Currency forecasting is inherently difficult. Getting monetary policy right can help in the short-term, but beyond three months, you can’t do any better than a random walk. That aside, the strong dollar (along with softer global economic growth) has played a major role in the slowdown in U.S. corporate profits this year. What can we expect for 2016?

First, some basics… The exchange rate of the dollar can be thought of as a price, dependent on supply and demand. There are trade flows and capital flows in and out of each country. Exchange rates will adjust to balance them (on net). One often hears complaints about the U.S. having to “borrow money” from the rest of the world. That is a function of the trade deficit, not the government’s budget deficit. Net capital inflows merely balance the net trade outflows in goods and services. Capital flows can react quickly to exchange rate movements, while trade flows respond more slowly. Simply put, global capital can move rapidly, but import and export activity doesn’t turn on a dime. This can lead to some “over-shooting” in exchange rates.

In most advanced economies, the exchange rate of the currency falls under the jurisdiction of the finance ministry (the Treasury Department in the U.S., the Eurogroup in Europe), not the central bank. However, finance ministries (in the advanced economies) have little ability to influence currencies beyond short-term interventions and jaw-boning. Central bankers can have a major influence on exchange rates in the short term, but that is not the goal of monetary policy. Rather, the central bank has to consider the impact of exchange rate movements on domestic growth and inflation. In general, policymakers are not much concerned about the level of the exchange rate. Rather, the speed of adjustment is what’s important. Rapid movements in currency markets can be destabilizing.

Over the last four quarters, U.S. merchandise exports fell 6.6%, but that decline largely reflects a drop in export prices. Merchandise exports fell 1.0% in inflation-adjusted terms – not a large decline. Merchandise imports fell 4.0% (3Q15-over-3Q14), but rose 5.4% adjusting for the drop in import prices. For services, exports rose 2.2% y/y, while imports rose 2.5%. Hence, the impact on GDP growth has been relatively limited (-0.7 percentage points from GDP growth over the last year). There may be some lag involved, so we may not want to write off concerns just yet. Moreover, the stronger dollar and softer global growth has had an impact on corporate profits.

On November 13, IMF Managing Director Christine Lagarde said she supported the staff’s recommendation that the Chinese renminbi be included in the basket of currencies which make up the IMF’s Special Drawing Rights (SDR). The IMF’s Executive Board will take up the issue on November 30 and, if approved, the Chinese currency would be added on October 1, 2016. The Chinese currency is still highly manipulated, but for the IMF the criteria are that it be “freely usable” and “widely used.” Some financial “newsletters” have suggest ed that this is a step in replacing the dollar as the premier reserve currency. However, these “newsletters” are simply selling gold (and this is only the latest excuse, among many, that they have put forth in the last several years). Still, there is a lot of downward pressure on the Chinese currency. Preventing it from falling comes with a cost.

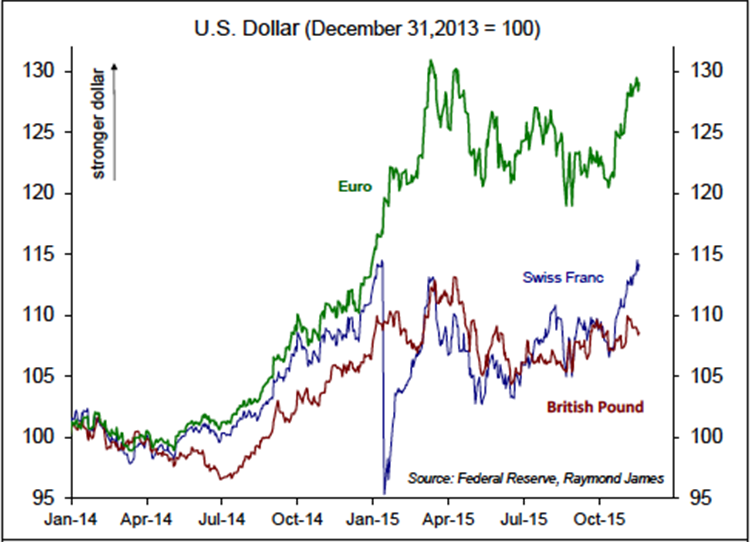

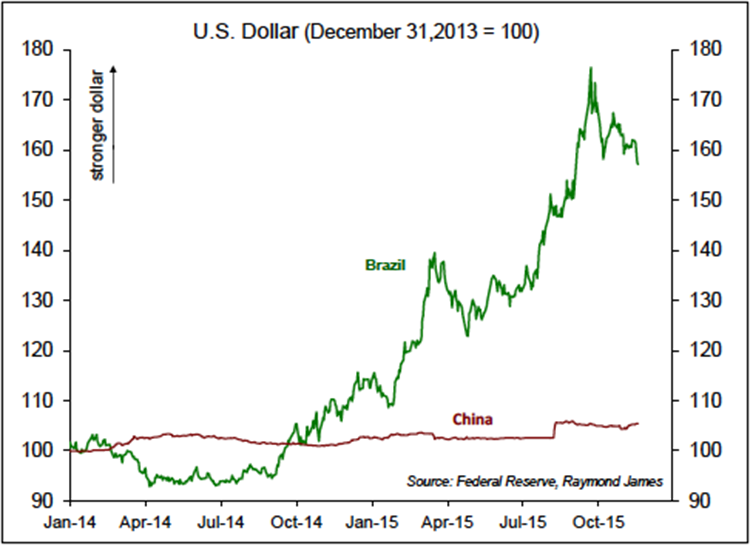

The dollar’s strength against the major currencies reflects relative monetary policy stances, but much of that is likely already baked in. The dollar’s strength against the world’s other currencies reflects concerns about growth in emerging economies. Growth in these economies should eventually pick up, but the pace may be more moderate than we’ve seen in the last decade or two. In any case, Federal Reserve policy is going to be based on what’s happening with the domestic economy.