It’s anticipated that the Fed will begin tightening monetary policy soon, but many investors may be unfamiliar with how policy will be tightened. Let’s review the key policy tools and how this tightening cycle will differ from previous cycles.

There are normally seven Federal Reserve governors in Washington (there are five currently, with two nominees stuck in the Senate). There are 12 Fed district banks; each has a president. The Federal Open Market Committee (FOMC) is made up of the governors, the New York Fed president, and four of the other district bank presidents (who rotate on or off the committee each January). All senior Fed officials participate in monetary policy meetings, but only the FOMC members vote.

Banks are required to hold a portion of deposits in reserve. The reserve requirement ratio depends on the size of the institution and thresholds are recalculated annually. The reserve requirement rate is an important policy tool for many central banks around the world, but the U.S. Federal Reserve no longer uses it as an active monetary policy lever.

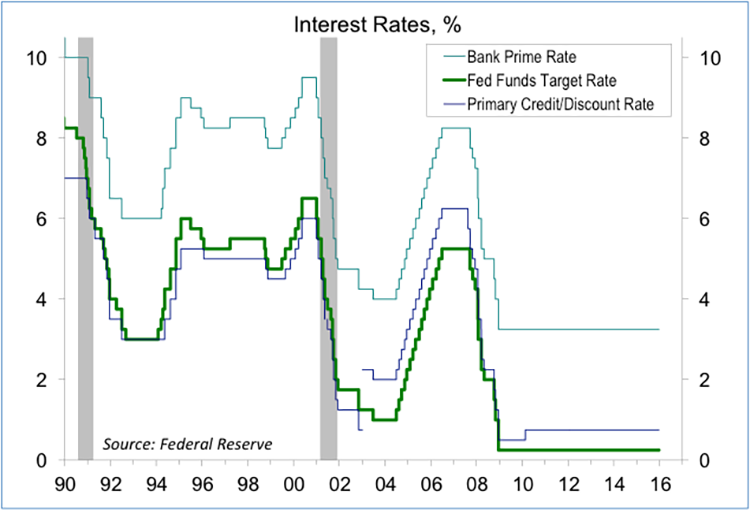

At the end of the day, banks may have excess reserves, which can be lent overnight to banks that have reserves below their requirement. The overnight borrowing cost is the federal funds rate. It is a market-determined rate, which the Fed tries to peg by buying and selling Treasury securities (these are called “open market operations” – hence, the name “Federal Open Market Committee”). Prior to 1994, the Fed did not announce changes to the federal funds rate. In October 2008, the Fed shifted from a federal funds target rate to a target range (currently, 0-0.25%). When the Fed begins to tighten monetary policy, it will now announce a higher target range (for example, 0.25-0.50%).

In October 2008, the Fed was granted the ability to pay interest on excess bank reserves held at the Fed. The rate paid by the Fed (IOER) is currently 0.25% and, as the Fed tightens, it will define the upper end of the federal funds target range.

The Fed intends to use overnight reverse repos to help define the lower end of the federal funds target range, but expects that to be temporary and will phase it out when no longer needed.

The Primary Credit Rate is the rate the Fed charges banks for short-term borrowing. This used to be called (and is still sometimes called) “the discount rate.” A bank may have a seasonal need for extra cash (for example, planting season in a farming community). The rate used to be lower than the federal funds target rate (hence, the “discount”), but there was some stigma attached to such borrowing (banks did not want to be perceived as possibly “in trouble”). Raising the rate above the federal funds rate removed that stigma. Prior to 1994, the discount rate was seen as the primary tool for monetary policy (as changes to the federal funds rate were not announced).

Now here’s where people often get confused. The federal funds target range is determined by a vote of the FOMC. The primary credit rate (currently 0.75%) is set by the Fed’s Board of Governors, but only following a request by one or more of the Fed district banks. The Board of Governors meets ahead of each FOMC meeting to consider requests to change the primary credit rate. Usually, if the FOMC votes to raise the federal funds rate target, the Fed’s Board of Governors will also raise the primary credit rate. Note that ahead of the FOMC meeting in late October, 9 of the 12 Federal Reserve banks had requested an increase in the primary credit rate (currently 0.75%). Two wanted no change. Minneapolis wanted a cut.

The Fed’s Large-Scale Asset Purchase program (LSAP, more commonly referred to as “quantitative easing” or “QE”) led to a significant expansion in the Fed’s balance sheet. Currently, to keep the size of the balance sheet steady, the Fed is reinvesting principal payments in its portfolio. At some point after the first increase in short-term rates, the Fed will end the reinvestment policy. The size of the balance sheet will then decline naturally as securities (Treasury and mortgage-backed) mature. It will probably take about 10 years to bring the balance sheet back to an appropriate level. There are some technical issues, such as keeping the mix of maturities in the portfolio unchanged – hence we are likely to see the Fed buying and selling Treasury securities as the balance sheet shrinks. The Fed has no intention of selling mortgage-backed securities.

For many months, Fed officials have indicated that the pace of policy tightening is much more important than the timing of the initial move. In recent comments, Fed Chair Janet Yellen has emphasized that 1) monetary policy will still be accommodative after the initial increase in short-term rates, 2) future policy moves will be data-dependent, and 3) economic conditions are expected to evolve in such a way as to warrant a gradual pace of rate increases over the next couple of years.