Introduction

In consideration of today’s low interest rate environment, fixed income securities offer little in the way of return. Moreover, the safety characteristics normally associated with fixed income are also potentially upside down. Since early 1982, the interest rates available with fixed income have been in a continuous freefall. This has presented both good and bad news for the conservative investor desirous of a high and safe income stream on their portfolios.

The good news is that bond prices move inversely with interest rates. Therefore, when interest rates drop, as they have done since 1982, the prices of previously issued bonds will rise. Therefore, fixed income investments, primarily bonds, have provided the opportunity for high yield and either capital appreciation or at least stable prices. This falling interest rate trend has gone on for more than three decades, and as a result, fixed income returns have been abnormally strong and even high.

However, the first part of the bad news is that fixed income investors need to understand that previously issued bonds will move to a premium valuation as rates are dropping, but will eventually move back to par when they mature. Consequently, the only way to lock in capital appreciation in addition to your interest income would be to sell your bonds before they mature. Otherwise, temporary capital gains created by falling rates will inevitably dissipate to breakeven levels. As a result, investors that hold bonds to maturity will in effect suffer losses of purchasing power due to inflationary forces.

On the other hand, the additional bad news is that falling interest rates result in the inability to reinvest in newly-issued fixed income instruments at rates that are attractive. But the worst bad news is that those investors purchasing fixed income at today’s extremely low rates are exposing their capital investments to potential losses in a rising interest rate environment.

Investors need to understand that bond prices fluctuate just as stock prices fluctuate. If future interest rates move higher, and if that were to happen quickly, originally issued bond prices could drop just as much as stock prices did during the Great Recession. Bonds are considered safe because they mature at par; however, bonds are also liquid. Therefore, bond prices can, and do, fluctuate between their issue date and maturity.

Fairly Valued Utility Stocks for Income and Safety

Consequently, and as the result of the fixed income dynamic discussed above, I have been, temporarily at least, eschewing fixed income. In other words, I have been recently looking for viable alternative income-producing opportunities. Importantly, I am just not focused on finding higher income streams; I’m also concerned about finding income-producing alternatives with reasonable safety characteristics. I believe that carefully selected utility stocks can fit the bill, as long as they are purchased at sound or attractive valuations.

Stocks and bonds are different investment types and therefore possess different investment merits and characteristics. In other words, I believe it would be a stretch to state that utility stocks are perfect fixed income alternatives. On the other hand, utility stocks, when purchased at sound valuation, do possess and/or share characteristics with bonds that are similar enough to consider them a reasonable alternative.

When interest rates are at normal levels, bonds pay higher interest income than most blue-chip dividend paying stocks provide in dividend yield. Furthermore, since bonds provide an implicit guarantee of returning principle at maturity, they also provide a level of safety not normally associated with stocks. However, it is also true that all dividend paying common stocks are not the same.

Utility stocks are generally regulated monopolies, and as such, have a history of producing reliable and consistent earnings growth and above-average levels of dividend income. Nevertheless, even though the earnings growth on utility stocks is generally consistent and reliable, earnings and dividends generally do not grow very fast. Regulation provides consistency and a level of reliability, but at the expense of higher or above-average growth potential.

Southern Company High-Yield Sound Valuation

Southern Company (SO) is a blue-chip utility stock that is considered one of the strongest among its peers. The two primary reasons supporting this view are the relatively friendly regulatory environment they operate in, and the better-than-average economic fundamentals associated with its region. Headquartered in Atlanta, Southern Company dominates the power business serving both regulated and competitive markets across the southeastern region.

For example, Zacks considers Southern Company one of the largest and best managed electric utility holding companies in the United States. Operating in one of the fastest growing and strongest regions of the country, Southern Company is a holding company for four regulated Southern electric utilities that serve about 4.4 million customers. Those utilities are Georgia Power, Alabama power, Gulf Power, and Mississippi power.

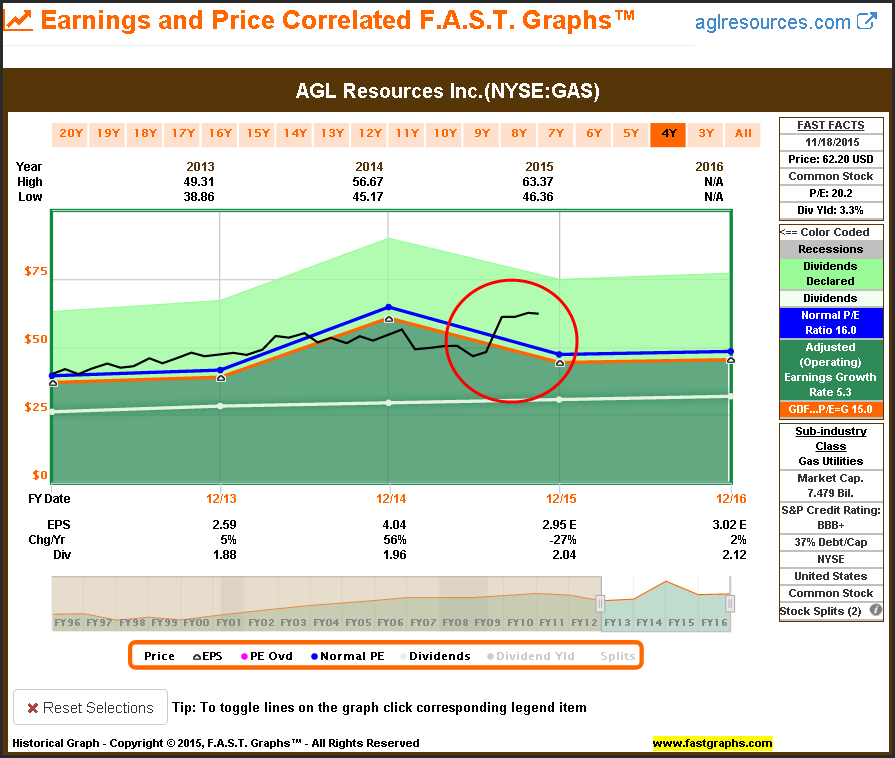

Additionally, Zacks estimates that Southern Company’s impending acquisition of AGL Resources (GAS) could double its customer base and generate more revenues. However, this additional growth potential is slightly mitigated by what many consider the high valuation (approximately $28 billion) they paid for AGL. The following earnings and price correlated graph on AGL (GAS) illustrates the premium valuation that Southern Company is paying.

On the other hand, when looked at from the perspective of the 3 to 5 year trend line growth estimates for AGL Resources, the valuation that Southern Company might be paying appears more reasonable. These long-term growth estimates may in fact be reasonable, and more importantly, could provide a meaningful benefit to Southern Company. Considering that Southern Company currently generates approximately 40% of its power from coal-fired plants, the AGL acquisition could provide a breath of fresh air (pun intended).

According to MorningStar: “If the AGL deal closes, Southern will operate 7 gas LDCs, including a core Georgia business and a large LDC in Illinois, while gaining stakes in two midstream gas projects with upside to more.” MorningStar also believes that: “Southern Company operates in the business friendly Southeast, where its relatively low power prices and sterling reputation help to foster a constructive and stable regulatory atmosphere.”

The following Short business description courtesy of S&P Capital IQ provides further insight into Southern Company and its businesses:

“The Southern Company, together with its subsidiaries, operates as a public electric utility company. It is involved in the generation, transmission, and distribution of electricity through coal, nuclear, oil and gas, and hydro resources in the states of Alabama, Georgia, Florida, and Mississippi.

The company also constructs, acquires, owns, and manages generation assets, including renewable energy projects. As of December 31, 2014, it operated 33 hydroelectric generating stations, 33 fossil fuel generating stations, 3 nuclear generating stations, 13 combined cycle/cogeneration stations, 9 solar facilities, 1 biomass facility, and 1 landfill gas facility.

The company also provides digital wireless communications services with various communication options, including push to talk, cellular service, text messaging, wireless Internet access, and wireless data; and wholesale fiber optic solutions to telecommunication providers in the Southeast. The Southern Company was founded in 1945 and is headquartered in Atlanta, Georgia.”

The biggest negative I see with Southern Company relates to issues within their nuclear power businesses. Cost overruns on their Georgia Power nuclear projects, principally Vogtle, do raise some concerns. However, I think those concerns are exaggerated given the diversity of Southern Company’s diverse electric generating businesses.

Investing In Utility Stocks at Sound Valuation Is Critical

When investing in low growth companies like utility stocks, getting valuation right is even more critical. Just as it is with all companies, utility stocks can become overvalued from time to time. However, since utility stocks do not grow very fast, overpaying for future earnings can dramatically destroy the dividend income advantage that utility stocks typically offer. Paying too much for a low growth enterprise can easily result in long-term capital losses and future earnings will generally not be large enough to bail you out. You can test this statement by utilizing the following live earnings and price correlated Southern Company graph.

Bonus: Live Fully-Functioning Historical F.A.S.T. Graphs on Southern Company

In order to assist the reader in understanding Southern Company’s current valuation and historical operating achievements, I offer the following live fully functioning historical F.A.S.T. Graphs™ on the company.

Furthermore, to get maximum benefit from this exercise, I offer the following tips on how to utilize and navigate the live graph. At the top of the graph there are orange rectangles representing different historical time frames. For example, you can click on the orange rectangle 10Y and the graph will automatically draw a 10 calendar year graph. Therefore, you can quickly move from one time frame to the next and evaluate changes in earnings growth rates and historical normal P/E ratio valuations over each respective time frame. There is also a scrollbar at the bottom of the graph that allows you to focus on any historical time frame of your choosing.

At the bottom of the graph there is a long orange rectangle that allows you to take the graph apart or rebuild it by simply clicking on any of the words. For example, if you click on the word "Price," monthly closing stock prices will be taken off of the graph and you can replace them by simply clicking on the word "Price" again. You can do this with all of the items located in the orange rectangle.

But most importantly as it relates to the thesis of this article (valuation) the graph also has a built-in performance calculation feature. Simply point and click your mouse on any price point on the graph (the black line) until a red dot appears. Then simply move your mouse to any other price point on the graph and click it and a pop-up will appear with the calculation of the performance over the time frame you chose. To erase the calculation, simply point and click on your second red dot and you will be ready to perform another calculation. Note: all these calculations are based on purchasing and holding one share of the company's stock.

I suggest that the reader utilizes this calculation function feature in order to evaluate the effects that valuation has on long-term performance. You can measure periods of time from high valuation to low valuation (when price is above the orange valuation reference line), from low valuation (when price is below the orange valuation reference line) to high valuation, etc. As you perform these calculations, notice the effect that various levels of valuation have on long-term performance over time. I hope you have fun performing these various calculation exercises, and I hope they reveal and solidify the important effect that valuation has on long-term returns when investing in utility stocks.

Southern Company’s Income Advantage

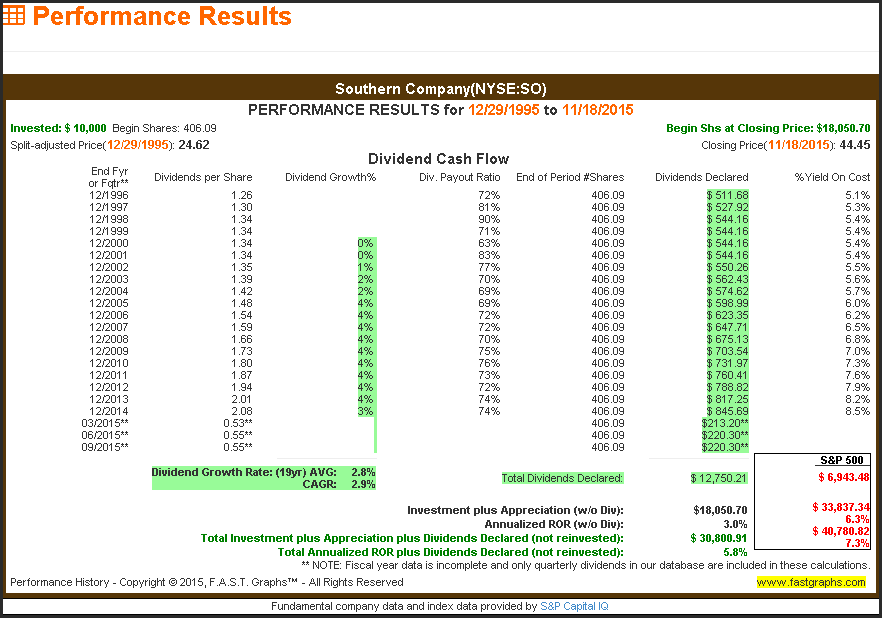

The following detailed performance report on Southern Company since 1996 illustrates the significant income advantage it has provided shareholders compared to an equal investment in the S&P 500. Total cumulative dividend income from Southern Company would have been almost twice as high as the index would have provided.

However, due to the low earnings growth rate that Southern Company (and utility stocks in general) has generated, higher yield came at the expense of capital appreciation. Nevertheless, in contrast to long-term bonds held to maturity, Southern Company did produce some capital appreciation in addition to its high dividend income generation.

Reinvesting Dividends in High-Yield Southern Company Levels the Playing Field

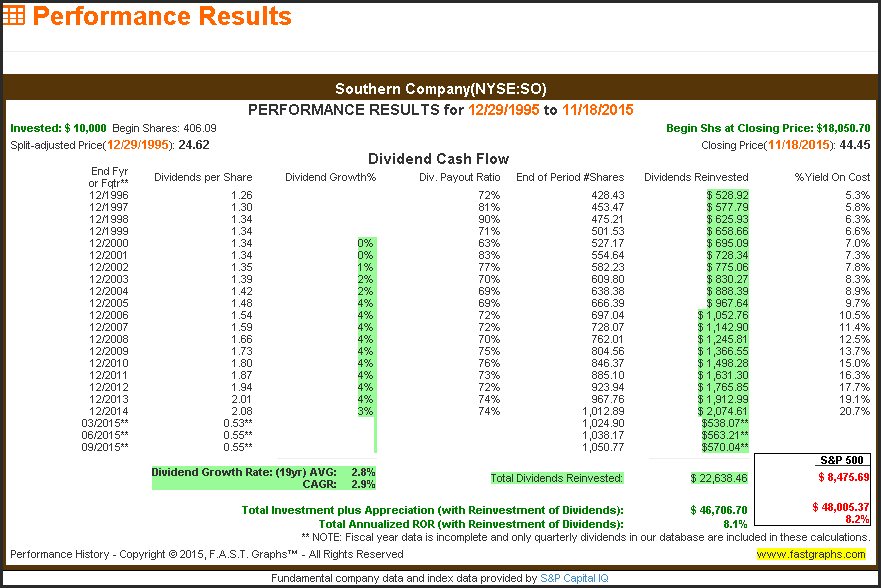

The above historical performance report on Southern Company validates the income advantage that a blue-chip utility stock investment can provide. However, for those investors focused more on total return, a low growth high yield utility stock like Southern Company can level the total return playing field - if you reinvest your dividends.

As the following performance report on Southern Company with dividends reinvested each quarter illustrates, the high income advantage remains. On the other hand, the capital appreciation (total return) advantage that the index held without reinvesting dividends disappears. With dividends reinvested, the total return on Southern Company and the S&P 500 end up in a virtual dead heat. I believe this validates the power and protection that high-quality high-yield dividend paying stocks offer.

This is especially true when a low growth high yielding utility stock like Southern Company is originally invested in when valuation is sound. On that note, I would like to add that both Southern Company and the S&P 500 were soundly valued at the beginning of 1996. Therefore, the return comparisons over this timeframe are apples to apples from a valuation perspective. Additionally, the virtual tie in total return between Southern Company and the S&P 500 happened even though Southern Company only grew earnings at 2.5% while the S&P 500 grew earnings at 6.1% over the same time period.

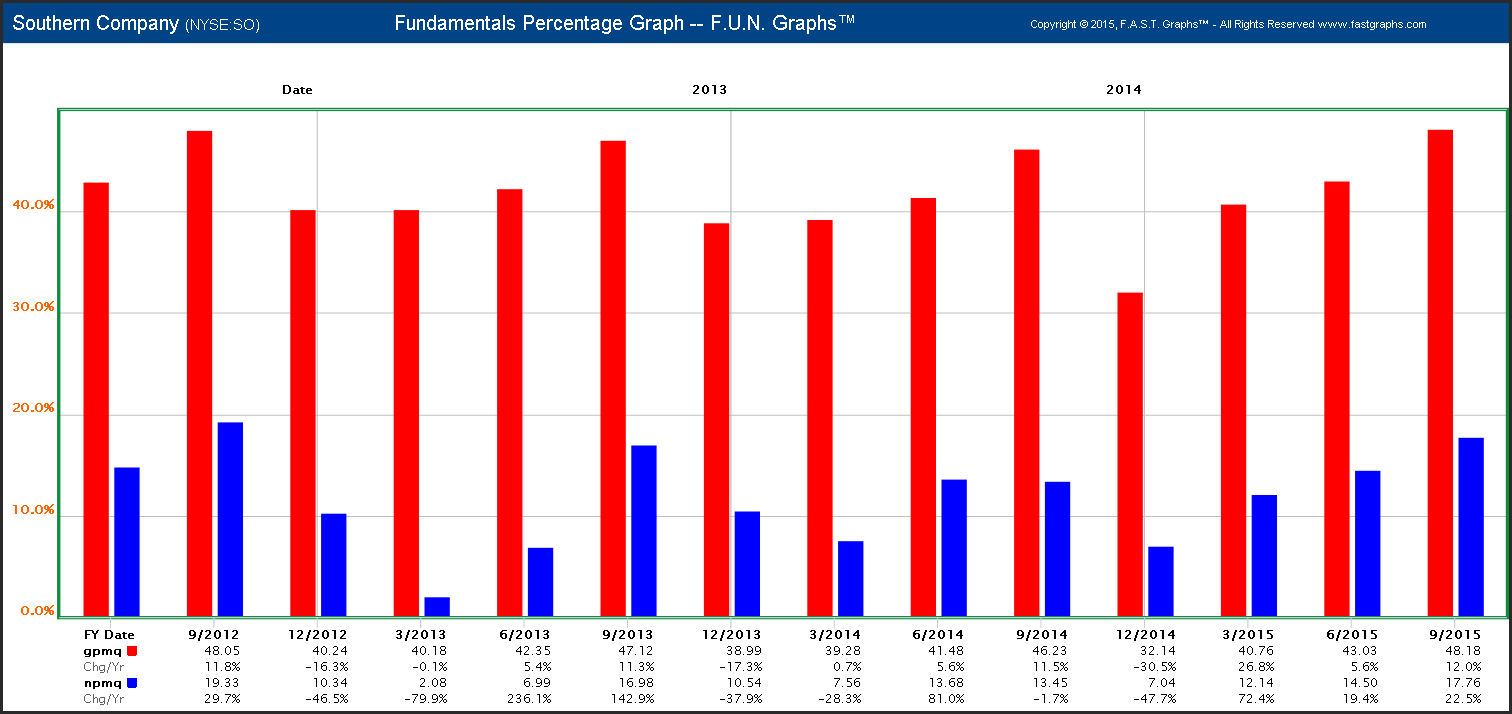

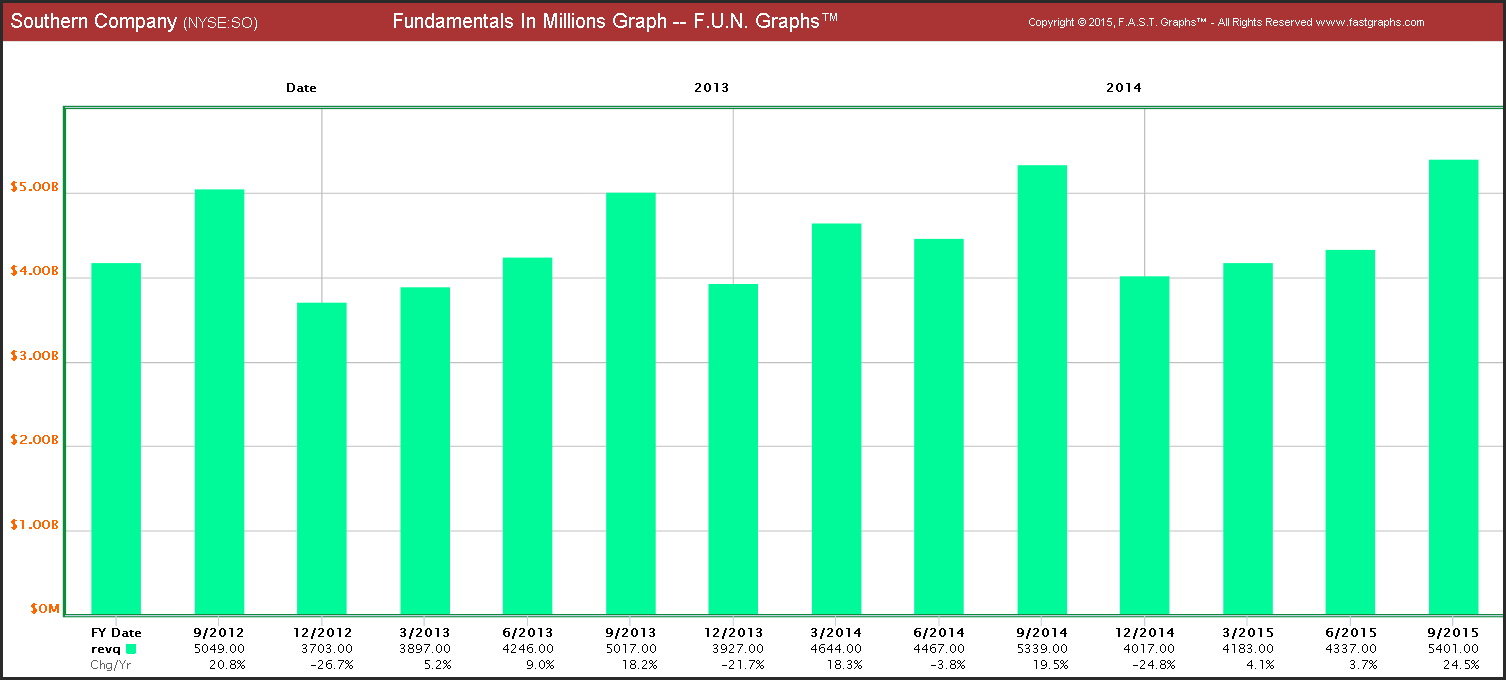

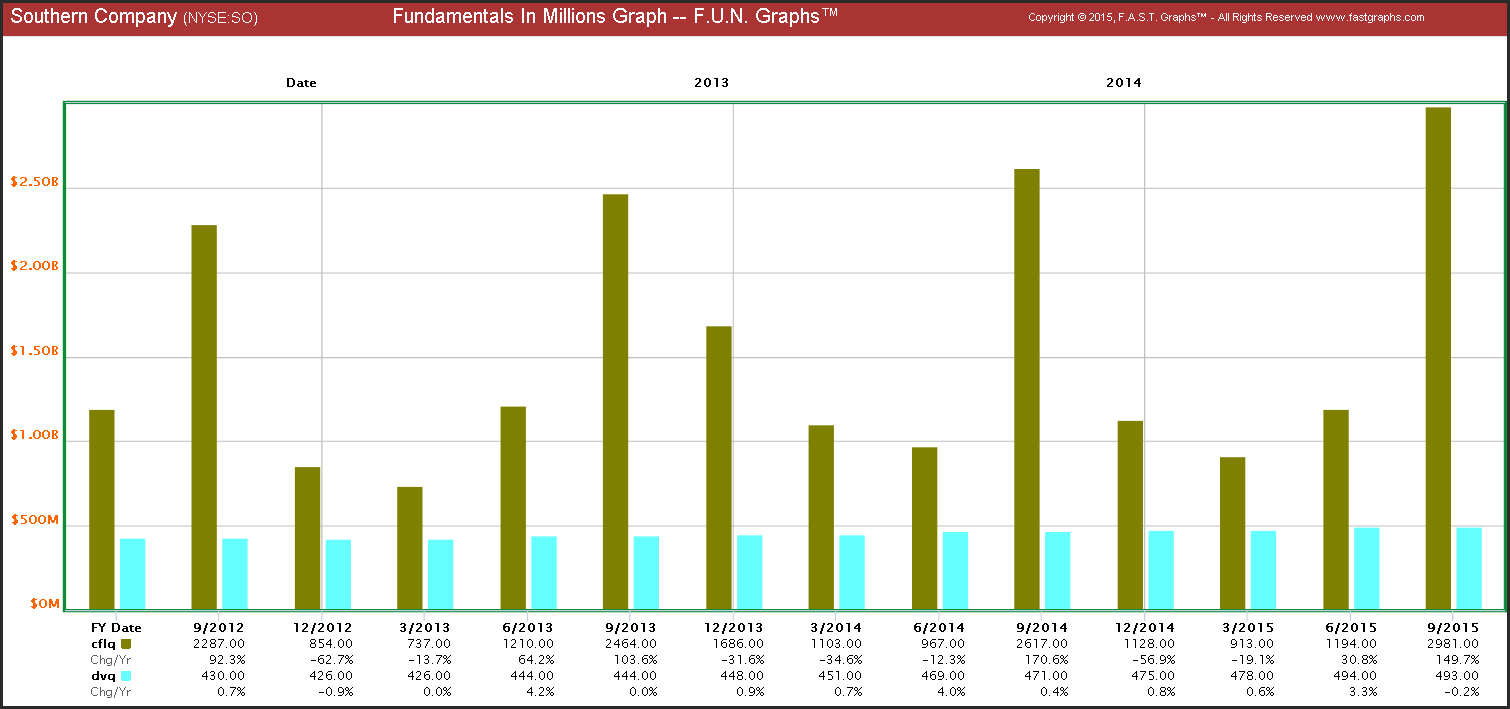

Additional supporting fundamental metrics on Southern Company

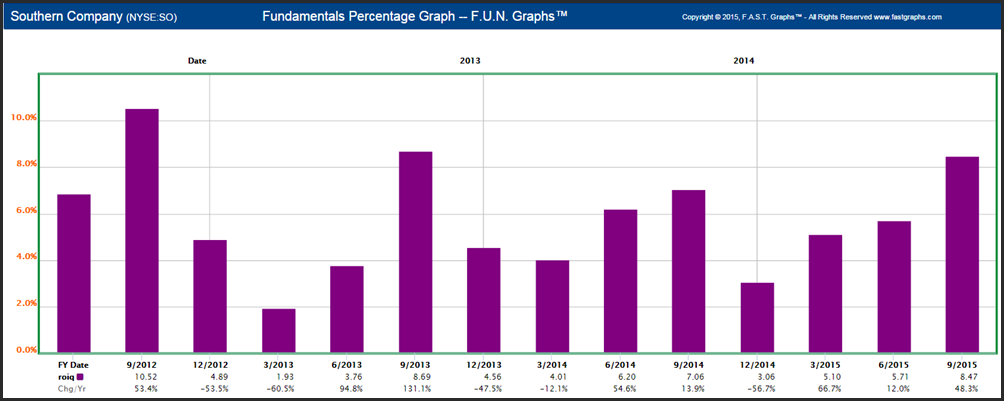

Returns on invested capital (roiq) is an important consideration when evaluating utility stocks. After hitting a low point in the last fiscal quarter of 2014, Southern Company has been steadily improving each quarter in 2015. I consider this a comforting accomplishment.

In concert with an improving return on invested capital, Southern Company’s bottom line has also been steadily improving throughout 2015. Southern Company’s net profit margin per quarter (npmq) in 2015 has increased from 7.04% to 17.6% in their most recent quarter ending in September 2015.

Southern Company’s revenues for quarter (revq) have also been improving throughout 2015. Importantly, revenues had recovered to 20-year highs in 2014, and 2015 is on track to be even higher.

But perhaps most importantly, since I’m attracted to Southern Company for its dividend yield, cash flow per quarter (cflq) strongly support dividends for quarter (dvq). Southern Company is a Dividend Challenger on fellow Seeking Alpha author David Fish’s CCC lists that has raised its dividend for 15 consecutive years. Moreover, southern company has paid a dividend every quarter since 1948.

Summary and Conclusions

I consider Southern Company a strong and healthy utility stock that can currently be purchased at a sound and attractive valuation. At current levels, its dividend yield is approaching 5%, and I believe this represents an opportunity for investors in need of current income. Consequently, I would recommend purchasing Southern Company as long as its yield remains above the 4.5% level or better.

In today’s low interest rate environment, a current yield above 4% with the potential for modest capital appreciation to fight inflation looks attractive. Southern Company, like most utilities, is not offered as a high total return opportunity. Instead, I suggest that is most suitable for those investors, including retired investors, that are looking for high current income and reasonable safety.

Disclosure: Long GAS

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.