China marked its currency lower once again yesterday. That makes eight days in a row they lowered the yuan. Last August, they devalued the yuan and that sent global equity markets into a dive. As Yogi Berra would say, “It’s déjà vu all over again.”

For many years, the yuan had been pegged to the dollar. The Fed’s move to raise interest rates not only strengthens the dollar versus most every other global currency, it also strengthens the yuan for the yuan is largely pegged to the dollar.

China is trying to escape the Fed effect and they are shocking the markets in Asia, in Europe and here in the U.S. China is just one of the risks. Add European Sovereign debt, emerging market dollar denominated debt and high yield bond market debt to the mix. Nothing new here to report. We are just seeing it begin to play out.

Last week, I shared with you my 2016 Outlook. This week, let’s look at the most recent valuation charts and trends in earnings. We’ll also take a look at the most recent recession charts. Why? Because markets tend to lose 40% to 50% or more in value during recessions. Recessions also present us with the best buying opportunities.

If you are under-weight equities (and hedged), equal-weight fixed income and over-weight liquid alternatives (defined as anything other than traditional buy-and-hold), then continue to bump through the volatility and stay patient, liquid and nimble.

As a quick aside, you may be getting a question from your client(s) who asks, “Why didn’t I beat the market?” Portfolios are built to be diversified for a reason (stocks, bonds, alternatives), yet we somehow as an industry/media have taught investors to compare everything they do against the DJIA (just 30 large stocks) and the S&P 500 Index (500 large cap stocks). We attempt to answer that question and several others in the links I share with you below. Feel free to use them. We hope you find them helpful in your work with your clients.

- When Beating the Market Isn’t the Point

- Correlation, Diversification and Investment Success

- The Merciless Math of Loss(this is about how compound interest works for you)

- Here is a link to our Advisor Blogpage

- Here is a link to our Advisor Resourcepage

Also, I often run across an interesting piece of research or an article that may not make it into OMR. I often use Twitter to share them. If you want to follow some of what I am reading you can follow my posts on Twitter here.

Ok, let’s take a quick look at the most recent valuation charts, several recession probability charts and an interesting chart that looks at the historical performance of the market in election years. Hint: poor first half, better second half.

You’ll find this week’s On My Radar to be a quick read. Thank you for your interest. It is appreciated.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Valuation Charts

- Recession Charts

- Market Performance During Election Years

- Trade Signals – Rough Start To The New Year

- Personal Note – Colorado, Florida and Lamb Chops

Market Valuation Charts

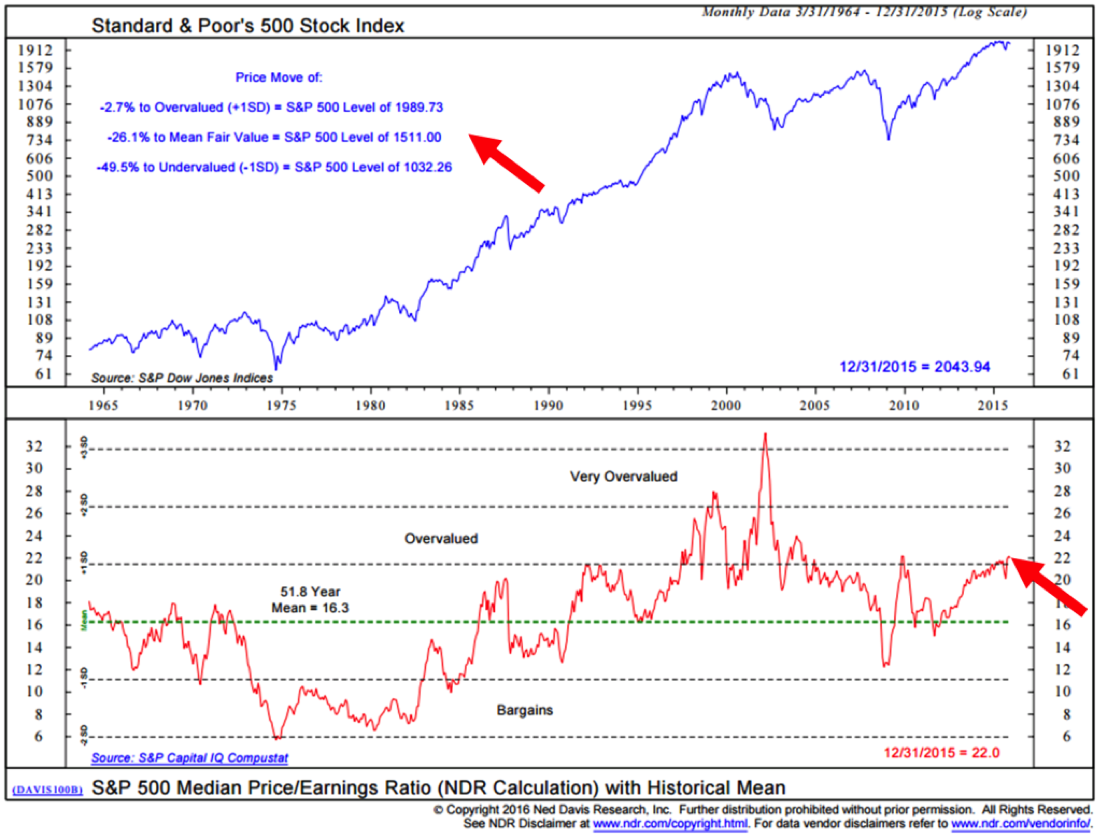

My favorite PE valuation chart is NDR’s Median PE. I like it because it takes removes a lot of accounting gimmicks. By tracking the current month-end median PE (based on the last 12-months actual reported earnings) and comparing the number to all of the historical month end numbers I believe it gives us sound footing for whether valuations are high or low and what probable 10-year forward return may likely be.

You’ll see in the next chart that prices are high relative to earnings. Median PE sits at 22.

A note on earnings growth:

The market has been driven higher by P (price) and less be E (earnings). The energy and commodity sectors are a mess. So what will be needed is expansion in earnings and that is unlikely at this stage in the cycle. Especially give strong employment and increasing wage pressures. P has historically had trouble at the “overvalued” dotted line and E is out of gas. Earnings expansion is a really tall wish.

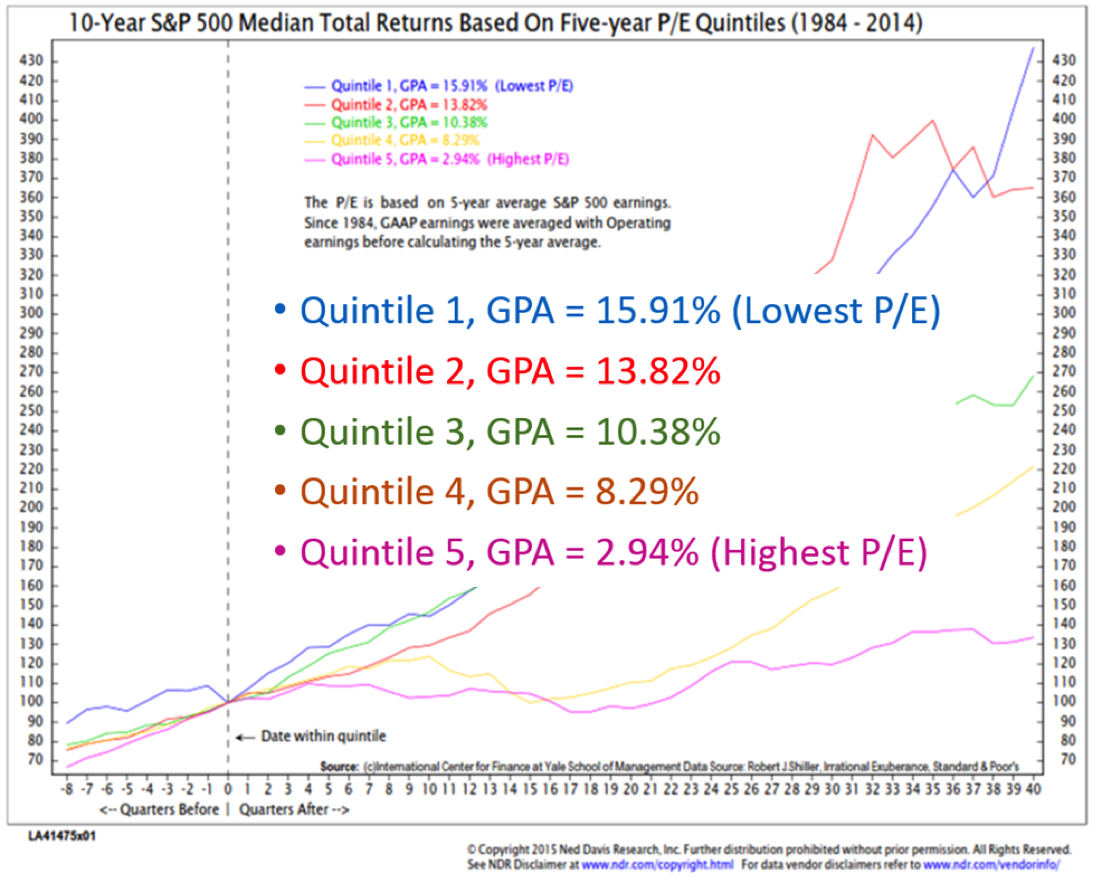

Here is another look at Median PE and probable forward 10-year returns. When PE is high, returns are low. We want to get aggressive into equities when PE is low. I’ll work with NDR to update this chart through 2015. Expect no significant changes.

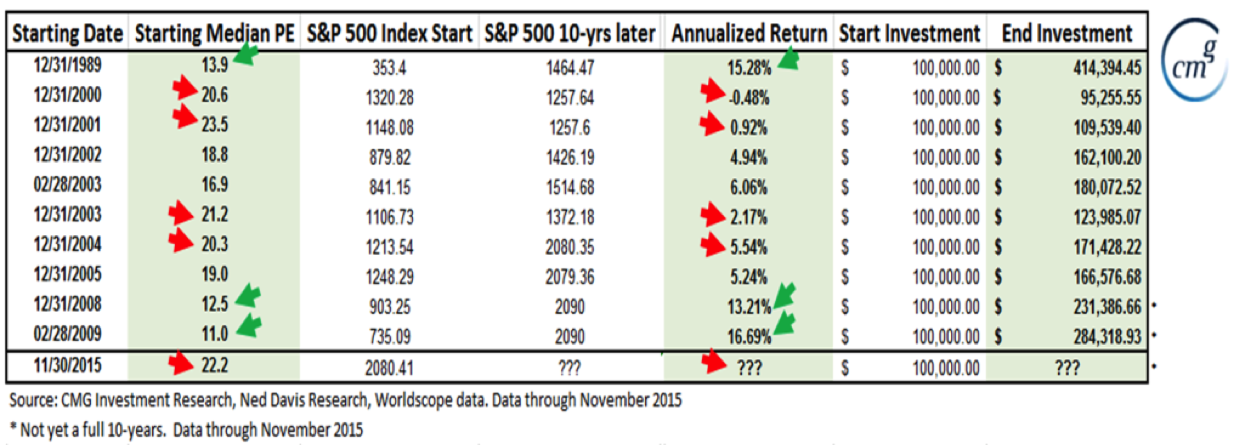

Next is a look at selected periods in time and subsequent 10-year annualized returns (red arrows point to high PE periods and green arrows to low PE periods).

The best buying opportunities come during periods of economic recession so let’s look there next.

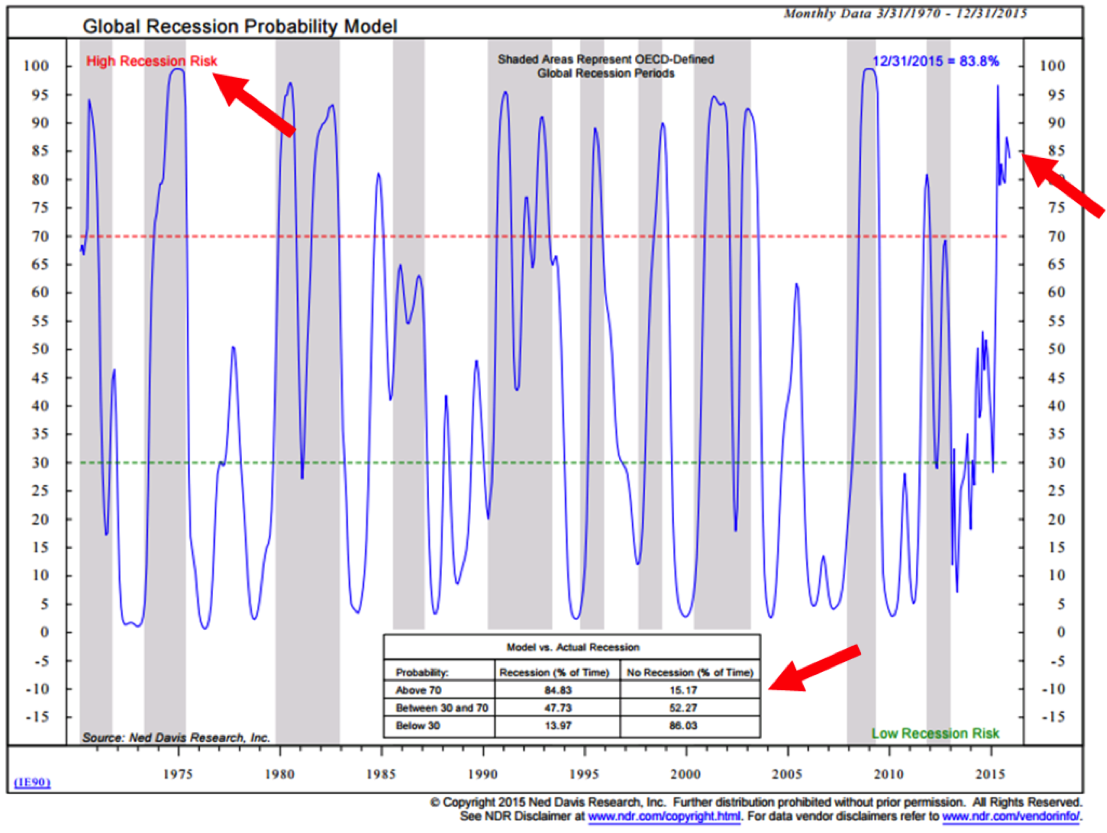

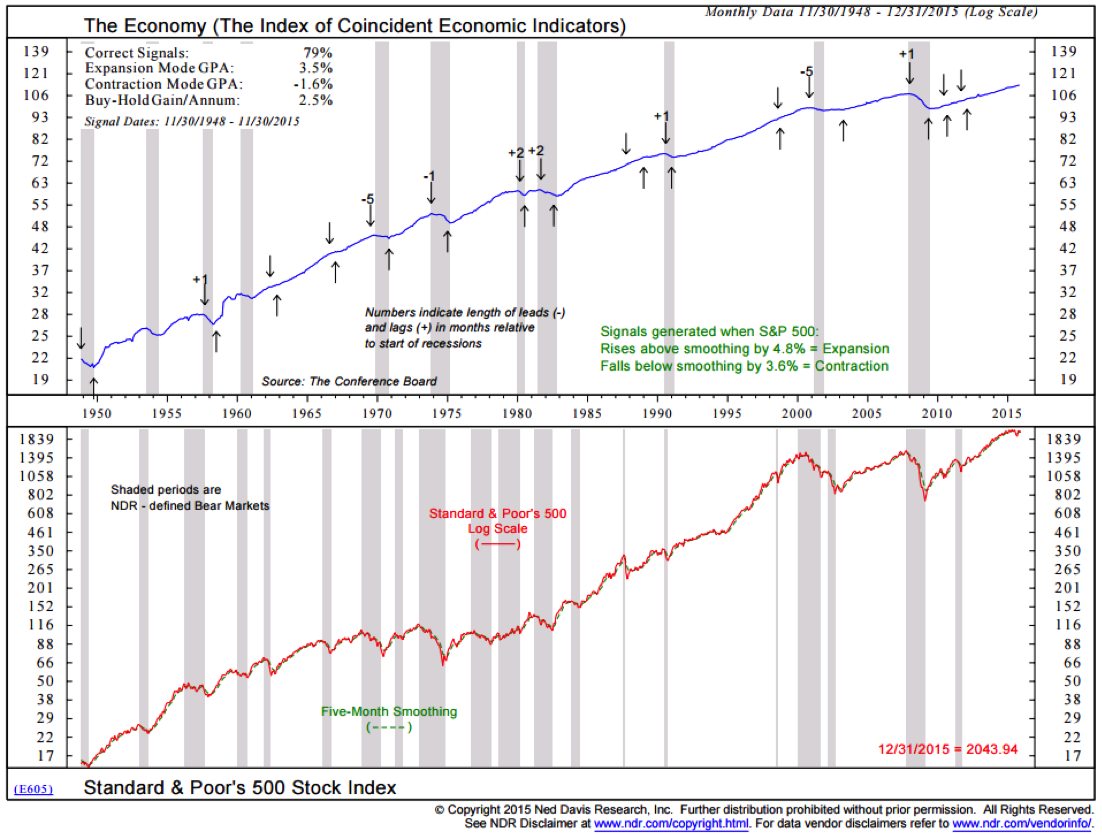

Recession Watch Charts

Chart 1 Global Recession (high probability a global recession has started)

Chart 2 – U.S. Recession Watch (no sign of recession)

The gray shaded areas show all of the recession since 1948. The down arrows show when the data signaled coming recession. The up arrows show coming expansion.

79% of the historical signals were correct. There idea here is that the stock market is a very good leading economic indicator. At the end of December, this recession prediction process continues to favor U.S. economic expansion.

However, the trigger for contraction is a drop in the S&P 500 index, on a month end basis, 3.6% below its Five-Month smoothed moving average. Today, the S&P 500 is approximately 5% below its Five-Month Smoothing. We’ll see how the balance of January unfolds.

I have a few quick additional economic observations to share:

- There remains extreme weakness in commodities even when the impact of strong dollar is eliminated. My longer-term negative view on commodities remains.

- Oil – still not near a bottom. At every major bottom, bullish speculators have given up their bullish posture and go net short. Sentiment remains bullish; therefore, I see more decline in oil. Need to remove the extreme bullish sentiment before I feel good about oil.

- HY vs Investment grade. If we separate out commodities and energy we see that it is not just energy and commodities showing spreads widening (corporate bond yields rising faster than safer Treasury yields). HY will tell us a lot about the economy (recession). It appears to be signaling growing concern.

Election Year Charts

I simply thought you’d find this next chart interesting. Note the historical first half of the year market challenges during election years and the second half strength. Generally, when the market is confident it has identified the winner it typically begins to rally at that point. We’ll see.

Trade Signals – Rough Start to the New Year

Equity Trade Signals:

- CMG NDR Large Cap Momentum Index: Sell Signal – Bearish for Equities

- Long-term Trend (13/34-Week EMA) on the S&P 500 Index: Sell Signal — Bearish for Equities

- Volume Demand is greater than Volume Supply: Sell Signal – Bearish for Equities

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Extreme Pessimism (short-term Bullish for Equities)

- Daily Trading Sentiment Composite: Extreme Pessimism (short-term Bullish for Equities)

Fixed Income Trade Signals:

- The Zweig Bond Model: Sell Signal

- High-Yield Model: Buy Signal(Now a HOLD and nearing a SELL)

Click here for the link to the full Trade Signals (updated charts and commentary).

Personal note – Colorado, Florida and Lamb Chops

The travel schedule is full in January. NYC is ahead on January 21. I’m attending and speaking at the Inside ETFs conference in Florida on January 24-27. Here is a link to the speaker line up and agenda. It is the largest ETF conference in the industry. Attendance is expected to exceed 2,000. Please reach out to me by email if you are going to be there. I’d love to grab a coffee.

As I was sitting on a chair lift in Park City, Utah with my kids a week ago, a call came in from one of our trade execution partners. “Join us in Vail for a few days,” they said. Talk about a good day. The plan is to meet in Vail this coming Sunday, Monday and Tuesday. Attending will be other ETF strategists and trade execution experts. So much is gained in these types of meetings.

Following the Inside ETFs conference, on January 28, I’ll be in Venus, Florida (just south of Sarasota) meeting with the research team at Ned Davis Research. Really looking forward to that. Fortunately, Susan’s mother and father live in Venus so Susan is flying down for a few days. I see one or two of Patricia’s famous lamb chops and some nice red wine in my near future.

Hope this note finds your year off to a great start. Have a great weekend!

With kind regards,

Steve

Stephen B. Blumenthal Chairman & CEO CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter entitled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG White Paper Understanding Tactical Investment Strategies, you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History: Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Provided are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of this Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro FundTMand the CMG Long Short FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro FundTM and CMG Long Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e., S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC registered investment adviser located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group