IN THIS ISSUE:

1. Deflation is Spreading Around the World – Why?

2. Wholesale Prices Make Deflation Look Even Worse

3. The Global Collapse in Commodities Prices Continues

4. Fed Intent on Raising Rates at December 15-16 Meeting

Deflation is Spreading Around the World – Why?

Consumer prices are running well below the 2% inflation target of central banks across the developed world. While central bankers continue to say they expect inflation to return to 2% or thereabouts in the medium-term, there is no evidence of that.

In fact, consumer price inflation is running at an annual pace of just 0.2% in the US, Germany, France, Italy and Japan. Whereas Spain, Switzerland, Sweden, Singapore, Poland, Finland and others are all experiencing deflation.

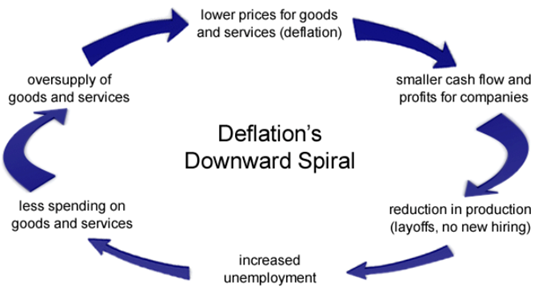

Deflation is defined as a general decline in prices, which sometimes is due to new technologies or innovations that cause prices to fall. More often, however, deflation is caused by a reduction in the supply of money or credit, or by a decrease in government, consumer or business spending and investment. With prices falling, consumers and companies have an incentive to delay purchases and investment, hoping to get an even lower price later on.

The opposite of inflation, deflation has the side-effect of increased unemployment since there is a lower level of demand in the economy, which can lead to a recession or depression. Central banks attempt to prevent severe deflation in an effort to keep significant drops in prices to a minimum.

Declining prices, if they persist, can create a vicious spiral of negatives such as falling profits, factory closures, shrinking employment and incomes and increasing defaults on loans by companies and individuals. To counter deflation, the Fed can use monetary policy to increase the money supply and deliberately induce rising prices – although that is not working well in the current cycle of falling inflation.

Deflationary periods can be either short or long, relatively speaking. Japan, for example, had a period of deflation lasting over two decades starting in the early 1990's. The Japanese government lowered interest rates to zero and printed lots of money to try and stimulate inflation, to no avail. Deflation is dangerous because it can travel across international borders.

Wholesale Prices Make Deflation Look Even Worse

The discussion above was regarding consumer price inflation. If we look at wholesale prices (Producer Price Index), the picture is even more troubling. Germany just reported that producer prices fell by 2.3% in the year ended October, the fastest pace of decline since 2010. Prices for factory goods in China are falling rapidly too, dropping by just under 6% in October, compared to the prior year.

Since China is the world’s largest exporter, that means it’s exporting those falling prices around the world. This means that significant deflationary pressures are pushing their way into the global production pipeline. And even the US Producer Price Index was down 1.6% year-over-year in October.

Most Americans pay little attention to wholesale prices and merely watch the Consumer Price Index. Ditto for many investors. As a result, many are not aware that deflation is alive and well in the US, despite the fact that this trend began back in 2012. Here’s another look at the US:

The disturbing chart above is one the Fed policy Committee should study carefully before voting to raise interest rates at the December meeting (more on that below).

The Global Collapse in Commodities Prices Continues

Speaking of charts the Fed should look at before hiking the Fed Funds rate, here’s another one. Commodities prices have been tanking since April of last year. While the collapse in oil and gasoline prices has been the main influence over the last year and a half, most other commodities have taken a beating as well.

The World Bank recently released its latest Commodity Markets Outlook, a quarterly update on the state of the international commodities markets. The report noted:

“We see a five-year-long slide in most commodity prices continuing in the third quarter of 2015. There are sufficient inventories of oil and other commodities and demand is weak, especially for industrial commodities, which is why prices may stay persistently low.”

Here are some of the highlights of the Report:

- The Energy Price Index tumbled 17 percent in the third quarter of 2015 from the previous three-month period, led by a renewed plunge in oil prices prompted by expectations of slower global growth, particularly in China and other emerging markets, abundant supplies, and prospects of higher Iranian exports next year.

- Industrial metals prices fell 12 percent in Q3, the fourth consecutive quarterly decline, reflecting slowing demand, notably from China. The World Bank projects metals prices to fall by 16 percent in 2015.

- Precious metals prices fell 7 percent in Q3 and are likely to slide another 8 percent in 2015 on lower investment demand.

- Agricultural commodity prices fell by more than 2 percent in the quarter and are likely to fall by 13 percent in 2015, reflecting abundant supplies and high levels of existing grain stocks.

- Fertilizer prices fell 1 percent in Q3, and may decline by 1 percent in 2015, because of weak demand, and rising supply.

The bottom line is that commodity prices in general are down more than 30% over the last year, and the World Bank does not believe that the bear market is over. Historically, broad-based commodity routs are not a good sign for the global economy.

Fed Intent on Raising Rates at December 15-16 Meeting

The minutes from the Fed’s latest policy meeting in October were released last Wednesday and made it clear that a majority of the Fed Open Market Committee (FOMC) members favor raising the Fed Funds rate for the first time in almost a decade at the next meeting on December 15-16.

In normal times, deflationary pressures like this would call for looser monetary policy, not tightening as the Fed is expected to do next month, absent any major negative surprises. The Committee members, including Janet Yellen, need to take a serious look at the chart above!

There’s been a theory floating around the last several months that the Fed will only raise the Fed Funds rate one time, in this case on December 16, and then will not raise the rate again anytime soon. This so-called “one and done” theory that lets the Fed get “lift-off” done and over with might be appropriate, especially if the trend toward deflation continues.

Liftoff, of course, is the much-awaited first increase in short-term interest rates since 2006. The US central bank took the key Fed Funds rate to near zero in late 2008.

The minutes from the October FOMC meeting made it clear last week that Chair Yellen has the votes necessary on the Committee to raise the Fed Funds rate on December 16, if she wants to. No doubt there will be a lot of speculation between now and then. The Fed Funds futures market now puts the odds of a rate hike on December 16 at 74%.

How to Dial Back Risk But Remain Fully Invested

Whether the Fed should finally begin to normalize interest rates in December or continue its zero-bound policy is a subject of great debate. There are convincing arguments on both sides. However, it is clear from reading the minutes from the most recent FOMC meeting that a majority of the voting members of the Committee believes that the Fed Funds rate should be increased at the December 15-16 policy meeting.

So here’s the question for investors: Is the first rate hike necessarily bearish for stocks?

It is clear that QE1, QE2, QE3 and zero-bound interest rates drove the equity and bond markets significantly higher since 2009. So, I have to assume that the upcoming period of higher interest rates and no bond buying by the Fed will weigh on both equities and bonds.

The next question is, by how much? Let’s take a look at a chart of the S&P 500 Index. Clearly, this market has struggled this year. While the S&P experienced a sharp downward correction in the fall of 2014, it managed to recover and surged to a new record highs in May/June.

Then came the massive drop in August. A drop of this severity should not happen in a healthy bull market. The market has failed to reach a new high and now has heavy overhead resistance, technically speaking. Will it manage to make a new high? Most buy-and-hold investors apparently think so.

You may recall that in March and April of this year, I recommended that investors reduce their long-only (buy-and-hold) exposure to equities. There were/are so many risks in the world, risks that I felt would weigh on stocks, and they did. My advice remains the same.

HAPPY THANKSGIVING EVERYONE!!

Thanksgiving is always an exciting time for me. The kids will be arriving on Wednesday. Other relatives will be coming as well, including my 97 year-old Mother-In-Law. We will be having turkey, ham, my cornbread dressing and all the trimmings. Most everyone will be staying until at least Saturday, and I love entertaining.

Like every year, I am most thankful for my family and all the blessings God has bestowed upon us. I am thankful for my loyal staff here at Halbert Wealth Management. And I am certainly thankful for the many clients we have all across the country! Without you there would be no need for this E-Letter or my blog.

May everyone reading this have a very Happy Thanksgiving!

Very best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.