10 Attractive Dividend Growth Stocks Poised to Become the Next Dividend Champions Or Aristocrats

Introduction

I screened the Dividend Contenders list provided by fellow Seeking Alpha Author David Fish searching for attractive valuation. This article presents 10 Dividend Contenders that I considered most attractive based on valuation and forecast long-term earnings and dividend growth. I want to be clear that these selections are not offered as a portfolio. Instead, these are 10 individual selections with various degrees of safety, yield and valuation levels that prospective investors can choose from. Hopefully, there is something here for every reader depending upon their own unique investment goals and objectives.

The Power of Attractive Valuation Misunderstood

In my most recent article found here I featured 10 undervalued Dividend Champions for 2016. The primary focus of my last article and this article is on identifying attractive dividend paying stocks that I feel are currently attractively valued for the long-term. In the comment thread of my last article I received a comment suggesting that the companies I wrote about had not outperformed the S&P 500 over various recent histories. What follows is an excerpt of that comment:

“Using your list of PEP, PG, AFL, T, EMR, ABBV, WMT, TGT, JNJ, HCP, I generated a quarterly, equal rebalanced, dividend adjusted portfolio of all of your stocks (source http://www.fasttrack.net). This average has under performed SPY (S&P 500 Index ETF), in the past 1 month, 3 months, quarter, year, two years, three years, 5 years, and 7 years. It had a really good 2000-2002 and 2007-2008.”

The reason I bring this up is to point out what I believe are misconceptions about investing in fairly valued or undervalued stocks. For starters, neither the companies featured in my previous article nor the companies featured in this article are presented as a portfolio. They are presented as individual research candidates that investors can pick and choose from.

Furthermore, what I believe the comment above is also misunderstanding is how and where valuation comes from in the first place. The answer is simple and straightforward, a company does not become undervalued because it is popular. Instead, it becomes undervalued because it has become unpopular. Therefore, to my way of thinking at least, it would seem illogical to think that currently undervalued stocks would be historical outperformers over the short run. But more importantly, logic would also dictate that since they are undervalued, they might be future outperformers going forward.

Moreover, the key to finding a true undervalued stock is to find one that has dropped in price below what fundamentals would justify. But once again my point is this. The very fact that the company has dropped in price would be the very reason why it might have underperformed other companies over recent timeframes. Warren Buffett put it quite succinctly when he said the following:

"Berkshire buys when the lemmings are heading the other way. Most people get interested in stocks when everyone else is. You can't buy what is popular and do well. Warren Buffett”

Additionally, I believe there is another important point that the above comment also misunderstands. My last article and this article are both focused on dividend-producing stocks that can provide more income than the average company. Dividends are paid based on the number of shares owned. Each of the companies I wrote about in my last article are exclusively Dividend Champions that have increased their dividends every year for at least 25 consecutive years.

As a result, each of the companies in my first article did in fact significantly outperform the S&P 500 on the basis of total cumulative dividends paid over all the timeframes cited in the comment. In my last article I suggested that investors should ask and answer this important question: What am I investing for? My last article and this article are offered for investors interested in dividend income and growth thereof.

I am a true value investor. In this regard, and as I stated many times in published articles, value investing is not a strategy designed to produce short-term or immediate price gains. There are practical reasons why this is so, and they also represent one of the greatest challenges to the successful implementation of a value investing strategy.

First and foremost, value investing is a strategy that is most appropriate for long-term oriented investors. The long-term opportunity to invest in a great and growing business at a discount to its intrinsic value is substantial. Moreover, sound valuation means having a firm foundation of fundamental strength supporting your position. This is where long-term safety and risk control comes in.

However, there is always a short-term dark side associated with being a value investor. This is especially true when the value investor uncovers a significantly undervalued opportunity. As previously stated, literally by definition a stock does not become undervalued unless it is out-of-favor in the marketplace. When a stock goes out-of-favor, short-term oriented traders are selling. The more they sell, the further a stock can drop. This can continue for some time until the selling stops. Unfortunately, there is no way to precisely predict when that might occur because it is primarily an emotional response.

Consequently, and once again, over the shorter run a stock can continue to fall, and as it does, if the fundamentals are intact, it becomes more and more undervalued. As the old saying goes, they do not ring a bell at the top or bottom of a market. Therefore, it is not only possible, but very likely, that you can make a great purchase of a super company that is undervalued and still watch the price continue to drop to lower levels before it inevitably turns around. The inevitable part comes when fundamentals support a higher value.

However, the key is to recognize, understand and take comfort in the fact that you bought the stock at an attractive valuation in the first place. Even though it might drop some in the short run, the odds are stacked heavily in your favor that your long-term returns will be even greater than the operating results (earnings growth) that the business itself can achieve. But most importantly as it relates to the thesis of both of these articles, a steadily-rising dividend pays you to wait for the long-term performance to manifest. Therefore, accomplished value investors invest for the long-term, and more importantly, trust fundamental value more than short-term price action.

As an aside, the same principle applies to overvalued stocks only in reverse. In other words, you can significantly overpay for a stock and watch it continue to rise. Even though you overpaid for it, momentum (often driven by greed) can continue to drive it upward for an extended period of time. However, investors should clearly understand two important factors. First of all, paying more than a company is worth implies taking higher risk than fundamentals support. Second, investors should never discount the reality that the market will inevitably come to its senses. It may not happen immediately, but an overvalued stock is vulnerable to almost any bad news.

The point being that true value investors understand that they cannot perfectly time the market, and consequently – they don’t try. Instead, they tend to very carefully assess the intrinsic value of the business they are investing in, and make their long-term decisions based on that assessment. They do this with confidence, because they understand that earnings drive market price (and dividend income) in the long run.

In my opinion, the true value investor buys the company and not the stock. Consequently, this approach requires focusing more on the underlying strength and fundamental value of the business in lieu of reacting to short-term price action. To clarify, I personally never judge the success (or lack thereof) resulting from my investment in a business over a timeframe shorter than 3 to 5 years. This is not an arbitrary timeframe; instead, this represents a normal business cycle. In other words, my minimum definition of long-term is a business cycle spanning at least 3 to 5 years. I emphasize that this is my minimum holding period. Ideally, my objective is to own a great company forever.

But more importantly, there is a simple logic supporting my view. When I am investing in the business, I am buying the company’s future earnings power and dividend growth potential. Although stock prices are reported virtually every minute of every passing day, operating results are only reported 4 times a year. Moreover, it takes the passing of time for future earnings growth and dividend growth to manifest. Understanding this, I personally recognize that the acid test for judging my investment in a business is to measure the level of earnings and dividends I am receiving no earlier than 3 to 5 years after my initial investment, and preferably longer.

In other words, if I invested in the business at a sound or attractive valuation in the first place, I can be almost certain of achieving a successful return if both earnings and dividends have grown over the 3 to 5 year timeframe. Additionally, it might be helpful to also understand that since I have no intention of selling my business for a minimum of 3 to 5 years, the price the market is placing on it between that timeframe is of little importance to me. On the other hand, I do expect to see earnings growth along the way, and for those stocks where I am investing for dividend income, it’s critical to me to see the dividend continuing to grow with each passing year. As long as those things are happening as expected, I have little or no concern about short-term price volatility.

The 3 Phases of Valuation

One of the most important valuation metrics that I often write about and discuss is the P/E ratio. I often point out that a current P/E ratio of 15 as a general rule represents sound valuation for most companies. The only exception to my P/E ratio of 15 valuation measurement would be with companies that are growing very fast. High-growth stocks are worth a higher P/E ratio valuation, because due to the power of compounding, they would generate significantly larger amounts of future earnings than the average company growing at lower rates is capable of. However, and this is critically important to understand, a current P/E ratio of 15 represents only the first of the 3 important phases of properly assessing fair value.

I consider a current 15 P/E ratio relevant as an initial fair valuation measurement for several valid reasons. In other words, I do not consider a P/E ratio of 15 as an arbitrary valuation measurement. Insight into the relevance of a P/E ratio of 15 comes from understanding and recognizing the current earnings yield it simultaneously represents. As I will next illustrate, I do not believe it is a coincidence that the long-term historical returns that common stocks have produced on average correlate very closely to the earnings yield that a P/E ratio of 15 represents. Nor is it a coincidence that the long-term historical normal P/E ratio of the S&P 500 falls within a range of a P/E ratio of 14 to a P/E ratio of 16 (P/E ratio 15 average).

The current earnings yield formula is simply the inverse of the P/E ratio which would be reflected as E/P ratio or earnings divided by price instead of price divided by earnings. A shortcut method of calculating current earnings yield is to simply divide the number 1 by the P/E ratio. Therefore a P/E ratio of 15 equals an earnings yield of 6.67% (1/15= 6.67%). The higher the P/E ratio, the lower the current earnings yield. For example, a P/E ratio of 20 represents a current earnings yield of only 5% (1/20= 5%). A P/E ratio of 25 represents a current earnings yield of only 4% (1/25= 4%) and so on.

The current earnings yield ratio basically tells you, “If this stock were a bond, how much would it earn as a percentage of my investment based on this year’s current earnings?” Once again, it is the inverse of the price-to-earnings ratio, or P/E ratio as it is more commonly known. Stated more simply, the current earnings yield is an easy way to evaluate how much return a company’s current earnings power is providing you if you invest in it. This calculation is metaphorically considering the percentage return your money would be earning if you owned the whole company and were entitled to all of its profits.

Obviously, as an investor you want the company’s profitability to generate you a return that is acceptable relative to the risk you are taking through investing your capital. The higher the current earnings yield (the lower the P/E ratio), the more attractive the valuation you are paying to buy those current earnings. This is important because at the end of the day as an investor in a business, your total compensation is subject to the future earnings power of the business. In short, investors in a business are buying future earnings power. Both future capital appreciation and dividend income will be sourced from the company’s ability to generate future profits.

To summarize, the importance and relevance of the first phase of valuation based on a company’s current P/E ratio is to understand that it only represents the beginning of a more comprehensive valuation assessment. In this regard, I look at it as essentially a screening tool. As a general rule, if I come across a company I like very much, but discover that it is currently being valued at a P/E ratio above 15, I will temporarily pass on further research and due diligence until it becomes more reasonably valued. However, I might place this company on a watch list where I am on-the-lookout for a better entry point. Phase 1 of a comprehensive valuation effort is a reasonable current P/E ratio. Phase 1 is assessing a company’s present or current valuation.

Phase 2 focuses on examining and analyzing a company’s historical operating history and normal market valuation levels. Phase 2 entails learning as much as we can from the past about the company by analyzing its historical operating history, growth rate achievements and how the market has normally valued those results.

Importantly, Phase 2 is executed in order to determine whether or not a company is maintaining its growth, reducing its growth or accelerating its growth. This process requires analyzing a company’s history over numerous historical timeframes. What we are primarily looking for here are trends and/or changes in those trends. Additionally, up to this point we are attempting to relate historical norms to present valuation in order to give us a perspective of what we might expect with an investment in a respective company. However, the completion of Phases 1 and 2 do not fully prepare us to make a final buy, sell or hold judgment.

Phase 3 is the final, and I contend most important step in properly assessing fair valuation and entails making reasonable forecasts of what the future may hold for the company in question on an operating basis. At this point it’s critical to understand that forecasting the future specifically relates to making assumptions about the company’s business prospects and not a forecast of what the stock price might do. However, this Phase 3 process derives its confidence from the notion that if the investor can assess future operating potential within a reasonable degree of accuracy, then stock price will surely follow in the long run. This supports the principle that long-term fundamentals are more important than short-term price action.

To summarize the 3 phases of valuation, the accomplished value investor is analyzing the past, present and future prospects of any stock they are interested in investing in. Although each phase is essential towards making a comprehensive valuation assessment, the third and final phase is most relevant regarding what your future return potential might be. We learn from the past, calculate the present and make our best forecasts about what the future might hold. At the end of the day, future returns from both capital appreciation and dividend income will be functionally-related to the valuation you pay to buy future earnings relative to the total amount of future profits (and dividends, if any) you will receive.

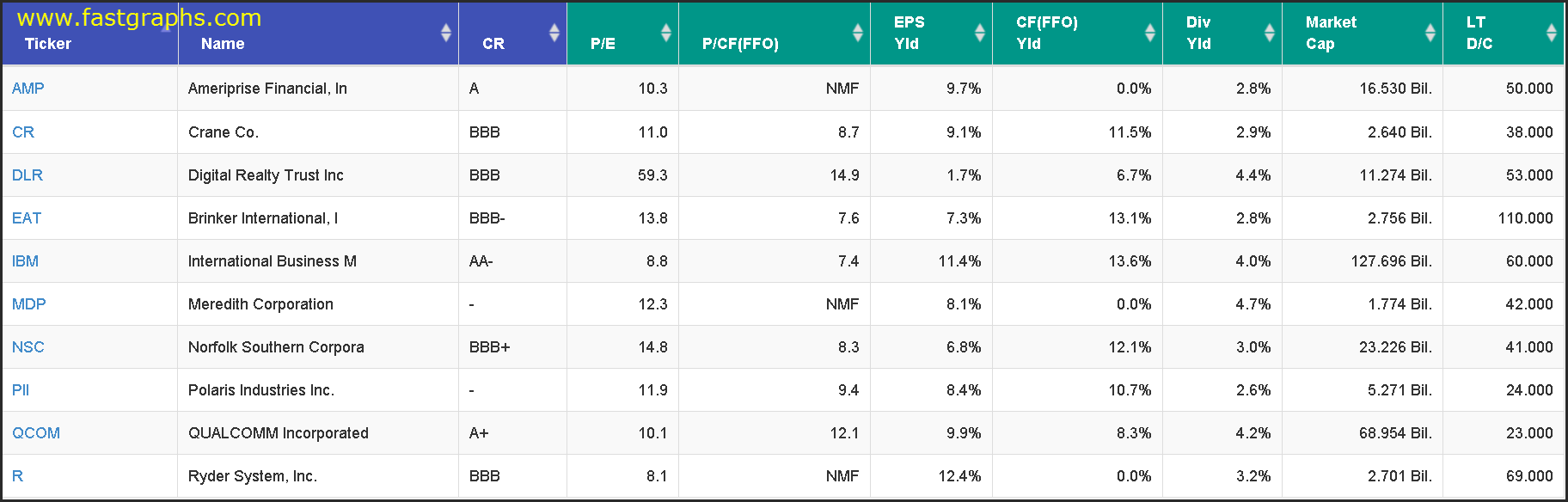

10 Currently Attractively-Valued Dividend Contenders

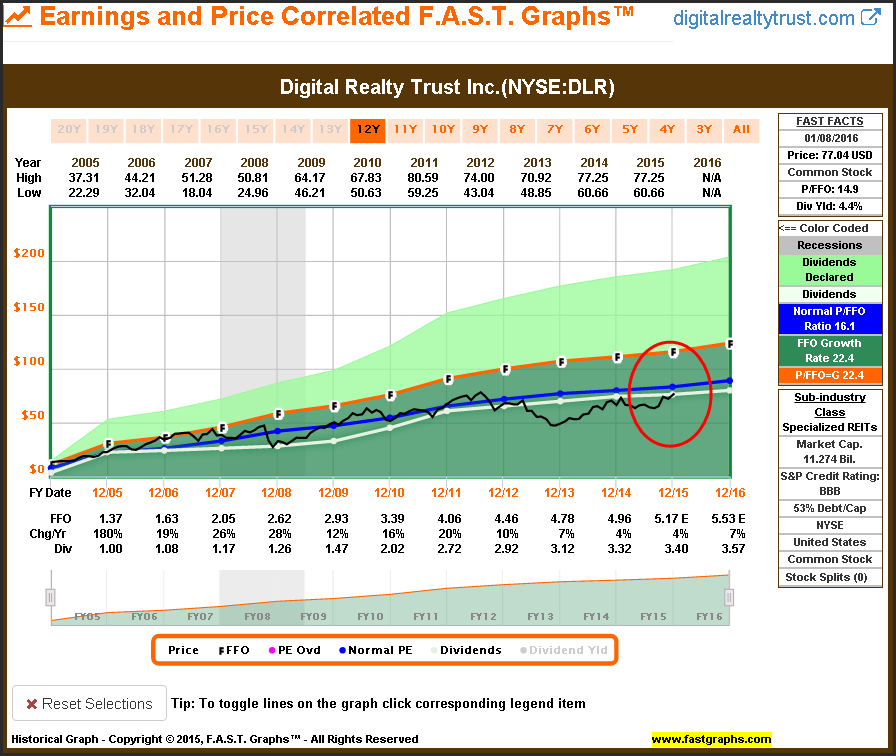

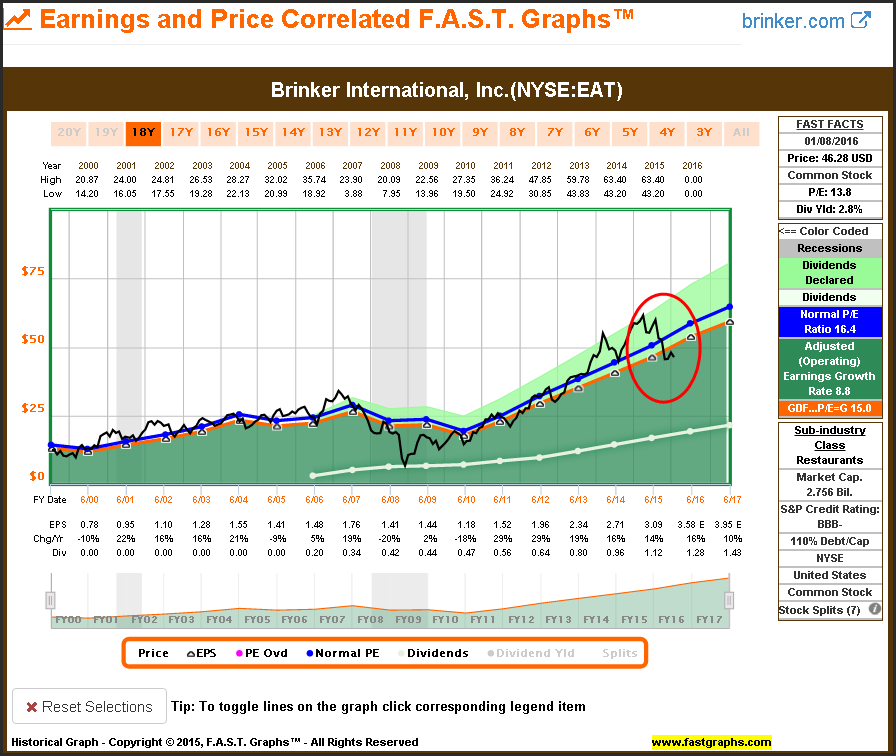

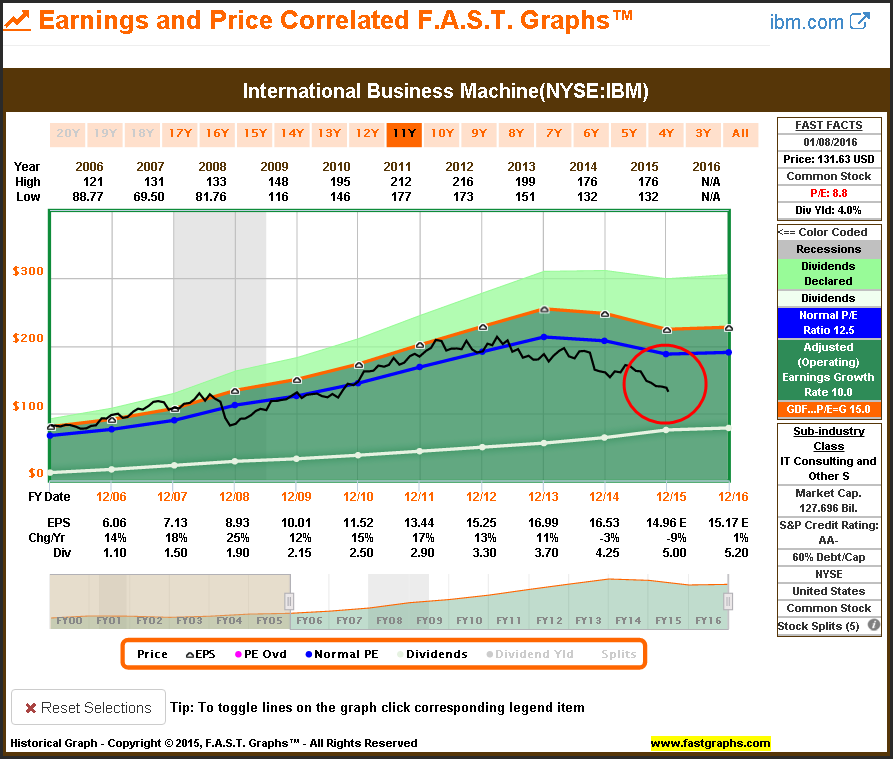

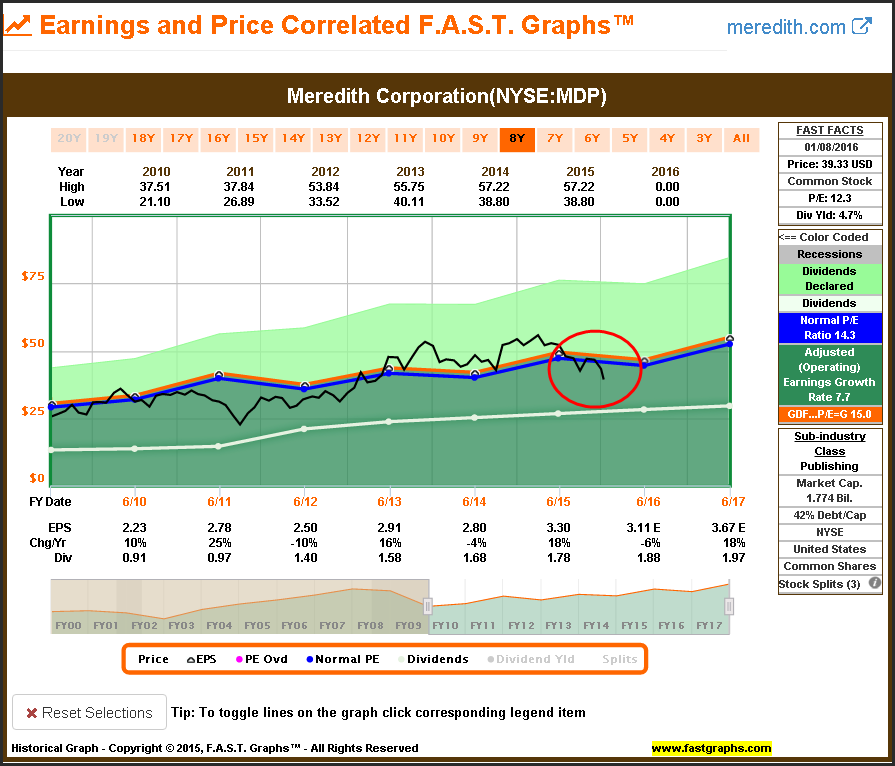

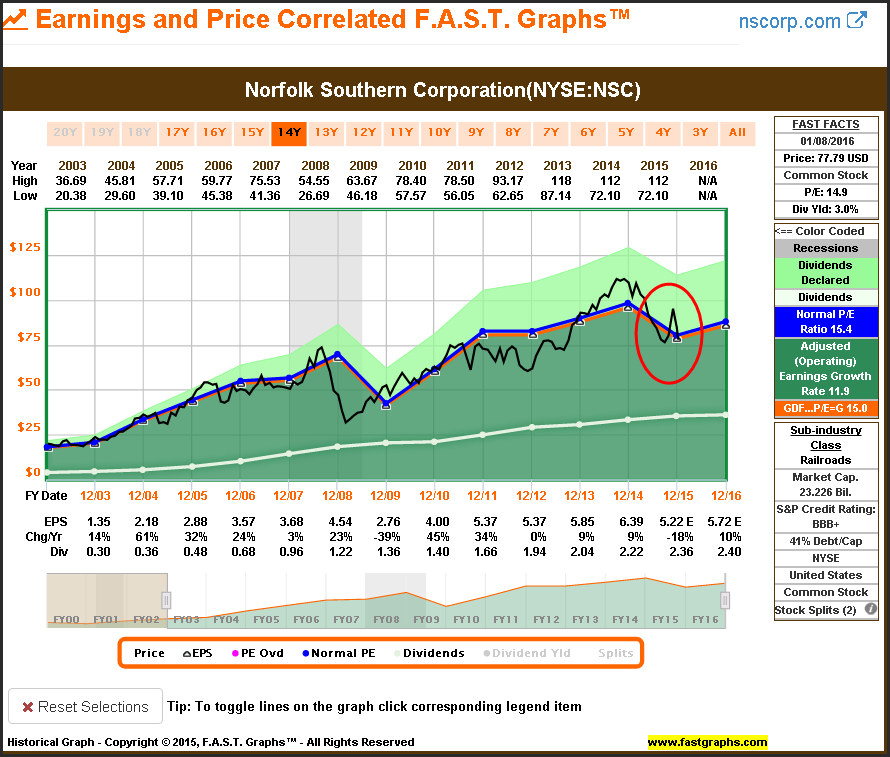

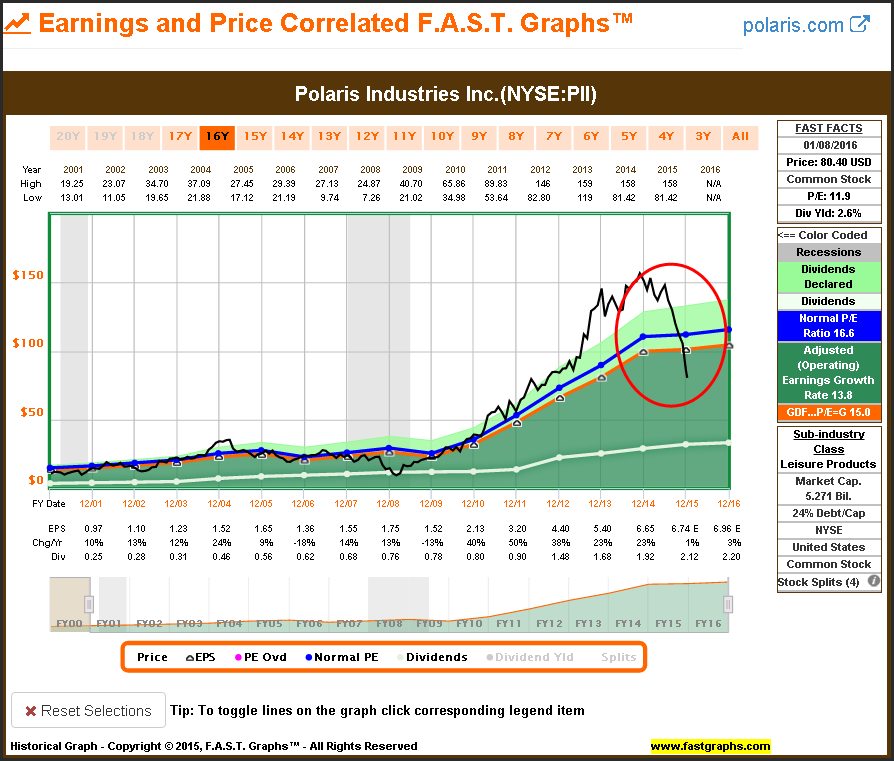

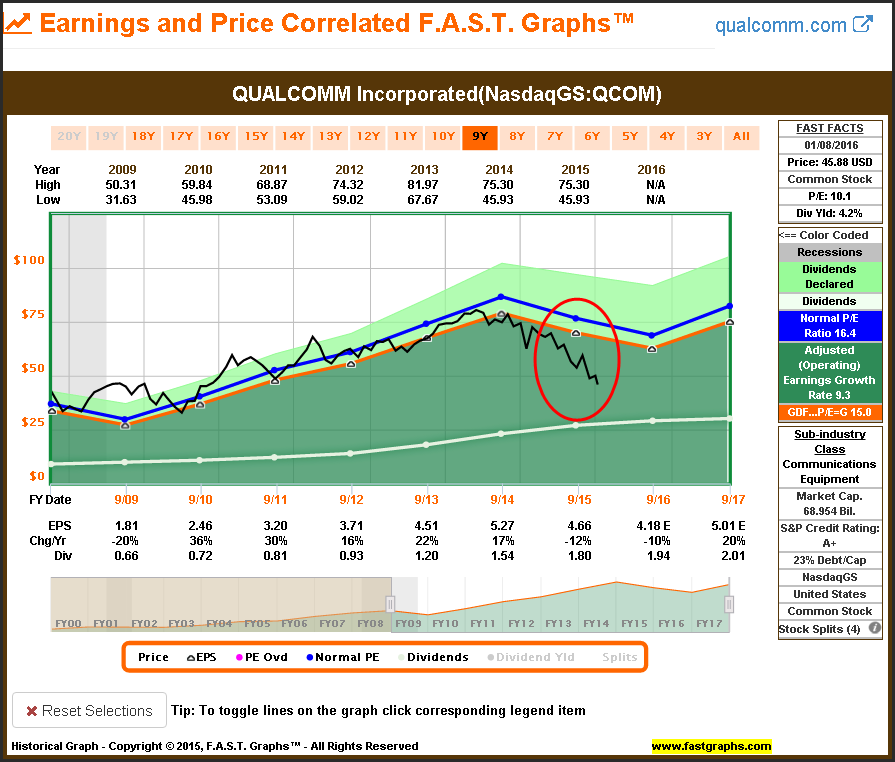

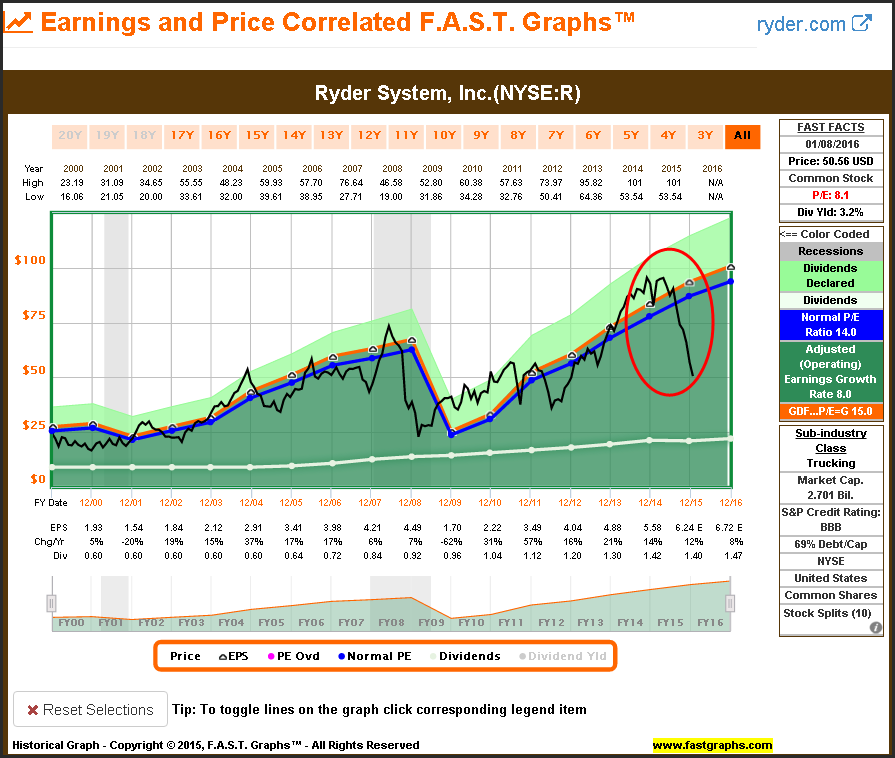

The following F.A.S.T. Graphs™ portfolio review lists my top 10 attractively-valued Dividend Contenders for 2016 based on valuation. Following the portfolio review, I will present individual earnings and price correlated F.A.S.T. Graphs™ plus performance reports on each company. On the earnings and price correlated graph, focus on price relative to the orange earnings valuation reference line. The venerable Peter Lynch pointed out the importance of this exercise in his best-selling book “One up on Wall Street” where he said this:

"You can see the importance of earnings on any chart that has an earnings line running alongside the stock price. On chart after chart the two lines will move in tandem, or if the stock price strays away from the earnings line, sooner or later it will come back to the earnings." Peter Lynch - 'One Up On Wall Street'

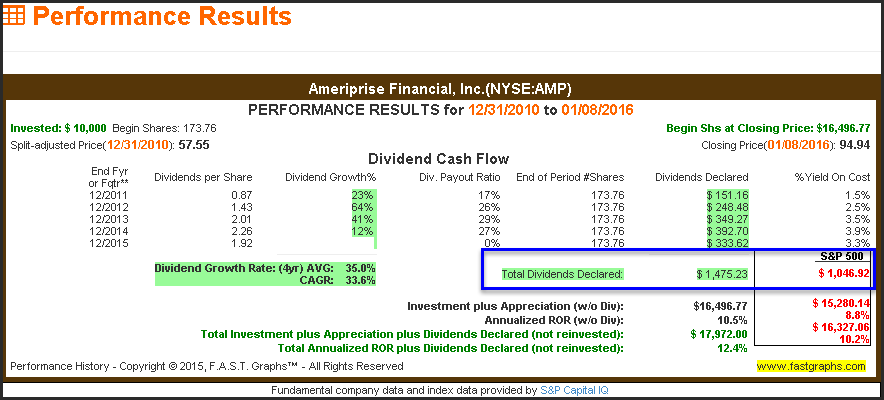

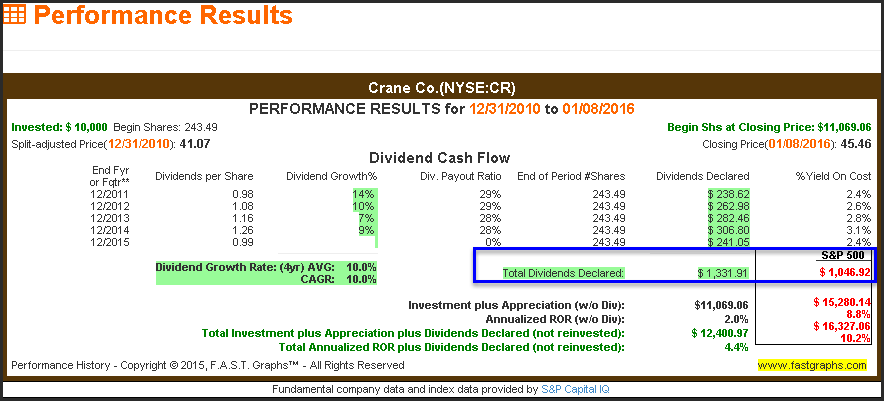

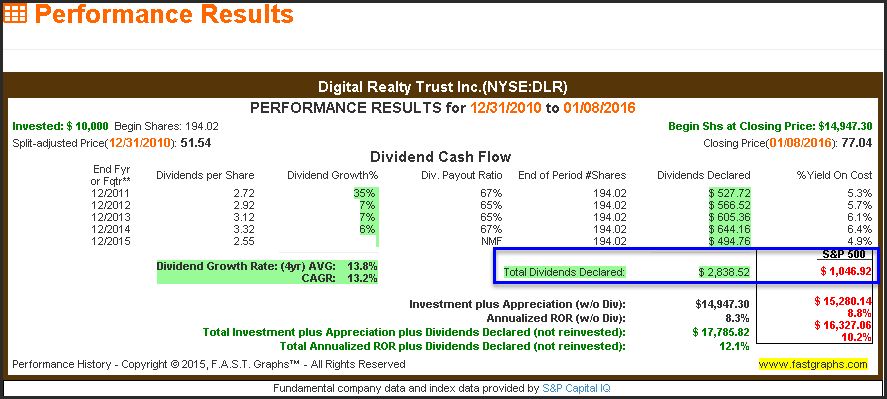

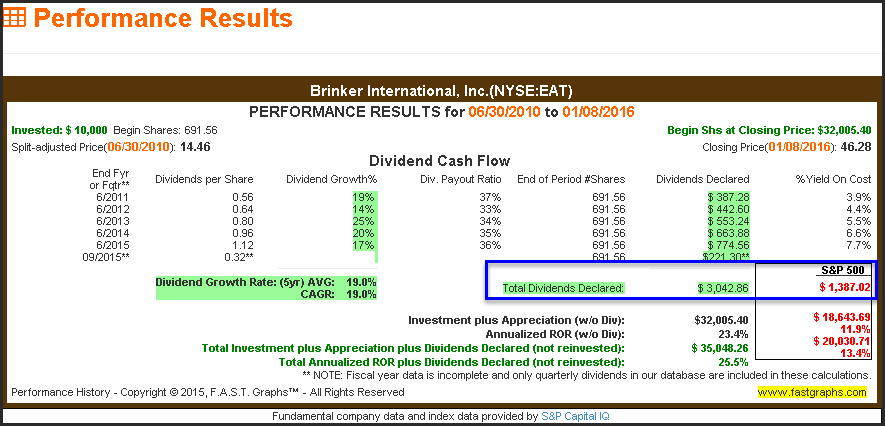

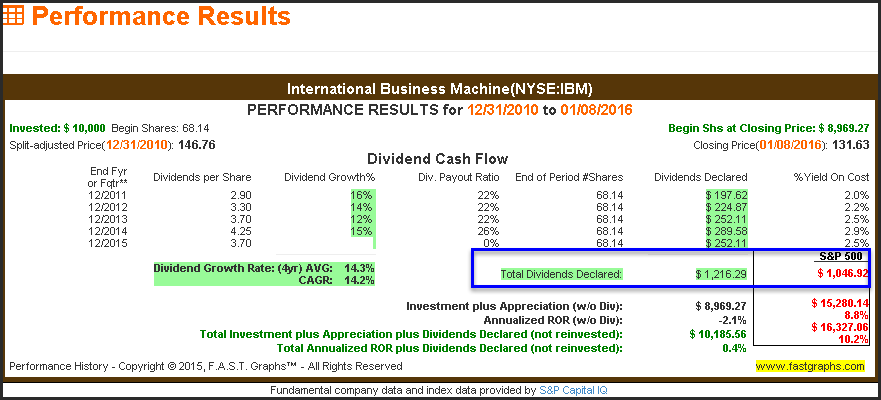

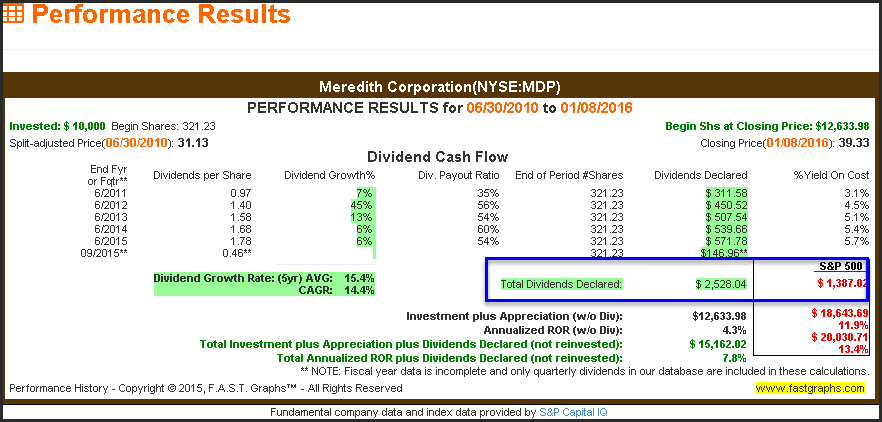

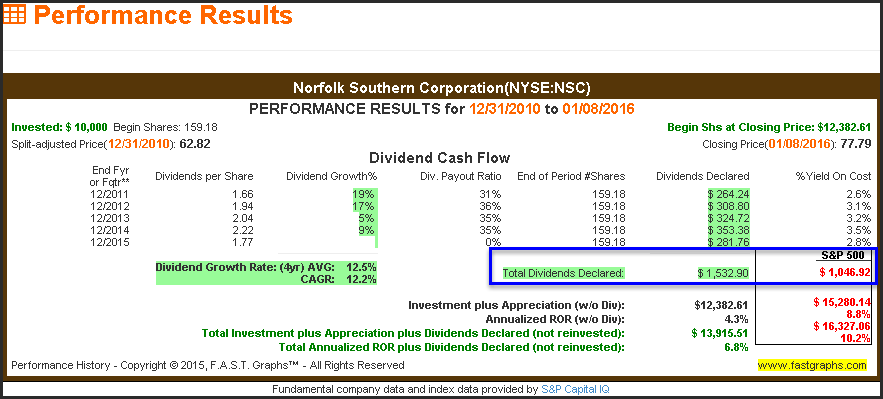

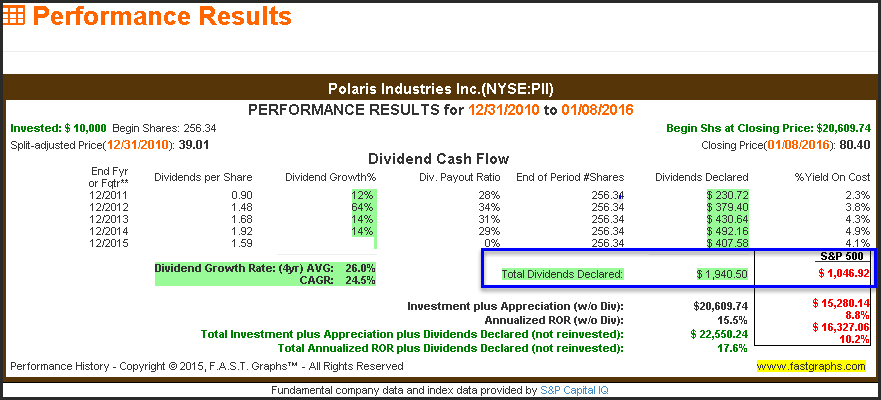

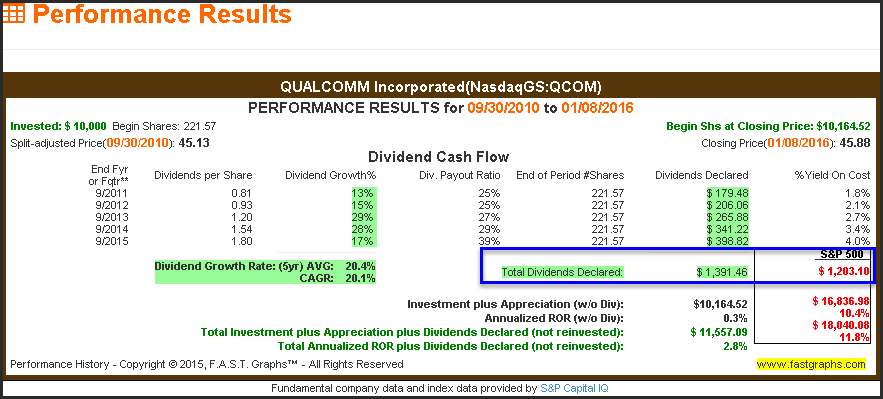

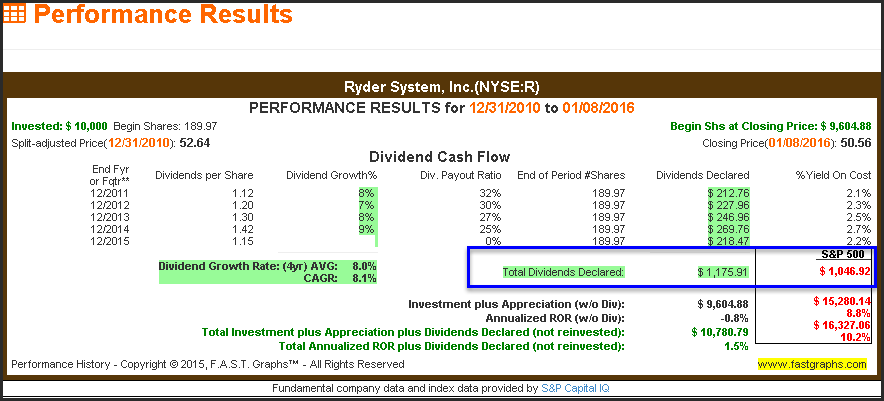

The performance reports presented in this article are produced for the past 5 completed years and therefore are not consistent with the length of the historical graphs. I did this to illustrate the income advantage that undervalued stocks can still have even over short periods of time. Therefore, on the performance reports, note the total cumulative income versus the S&P 500. Since these companies are generally currently out-of-favor, many of them have not outperformed the S&P 500 on a total return basis over the past 5 years. However, all of them have produced more cumulative total dividend income than an equal investment in the S&P 500 over the past 5 years. This article is focused on investing for dividend income.

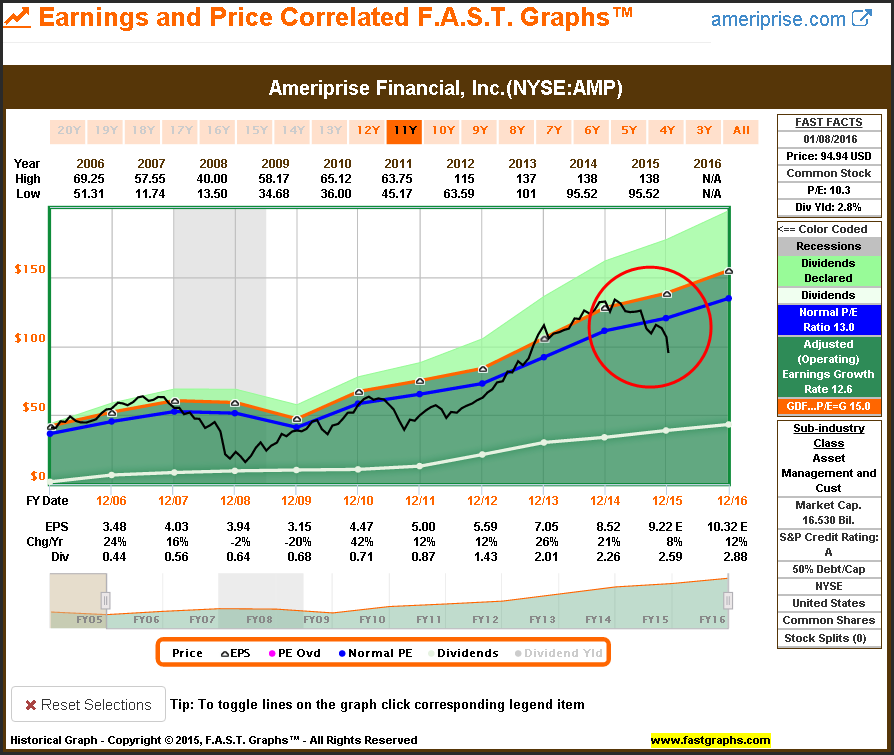

(AMP) Ameriprise Financial Inc: Dividend Increases for 11 Consecutive Years

(AMP) Ameriprise Financial Inc: Dividend Increases for 11 Consecutive Years

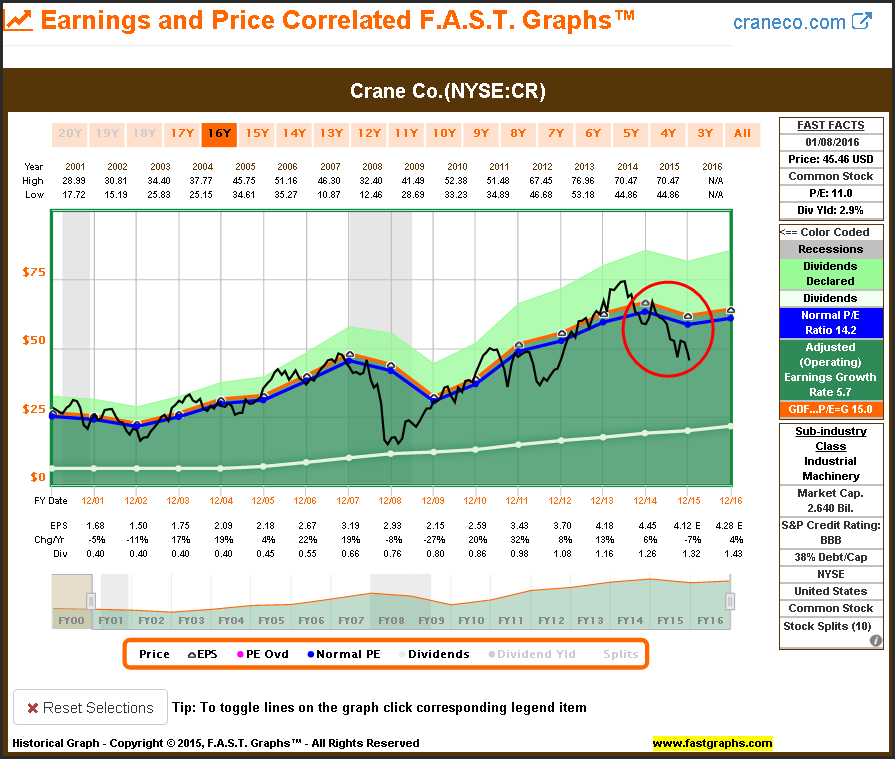

(CR) Crane Co: Dividend Increases for 11 Consecutive Years

(DLR) Digital Realty Trust Inc: Dividend Increases for 11 Consecutive Years

(EAT) Brinker International: Dividend Increases for 11 Consecutive Years

(IBM) International Business Machines: Dividend Increases for 20 Consecutive Years

(MDP) Meredith Corporation: Dividend Increases for 22 Consecutive Years

(NSC) Norfolk Southern Corporation: Dividend Increases for 14 Consecutive Years

(PII) Polaris Industries Inc: Dividend Increases for 20 Consecutive Years

(QCOM) Qualcomm Inc: Dividend Increases for 13 Consecutive Years

(R) Ryder System Inc: Dividend Increases for 11 Consecutive Years

Summary and Conclusions

Following a valuation-based investment approach is a proven strategy towards producing above-average long-term returns. Applying the discipline to only invest in a stock when it is fairly valued works equally well for growth oriented investors as it does for dividend income oriented investors. However, it could be argued that value investing is most advantageous for dividend income oriented investors than it is for growth oriented investors. The reason is simple and straightforward. Dividend growth investors can expect to receive a continuously growing stream of income that compensates them for waiting for the long-term results to manifest.

Importantly, value investing is not a short-term oriented strategy. It is both possible and likely that short-term total return results may be disappointing for a time. Therefore, a key component for implementing a successful value investment strategy is patience. However, I like to think of it as intelligent patience that is supported from understanding the fundamental value of the businesses you are investing in. The most accomplished value investors trust fundamentals more than they do fickle short-term price action.

Disclosure: Long AMP,DLR,EAT,IBM,MDP,NSC,QCOM.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.