Celgene: A Primer on Growth Stock Value Investing (GARP): Part 2

Introduction

This article is the second in a two-part series on applying the principles of value investing. In part 1 my primary focus was on the benefits of investing in fundamentally strong dividend growth stocks when they are out of favor, and therefore, undervalued as a result. In this part 2, I will be turning my attention to determining the fair value of growth stocks. Although the underlying principles of value investing apply, assessing the fair value of a true growth stock differs greatly from valuing a dividend paying company. In both cases, the primary focus of the value investor is on fundamentals first and stock price secondarily.

However, one of the primary differences when valuing a growth stock versus valuing a dividend paying stock is the absolute necessity to focus on the future earnings potential of the company in question. Many of the most famous value investors, Ben Graham for example, believed in valuing a company solely based on historical earnings, and never on future earnings estimates.

Personally, I disagree with that approach, but only in part. When valuing a dividend paying stock, I agree that your primary focus can rationally be placed on the company’s historical achievements. On the other hand, since all investing results do, in fact, occur in future time, I believe that it is important to also have a reasonable perspective of the future growth potential of even a dividend paying company. In the long run, future earnings will determine future market price and the amount of dividend income you will receive.

In contrast to dividend paying stocks, investing in pure growth stocks is primarily based on the opportunity and expectations for above-average future capital appreciation. Since there is no dividend income to soften the blow of stock price volatility, when investing in growth stocks everything is about receiving a higher future price on your investment. Consequently, I believe that it is imperative to place most of your focus on the company’s future growth potential when considering investing in growth stocks.

Growth Stocks Defined

My definition of a growth stock is straightforward and precise. First of all, a growth stock represents the common stock of a company whose business is consistently growing earnings and cash flow at a significantly above-average rate. More precisely, I define a growth stock as a company whose earnings are consistently increasing at a minimum rate of change of earnings growth of 15% or better.

Additionally, I would define a hyper growth stock as one that is growing earnings at a rate of change of 25% or better. Admittedly, although both categories are rare, there are more 15% growers than there are companies growing earnings at 25% or higher. In between these broader gradations of growth are additional growth categories such as a high grower at 20%, etc.

The reason I am offering my precise definition of a growth stock, is because my experience has taught me that modern finance often holds a very cavalier or vague definition of what a growth stock is. Consequently, those engaged in the growth stock versus dividend growth stock debate will often cite studies indicating that dividend stocks outperform growth stocks. However, when I have personally reviewed and analyzed many of those studies, I usually discovered that the researchers were taking great liberties with the definition of a growth stock.

For example, it is commonly asserted that a growth stock is a company with a high P/E ratio. However, a high P/E ratio does not necessarily indicate a high-growth company. In many cases, a high P/E ratio can simply represent a lower growing business that the market is currently significantly overvaluing. On the other hand, it is true that growth stocks tend to carry higher P/E ratio valuations than are typically applied to blue-chip dividend growth stocks. For me to consider a company to be a growth stock, it must also have both a historical and the potential for a high-growth rate of earnings. A high P/E ratio without supporting earnings growth does not make the company a growth stock.

Consequently, many investors hold a vague or even inaccurate view of what a growth stock truly is. Therefore, in the context of this article, I am only discussing the possibility of adding true growth stocks into retirement portfolios based on the definition of a growth stock provided above.

10 Reasons Why Growth Stocks Can Be Appropriate For Retired Investors

Growth stocks are riskier investments than blue-chip dividend paying stocks. However, the potential for extraordinary future returns are often worth the risk. In June of this year I posted an article where I listed 10 reasons why growth stocks might be appropriate for retired investors.

I listed those 10 reasons below. However, the above article provides a more comprehensive explanation of the 10 potential benefits of investing in growth stocks.

The reason I am revisiting the benefits of how a sprinkling of growth stocks might benefit anyone’s portfolio is to put a spotlight on how powerful and extraordinary the returns can be through growth stock investments. On the other hand, I also want to illustrate how tricky growth stock investing can be. But most importantly, my objective is to emphasize the importance of valuation when investing in growth stocks. As pointed out in number 6 below, growth can overcome valuation mistakes. Nevertheless, getting valuation right can both support high future returns while simultaneously keeping your risk under control.

1. Performance Considerations-Opportunity for Significantly Higher Total Returns

2. Today's Growth Stock Can Become Tomorrow's Dividend Growth Stock

3. You Already Have All the Current Income You Need

4. Time and Inclination

5. Growth Stocks Are Contemporary, Interesting, Exciting and Even Fun

6. Growth Can Overcome Valuation Mistakes

7. Growth Stocks Are Often Misunderstood

8. The Power of Compounding

9. Earnings Growth Often Easier to Forecast

10. Growth Stocks Can Add Diversification

Principles of Valuing a Growth Stock

When investing in blue-chip dividend growth stocks I believe a good rule of thumb is to look for P/E ratios in the 14 to 16 range. In addition to representing the historical P/E ratio average range, P/E ratios of 14 to 16 also provide a reasonable current earnings yield on your investment. In contrast, the P/E ratios of growth stocks can be much higher and still represent fair value. Consequently, when valuing a growth stock I favor applying the formula that a fair value P/E ratio will be equal to the company’s earnings growth rate. For example, a company growing at 30% per year can be fairly valued with a P/E ratio of 30.

Although a high P/E ratio (for example a P/E ratio of 30) on a growth stock will represent a lower current earnings yield, when investing in growth stocks I believe it’s all about future earnings yield. The future earnings yield from growth stock investing is all about the power of compounding. Therefore, I felt it would be appropriate to repeat what I said about compounding (reason number 8) in my previous article:

Thanks to the power of compounding, investing in growth stocks can in effect compress time. In other words, instead of taking a decade or more to double your money in a blue-chip dividend growth stock, you can double your money much quicker in a true growth stock.

To illustrate my point I will turn to the widely-recognized Rule of 72. This rule states that you can calculate the number of years it takes to double your money at a given compound return by dividing it into the number 72. I have often utilized the following analogy to illustrate the point I am making about the power of compounding compressing time.

First I will make the assumption that the average person has a working lifespan of 36 years. In modern times this may be a conservative assumption, but as I will soon illustrate it facilitates the math. Next I will assume two different compound rates of return as they apply to the average dividend growth stock, and then to the pure growth stock. For the dividend growth stock I will assume a generous and above- average rate of return of 10% per annum. For the pure growth stock I will assume the appropriately higher rate of return of 20% per annum. The math then looks like this:

With the dividend growth stock, If I divide 10% into 72 I calculate that it will take 7.2 years to double my money (72/10% = 7.2 years).

With the pure growth stock, if I divide 20% into 72 I calculate it will take 3.6 years to double my money (72/20%=3.6 years).

If I apply this math to my assumed average working life of 36 years I get the following results:

If my money doubles every 7.2 years at a 10% rate of return, I will get 5 doubles in 36 years (36/7.2=5).

If my money doubles every 3.6 years at a 20% rate of return, I will get 10 doubles in 36 years (36/3.6=10).

The net effect is that by doubling my average rate of return from 10% to 20% per annum I do not earn two times the money by earning twice the return. Instead, I get double the doubles. Looked at from the perspective of the first $1 (dollar) invested, the power of compounding (compressing time) becomes vividly clear. Doubling my first $1 (dollar) 5 times at the 10% return results in the following: $1 doubles 5 times to $2, $4, $8, $16, and finally to $32. However, at the 20% return I get 5 additional doubles over the same 36 year timeframe as follows: $64, $128, $256, $512, $1024.

To put this into perspective, over my assumed 36 year working lifetime I earn 32 times more money by earning 20% than I would have if I earned 10% (1024/32=32). Doubling the number of doubles over the same timeframe shows the incredible power of compounding that true growth stocks are capable of offering.

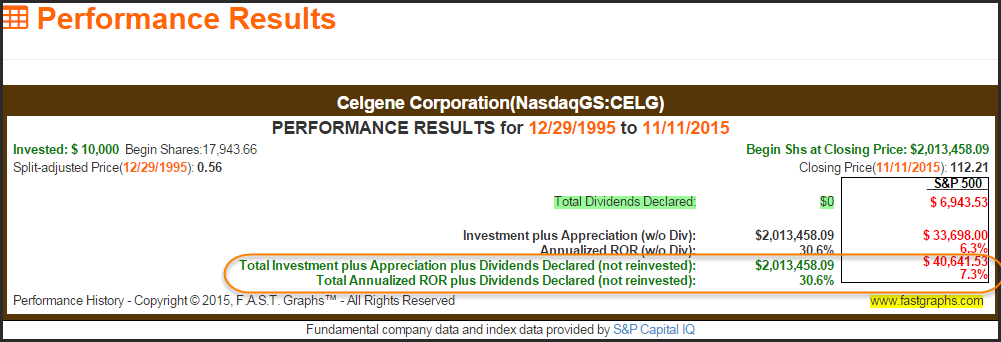

Celgene Corporation (CELG): 20 years of 30% Returns

My pure growth stock example to illustrate the power of growth stock investing is the biotechnology company Celgene Corporation. If you had invested $10,000 in Celgene on December 29, 1995 which is as far back as I have data, you would have earned a total annual rate of return exceeding 30% per annum. This would have turned $10,000 into more than $2 million which is more than 50 times greater than an equal investment in the S&P 500 over the same timeframe.

Although the above is an accurate calculation, I doubt that there are many investors that enjoyed such a powerful return. From 1996 through 2002, Celgene was generating negative operating earnings. However, the company generated positive earnings in 2003 and earnings grew rapidly from that point.

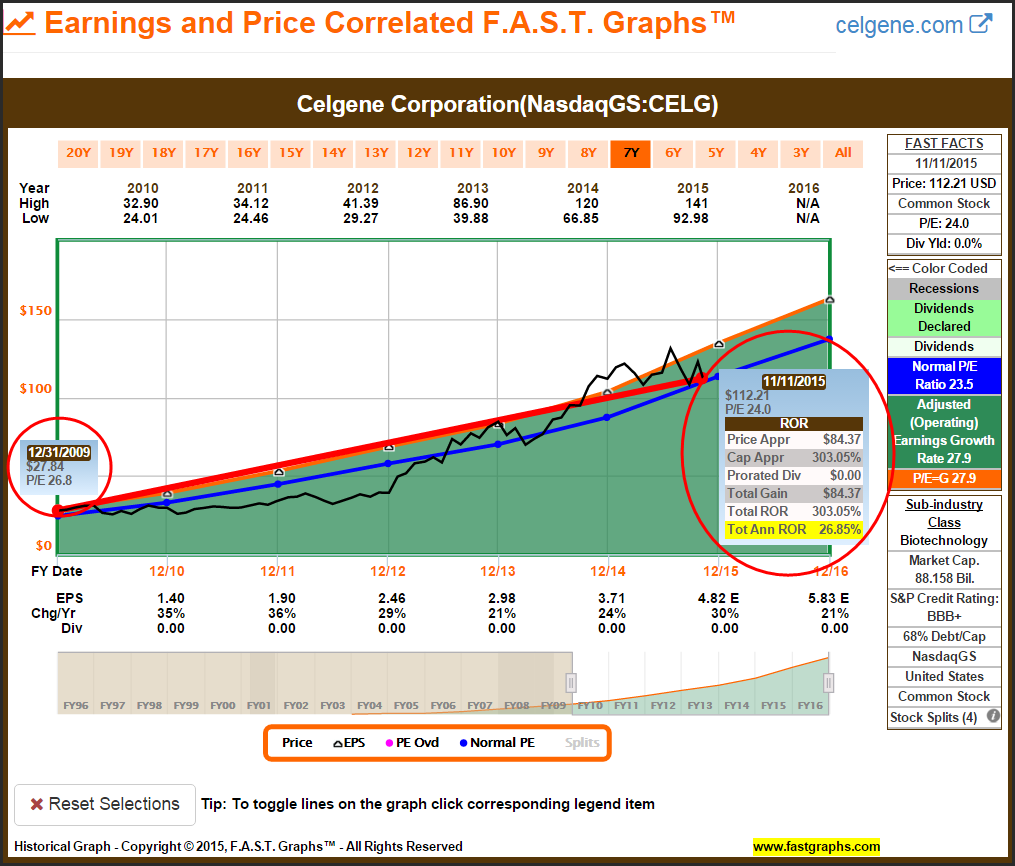

Since this article is about assessing fair value on growth stocks, I looked for a time when the company was fairly valued based on the P/E equals earnings growth rate formula. I want to be clear that the following earnings and price correlated F.A.S.T. Graph on Celgene since 2010 is a 20/20 hindsight presentation. In other words, I am not suggesting that we would have, or even could have, known that Celgene would grow earnings at approximately 28% a year going forward. Instead, I am simply illustrating the validity of the P/E equals earnings growth rate formula.

However, I believe the following example also serves to illustrate the power of investing in growth stocks when they are fairly valued. Note that Celgene was available at a P/E ratio that ended up equaling its future earnings growth rate at the beginning of 2010. Utilizing the calculating function of F.A.S.T. Graphs™ we see that Celgene generated a total annual rate of return that was consistent with the company’s earnings achievement over that time.

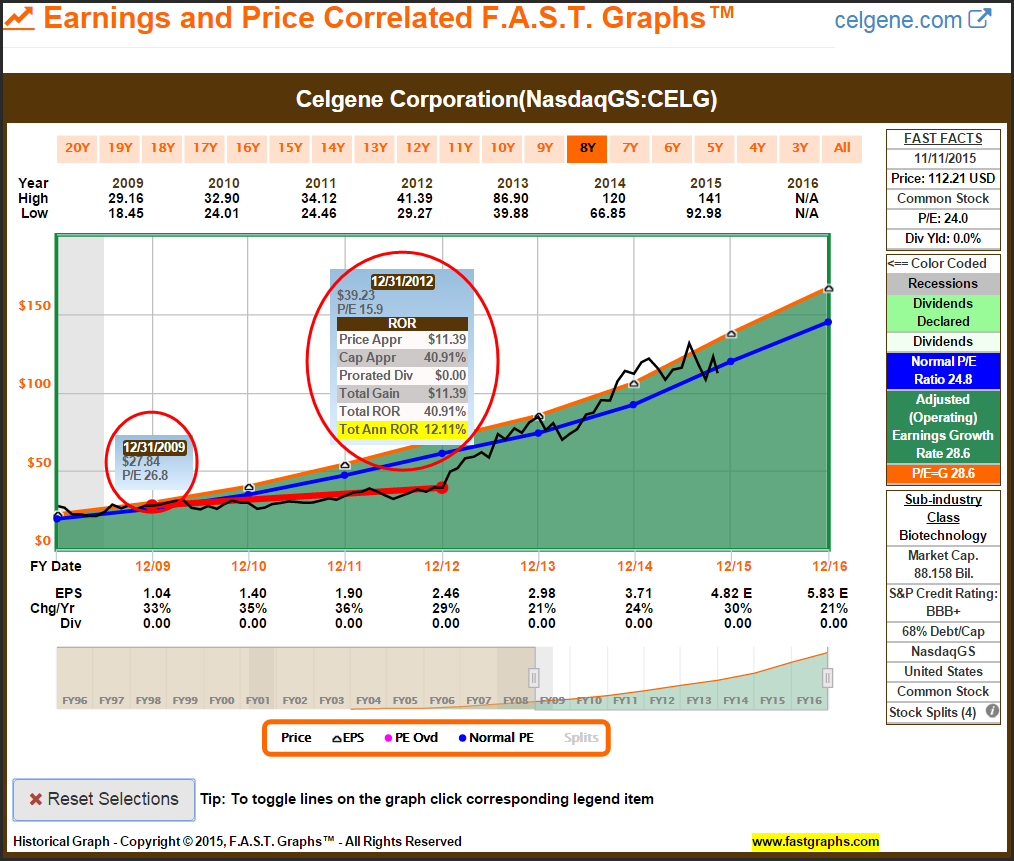

However, my next calculation is run over the next 3 years ending on December 31, 2012 which represents a period when Celgene’s stock traded at a more reasonable valuation (P/E ratio 15.9) which is moderately less than its earnings growth rate. I offer this to illustrate that investing in a true growth stock can still generate good returns even if the market is currently undervaluing the shares.

Even though Celgene was technically undervalued over that 3-year timeframe, thanks to earnings growth that continued above 30% per annum, shareholders would have still earned an annual return in excess of 12%. This simply illustrates the power of compounding future earnings discussed above.

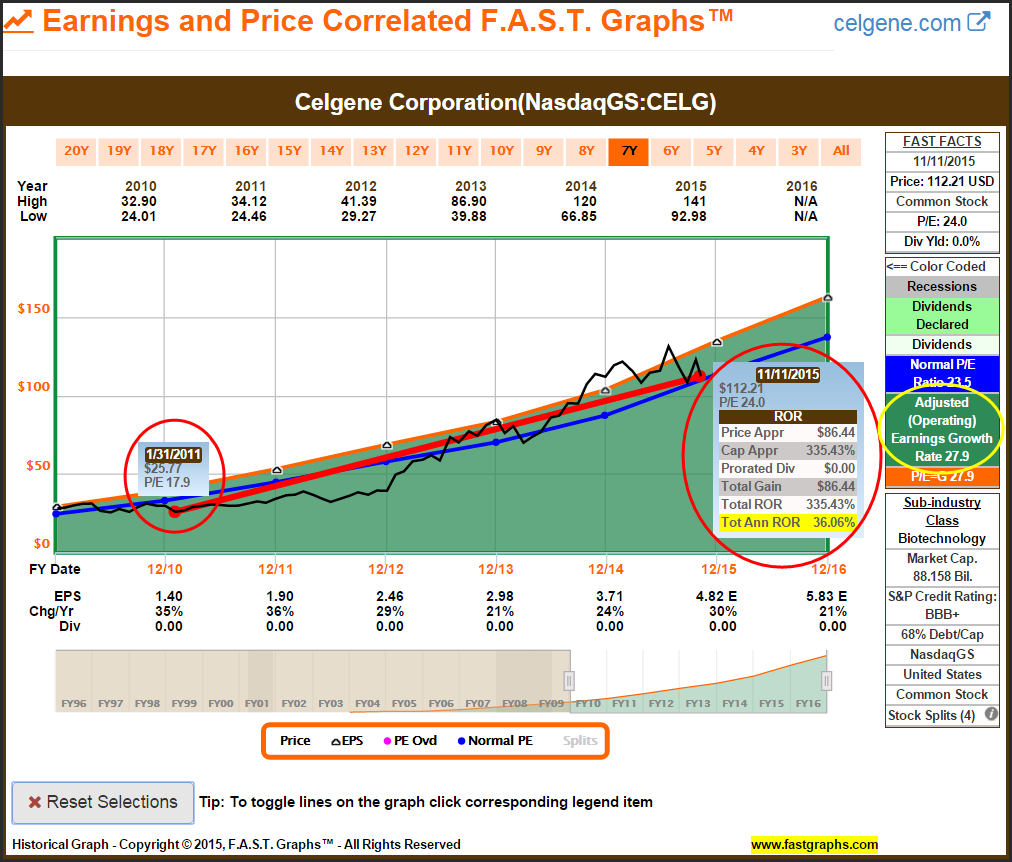

In contrast, if you had the foresight to pick up shares of Celgene on January 31, 2011 when the shares were available at a P/E ratio of 17.9, which was approximately half of its future earnings growth rate, you would have earned a total annual return of 36.06%, which was greater than its 27.9% earnings growth rate. This simply illustrates the powerful benefit of investing in a true growth stock when it is undervalued in relation to its earnings potential.

Perhaps the most important point about growth stock investing that I stressed earlier is the importance of assessing future growth potential. Pure growth stocks like Celgene do not pay dividends; therefore, investors in growth stocks must rely on capital appreciation for future returns. Consequently, when investing in growth stocks, it’s critical to apply your best judgments about the company’s future growth potential.

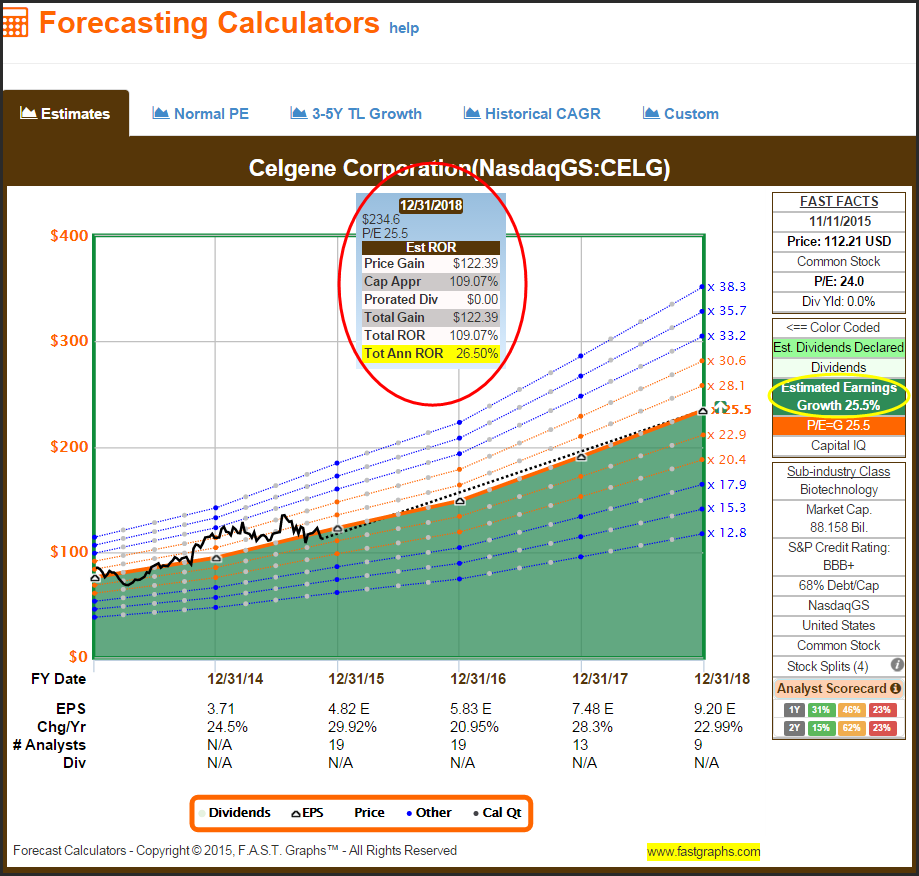

I believe a good starting point is to check consensus analyst estimates. The following forecast calculator shows that a large group of analysts expect Celgene to grow earnings at an average rate of 25.5% over the next 3 years. Assuming you consider that those estimates are reasonable, this would imply that Celgene is currently available at fair value with its current P/E ratio of 24, slightly less than its forecast earnings growth rate.

However, I never totally rely on analyst estimates, even though I consider them a good first step. If the stock passes this first look, and sometimes even if it doesn’t, if I like the company I will dig deeper. As an aside, Celgene’s stock price has recently been under pressure. I attest some of that pressure to the company’s previous high valuation, and some to what some consider a mixed recent earnings report. In other words, I’m suggesting that the recent weakness may have brought Celgene shares down to attractive long-term levels. The following article by DoctorRx offers a comprehensive and learned overview on Celgene.

Reason number 5: Growth Stocks Are Contemporary, Interesting, Exciting and Even Fun

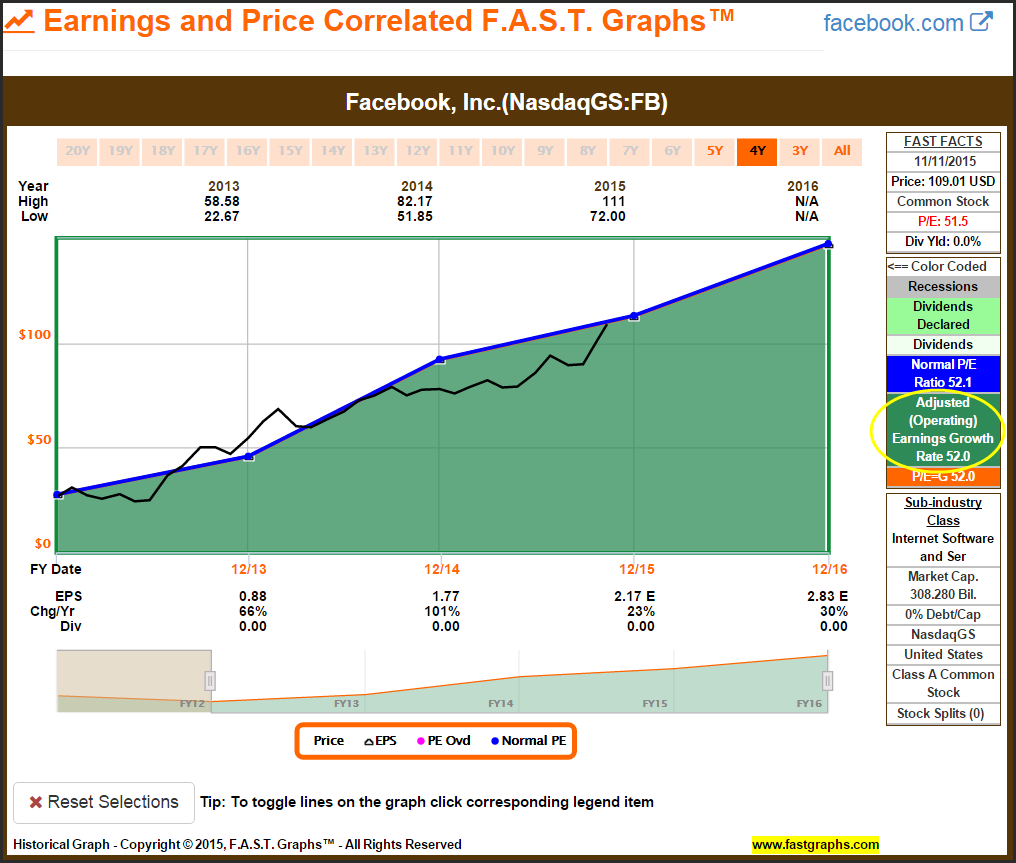

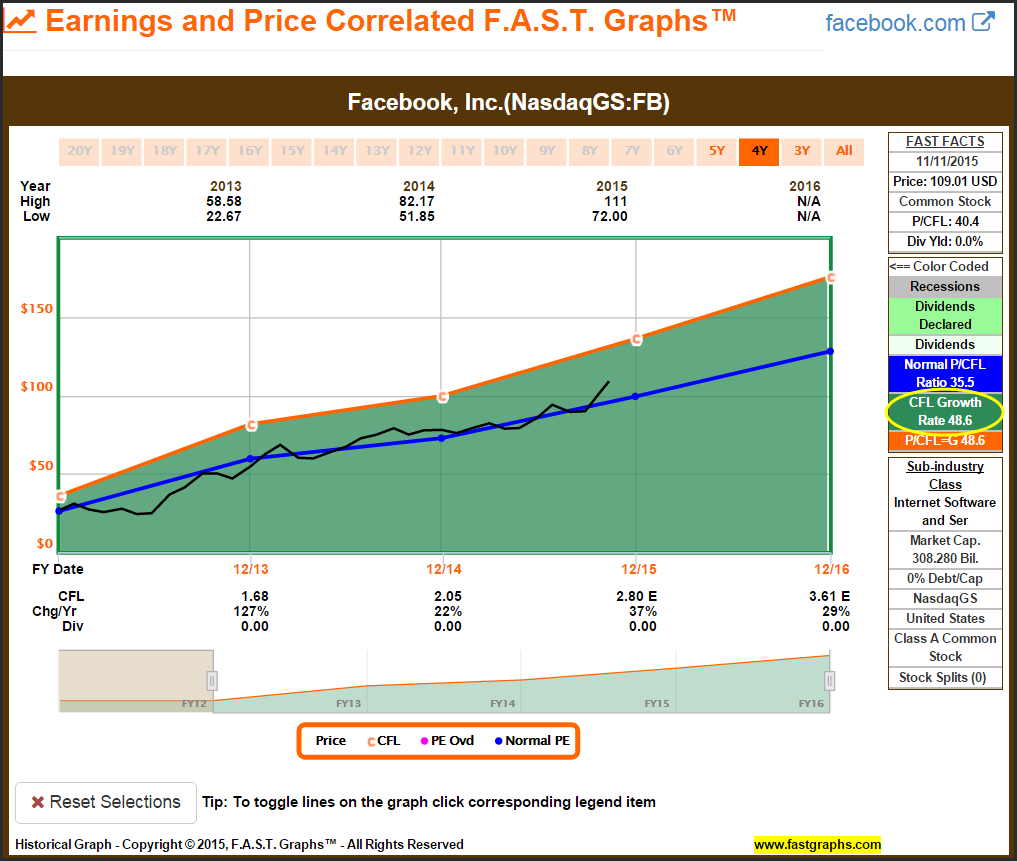

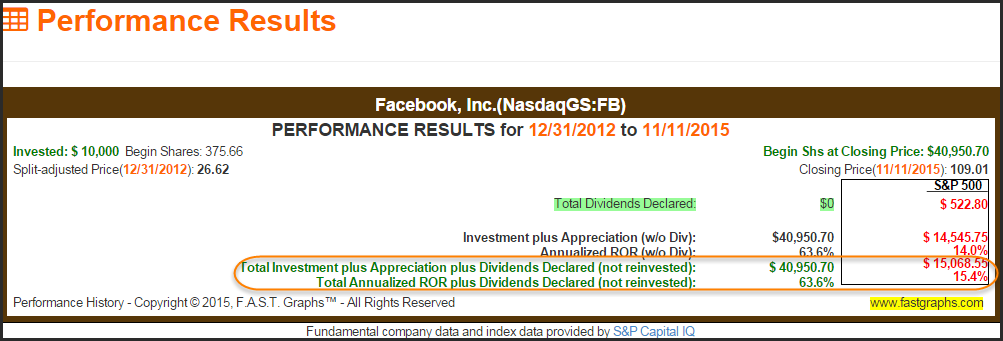

Facebook (FB) is one of the most popular growth stocks in the modern era, and for good reason. Since the beginning of 2013 the company has grown earnings at an astounding rate exceeding 52%, and operating cash flows have grown at the astounding rate of 48.6%. Since going public in May of 2012, Facebook has generated a total annual rate of return of approximately 46% for shareholders. On the other hand, had investors waited for the IPO hype to settle down and purchased the stock at the beginning of 2013, their annualized rate of return would have been 63.6% or almost 4 times greater than the 15.4% generated by the S&P 500 over the same timeframe.

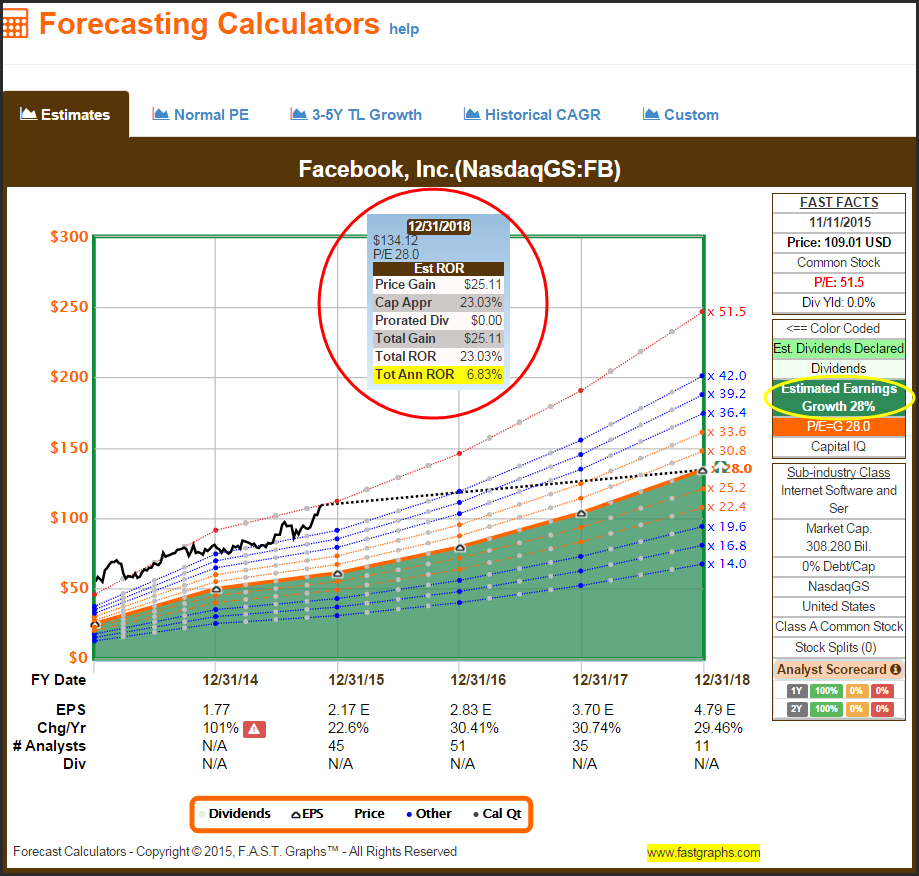

However, investing in growth stocks, although exciting, can also be tricky. Although the numbers quoted above are accurate, the close examination of the earnings and price correlated and earnings and cash flow correlated graphs below would indicate that the growth rates of both metrics are slowing down. Facebook’s year-by-year earnings and cash flow growth rates are listed at the bottom of each of the graphs below. This should not come as a surprise considering that Facebook has already grown to a market-cap exceeding $300 billion. When investing in powerful growth stocks, value investors need to keep the law of large numbers in mind. The bigger the company gets, the more difficult it becomes to sustain excessively high growth rates.

On the other hand, even a company as big as Facebook already is can be capable of continuing to grow at significantly above-average rates for a long time. However, they cannot grow as fast as they have grown in the past off of a smaller base. Facebook’s current P/E ratio of approximately 51 is consistent with the P/E ratio equal to growth rate formula based on past earnings. Likewise, Facebook’s price to cash flow of approximately 40 is also consistent with and supported by historical achievements. Importantly, growth stock investors, just like all investors, must always remember that you cannot buy the past; you can only invest for the future.

As I previously alluded to, Facebook is one of the most popular growth stocks of the modern era, and as such, they have a large following and receive a lot of attention from analysts. The following forecasting calculator is based on the consensus estimates of this large analyst base for the next 3 years. Note that the number of analysts comprising each year’s forecast is listed at the bottom of the graph. The bottom line is that consensus expects Facebook to continue to grow earnings at the strong rate of 28% per annum out to fiscal year-end 2018. Although that is clearly an excellent forecast, prudent investors need to ask themselves - does that rate of earnings growth justify a current P/E in excess of 51?

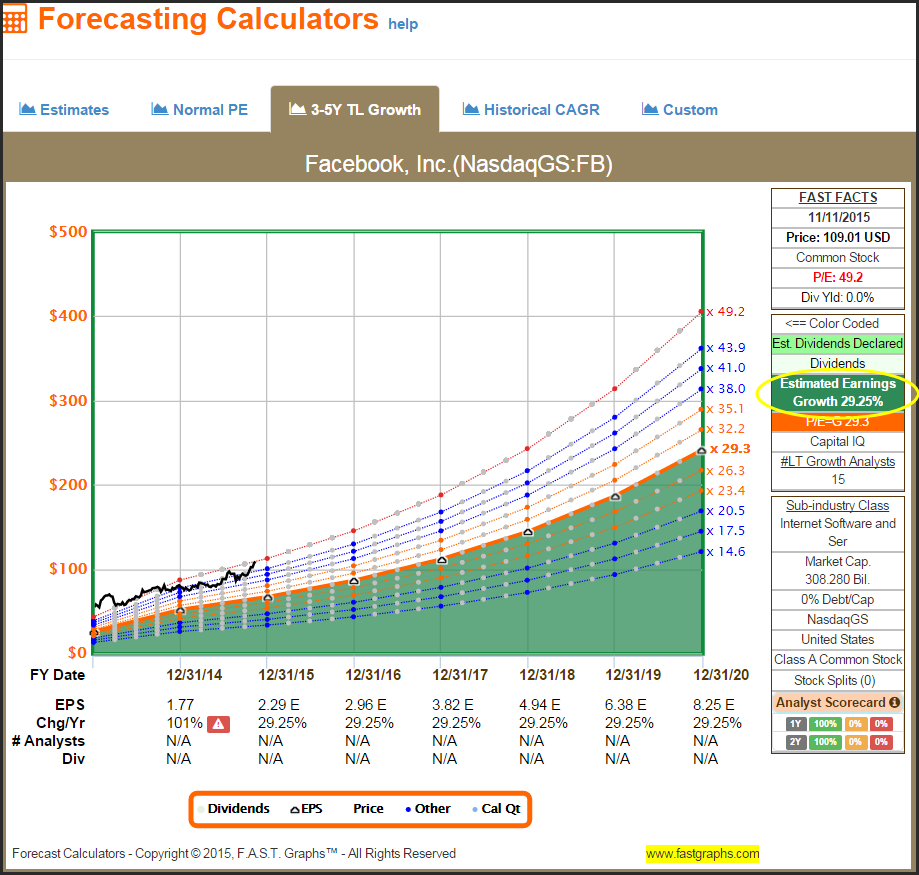

In addition to the near-term forecasts and estimates presented above, there are 15 analysts brave enough to forecast a longer-term 3 to 5 year earnings growth rate for Facebook. The long-term earnings growth rate forecast is in excess of 29% per annum. Once again, a great number, but it is not consistent with their historical 50% plus achievement.

Summary and Conclusions

Truly successful growth stocks are capable of producing game-changing long-term returns for investors. Nevertheless, investing in growth stocks can be tricky and price action very volatile in the short run. Moreover, a true fast-growing business is capable of supporting higher P/E ratios then traditional blue-chip dividend paying stocks. However, from a valuation perspective, it’s important that investors recognize that the P/E ratio of a growth stock should be relative to and related to its earnings growth potential.

Consequently, generating successful investment results is highly dependent on making reasonable assumptions about the company’s future growth. Even though the power of compounding associated with higher earnings growth rates will generate substantial future earnings, there is a limit to what you can pay today and still generate an attractive long-term return. In other words, sound valuation, even though it can be at higher levels when evaluating growth stocks, is still a critically important consideration.

Wall Street has generated the acronym GARP (Growth At a Reasonable Price) for valuing growth stocks. It is a fact that you can pay higher valuations for growth stocks, but even with growth stocks, valuations need to be reasonable enough to support future returns that are commensurate with the risk associated with investing in them. When investing in growth stocks, the future is more important than the past.

Disclosure: No positions.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.