Where do we stand now, economically?

“Well, we are right back at it: trying to stimulate growth through easy money. It hasn’t worked, but it’s the only tool the Fed’s got. Meanwhile, the Fed’s policies widen the wealth gap, which feeds political extremism, forcing gridlock in Washington. It seems the world is headed toward negative real interest rates on a global scale. This is toxic. Interest rates are used to price risk, and so in the current environment, the risk-pricing mechanism is broken. That is not healthy for an economy. We are building up terrific stresses in the system, and any fault lines there will certainly harm the outlook.”

-Michael Burry, Scion Asset Management (Source: Big Short Genius Says Another Crisis is Coming)

If you haven’t seen the movie The Big Short, go see it. Christian Bale plays Michael Burry in Adam McKay’s adaptation of Michael Lewis’s book about the 2008 financial crisis. Burry was one of the hedge fund managers me and my team knew well. He and others helped us to better understand the approaching sub-prime crisis. I wrote about the issue frequently back then.

Nobody knew when it would happen nor the depth of the break, but we were pretty sure it would be big. As it turned out, it was far worse than we anticipated. I never imagined the near collapse of the financial system. I should have gone short the sub-prime trade I was well aware of, or shorted Fannie Mae, or the mortgage lenders or the banks.

Back in 2007, most of the emails I received were not favorable. Steve, you’re way too bearish. It turned out I wasn’t bearish enough.

Today, it feels to me much like it did in 2006 and 2007. However, this time around I’m looking through a lens of opportunity — not worry, not fear.

If you’ve been reading my weekly On My Radar posts, you know I believe valuations are too high, the Fed is too involved and debt in the U.S. and globally is choking growth. My overall message is to hedge your equity exposure, tactically manage your bond exposure and find some liquid alternative strategies that drive a return stream with little correlation to the stock and bond markets. A broader mix of risks to hopefully provide growth and downside protection. Diversification that will allow you to pivot when valuations become attractive.

“Government intervention is causing financial investor chaos by destroying the analytical value of any economic or financial variable it touches. The extremely wide ranging fiscal and monetary policies since the AIG/Lehman default have rendered financial variables such as interest rates, yield curves, credit spreads and various money supplies useless for either assessing asset values or forecasting.”

The above quote is from a recently published book entitled, Not My Grandfather’s Wall Street: Diaries of a Derivatives Trader by David von Leib. David is a long-time friend. For me, watching a movie like The Big Short or reading David’s fine book brings back to center the reality of how things work. We’d like it to be different but for now it is not.

And unfortunately (or fortunately, if you are on the right side of the trade), we find ourselves in a place not too dissimilar to 2008. David summed up the challenge we investors face back then (and now):

“In other words, in trying to artificially prop up the world, the Fed and other global central bankers had left savvy Wall Street investors relatively confused. A culture of general artificiality had evolved where you could either bet that governments would win in the short term (but risk losing your shirt over the longer-term) or bet against governments and be ever so frustrated in the short-term (and then see if your capital under management would survive long enough to potentially still win in the longer-term). It was next to impossible to wager on both outcomes—or shift between the two views—with enough alacrity to also remain sane.”

This is the challenge we face today.

My outlook for 2016 is neutral on equities and neutral on fixed income. Nothing exciting there, but like the Fed, I’ll hedge and say it is “data dependent.” Following are the significant risks I see:

- Global Recession – Likely underway

- U.S. Recession – Possible in 2016. Probable in 2017. The largest market declines come during periods of economic recession.

- High-yield bond defaults – Rising in 2016, peaking in 2017 (tactically trade HY)

- European Sovereign debt crisis – The EU banks are loaded up on that debt (shorting EU banks or buying out-of-the-money put options may be a good equity hedge).

- Emerging Market dollar denominated debt crisis

- Watch the Fed, ECB, JCB and Chinese central bankers

- Tax and structural reform would be a positive for the markets, but unlikely in 2016

We’ll keep a close eye on the data each week in OMR and Trade Signals.

In 2007, it was about no-doc mortgages, sub-prime mortgage debt, pools of packaged mortgage debt and the derivatives that were tied to those risks. When the defaults came rolling in, it was the banks that broke and nearly collapsed the entire financial system.

This time, the nature of the debt is not mortgage debt. It is record high-margin debt (investor brokerage accounts), government debt (Europe, Japan, the U.S. and China), Emerging Market debt (based in dollars and subject to default risks due to a rising dollar) and high-yield bond market debt. But like last time, the coming default issues may likely find their way to the banks. Recall in 2008, you were impacted even if you didn’t own the bad debt. This is known as “systemic risk.”

My friend Jim Rickards, the author of Currency Wars, penned the following and I share it with you in bullet format (as you read it, think in terms of probable human behavior):

- The natural state of the world is deflationary, due to demographics, technology and debt.

- This is the outcome central banks fear most. Deflation increases the real value of debt and accelerates defaults. We’re already seeing this in energy and other junk debt.

- The defaults will soon spread to more highly rated corporate debt. Ultimately, these losses fall on the banks.

- Deflation also destroys tax collections. Taxes are imposed on nominal dollar returns, not real returns. When deflation causes prices and incomes to drop, less tax is collected, pure and simple.

- The combination of bank losses, higher real debt burdens and diminished tax collections is a government’s worst nightmare. For these reasons, central banks and governments will do whatever it takes to stop deflation.

- The current business expansion is already 79 months old — longer than the average expansion since 1980 (77 months).

- This does not mean that a recession begins tomorrow (although it might). It does mean we are late in this cycle and at a point when the Fed historically stands pat or even begins to contemplate rate cuts.

- The situation around the world is even more dire. Russia, Japan and Brazil are already in recession. Canada and Korea are close to one. China is slowing down rapidly and taking a large bite out of global GDP growth.

- Deflation is intolerable to governments, we look for evidence that governments are taking steps in the direction of increased deficit spending (debt monetization).

- Two months ago, the U.S. Congress and the White House agreed to bust the spending caps that had been in place for the past three years. Large new spending programs are also getting underway in France, China, Japan and Canada. This will take time to play out, but the direction is clear.

- Governments fear deflation and will do anything to avoid it. Yet central bank monetary tools have failed to produce inflation and will likely continue to fail. What else can a government do?

- The answer is debt monetization. This is also known as “helicopter money” or “people’s QE.” A more technical name for it is “fiscal dominance.” It all amounts to the same thing. If the people won’t spend money, the government will.

- Governments will pick spending programs to stimulate growth and then incur huge deficits to support the spending. The deficits will be financed with government debt. Then the central banks will print money to buy the debt.

- The difference between debt monetization and quantitative easing is that the money does not just sit in the bank. It goes directly into whatever spending programs the government chooses. The spending is guaranteed to happen, and in theory, that will get the economy moving and produce the desired inflation.

- You can learn more about Jim at www.agorafinancial.com

Two weeks ago, I wrote in On My Radar about Henry Hazlitt and Inflation. Why inflation when deflation is currently winning? Maybe I’m a few years ahead of that trade (and I think I am) but it is because deflation is feared most and the human response of central bankers and politicians will be to throw their collective weight and sit it on the other side of the deflation/inflation seesaw. In short, ultimately, inflation will win.

To that end, commodity plays may likely find a bottom as the bear market ends and a cyclical bull market begins. Down more than 50 percent, “buy when everyone else is selling” may be the right move.

We just don’t know the timing of how all of this plays out. I’ll be watching our models for strong relative strength. Data dependent…

So why am I neutral on equities and fixed income? It is hard to make a lot of money in the bond market when interest rates are so low. As for equities, valuations are too high, thus limiting forward returns. Could the comparatively higher rates in the U.S. and a sovereign debt crisis reemerge in Europe causing global capital to race into U.S. dollars and further into U.S. equities? Yes. But like what followed similar global events in the late 1920’s, that capital flight into both U.S. equities and government bonds looked good at first but ended badly. Don’t chase into equities at expensive prices, but if you do, make sure you are hedged. Be careful, stay hedged and stay nimble.

Finally, I’ll be sharing with you the December 2015 valuation updates in a week or so. Until then, note the following from GMO and Market Watch.

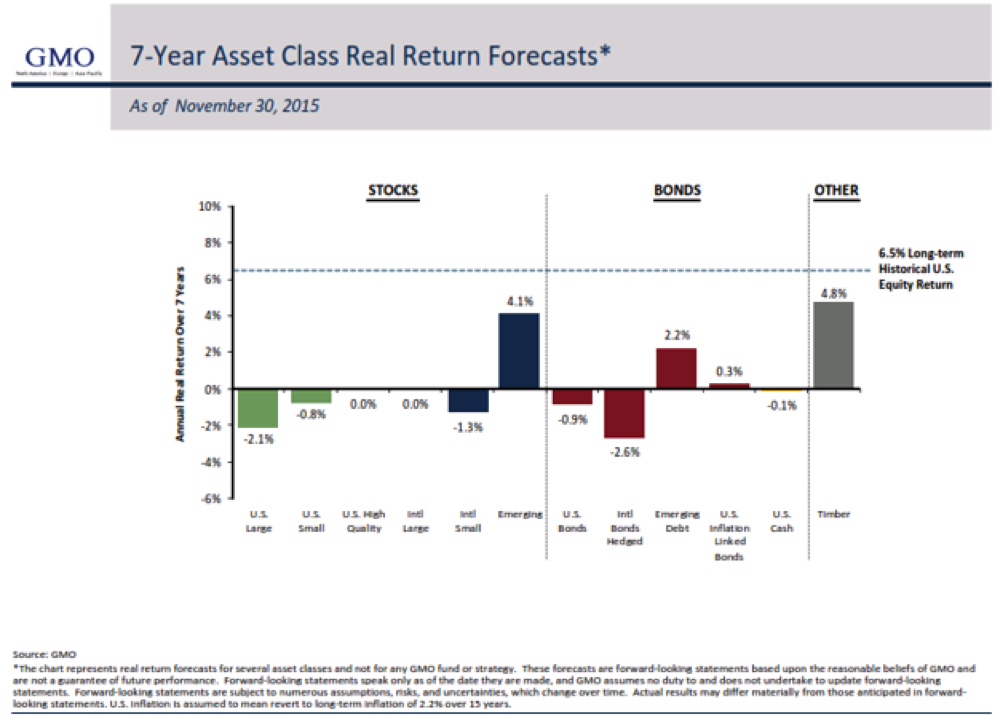

Jeremy Grantham’s firm GMO puts out a 7-Year real return forecast. Source

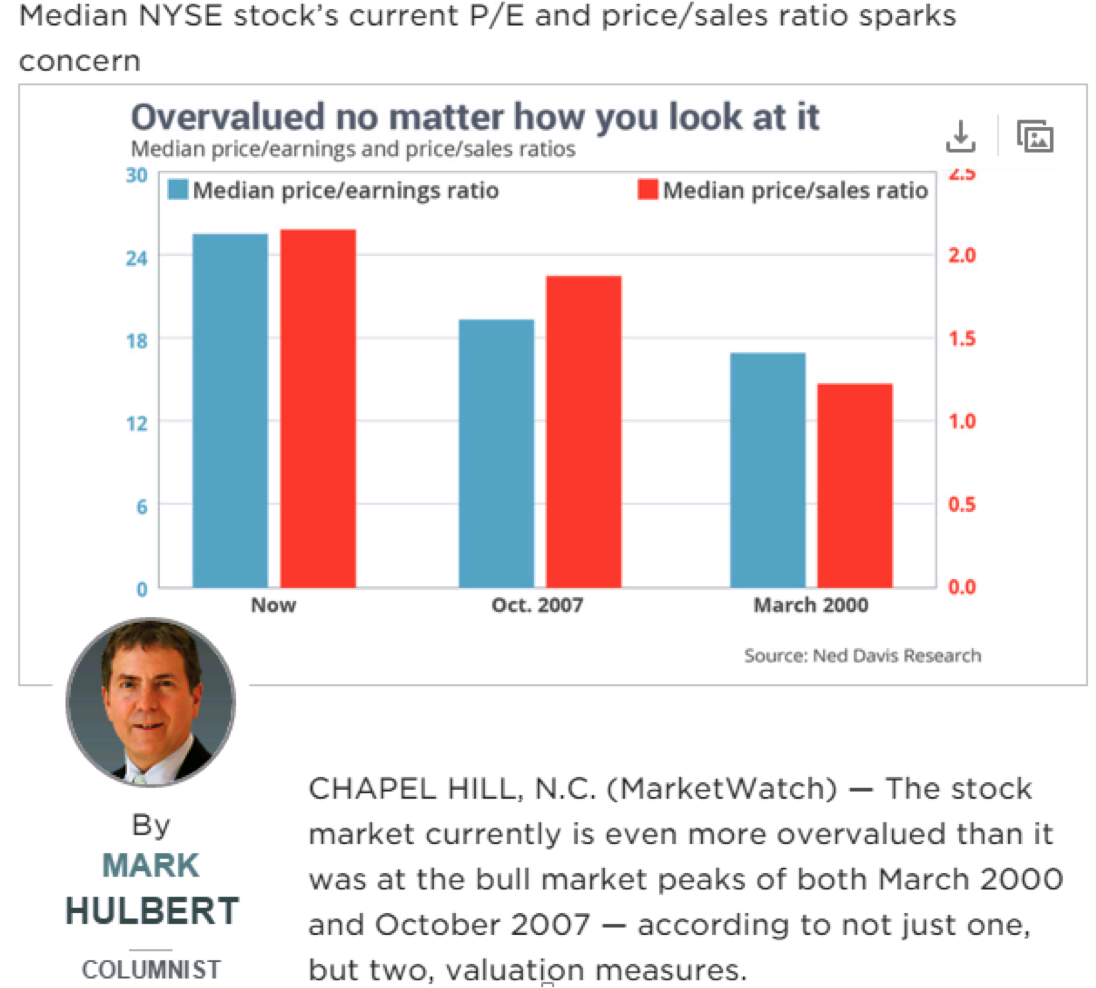

This from Market Watch – Stocks are more overvalued now than at the 2000 or 2007 peaks. Source

Further below are the most recent Trade Signals charts. Extreme Pessimism remains in place which is short-term bullish for the equity markets. The trend data is neutral at best.

Wishing you a happy, healthy and joy filled New Year! All the very best to you and yours, Steve

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Trade Signals – Extreme Pessimism is ST Bullish for Equities

- Concluding Thought – What You Can Do

Trade Signals – Extreme Pessimism is ST Bullish for Equities – 12-30-2015

Click here for the link to Trade Signals (updated charts and commentary).

Concluding Thought – What You Can Do

2015 has proven to be a challenging year for investment returns. Challenging for buy-and-hold, challenging for tactical, challenging for international equities, emerging markets equities, commodities, gold and most alternative strategies. Nonetheless, we have seen several liquid alternative strategies do well.

Most advisors we speak with are seeing client returns in the -2% to -5% range. Disappointing. Global 60/40 is in that same range (we’ll have all of the year-end comparative data soon).

I believe it is because equity valuations are too high and interest rates are too low. I also believe that the Fed is distorting price discovery creating a challenging environment for many managers. I believe risk remains high.

My Two Cents On What You Can Do Today

If you are broadly diversified in a way that includes a number of non-correlating return streams and your equity exposure is hedged, then my best advice is to stick with your game plan. I think it is time to play defense. This strategy should allow the power of compound interest to work in your favor over time. You may add or replace a particular risk here or there, but make sure it fits well in a way that meets your return and risk objectives.

Tamp down your return expectations and stay defensive, so that when the next correction causes equity valuations to once again become attractively priced, you can switch back to over-overweight equities. Stay patient until the forward return getting gets good.

If you chase into equities today (and it is tempting), you won’t have the ability to redeploy your capital to take advantage of the opportunities that will present.

Finally, I continue to favor the following weighting: 30% equites (hedged), 30% fixed income (tactically managed) and 40% liquid alternatives (tactical, managed futures, etc.).

I wrote a piece entitled, When “Beating the Market” Isn’t The Point. It is about broad portfolio diversification and attempts to answer the question you may get from your client(s): Why didn’t I beat the market (the Dow or the S&P 500 – to highly concentrated equity risks)? Feel free to share it with your client(s). You can find it here.

Personal note: I’m in Utah with Susan and the kids. It is so much fun to see our children bond together so well. The snow is soft and deep, the sun is just now rising and another fun day awaits.

Wishing you a very Happy New Year and continued great success!

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG White Paper Understanding Tactical Investment Strategies you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at@askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History: Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Provided are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out of the money covered calls and buying out of the money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out of the money put options for risk protection.

Please note the comments at the bottom of this Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group

© CMG Capital Management Group