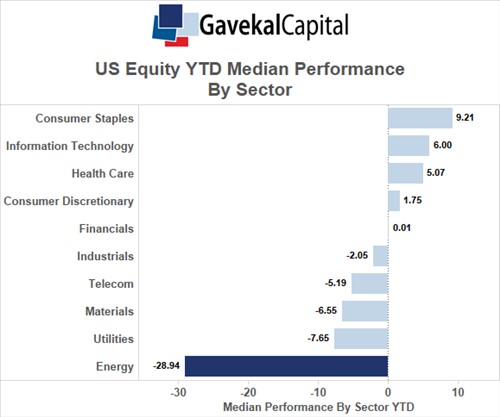

It’s not breaking news to say its been a bad year for energy stocks but it might be breaking news that not all energy stocks are trading at cheap valuations. In the United States, the median energy stock is down nearly 29% (the average energy stock is down about 23%). As this first chart shows, energy has clearly been the worst sector by a wide margin.

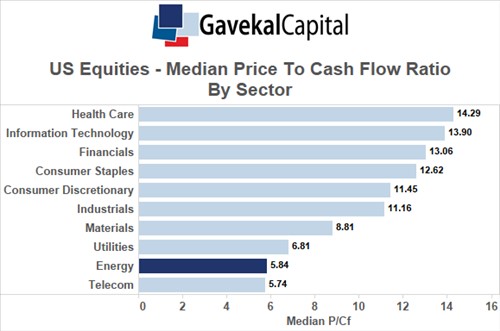

Given the slide in commodity prices and energy stocks, one would expect to see some compelling valuations emerge. Overall, the energy sector has the second lowest median valuations of any sector in the US. Telecom takes the prize for having the lowest price to cash flow ratio (5.7x), just nudging out energy (5.8x). Health care continues to have most expensive price to cash flow valuations in the United States (14.3x).

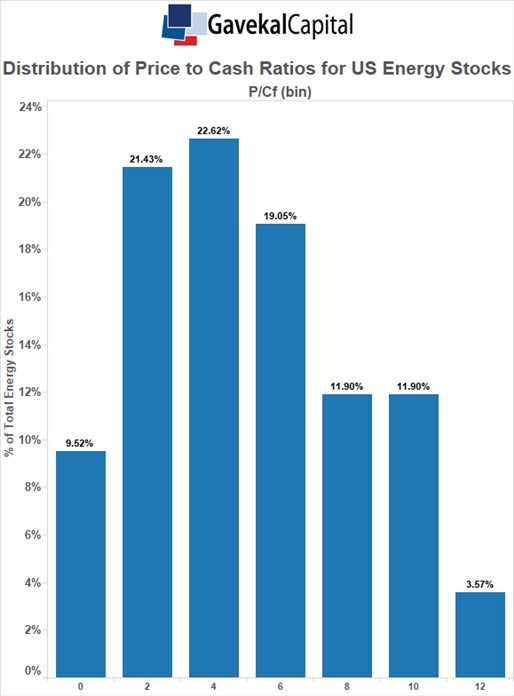

It’s interesting, however, to see that not all energy stocks are trading at rock bottom prices. In the chart below we break out energy stocks into groups based on its price to cash flow ratio. We then plot the groups in a chart to see what the distribution of energy valuations looks like. For example, we can see that 9.5% of all energy stocks (8 stocks in all) have price to cash flow ratios between 0-1.99x. The greatest concentration of stocks have price to cash flow ratios between 4-5.99x. 63% of all US energy stocks are trading between 2x-7.99x cash flow. However, over 27% of energy stocks are trading above 8x cash flow still.

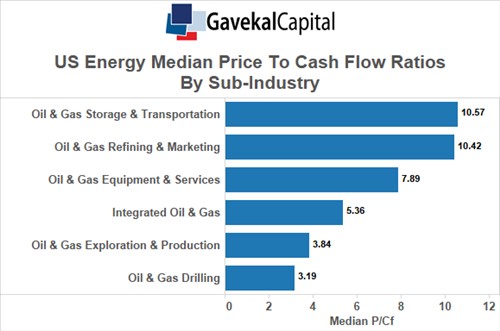

If we slice the data one step further and break the energy sector up into sub-industries, we get a better understanding of energy valuations. Nearly half of all energy stocks fall within the oil & gas exploration & production sub-industry. Valuations in this sub-industry have fallen substantially as the median valuation in this group is just 3.8x cash flow. However, valuations in the oil & gas storage & transportation and the oil & gas refining & marketing sub-industries remain buyout as the median valuations in these two sub-industries remain over 10x cash flow. This isn’t an inconsequential group of companies either as these two sub-industries are nearly a quarter of all energy stocks.