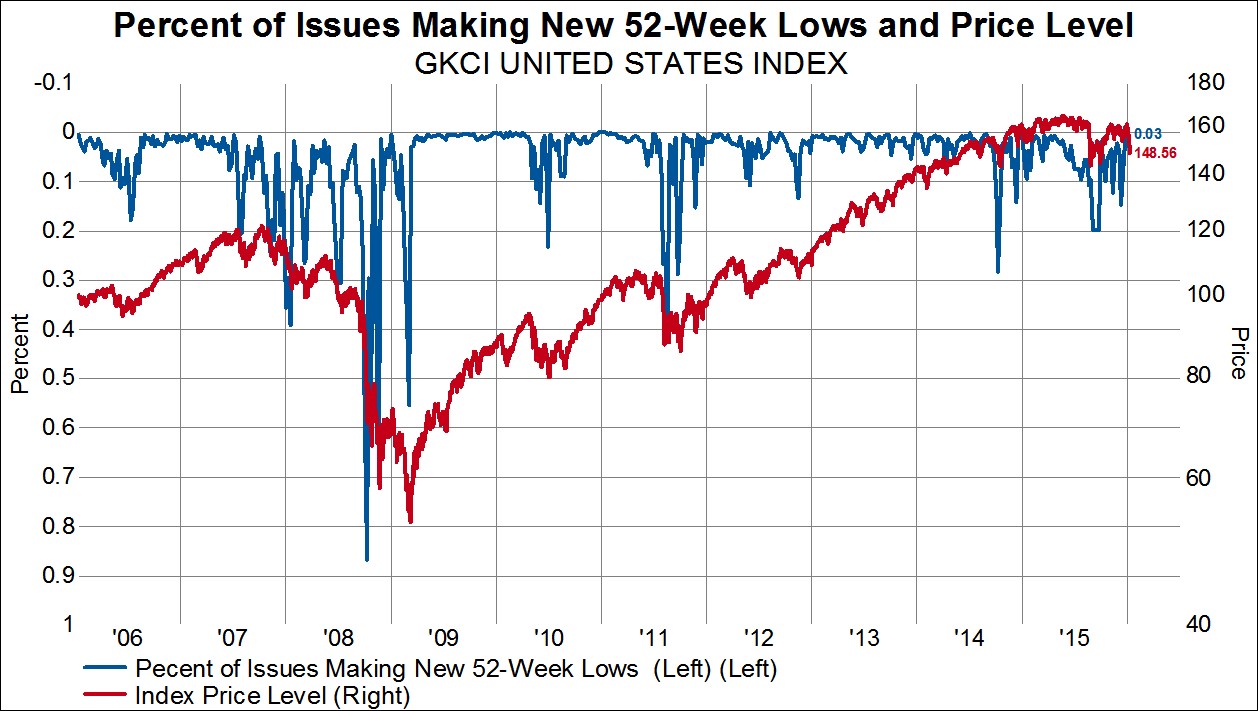

There has recently been a spike in the percentage of stocks making new lows across a variety of time frames. On a short-term basis (20 days), we are in the midst of a 20-day washout that we have only seen four other times since 2011. On a longer-term basis (200 day), the current percentage of stocks suggests that we are in the midst of a re-test of last September’s low. In fact, only 3% of our GKCI United States Index is currently making new 52-week lows. Considering how many stocks are making new 20-day lows and the current level of longer-term charts, this metric would suggest that at the very least the US market is due for a positive price bounce.

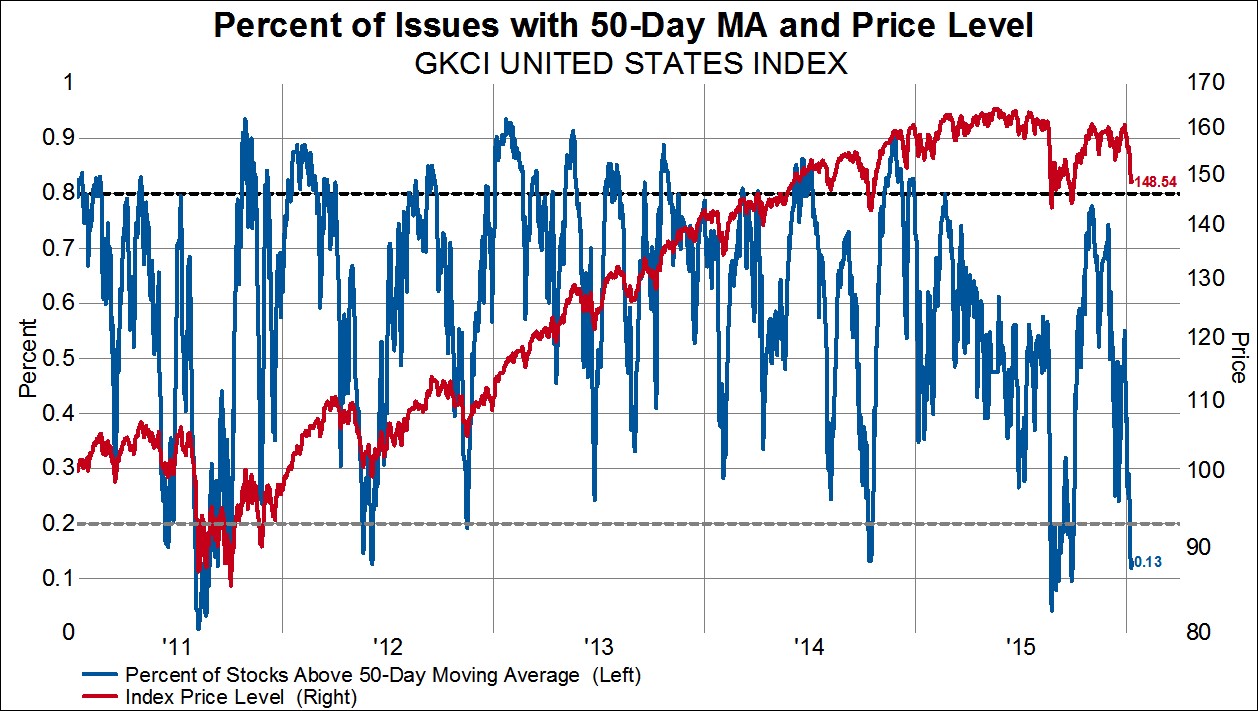

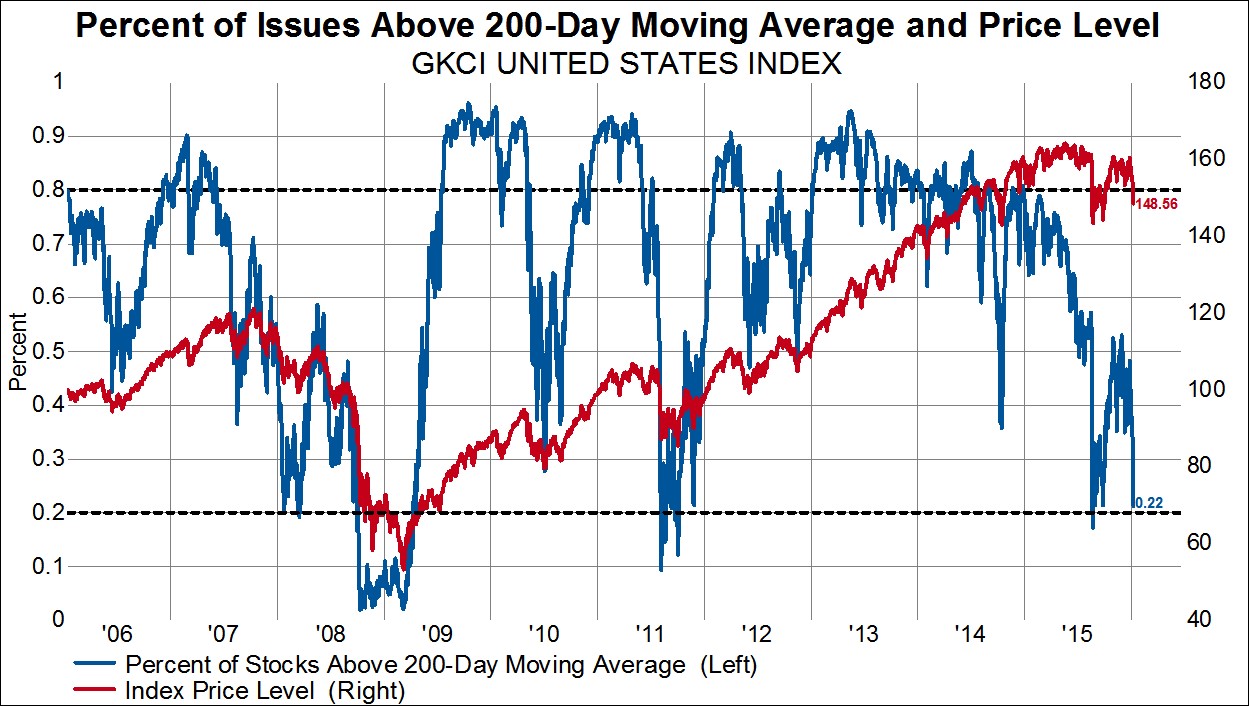

US stocks have moved into oversold territory across pretty much every time frame if one looks at the percentage of stocks trading above its price moving average. Only 13% of US stocks are trading above its 50-day moving average while 22% of stocks are trading above its 200-day moving average. During the September low, the percentage of stocks trading above its 50-day moving average got as low as 4% and the percentage of stocks trading above its 200-day moving average hit 17%. During 2011, the latter metric hit 9%. Looking at this blunt measure of momentum it would seem that there may be a bit more downside to US equity prices, however, momentum is already very negative.

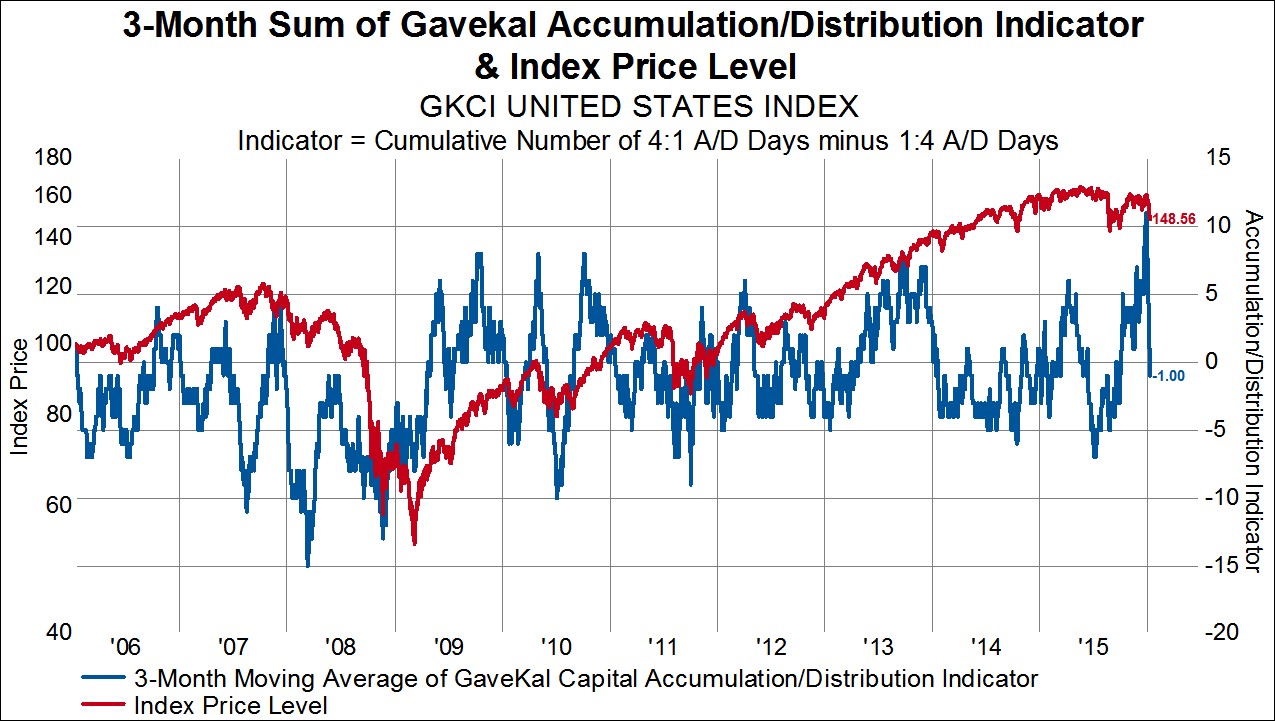

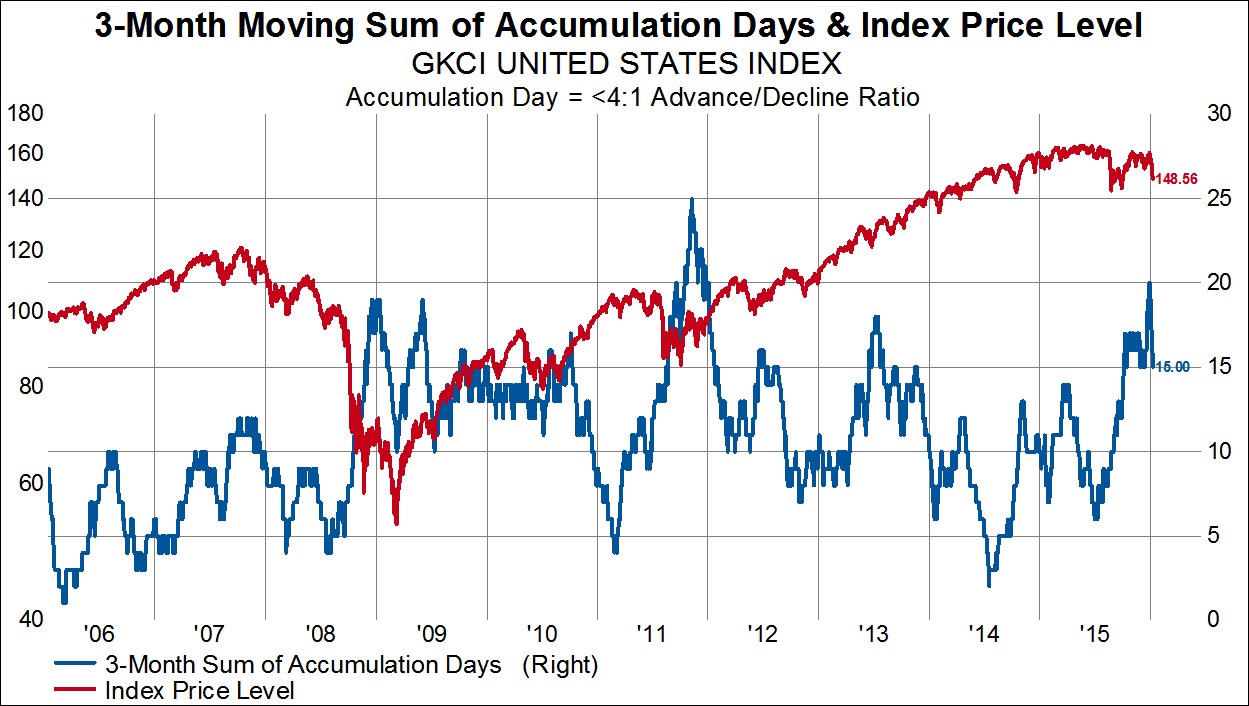

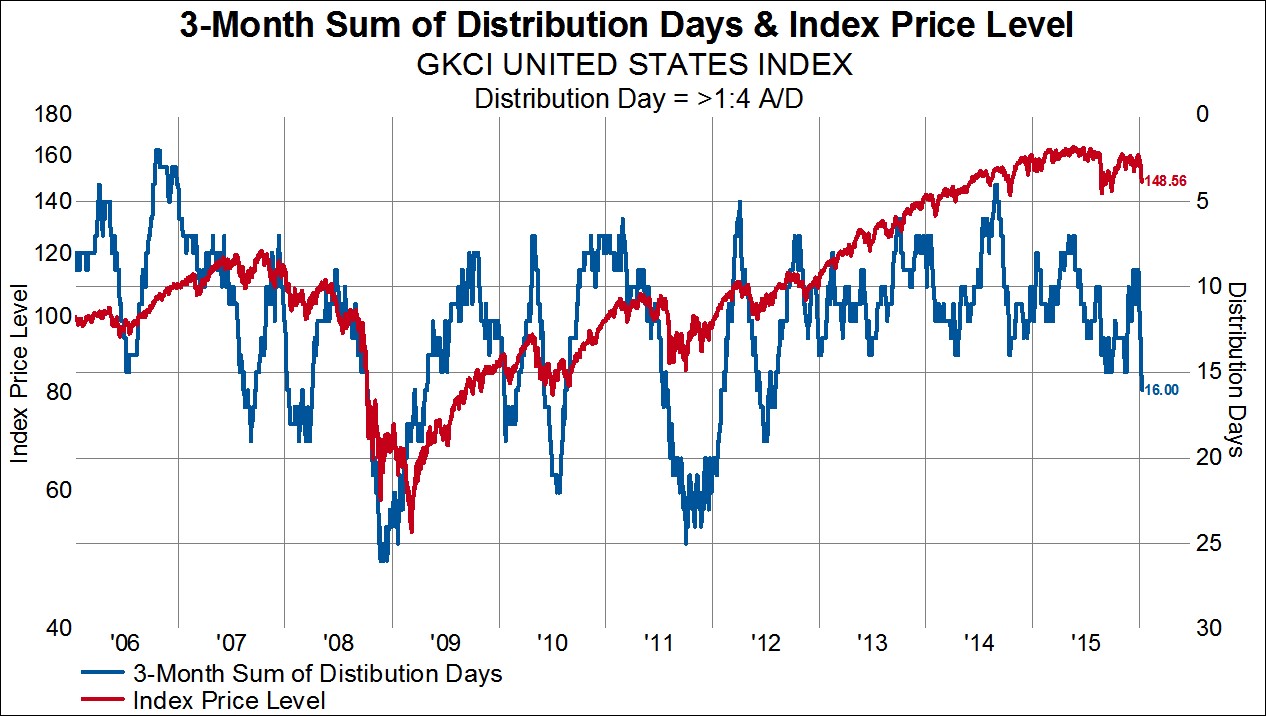

The Gavekal Capital Accumulation/Distribution Indicator currently sits at -1 after actually making an all-time high at the end of the year. An accumulation day is any day where the number of advancing stocks outnumber the number of declining stocks by at least 4 to 1. A distribution day is when the number of declining stocks outnumber the number of advancing stocks by at least 4 to 1. We net out accumulation days against distribution days and then take the three-month moving average of that series. We had a strong number of accumulation days off the September low as the three month sum moved from 9 to 20 days. However, we have had a recent spike in the number of distribution days since the end of last year as the number of distribution days moved from 8 to 16. The current level is the most distribution days we have had over a three month period since 2012. We may have a few more distribution days ahead of us, however, we wouldn’t expect too many. The net indicator tends to hang out in a range from -5 to 5 so the current -1 is right in the middle of the usual range.

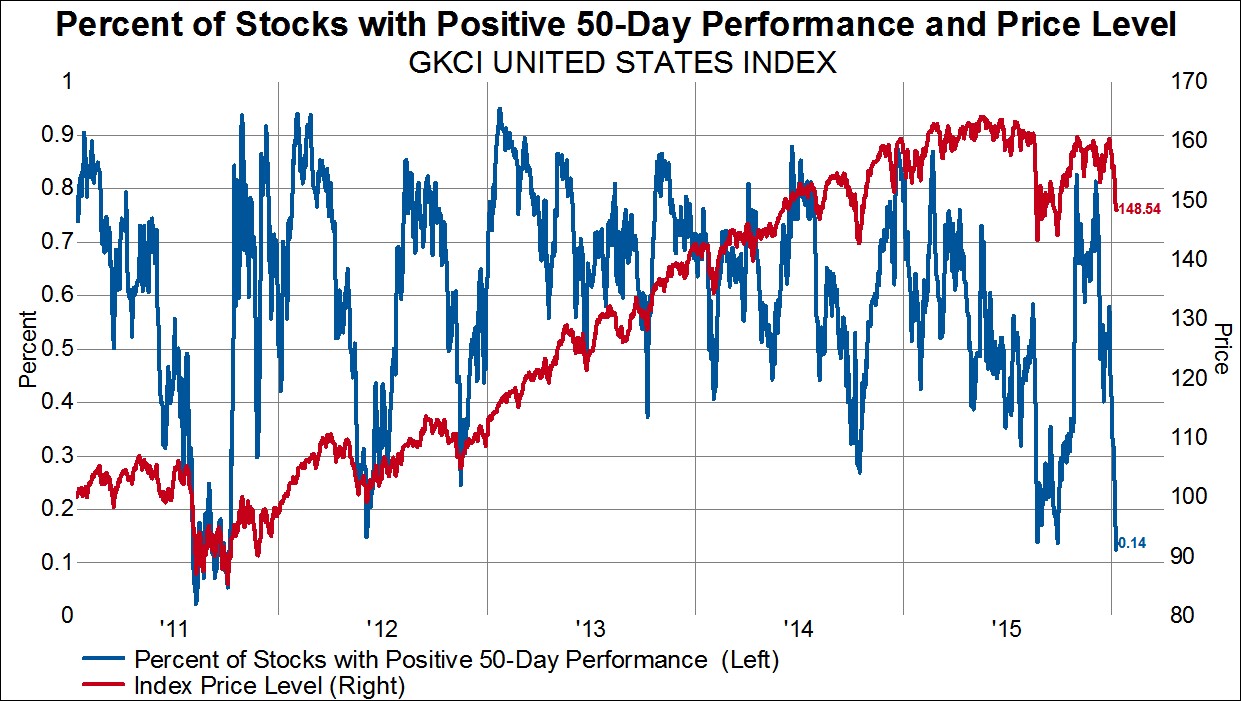

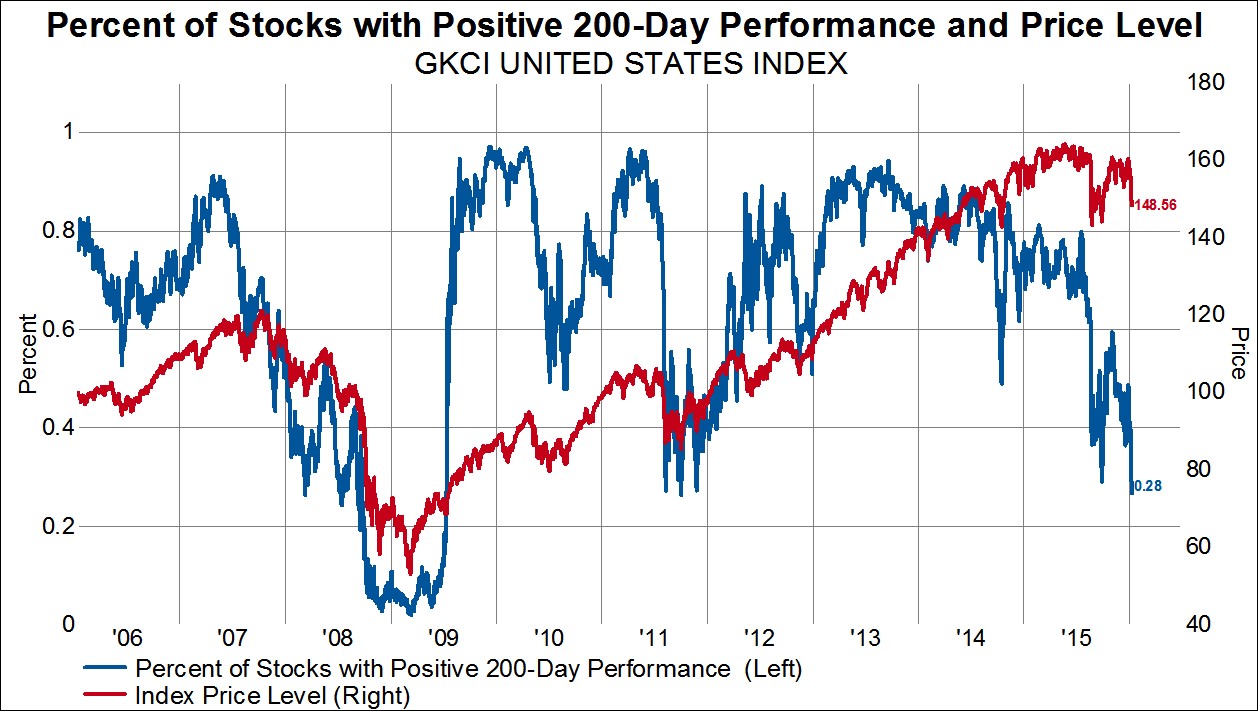

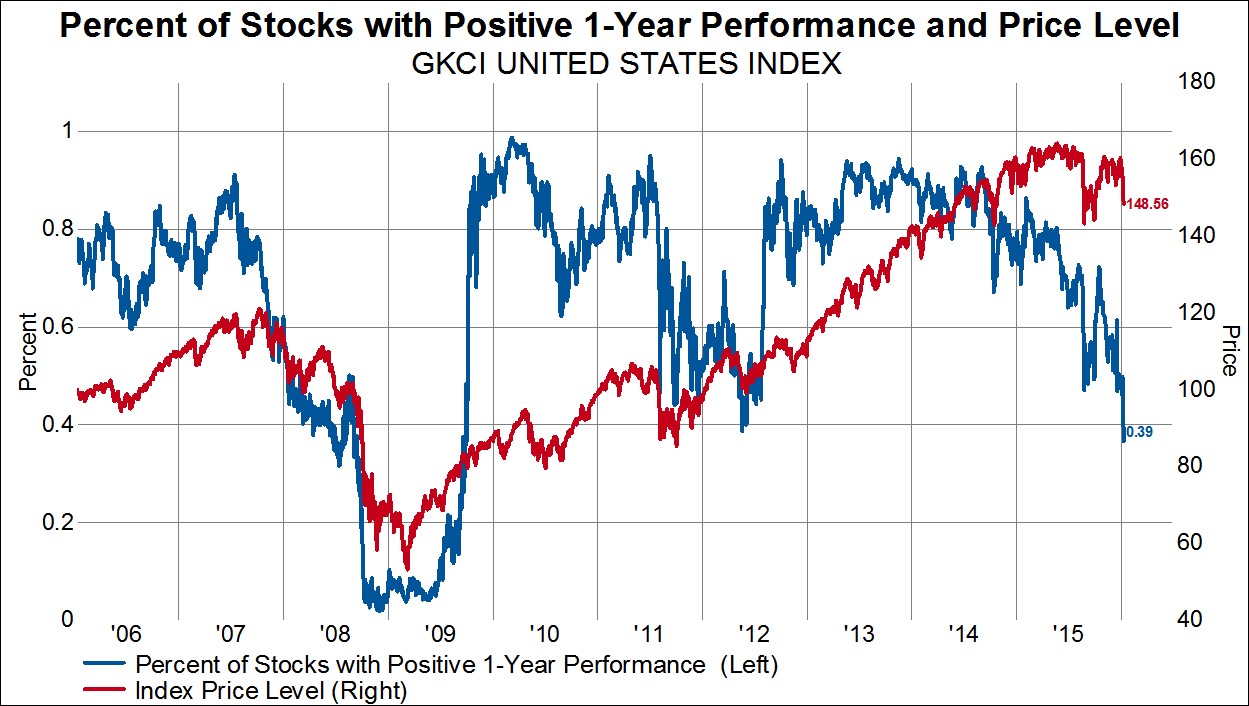

Finally, the percentage of stocks that currently have positive price performance over the last 50-days, 200-days and 1-year, suggest that stocks are once again oversold and probably due for a bounce. The percentage of stocks that have positive 50-day performance is just 14%. This level is commensurate with levels hit in September and is just slightly higher than what we saw in 2011. Only 28% of stocks have positive performance over the past 200-days, which is lower than what we saw in September and is equal to levels we hit in 2011. Lastly, 39% of stocks have had positive performance over the past year. This is actually the fewest number of stocks with positive performance over the prior year since 2009.

Overall, looking at the internals of the US stock market suggests that the US market is very oversold in the short-term and a bounce should most likely be on the near-term horizon. Most indicators are near September 2015 lows and just above 2011 levels. We are still far from 2008-2009. Unless fear dramatically increases in the market for some currently unknown reason to the degree that the market was scared during the financial crisis, we wouldn’t expect a waterfall type decline in US equity prices and would consider the current period of weakness as an ongoing consolation in the equity market.