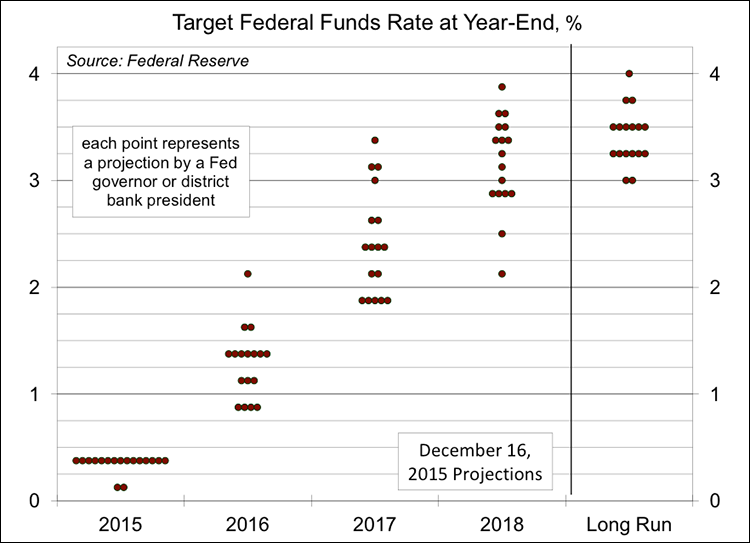

The Federal Reserve has now raised short-term interest rates for the first time in nine and a half years. In the policy statement, the Fed signaled that policy will still be accommodative, that future action will be data-dependent, and that the pace of rate increase is likely to be gradual. None of that should be a surprise. The more important message was in the dot plot (senior Fed officials’ forecasts of the appropriate federal funds target rate at the end of each of the next few years). There is still a range of opinion among Fed officials, but there is considerably less dispersion than in September.

The Federal Open Market Committee voted 10-0 to raise the target range for the federal funds rate by a quarter percent, to 0.25-0.50%, citing “considerable improvement” in the labor market, an expectation that inflation (as measured by the PCE Price Index) will move back toward the 2% goal, and recognition that it takes time for policy actions to affect the economy.

In a secondary statement on policy implementation, the Fed’s Board of Governors raised the interest rate paid on excess reserves held at the Fed (IOER) to 0.5% (the top end of the range for the federal funds rate). The BOG also approved a request from 10 of the 12 district banks to raise the discount rate (the primary credit rate) by a quarter percent, to 1%. The FOMC directed the New York Fed trading desk to peg the overnight reverse repo at 0.25% (the bottom of the range for the federal funds rate) as needed. The Fed’s reinvestment policy remains (rolling over maturing Treasury securities at auction and reinvesting principal payments on agency debt and mortgage-backed securities in mortgage-backed securities).

At every other Fed policy meeting, senior Fed officials (the governors and the district bank presidents) submit forecasts of growth, unemployment, and inflation. December projections were very similar to those made in September.

In recent quarters, the dots in the dot plot have varied widely, suggesting no consensus on the likely path of short-term interest rates – and if there’s no general agreement among monetary policymakers, what hope is there for a clear view for financial market participants? December’s dot plot still shows differences of opinion, but the 2016 dots are now more tightly bunched. Of the 17 Fed officials (not all of whom get to vote on policy), seven expect another 100 basis points in rate increases over the course of 2016 – or 25 basis points at every other Fed policy meeting. Seven expect less than that (two or three rate increases in 2016). Financial market participants should therefore view 100 basis points as the base-case scenario for 2016 (with rate increases most likely in March, June, September, and December), with some chance that the Fed will be less aggressive (two or three hikes, instead of four). Currently, the yields on 1-year and 2-year Treasury securities imply a somewhat lower glide path that the 100 bps/year scenario.

Of course, the Fed can move faster or slower depending on the economic data. The focus will be on the labor market and inflation – and this is still where senior Fed officials’ opinions differ. How much slack remains in the job market? How much of an increase will we see in wage growth? Do firms have pricing power (the ability to pass higher wage costs along)?

The Fed’s median forecast for 2016 GDP growth was 2.4%, apparently reflecting the recent themes of domestic strength and global softness. If growth remains strong and the job market continues to improve, the Fed should stay on the 100 bps/year path. That’s not necessarily bad for the stock market. After all, the economy would be improving. If growth slows and the job market improvement cools down, Fed policy will be on a lower path, but that would not necessarily by good for the stock market. Yet, while the Fed policy outlook is still uncertain, there’s a lot less uncertainty than there was a few months ago.