The agonizing over whether the Fed will begin raising short-term interest rates is unlikely to end soon. A 25-basis-point increase shouldn’t have much of an impact on the economy, especially if the Fed makes it clear that it intends to go slow with further rate hikes. However, the financial markets believe this to be a big deal. So it is. Fed officials have continued to signal that it “may be appropriate” to start in December, but they have also continued to signal that this is not a done deal.

Many market participants viewed the October employment data as being the clincher – a clear catalyst for Fed liftoff. However, Fed officials were already leaning hard in that direction before the jobs data. Recall that the Fed came very close to raising rates in September, but delayed, citing possible downside risks from the rest of the world. Those downside risks are still with us, but they appear to be less worrisome than two months ago. The stronger dollar and weaker global economy have restrained U.S. exports, but it hasn’t been a sharp drag.

Domestically, the economy appears to be in relatively good shape, although GDP growth is likely to be somewhat slower in the near term. Retail sales disappointed in October, suggesting less positive momentum for consumer spending into 4Q15, but aggregate wage gains (from the Employment Report) picked up.

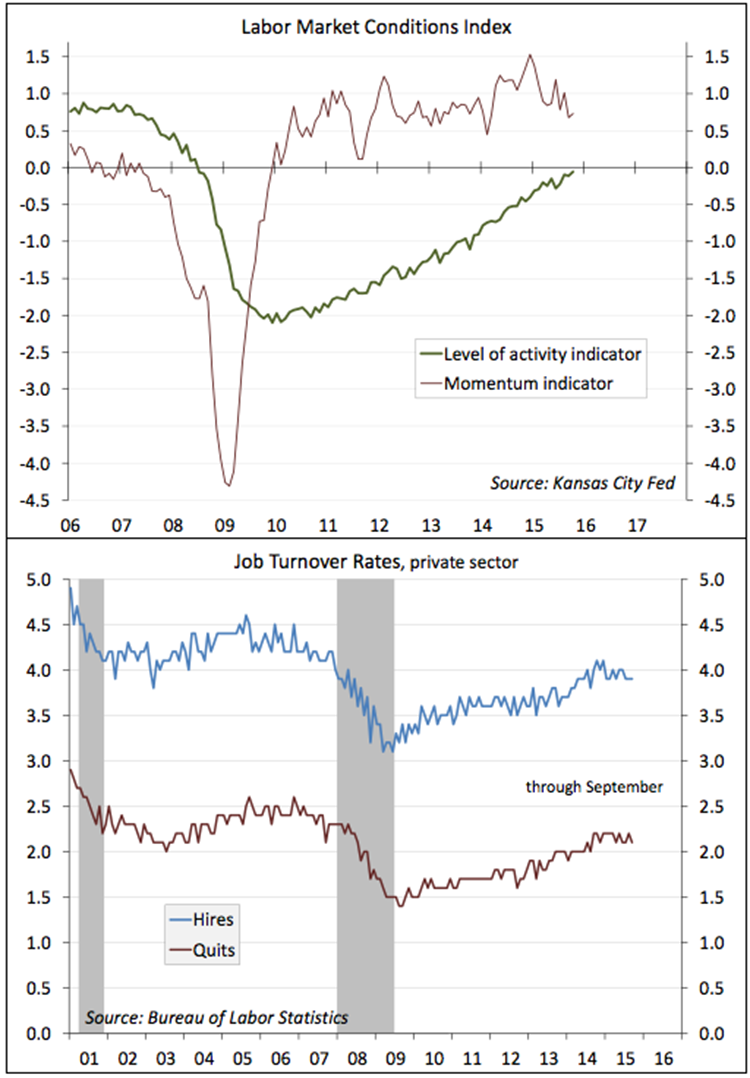

Why does the Fed want to raise rates? It’s largely about the job market. Monetary policy affects the economy with a long and variable lag (usually taken to be 12 to 18 months). At the current pace, there will be a lot less slack in the job market a year from now. In early 2014, Fed Chair Yellen highlighted hiring and quit rates as important gauges of the job market’s strength. Hiring and quit rates improved since the start of the economic recovery, but have flattened out over the last year. Although the unemployment rate has declined, there may be a lot more slack in the job market than that figure would suggest.

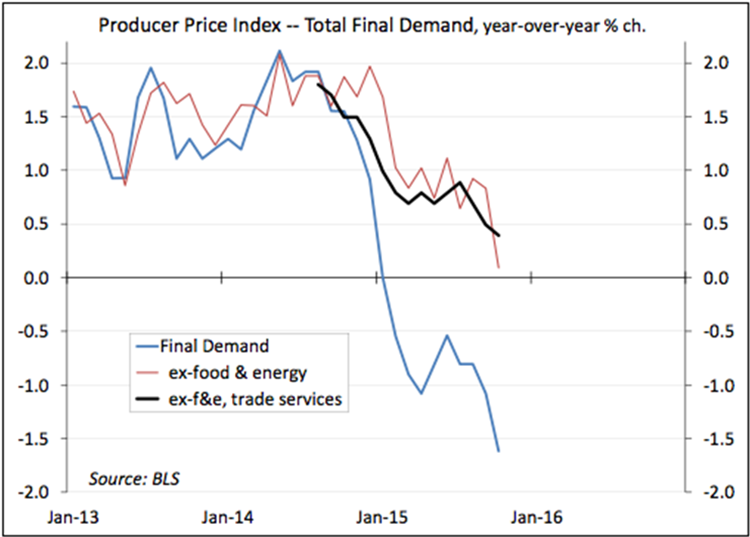

In the October 28 policy statement, the FOMC repeated that it wants to see some further improvement in the labor market, but it also needs to be “reasonably confident” that inflation will move back toward the Fed’s 2% goal. In public speeches, senior Fed officials have repeated the simple logic that inflation should pick up as the impact of low oil prices and low import prices fade. However, over the last couple of weeks, the dollar has strengthened again and commodity prices have dipped. The Producer Price Index showed further downward pressures.

Many see the Fed as being in a box – policymakers can’t raise rates, because the markets won’t let them. Falling share prices and a stronger dollar will further restrain economic growth and put additional downward pressure on inflation. However, a small rate increase should not have much of an impact on the economy and Fed officials have continued to stress that the path of policy tightening will be data-dependent and likely very gradual. We should get a strong, clear signal from Chair Yellen when she delivers her JEC testimony on December 3.