10 Undervalued Dividend Champions For 2016: Be Greedy When Others Are Fearful

Introduction

Dividend Champions/Aristocrats are the go-to dividend paying stocks for prudent investors desirous of a safe, predictable and growing stream of income on the common stock portion of their retirement portfolios. As most investors are aware, in order to be classified as a Dividend Champion/Aristocrat a company must meet the stern test of consecutively increasing their dividend for 25 years or longer. Of all the dividend paying stocks in the universe, only a select few make these prestigious lists.

However, the popularity of Dividend Champions/Aristocrats often presents a conundrum to value-oriented dividend growth investors. These best-of-breed dividend paying stalwarts are rare to find at attractive or prudent valuations. Nevertheless, since I am a fervent believer that you make your money on the buy side, high quality and an impeccable dividend record are not enough for me.

Before I am willing to invest in any company, Dividend Champion/Aristocrat or not, the company must be available at a prudent and attractive valuation. Of the more than 50 Dividend Aristocrats, and more than 100 Dividend Champions, I only found 10 that I considered currently attractive based on valuation.

Price Is What You Pay - Value Is What You Get

In December 2010, I started a series of articles where I presented the principles of valuation. Since I believe that principles of valuation are timeless, I offer the following excerpts from that series in order to revisit some of the more important principles, benefits and aspects of investing at fair value.

In part 1 of that three-part series I presented the important principle that distinguishes the difference between price and value:

“Price Is What You Pay. Value Is What You Get.

The venerable investor Warren Buffett has a real knack of putting complex concepts and ideas into simple and easily understood terms. In my opinion, his quote, "Price is what you pay. Value is what you get" is one of the more profound and important statements he has ever uttered. If truly understood, these simple words represent perhaps some of the most important bits of investment wisdom that an investor could ever receive.

The concept of value represents the key to receiving the full benefit that these wise words provide. Knowing the price you pay is simple and straightforward. And, although many have an intuitive understanding of value, its deeper meaning is often only vaguely comprehended. Anyone who has truly made the effort to study Warren Buffett's investment philosophy understands that receiving value on the money he invests is of high importance to him.

So how do you know, when buying a stock, if you're getting value or not for your money? I contend that the answer lies in the amount of cash flow (earnings) that the business you purchase is capable of generating on your behalf. And regardless of how much cash flow the business can generate for you, its value to you will be greatly impacted by the price you pay to obtain it. If you pay too much you get very little value, but if you pay too little then the value you receive is greatly increased.

Therefore, if value is what you're looking for, then it's important that your attention be placed on the potential cash flows that you're expecting to receive. Unfortunately, few investors possess the presence of mind to focus on this critical element. Instead, investor attention is more commonly and intensely placed on stock price and its movement. A rising stock price is usually considered to be good, and a falling stock price considered bad.”

At this point, I would like to focus the reader on an important subtlety about valuation that I alluded to in the above excerpt. Notice that I discussed cash flows, but also made a reference to earnings. As I will illustrate later, earnings are an important valuation metric, because in the long run earnings drive stock price, which is the source of capital appreciation. However, when investing in dividend paying stocks, cash flows are equally if not more important because they represent a company’s ability to cover their dividends. Moreover, there are certain companies where the correlation between cash flow and stock price is more distinct than the correlation between earnings and stock price.

Dividend payout ratios are typically expressed as a percentage of earnings. However, they can also be expressed as a percentage of cash flows. Additionally, the reader should also recognize that a company’s cash flow per share will normally be higher than its earnings per share when examining a high-quality company producing consistency with both metrics. Consequently, many best-of-breed dividend paying stalwarts command a premium valuation based on earnings, but will appear more attractively valued based on cash flows. This important point will be elaborated on later in the article.

Nevertheless, in part 2 of the 3 part series I wrote in 2010 I discussed the utilization of the P/E ratio as a first step in the valuation process. In the following excerpt, I discussed the relevance of a P/E ratio of 15 as a reasonable first blush valuation level, its limitations, and I also again alluded to the notion that certain companies routinely command premium valuations above that benchmark level.

“In Part 1, I also offered the idea that a P/E ratio of 15 was appropriate for companies whose growth rates fell in the range of 0% to 15%. In other words, in addition to the fact that the P/E ratio of 15 has been the average for indices like the S&P 500, there is also a logical and mathematical reality behind its validity. However, although a P/E ratio of 15 was an appropriate valuation to pay for growth of up to 15%, I also pointed out that it did not necessarily indicate the rate of return investors should expect to receive.

Also, the 15 P/E ratio should not be looked at as an absolute, instead it should be viewed as a baseline barometer for fair value. In other words, the 15 P/E is a good starting point guideline to ensure that you are not overpaying and taking too much risk. Consequently, anytime you come across a moderately growing company (5%-15%), whether a blue-chip or even a moderate to high dividend payer that is trading at a P/E ratio above 15 then caution is called for. However, there are certain companies that will always command a premium valuation.”

In part 3 of my series on the principles of valuation I discussed the key, as well as the importance that valuation plays regarding the avoidance of making obvious mistakes.

“In this, my 12th and final installment of my series of articles on when and why to buy a stock, I will focus on how to use the principles of valuation to avoid obvious mistakes. As mentioned in previous articles, investing is never a game of perfect. The best that an investor can hope for is to make sound long-term decisions, with the majority of them working out to their benefit in the end.

However, investing is a very complex endeavor, and mistakes are inevitable. Therefore, it's imperative that the obvious mistakes which can and should be avoided are avoided.

Obviously, mistakes usually occur when the market or people are caught up in emotion. As we all know, the primary emotional responses that can affect investor behavior are fear and greed. When gripped by the hype from greed or by the hysteria from fear, investors rarely behave rationally. It is during times like these when stock prices can become disconnected from True Worth™ valuations. This undeniable fact that stock values are not always rational needs to be recognized and accepted.

In my opinion, one of the primary reasons why investors often make bad investment decisions is because their judgment is usually based only on price movement. Price movements alone can be very misleading. A rising stock price will often lull an investor to sleep creating a false sense of security where they believe that all is well.

On the other hand, a falling stock price usually creates anxiety and sometimes leads to outright panic. These feelings can be rational as long as they are justified by sound fundamentals. Knowing the differences between rational and emotional reactions will make all the difference.”

10 Fairly Valued Dividend Aristocrats/Champions Based On Earnings

As I screened the list of Dividend Champions presented by fellow seeking alpha author David Fish and the Dividend Aristocrats compiled and presented by S&P Capital IQ, I was only able to come up with 10 names that I felt were fairly valued based on earnings. Part of this relates to normal premium valuation applied to these names discussed above, and part of this relates to the popularity of these dividend paying stalwarts. To be clear, many of these premier dividend paying companies are currently being valued far in excess of even the normal premium valuations they have commanded in the past.

What Are You Investing For?

Every individual investor does not have the same investment goals, needs or investment objectives. Some investors are concerned with beating the market, others are concerned with maximum safety over the highest return, and others are concerned with maximizing their income and the growth thereof. In addition to these objectives there are numerous variations and combinations that each unique individual investor is concerned with. Consequently, I believe one of the most important questions that every investor - in common stocks especially - should ask and answer for themselves before investing is: what am I investing for?

This question may seem simplistic to some, but I consider it one of the most vitally important questions an investor should ask and answer. The reason I say this is because it speaks to the reality that there are trade-offs in investments. As a general rule, and there are always exceptions to every rule, higher yield often implies lower capital appreciation, and vice versa.

Therefore, if for example, your investment objective is maximum current yield, you must generally be willing to accept a lower rate of capital appreciation in order to achieve that goal. If that’s not true, then it might also apply that you taking on significantly more risk than you should be or are comfortable with. Of course, the opposite also applies. If you are looking for maximum capital appreciation or total return, you will typically not find it with the highest yielding securities.

High total return is a function of growth, and growth hungry companies are typically starved for capital to fund that growth. Consequently, they tend to retain more earnings and pay out less to shareholders in the form of dividends. In contrast, a more mature company looking to simply establish or maintain moderate growth, might not have use for all of their capital (cash flow), and therefore, pay out more earnings in order to attract shareholders through higher yield.

With the above in mind, I have presented my 10 fairly valued Dividend Champion/Aristocrats in order of highest yield to lowest. Additionally, future total returns will also be functionally related to the level of valuation that a company can be purchased at. Lower valuations can lead to higher future returns generated by P/E expansion as a result of a reversion to the mean. Consequently, if valuation is low enough, which could also be the source of an above-average current yield, this can result in high or above-average future returns that can be accomplished even through investing in lower growth entities.

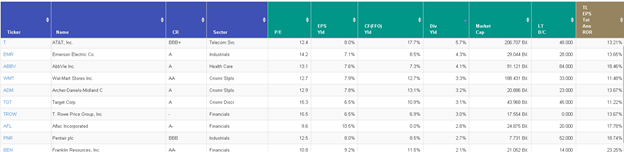

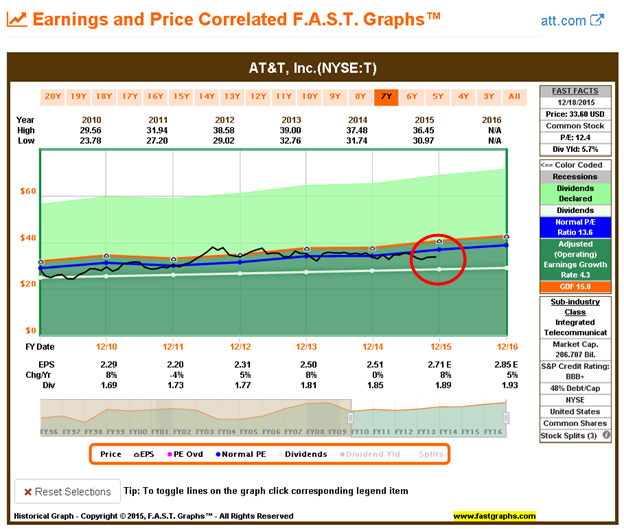

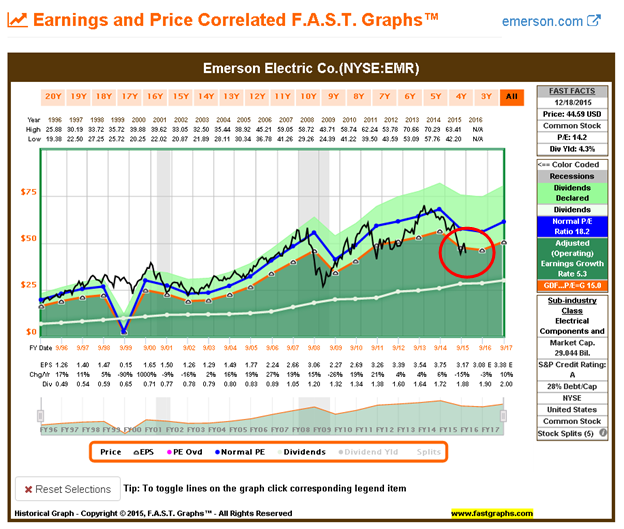

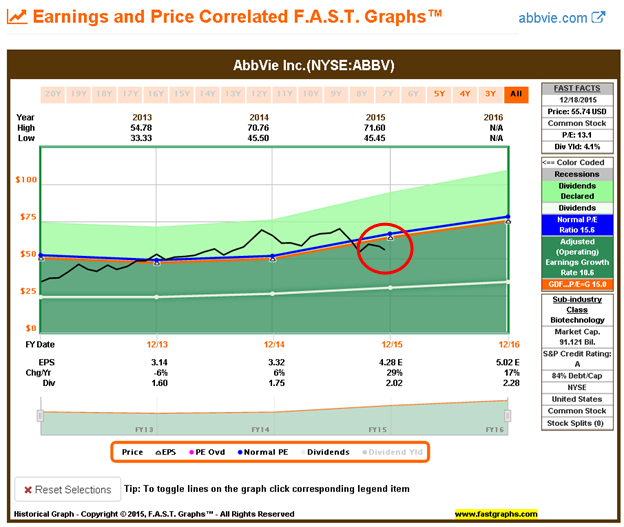

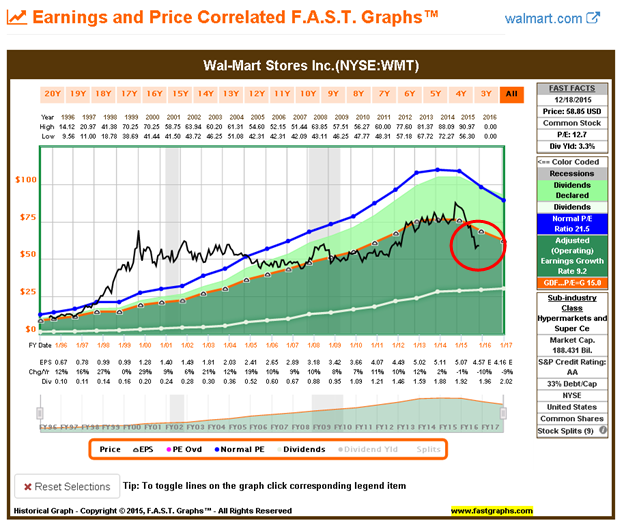

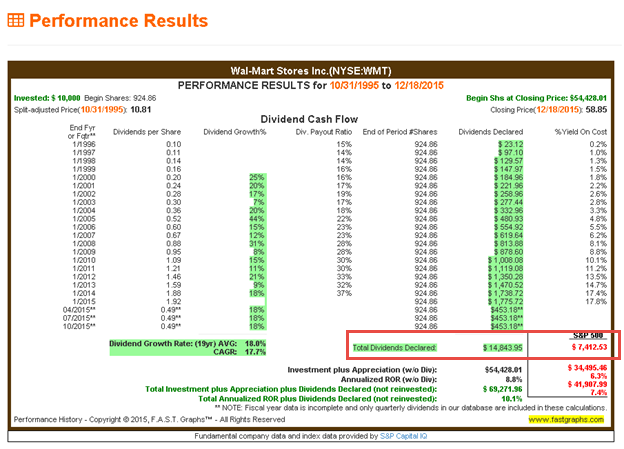

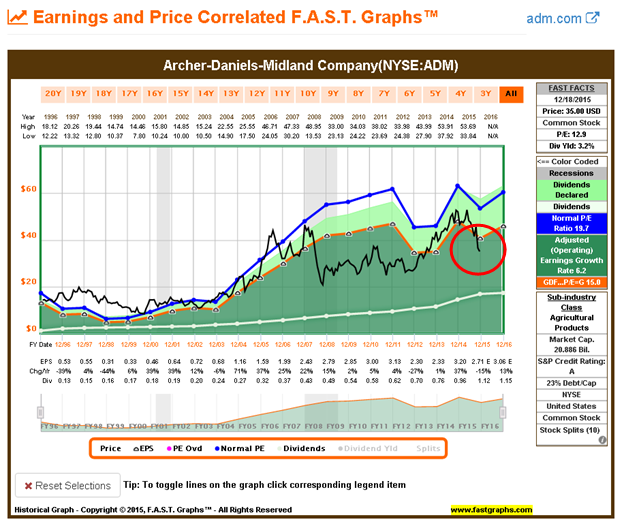

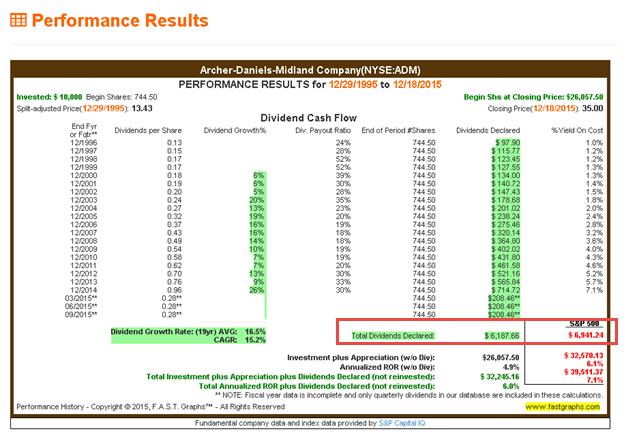

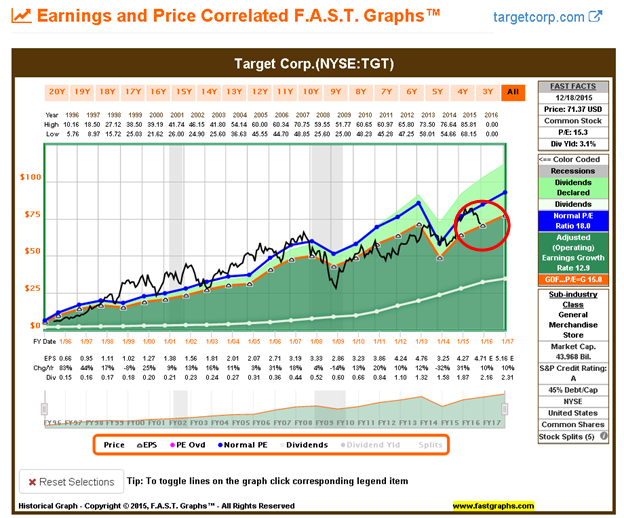

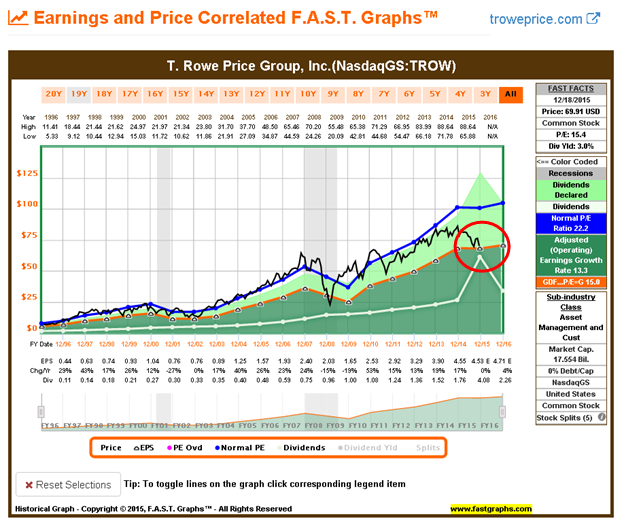

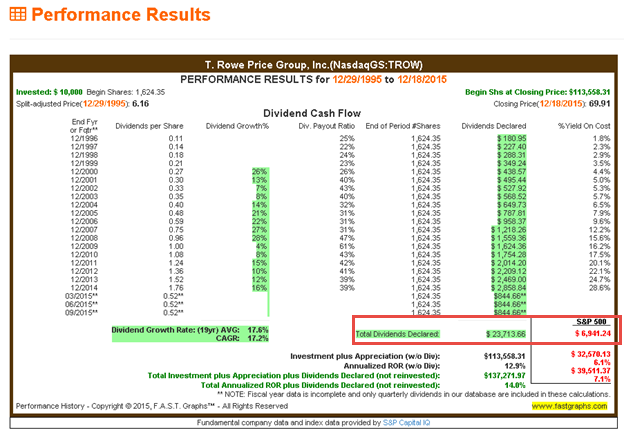

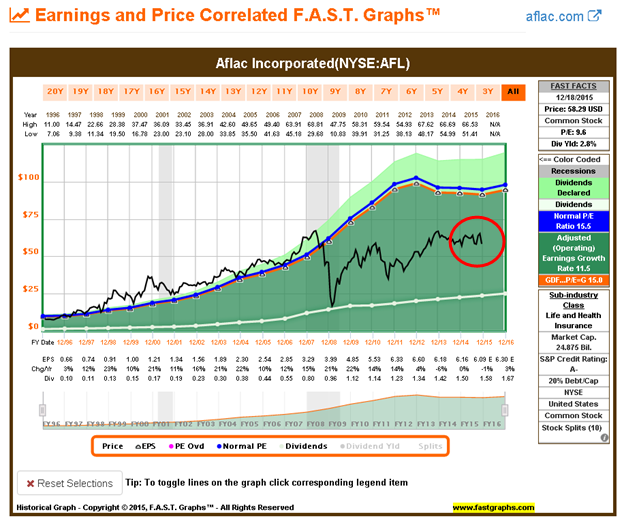

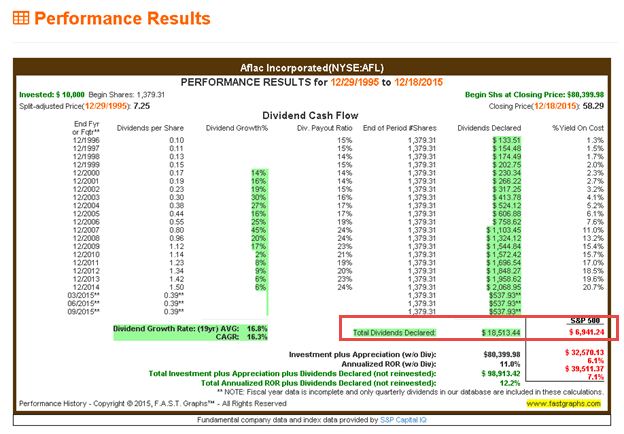

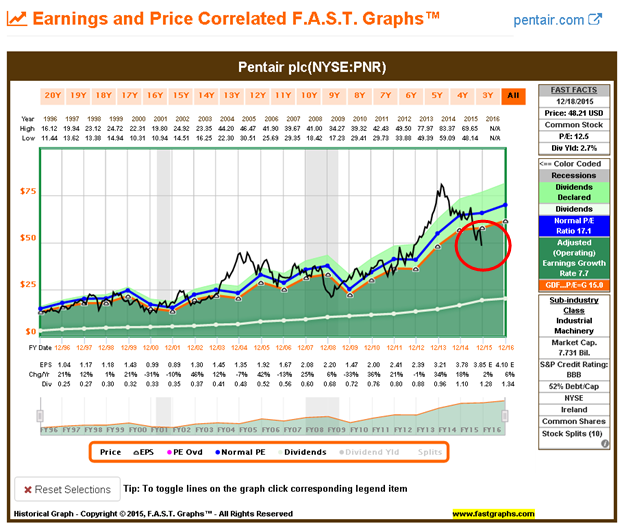

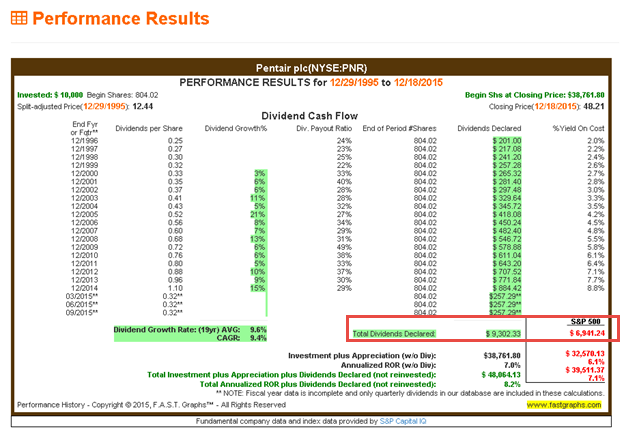

The following F.A.S.T. Graphs™ portfolio review lists my top 10 attractively valued Dividend Champion/Aristocrats based on earnings for 2016. Following the portfolio review, I will present individual earnings and price correlated F.A.S.T. Graphs™ plus performance reports on each company. On the earnings and price correlated graph, focus on price relative to the orange earnings valuation reference line. On the performance reports, note that total cumulative income versus the S&P 500. When appropriate I have utilized 20 calendar year graphs. However, on AT&T and AbbVie specifically I have utilized short of timeframes as appropriate.

AT&T, Inc. (T)

Emerson Electric Company (EMR)

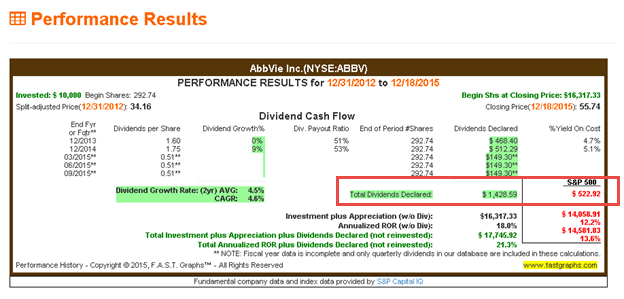

AbbVie Inc. (ABBV)

Wal-Mart stores Inc. (WMT)

Archer- Daniels- Midland Company (ADM)

Target Corp. (TGT)

T. Rowe Price Group, Inc. (TROW)

AFLAC Incorporated (AFL)

Pentair plc (PNR)

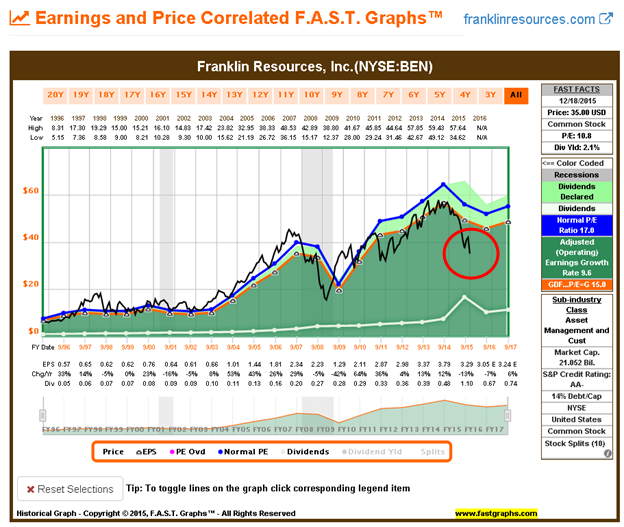

Franklin Resources, Inc. (BEN)

Bonus: 5 Stalwarts Fairly Valued Based On Cash Flows

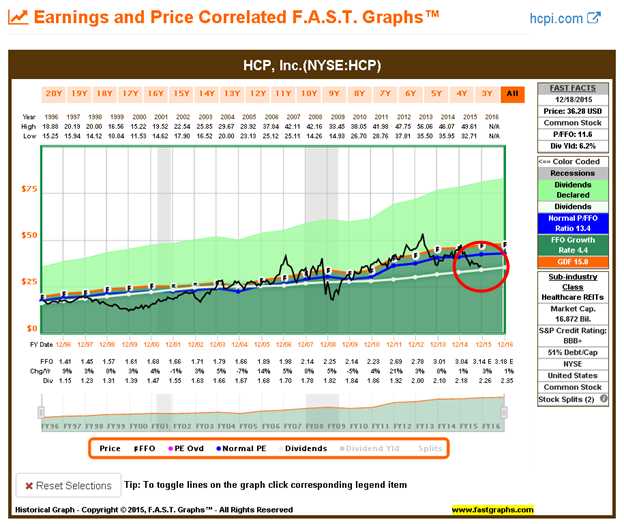

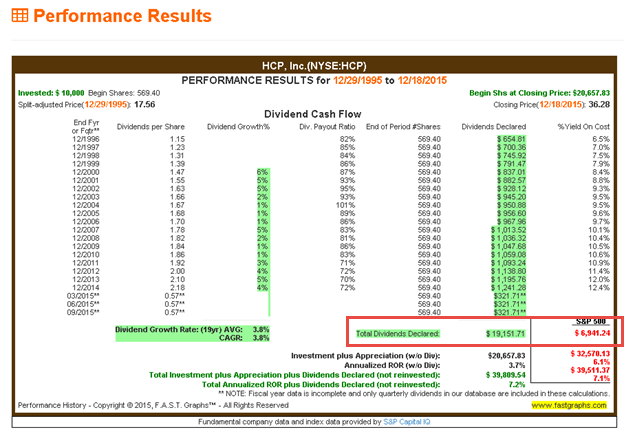

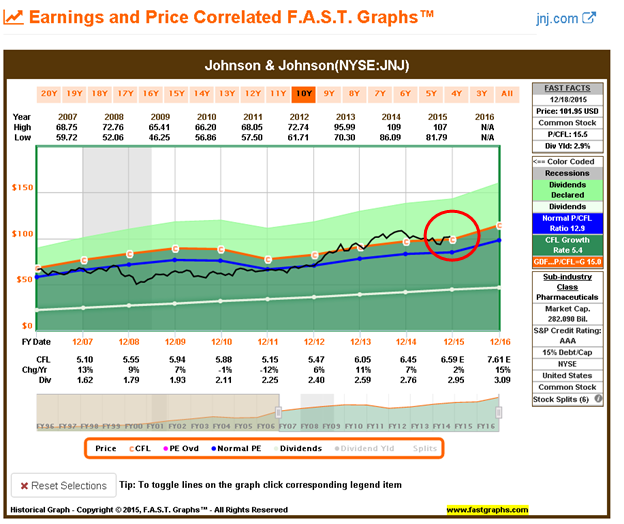

These 5 bonus companies are quintessential examples of highly-rated blue-chips that often commands a premium valuation based on earnings. However, since these examples are most appealing based on safety and dividend yield, I am offering valuation graphs based on price and cash flow. Of course, HCP is a REIT, and therefore, appropriately valued based on funds from operations.

HCP, Inc. (HCP)

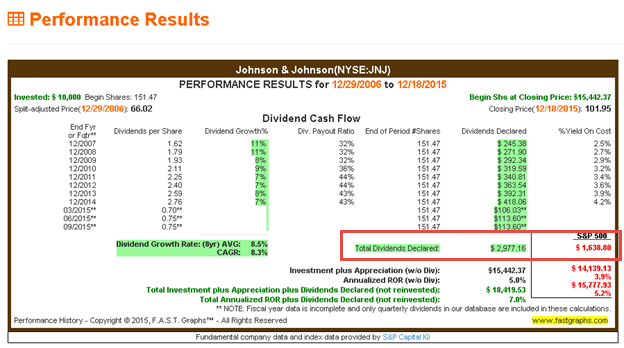

Johnson & Johnson (JNJ)

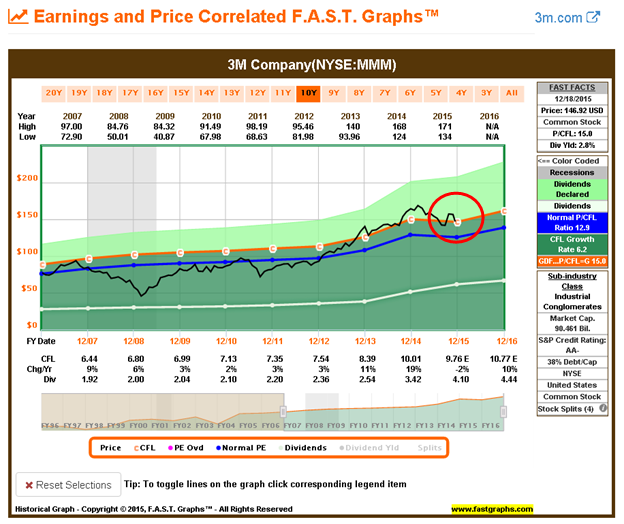

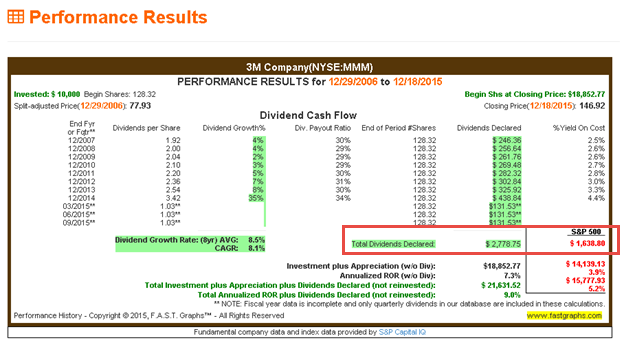

3M Company (MMM)

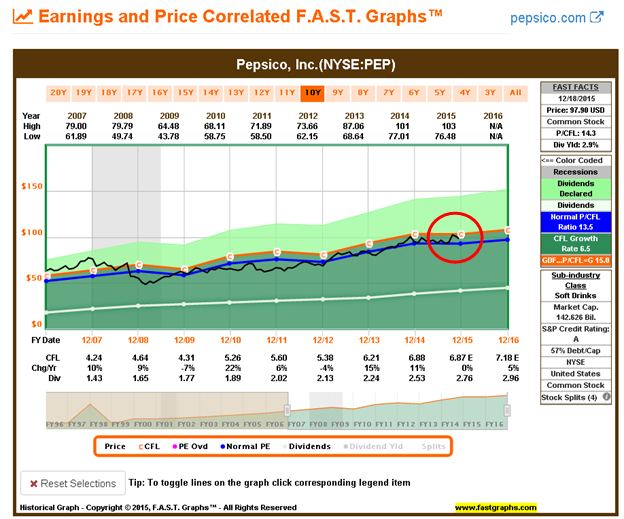

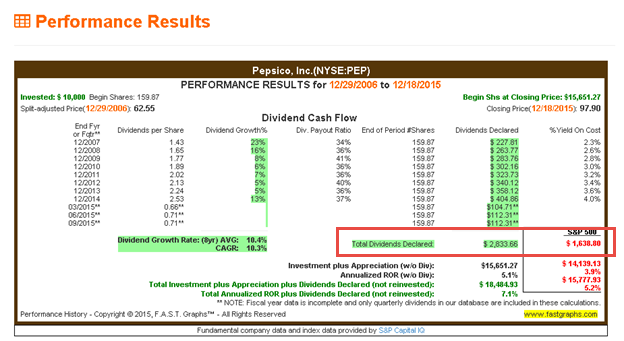

PepsiCo, Inc. (PEP)

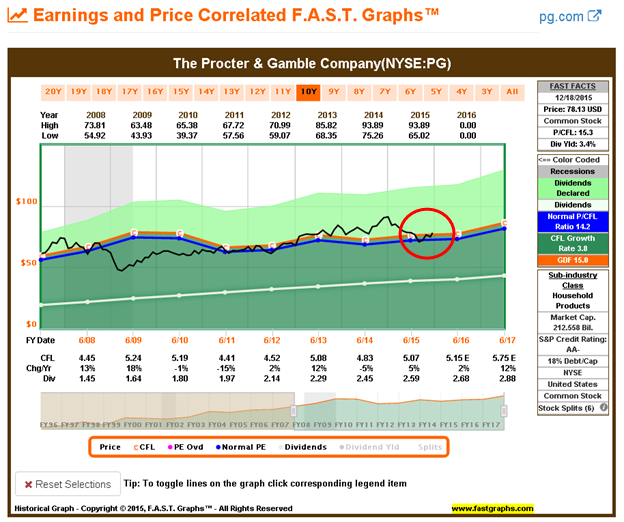

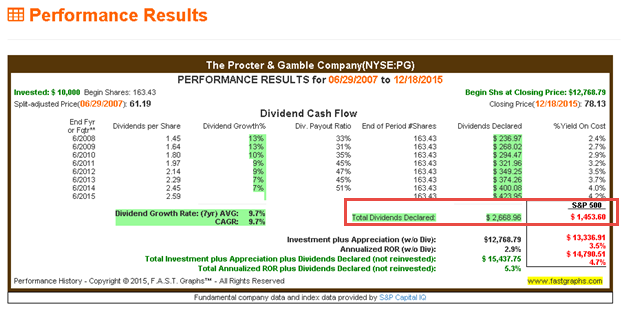

Procter & Gamble (PG)

Summary and Conclusions

I want to be clear that these are not necessarily my favorite or what I consider best valued dividend growth stocks. Instead, these are specifically what I consider the best or most fairly and attractively-valued Dividend Aristocrats or Dividend Champions. Each of these companies has increased their dividends for 25 consecutive years or longer. Therefore, they all fall into the elite group of dividend growth stocks with long histories and legacies of dividend growth.

Consequently, I offer these 10 Dividend Aristocrats and Champions, and the 5 bonus selections based on cash flow for consideration by those investors most concerned with safety and dividend growth. In other words, these are not necessarily companies that will produce above-average long-term total returns.

On the other hand, I believe each of these companies represent a high level of safety and the opportunity to produce above-average current dividend income and long-term dividend growth. Therefore, these suggestions are offered for those investors desirous of achieving the highest long-term total accumulated amounts of dividend income from safe blue-chip dividend paying stocks.

Disclosure: Long PEP,PG,AFL,T,EMR,ABBV,WMT,TGT,JNJ,HCP

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.