It was an important week for U.S. economic figures, but the data releases were overshadowed by market developments in China. The country’s new circuit breakers, which were meant to reduce market volatility, were a disaster, and were jettisoned after the Shanghai market was shut down completely in two of four trading sessions. The hope is that the Chinese authorities will stabilize the situation. However, currency management should be more of a challenge and poses the greater risk.

The Fed policy meeting minutes from December showed that officials viewed the risks to growth and inflation as “balanced.” However, many officials noted lingering concerns, including the impact of a strong dollar and the prospects for China. While the mid-December dot plot (the individual Fed officials’ forecasts of the appropriate level of the federal funds target rate) were more tightly bunched for the end of this year, there was still some disagreement (of the 17 meeting participants, seven expected four rate hikes, three saw three rate hikes, and four were looking for only two). That range reflected differing views on the amount of slack in the job market and the prospects for inflation returning to the Fed’s 2% goal. Not much new, but the minutes reinforced the idea that future policy moves will be dependent on the data (especially the labor market figures).

A lot of the recent economic data have been soft in recent weeks, consistent with a more modest pace of GDP growth in 4Q15 (advance estimate to be reported on January 29). At the same time, expectations of most senior Fed officials, including Vice Chair Stanley Fischer, have not strayed from the mid-December outlook – that is, that three or four 25-basis point rate increases are likely to be warranted in 2016.

Nonfarm payrolls rose more than expected in December, with an upward revision to the two previous months. Note that seasonal adjustment can be tricky and strength may have been exaggerated by the seasonal adjustment. For example, construction jobs fell 151,000 before adjustment and rose by 45,000 after adjustment. Seasonal adjustment won’t get any easier in January, as we can expect to lose about 2.8 million jobs (again, before seasonal adjustment) due to the end of the holiday shopping season. Still, the broad range of labor market data suggests that the economic recovery remains on track.

Normally, the Employment Report would be the main focus for the week. However, developments in China took center stage. The Chinese trading authority implemented new circuit breakers. These were meant to prevent excessive market volatility. Instead, they added volatility. With the Shanghai Composite Index down 5%, the market would shut down for 15 minutes. Upon reopening, if the market was down 7%, the exchange would be shut down for the rest of the day. The two circuit breakers were triggered on Monday, dampening the global stock market mood. In a more dramatic development, both triggers were hit in the first half hour of trading on Thursday. The Chinese trading authority jettisoned the circuit breakers and the market appeared to stabilize on Friday.

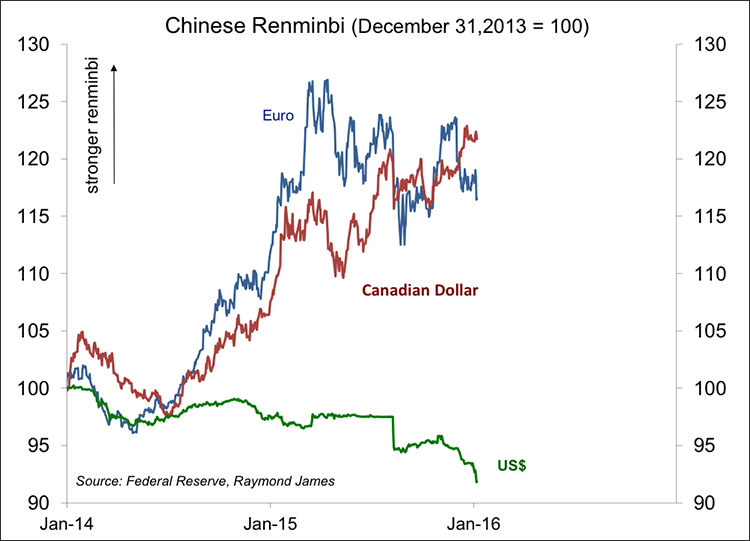

Since the end of 2013, and until about a month ago, the yuan was down only about 5% against the U.S. dollar. The dollar has appreciated a lot more against most other currencies. In turn, the yuan’s close tie to the dollar means that the Chinese currency has appreciated a lot against most other currencies. There is considerable pressure for the yuan to weaken. The People’s Bank of China has used some of its currency reserves to support the yuan and could continue to do so for quite some time, but it’s unclear how long that will go on.

The general view is that the PBOC will allow the currency to weaken gradually over the course of this year. If so, global investors will be reluctant to participate in the Chinese stock market or in the economy. Capital outflows, which have added pressure on the currency, are likely to continue. It might be better to devalue all at once and get it out of the way – but that would also be disruptive. Nobody said that the transition to a less export-oriented economic system and freer financial markets was going to be easy.

A more significant depreciation of the yuan might lead other countries to devalue their currencies in response, putting more downward pressure on commodity prices. A stronger dollar and a further decline in commodity prices would likely delay (not permanently postpone) future rate hike.

For U.S. investors, we are now in a replay of last summer, where worries about China and the pace of Fed rate increases dominate signs of improvement in the U.S. domestic economy. Nobody also said that investing was easy. However, such anxieties may be likely to fade and return repeatedly in 2016.