Credit spreads, which measure the relationship between bonds of different credit ratings, are arguably one of the most overlooked tools in financial market analysis. That is a shame because reversals in the momentum of credit spreads offer reliable signals of changes in the fortunes of bonds, stocks and commodities. Current evidence suggests some of these relationships have reached a critical juncture point, which means further deterioration in junk bonds and their connection with higher quality ones could lead to a crisis prone 2016. Alternatively, a fundamental improvement in these relationships, as junk bonds pull back from the brink, would signal an improving economy, equity and commodity markets. In this respect, it is perhaps ironic that mini-crises, such as that developing in the area of credit challenged bonds, would normally elicit easing from the Fed, yet instead the central bank has decided to raise rates!

The Contrarian Aspect

To set the scene, there have been several prominent articles in the financial press concerning the drop in junk bond prices. In addition, the Third Avenue junk bond fund recently halted redemptions to enable management to liquidate its portfolio in an orderly fashion. This very unusual step, combined with the plethora of articles, is more typical of the terminal phase of a trend than its initiation. The possibility that junk bonds have already hit their lows is therefore a very real possibility. After all, the theory of contrary opinion tells us when everyone understands the argument, there is no one left to sell. Ergo, the prevailing trend is more likely to reverse than continue. Let us hope so, because Chart 1 shows that, if we exclude the financial crisis, Moody’s BAA corporate yield has violated its secular downtrend. The 2013 high has not yet been surpassed, but a rising not yet extended momentum curve in the lower panel argues that it might soon. The chart is telling us that these rates are going up, but the way in which they rise is far more important. For example, a general rise in rates, at least initially, would signal a healthy economy. Higher yields due to fears of widespread defaults would be another matter.

Chart 1 Moody’s BAA Corporate Bond Yields

Long-term trendline violations are usually followed by a long-term move in yields

More to the point, the relationship between such bonds and higher quality treasuries has proved to be an excellent canary in the financial coal mine for the economy, bond yields, equities and commodities. The basic concept compares the yield of a poorer quality credit instrument with that of a higher quality one. When investors are confident they push up the prices of riskier higher yielding paper. This is echoed in a recovering economy, together with higher bond yields, equity and commodity prices. When bond investors show a strong preference for treasuries this caution is usually associated with a reversal in these financial market trends.

Credit Spreads and the Bond Market

Chart 2 compares the yield on Moody’s Corporate AAA bond yield to that of a momentum measure of the ratio between Moody’s BAA corporate bonds and 10-year treasuries. We use the BAA series due to the fact that it has a longer history than junk bond ETF’s or indexes. Also, momentum, rather than the ratio’s raw data, is employed because it is more subject to cyclical swings and tends to trade in definable bands. BAA rated paper is not considered to be junk, rather a lower quality investment grade. Even so, this relationship reflects swings in bond market confidence quite accurately. The principal message is that reversals in the spread favoring BAA bond prices indicate a growing investor confidence in the economy, as witnessed by the fact that such action is usually followed by higher rates. Upside reversals are signaled when the ratio crosses above its 6-month MA from a sub-zero position. Such instances have been identified with the solid vertical green lines. The dashed ones indicate where such crossovers were not followed by a rise in rates. Relating the red highlighted recessions to the vertical lines indicates that credit spread momentum has a strong tendency to reverse during the very early stages of the recovery. Other reversals, not marked by a recession such as 1966, are typically followed by a resumption of growth, which is also followed by higher corporate bond yields.

Chart 2 Moody’s AAA Bond Yields versus Credit Spread Momentum

Sub-zero reversals in credit spread momentum are usually followed by an improving economy and higher bond yields

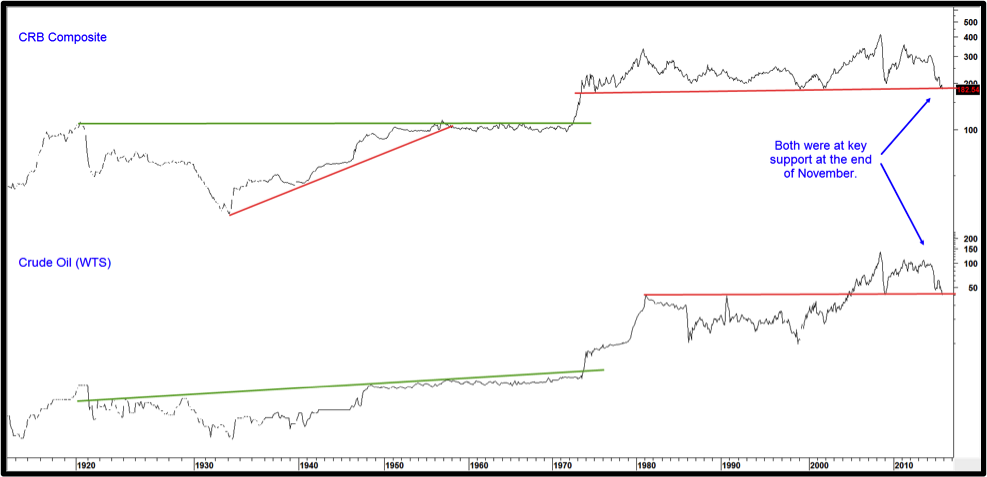

This relationship is currently quite overextended on the downside, so it would not be unreasonable to expect a reversal, but there is one important caveat. Chart 3 shows that at the end of November the CRB Composite (182.5) was right at a 40-year support trendline; so was the price of West Texas Crude ($39.75). Since then both series have extended their declines to 171 and $36, respectively. It is important to note that this is a monthly chart which requires a month end close. Current prices are an “estimate” therefore, and do not officially count. Even so, early December price erosion does underscore the current precarious technical nature of the commodity markets. The relevance to our discussion is the fact that resource based bond issues, have been leading junk bond prices lower because of their questionable credit rating. Commodity weakness, if it continues, will exacerbate the problem, suggesting that the final bottom for the spreads featured in Chart 6 may lie ahead. If that proves to be the case, it would likely mean lower rates for top quality debt instruments.

Chart 3 CRB Composite and Oil Prices

Long-term trendline violations are usually followed by large price moves

Quality Spreads and the Equity Market

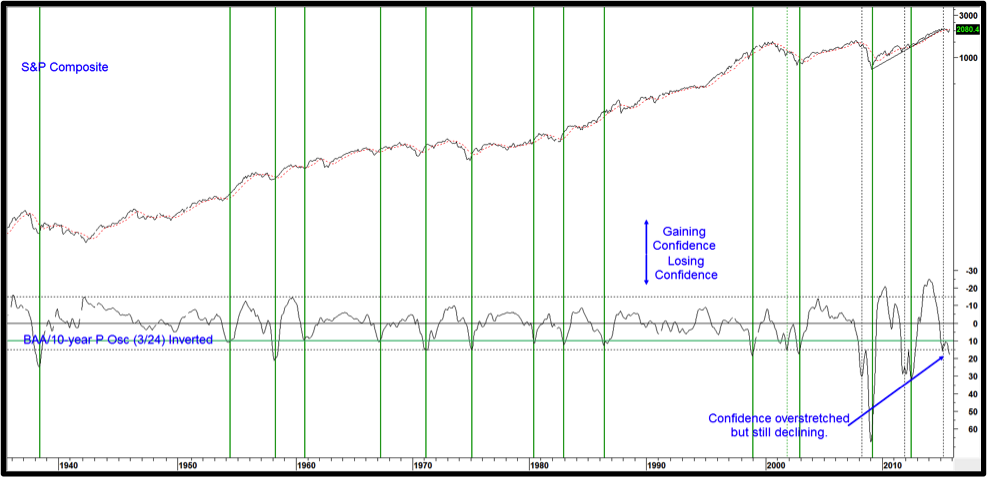

Chart 4 shows the momentum of this same relationship, but this time it is being compared to the S&P Composite. In this instance the vertical lines indicate reversals from at or below the -10% green horizontal line. Solid lines again represent success and dashed ones false positives. Note that pretty well every time this series reverses to the upside it signals a great buying opportunity for equities.

Two of the four false signals developed when the S&P was below its 12-month MA and the other two in 2011 and early 2015 were quickly reversed. Currently, the indicator is moving lower so this model is bearish.

Chart 4 Equity prices Versus Credit Market Spread Momentum

When quality spread momentum reverses to the upside it’s usually positive for equities

Quality Spreads and Commodities

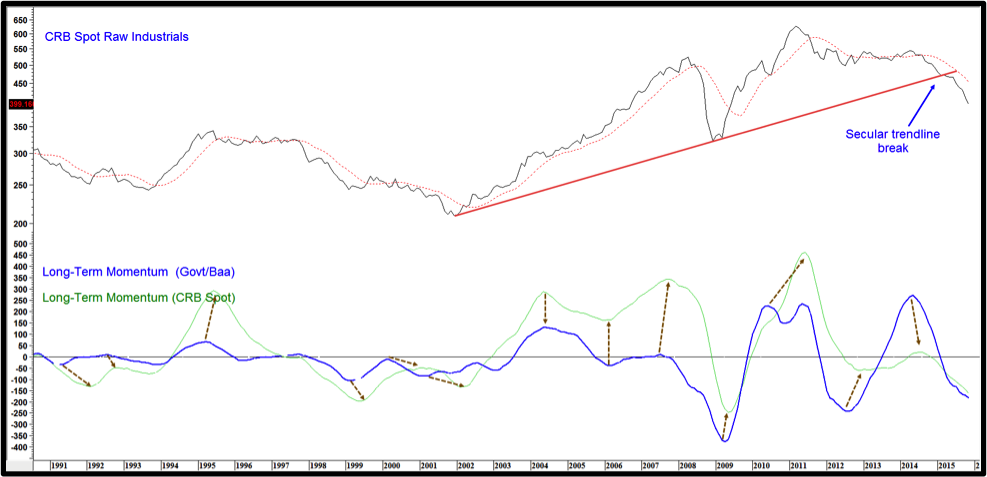

Because quality spreads are tied to the economy their momentum also acts as a leading indicator for bull and bear price movements in industrial commodity prices. Chart 5 compares the CRB Spot Raw Industrials with their long-term momentum and that for the spread between the Moody’s BAA yields, but this time using the 20-year government series. The brown arrows indicate that (blue) bond market momentum has a strong, but not perfect, habit of turning ahead of (green) commodity velocity. Right now both are declining, so neither is signaling that commodities have bottomed.

Chart 5 Commodity Prices versus Credit Spread Momentum

Reversals in credit spread momentum usually lead commodity prices

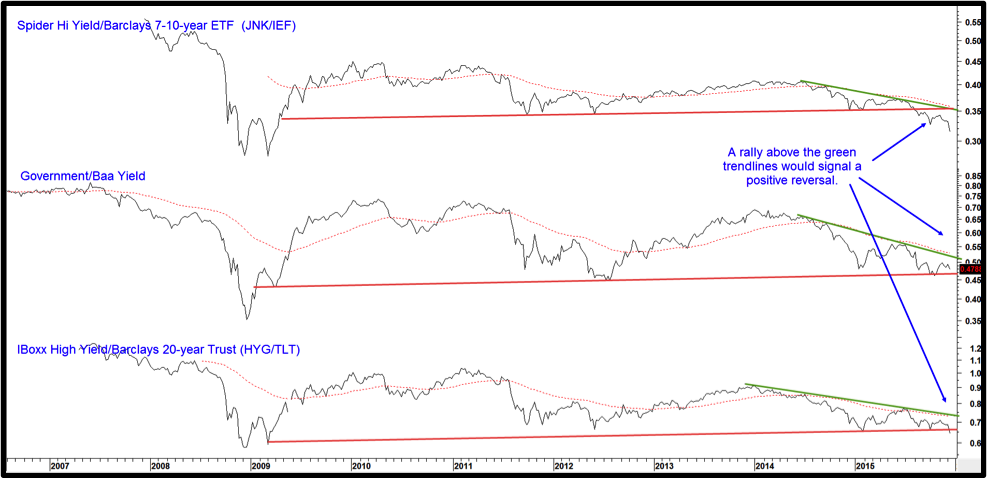

Quality Spreads at a Crucial Technical Juncture

Chart 6 shows three more measures of bond market confidence, this time featuring the actual relationships as opposed to their momentum. Each one is either approaching or cutting through very important support in the form of the three horizontal trendlines. More serious violations of those support zones would signal that further deterioration lay ahead. In that event, these “canaries” would indicate a weaker economy, lower equity prices and higher long-dated treasuries.

On the other hand, a successful assault on the three green trendlines and 65-week EMA’s would strongly indicate that financial markets were moving away from crisis mode towards a more optimistic one. That is because a set of rising ratios would represent bond market sentiment voting for a stronger economy, higher equity and commodity prices. Using Friday close prices that would occur with a JNK/IEF reading in excess of .36 and a HYG/TLT level above .76. Such action would decisively violate the trendlines and cross above the 65-week EMA.

Until then, the song being sung by our canaries is a very cautious one.

Chart 6 Three Credit Spreads

Credit spreads near critical juncture points

Martin Pring is Chairman of Pring Turner Capital (Pringturner.com) and editor of the Intermarket Review (Pring.com)