“I have long made the claim that the transnational nature of Europe cannot be sustained. The divergent economic interests of EU countries, some with unemployment over 20 percent, some with it under 5 percent, meant that it was impossible for all of them to live not only under the same monetary regime, but under the same trade regime, which we cannot call free trade with agriculture, among other things, being protected. This would lead to a focus on national interest and on a resurrected nation-state.”

-George Friedman

Following up on last week’s piece highlighting the catastrophe of negative interest rates created by Central Bank Policy, I found myself thinking, as I’m sure you did too, a lot about the catastrophe in Paris. Outside of the dark vs. light human battle (of which I believe light will win), I gave thought to the potential unwinding of the great European Union experiment and what it might mean for our collective financial health. Coincidentally, a great geopolitical strategist piece crossed my desk this week. I share it with you below.

Maybe I’m obsessing over what I feel is transitory faith placed in global central bankers (the Fed, ECB, JCB) but I can’t help recalling Bernanke’s “Goldilocks” quote on February 14, 2007 (New York Times) and the happy no-doc mortgage days in 2007/08. The economy was not too hot, not too cold but just right. Right?

“Fear and euphoria are dominant forces, and fear is many multiples the size of euphoria. Bubbles go up very slowly as euphoria builds. Then fear hits, and it comes down very sharply. When I started to look at that, I was sort of intellectually shocked. Contagion is the critical phenomenon which causes the thing to fall apart.”

– Alan Greenspan

I felt a bit like Chicken Little in my writings back then. The “sky is falling” and all that sort of thing. Was the sky falling or was opportunity being created. It depends on your portfolio positioning at that time. It turned out to be a great opportunity if one was prepared. Wait and see what happens if Italy, Spain or Portugal pulls a Greek-like default move. Contagion being the “critical phenomenon”. I feel a little bit like Chicken Little again today.

In the book House of Cards, William Cohan exposed the corporate arrogance, power struggles and deadly combination of greed and inattention which led to the collapse of not only Bear Stearns and Lehman Brothers, but the very foundation of Wall Street. Despite Fed Chairs Greenspan and Bernanke’s inability to (admittedly) see the risks, there was abundant evidence that I and others wrote frequently about prior to the crisis. Though truthfully, in my wildest dreams, I didn’t imagine the entire financial system would come so near to collapse.

“Sort of intellectually shocked”? Gotta love his honesty.

One of the pieces I penned in late 2008 was titled “So Bad It’s Good”. It just didn’t feel good, emotionally, at the time. But with fear in heart and conviction in process, I took action and while I was a bit early, it turned out to be an exceptionally good trade. Then, yields on high yield bonds were close to 20%. That’s what I believe may present again in the not too distant future. Until then, it’s a process of participation, protection and patience.

At a recent conference, I was asked what I see as the biggest risks ahead. I answered that it is not subprime but everything that existed in 2008 from the perspective of debt levels, debt to GDP, margin balances and derivative exposure (and the related counter-party risks) is worse today than in 2008. Further, the Fed now finds itself painted into a corner with an inflated balanced sheet (QE asset purchases) and a zero interest rate policy.

So, I spoke of three big risks on the near horizon that may impact the equity and high yield markets and added that I feel like I did when I wrote about crazy high valuations in 1998 (“It’s not different this time” though I was two years too early) and in 2007 and 2008 (writing about subprime and leveraged derivative products).

All three risks have one common denominator – too much debt. Here are my big three:

- An approaching sovereign debt crisis in Europe

- An emerging market debt default cycle tied to a rising dollar and

- A coming high yield junk bond default wave of record proportion

Included in this week’s On My Radar:

- The Big Three

- The Resurrection of Old Europe

- Global Recession – Highly Probable

- A Few Equity Hedging Ideas

- Trade Signals – Excessive Optimism (ST Bearish)

The Big Three

Sovereign Debt Crisis: I believe a sovereign debt crisis will be tied to loss of confidence in government (and central bankers). That appears to be in motion. The debt to GDP ratios of the sovereign debt issuing countries are, in a word, unmanageable. Too much debt slows growth. Governments, absent the hoped for growth, raise taxes to cover increasing payables. Expect further slowing. We are in a debt deflationary cycle and the evidence, at least to me, is clear a global recession is probable if not already under way (see updated global recession watch chart below). Enter Draghi stage right. For now, it is kick the can. In the end, I believe some form of default/reorg of debt will be required.

EM Debt Crisis: With negative interest rates in Europe and the ECB talking more QE, while at the same time the U.S. exiting QE and looking to raise rates, it is advantage dollar. The balance of the developed world is in the same high debt induced low growth deflationary mess. They are all working off the same play book – devalue their currencies. Such would make their goods more attractive to foreign consumers. Advantage U.S. dollar.

However, it is the strong dollar that may trigger risk number two. Non-U.S. borrowers took out loans from dollar based lenders, then a low interest rate loan with belief that U.S. QE would further devalue the dollar. Borrow low and use their appreciated currency gains to reduce the amount of money in real terms needed to pay back. A win win.

However, just several years later, who would have imagined negative interest rates in Europe vs. higher interest rates in the U.S. More QE there vs. exit of QE here. A rising dollar means that $9.6 trillion in such loans may have to pay back $12 trillion (if the dollar rises another 20%) due to their bad dollar bet. Oops.

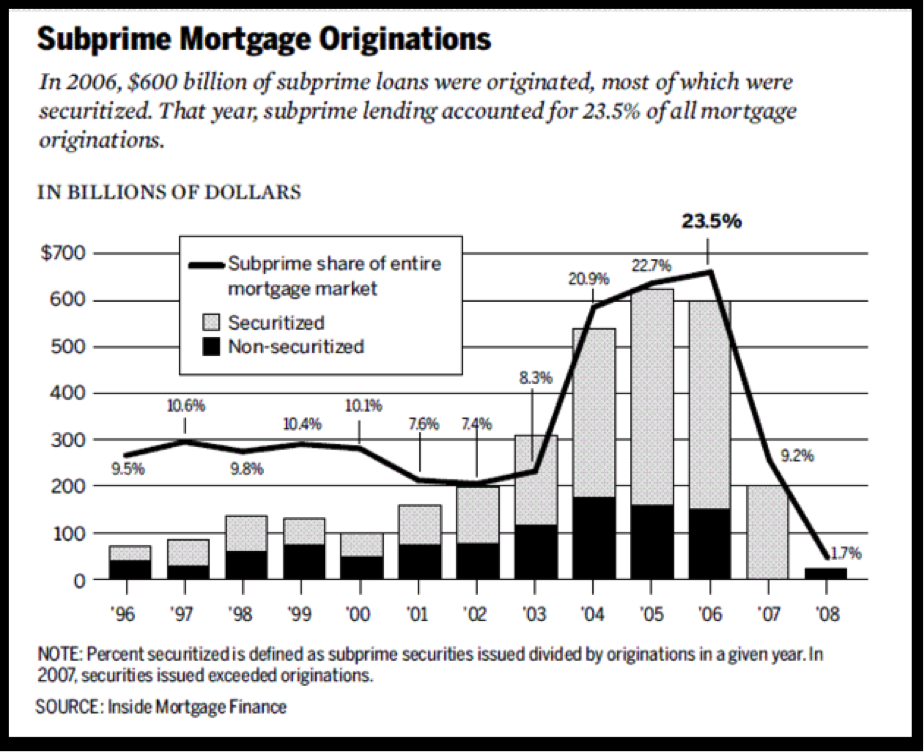

In comparison to subprime (call it $2 trillion at face value), this EM dollar denominated debt issue is no small issue. The next chart is a look at subprime origination pre-crisis. Roughly $1.8 trillion was originated between 2004-2007. The point I am trying to make is that $9.6 trillion is real money certainly relative to the size of the subprime crisis that tripped the blow-up wire in 2008. Big problem – number two is tied to EM dollar denominated debt. It is going to get trickier if the dollar continues upward. The Fed is painted into a corner.

High Yield Default Crisis: The third risk is tied to the $1 trillion in high yield debt issued in the last five years. The size of the high yield market is now $2 trillion. It took from the late 1970s and the early days of Michael Milken and Drexel Burnham to 2010 to grow to $1 trillion and just five years later it stands at $2 trillion.

Many companies received money that extended their life line. Investors chased into higher risk assets making that easy money available. Recession is probable in 2016 or 2017. Nearly $750 billion is set to mature over the next several years. Finding additional borrow will be difficult in recession. The lesser will default. Default rates will spike. Prices will decline. Yields will go higher.

Recession happen once or sometimes twice every decade. Watch the timing of recession and be prepared to take advantage the opportunity that will be created.

What happens when the good times end?

The 2008 crisis had severe, long-lasting consequences for the U.S. and European economies. The U.S. entered a deep recession, with nearly 9 million jobs lost during 2008 and 2009, roughly 6% of the workforce. One estimate of lost output from the crisis comes to “at least 40% of 2007 gross domestic product.” U.S. housing prices fell nearly 30% on average and the U.S. stock market fell approximately 50% by early 2009.

By early 2013, the U.S. stock market had recovered to its pre-crisis peak but housing prices remained near their low point and unemployment remained elevated. Economic growth has remained well below par. We are in a 2% growth world and not the 3.5% governments are hoping for.

Europe continues to struggle with elevated unemployment and severe banking impairments estimated at €940 billion between 2008 and 2012. With a heavy hand to the banks, it was hey boys, we want you to buy all the AAA rated Greek, Italian, Spanish, French bonds you can buy. Now, the ECB (QE) is trying to bail out the banks. Those banks are in trouble. Too much debt. The problem is far from over.

The big bubble today is in the bond market. Sovereign, EM and HY defaults. Keep a close eye on the recession probability models I share frequently in Trade Signals.

Of course, whatever I think I see, there is far more I do not see. It would be arrogant of me to think otherwise. This is a game of complexity, risk and risk management. I think the jig is up when confidence in government is lost. Melt up? It could happen though I don’t have high conviction. Thus, I sit in the own equities but “hedged” camp. Valuations are just not attractive so I favor 30% instead of 60% but note that this is just a conceptual thought and not a recommendation as I don’t know your risk level nor risk tolerance. And add a handful of liquid alternative return streams to your portfolio for enhanced diversification.

As a quick aside, if you haven’t had a chance to watch “How The Economic Machine Works” by Ray Dalio – click here. It’s awesome. Have your kids watch it too.

I mentioned that the timing of a sovereign debt crisis in Europe, in my belief, is tied to a loss of confidence in government. So let’s go there next.

George Friedman – The Resurrection of Old Europe

The following excerpt is from the great geopolitical strategist, George Friedman.

When I read the piece, I kept thinking about fractures and lost confidence in government. It is on my radar for reasons introduced above. I believe you’ll find Friedman to be a deep thinker.

The wave of immigration that has swept into Europe from the Islamic world in general, but particularly the more recent stream of refugees from Syria, has created a political crisis in Europe and one that was particularly raucous prior to October 1. Charges were being levelled by Germany against Central European countries for refusing to accept refugees. In turn, those countries charged that Germany was demanding that small countries transform their national character with the overwhelming numbers of refugees housed there. In addition, these countries, particularly Hungary, argued that among the genuine refugees there would be members of terrorist groups and that it was impossible to screen them out.

Had Europe been functioning as an integrated entity, a European security force would have been dispatched to Greece at the beginning of the migration, to impose whatever policy on which the EU had decided. Instead, there was no European policy, nor was there any force to support the Greeks, who clearly lacked the resources to handle the situation themselves. Instead, the major countries first condemned the Greeks for their failure, then the Macedonians as the crisis went north, then the Hungarians for building a fence, but not the Austrians who announced they would build a fence after the migrants left Hungary. Between the financial crisis and the refugee crisis, Europe had become increasingly fragmented. Decisions were being made by nation-sates themselves, with no one being in a position to speak for Europe, let alone decide for it.

I have long made the claim that the transnational nature of Europe cannot be sustained. The divergent economic interests of EU countries, some with unemployment over 20 percent, some with it under 5 percent, meant that it was impossible for all of them to live not only under the same monetary regime, but under the same trade regime, which we cannot call free trade with agriculture, among other things, being protected. This would lead to a focus on national interest and on a resurrected nation-state.

This was the fundamental problem of Europe and the migration crisis simply irritated the situation further, with some nation-states insisting that it was up to them to make decisions on refugees in their own interest. The response of Europe to the Paris attacks brought together all of these matters, and Europe only responded when some nations decided to use their national borders as walls to protect them from terrorists.

It is important to notice that this was not the EU creating checkpoints independent of national borders to trap terrorists or block them. The EU wasn’t built for that. Rather, it was the individual nation-states, reasserting their own rights and obligations to secure their own borders that acted. Despite all the rhetoric of a united Europe, the ultimate right of national sovereignty and the right of national self-defense was never removed.

Once it has been established that this implicit right can be used and the basic boundaries inside of Europe are the old European borders, we have entered a new Europe, or rather the old one. It is not clear when or if the border checkpoints will come down. After all, the war with the jihadists has created a permanent threat. Since there is no one to negotiate with, and no final blow that will end the war, when should the borders be opened again? What IS created, without intending it, is the fragmentation of Europe, with each state protecting itself. When will Europe decide it no longer needs checkpoints at the borders? When is it safe? And, if it is not safe, how do the borders come down?

You cannot control the movement of people without controlling the movement of goods. Whatever the rules at the moment, the nation-state has reasserted its right to determine what vehicles enter. Once that principle is in place, the foundation of Maastricht does not disappear. The agreement is still there, but the claim to ultimate authority is not in Brussels or Strasbourg, but in Madrid and Budapest and Berlin. This causes more than delays at the border, it essentially creates a new mindset.

This started as a counter to Russian and French airstrikes. It has culminated in unintended and unanticipated consequences, as is the norm. An airstrike in Syria, attacks in Paris, and the borders are back. Only to stop terrorists, of course. But that “of course” is dripping with historical irony. Source

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

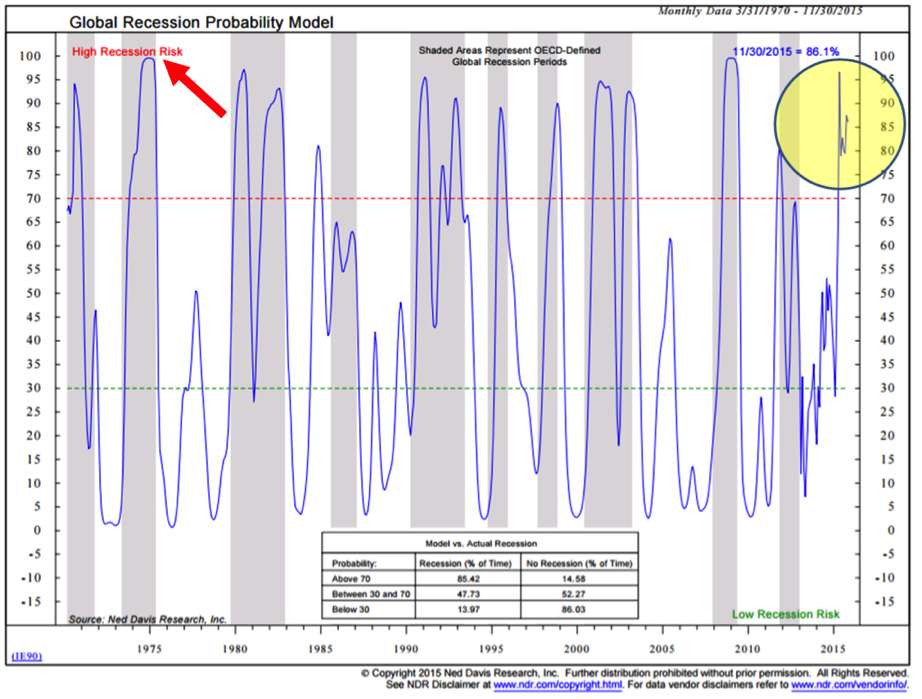

Global Recession Probability Model

“Eventually, negative interest rates will kill growth.” – Charles Gave

The following model looks at a composite of leading indicators for 35 countries. Indicators such as money supply, yield curve, building permits, consumer and business sentiment, share prices and manufacturing production. It then uses a logistic regression method incorporating the composite of leading indicators and trend data for all 35 countries. The objective is to predict the likelihood of a global recession.

A score above 70 indicates a high recession risk and below 30 signals low recession risk. The box at the bottom center of the chart shows the “Model vs. Actual Recession.” Note that global recession has occurred 85.42% of the time when the model reading has been above 70%. It is at 86.1% today.

I find it hard to bet against the current odds of a global recession. I believe we are in one now.

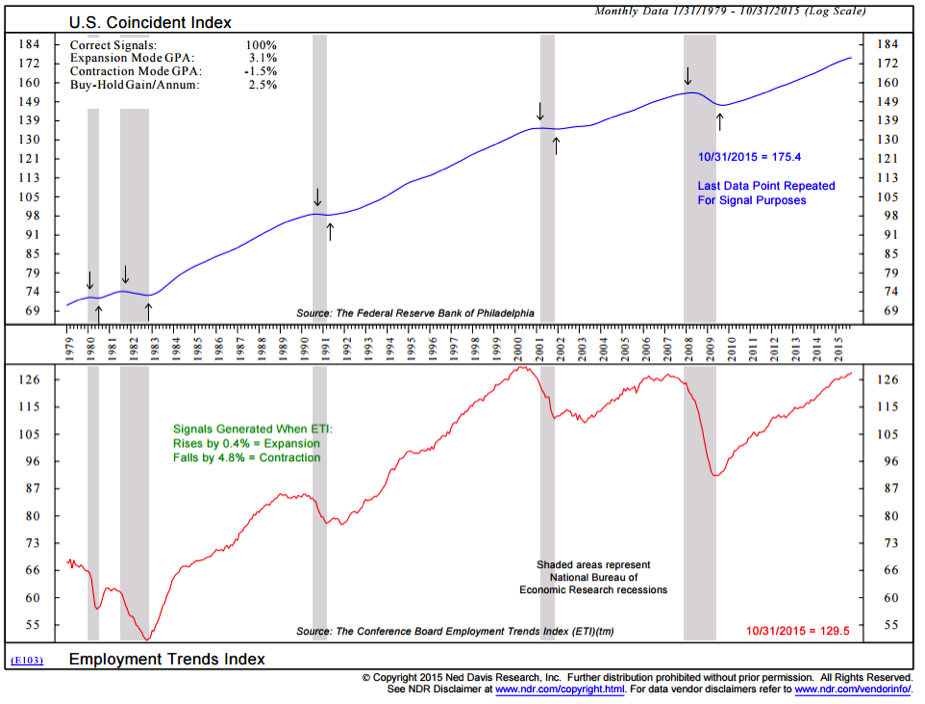

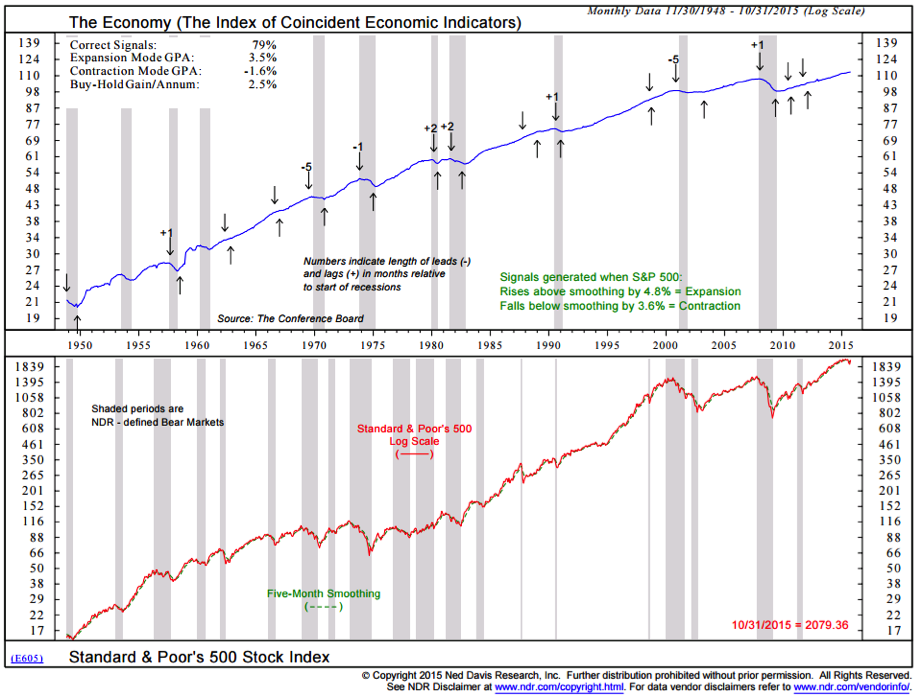

The U.S. is in better shape. Though let’s keep a close eye on the next two charts.

Chart 1 shows Low Current U.S. Recession Risk:

Chart 2 shows Low Current U.S. Recession Risk:

Keep an eye out for down arrows in the top section of the above two charts. Send me a note if you find the charts confusing. I’ll be happy to walk you through them.

A Few Equity Hedging Ideas

Here is what you can do:

- Invest in a few liquid alternative mutual funds. Look for proven managers and find complementary pairs meaning strategies that may deliver return but do so in a way that don’t correlate with each other. Match their historical return streams together and see if the correlation is close to zero.

- Consider current high valuation levels in U.S. equities. If you agree they are high (with forward probable 10-year returns low much like 2000 and 2008), then reduce exposure and hedge. Find equity mutual funds that do it within a strategy or do it yourself.

- Get in front of the coming high yield opportunity. Find mutual funds that trend trade and others that are tactical or more flexible in nature. Default waves create outstanding opportunity. Be positioned and, importantly, mentally prepared to take advantage of the opportunity (it won’t feel good when the opportunity is best).

Let me know if you would like some targeted ideas. The point is that there are many good funds and ETF’s to consider.

Trade Signals – Watch Out for Minus 2 (Don’t Fight the Tape or The Fed Indicator is in a Rare -2 Model Reading) – A Strong Sell Signal (Hedge!)

The significant signal this week is the -2 reading on the Don’t Fight the Tape or the Fed model. The model looks at the technical health of the broad equity market (how are most stocks doing across the various sectors). When the majority begin to break down and just a few support the market (looking at trend and momentum of thousands of stocks), the technical health is not good. This indicator combined with a 10-year Treasury yield indicator creates a reading from +2 (bullish) to -2 (bearish).

The last model reading of -2 was in 2012. As you’ll see below, the annual gain per annum when the reading was -2 was a -46.8% (an occurrence 5.9% of the time since 1998). Note that doesn’t mean a 46.8% decline is coming; it just means that the market has declined during past periods of -2. Thus the “watch out for -2” warning. Also interesting is the relatively high level of investor optimism. This is surprising after last week’s negative week for U.S. equities.

This combined with a negative reading in the CMG NDR Large Cap Momentum Index and a collection of other unfavorable technical readings (below), suggests, to me at least, reduce and hedge equity exposure. The market remains richly priced. Risk is high.

Included in this week’s Trade Signals:

Equity Trade Signals:

- CMG NDR Large Cap Momentum Index: Sell Signal on June 30, 2015 at S&P 500 Index 2063

- Long-term Trend (13/34-Week EMA) on the S&P 500 Index: Sell Signal – Bearish for Stocks

- Volume Demand is greater than Volume Supply: Sell signal for Stocks

- NDR Big Mo Signal: Buy Signal for Stocks

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Neutral Optimism(short-term Neutral for Equities)

- Daily Trading Sentiment Composite: Excessive Optimism(short-term Bearish for Equities)

Fixed Income Trade Signals:

- The Zweig Bond Model: Buy Signal

- High Yield Model: Sell Signal

Economic Indicators:

- Don’t Fight the Tape or the Fed: Indicator Reading = -2(Bearish for Equities)

- Global Recession Watch – High Global Recession Risk

- U.S. Recession Watch – Low U.S. Recession Risk

Click here for the link to the charts.

Personal note

“Make no small plans. They have no power to stir men’s blood and probably themselves will not be realized. Make big plans.”

– Daniel Burnham

Blackrock estimates that nearly 75% of all investable assets will be in the hands of pre-retirees and retirees by 2020. Gone are the defined benefit plans. Today it’s self-directed 401k plans, IRAs and Roth self-directed retirement accounts.

Part of Merrill Lynch’s strategy is summed up in a quote I found in a Harvard Business Review article titled, Can You Say What Your Strategy Is?, “As baby boomers age and move from the relatively simple phase of accumulating assets to the much more complex, higher-risk phase of drawing cash from their retirement accounts, needs change.”

If you are a financial advisor, this is great news for your business model. “Make no small plans.” Better to dream big. As I tell my kids, “we are here to create great things.” It certainly makes the journey much more fun.

Thanksgiving is next week and I’m getting excited. My sisters are coming with their families, Brianna is coming home from NY, Tyler is coming home from school and Susan, me and our other four boys are really looking forward to family coming home.

I’ll be writing Trade Signals next Wednesday and posting it to the website (here). I’m going to wish you an early Happy Thanksgiving and hope this note finds you enjoying your family.

There won’t be an On My Radar published next Friday.

The travel schedule is building in December. I’ll be presenting at the IMN Global Indexing and ETF Summit in Scottsdale, Arizona on December 6-8. The lineup looks outstanding. There is much growth in the ETF space – enhanced tools for you and me to use. I’ll share what I learn in a future post.

On December 7, and just a few blocks away from the conference venue, I’ll be visiting Steve Captain and Kevin Bauer and their team at BCJ. Salt Lake City follows on December 14-16. Lined up is a meeting with David Russon, Rhett Jeppson, Brent Cochran and the senior team at Investment Management Consultants. Talk about two firms with great strategy and process. One of the really nice benefits in any business is working with people you really enjoy. “Make big plans” – indeed.

I’m heading out a few days early with plans to test my repaired ACL at Snowbird. Physical Therapist Mike is telling me to take it easy. I’m hoping for a lot of early season snow, a strong left knee and an ice-cold end of day beer.

I’ll be traveling through Dallas on my way home from Salt Lake City to visit with my buddy John Mauldin. He’s working on a new project that sounds pretty exciting and it will nice to see what he is thinking about as we move into 2016. He too is a “make big plans” guy.

Have a great weekend and here is an early wish to you and your family for a warm and wonderful Thanksgiving holiday!

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG White Paper Understanding Tactical Investment Strategies you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at@askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History: Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Provided are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out of the money covered calls and buying out of the money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out of the money put options for risk protection.

Please note the comments at the bottom of this Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group

© CMG Capital Management Group