Last week, we looked at the Fed’s various policy tools and how the central bank will use them. This week, let’s examine the implications of a Fed rate hike. While a rate increase should be largely factored into the markets by now, the global reaction may be the largest concern for Fed officials.

First, it’s worth noting that a Fed rate hike this week is not a 100% certainty. Comments from most Fed officials suggest that there is broad agreement to begin tightening, but Yellen’s recent speech and testimony fell short of making a firm commitment. One thing that would lead the Fed to delay would be signs of significant financial instability. A Fed rate hike this week should not surprise anyone and a small move should not matter much in the overall scheme of things, but the financial markets have been skittish and overly concerned.

What would a rate hike mean for investors? Bank deposit rates normally lag the Fed on the way up. Don’t expect to earn a lot more on your savings and checking accounts. Bank credit is unlikely to tighten much. Long-term interest rates, including home mortgage rates, may edge up a little. Credit spreads have already widened, partly reflecting an unwinding of a stretch for yield, but shouldn’t widen much more.

There are two basic theories of stock market valuation. The first considers the stock price as a measure of the risk-adjusted discounted stream of expected future earnings. Higher interest rates mean greater discounting – and all else equal, share prices would fall. However, stronger economic growth (which is why the Fed is raising rates) would imply an increase in earnings. So, the impact on the stock market is unclear. If the Fed is perceived as “overdoing it,” and choking off future growth, that would be a negative for stock prices.

The second basic theory of stock market valuations is akin to how we value works of art. It’s simply what the next person is willing to pay. Don’t laugh. Sentiment and herding are factors known to drive share prices. This is why it’s important to consider technical analysis along with the fundamentals. The charts will pick up things not evident in the earnings outlook. Here, a Fed rate hike could lead to a sharp move in sentiment (or an over-reaction) even if the move was widely anticipated and would have little impact on the overall economic outlook.

There are a number of factors that determine exchange rates, but it always comes down to supply and demand. In the short run (six months or less), it’s largely about central bank policy. Tighter monetary policy here and easier monetary policy abroad implies (all else equal) a stronger greenback. The key question is how much is already baked into the market. Further strength in the dollar puts downward pressure on commodity prices, which helps keep overall consumer price inflation low.

The impact of a strong dollar on import prices is mixed. The Bureau of Labor Statistic data show substantial declines in in prices of raw materials over the last year and a half. However, prices of imported consumer goods have not fallen nearly as much. Since the end of 2013, the euro is down around 20% against the dollar – but if you go to a BMW or Mercedes dealership, you’re not going to see many bargains. That’s because consumer prices are driven locally, not globally (in contrast to commodity prices). The Fed knows this.

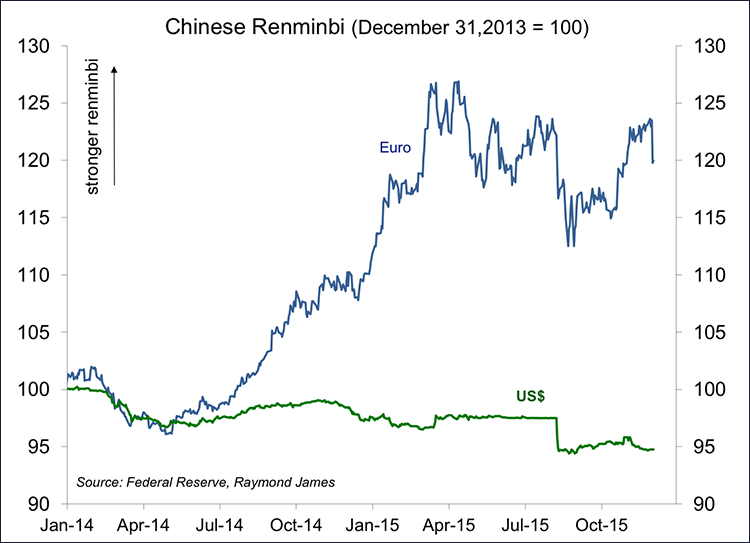

Last week, the China Foreign Exchange Trade System (CFETS), an arm of the People’s Bank of China (the country’s central bank) began publishing an exchange rate index. The purpose, according to the CFETS, was to turn the currency market focus away from RMB/US$. The new index measures the renminbi (RMB) against a basket of currencies, similar to indices in use by other central banks. The Chinese currency has been tied mostly to the U.S. dollar. As the dollar has appreciated against most major currencies, so too has the renminbi. Pressures have been building to devalue. To prevent that from happening, the PBOC has been burning through its currency reserves. That can’t go on forever. Hence, the announcement of this new exchange rate index is seen as paving the way for a gradual depreciation. None of this has anything to do with the IMF’s decision to include the renminbi in its benchmark basket.

Now here’s where things get interesting. The increased globalization of finance means that cross-country capital flows can now be very large and quick. That means conditions are inherently more unstable. Capital outflows lead to currency weakness, which can hasten further outflows, leading to further pressure on the currency. Eventually, things will go too far and it will become more attractive for the capital to move the other way. This may be the biggest worry as the Fed gets set to tighten, and it may give some officials reason to pause.