“U.S. interest rates are already zero. Japanese interest rates are zero also. European interest rates are negative. All of these central banks have printed trillions of dollars in their respective currencies under various QE programs. They are at the point where they simply cannot print trillions more without risking political backlash or the collapse of confidence in their currencies.” – James Rickards

At 8:30 a.m. this morning, we got the October jobs number. The estimate was 185k new jobs with the consensus believing that a 150k number would be enough for the Fed to hike rates in December. The number came in at 271k. The unemployment rate dropped. There is nothing but good news in the numbers. However, for now – good news is bad.

With the Fed more likely to raise rates next month, the market moved lower, the 10-year treasury yield shot up to 2.32% (it was under 2% just a few weeks ago) and the dollar gained against the yen and the euro.

Fed members have been more vocal about a December rate increase. Markets were pricing in a 56% chance of a hike at the December meeting with the expected hike taking the Fed target to .375. After today’s jobs report, the probability of a hike will go up.

Today, let’s take a step back and jump out of the noise. Investing is relatively simple to do when valuations are low. It becomes far more challenging (and risky) when valuations are high.

As you’ll see in the data I share with you below, stocks are richly priced and forward probable 10-year annualized returns will likely be low (if history is any guide). My Philadelphia Phillies may win the World Series next year but the data points to a low probability of it happening. While my heart says go with my team, I just can’t take that bet. The same is true for the stock market today.

The Fed’s been driving the QE bus for seven years. That ride appears to be ending. We can’t expect the same response when the punch bowl is pulled away. My two cents is to stay patient and prepared to overweight equities when the valuation data is back in our favor. The next recession will likely make that happen. Until then, underweight and hedge that equity exposure (it is relatively easy to do), tactically trade fixed income and overweight liquid alternatives (long/short, managed futures, tactical all asset, etc.).

The current median PE (21.9 as of October 31, 2015) is telling us forward 10-year annualized returns will be in the 3% range (this before inflation and advisor fees). Could it be higher? Sure, but it could also be lower.

Along with the most recent valuation metrics, you’ll also find several charts that have done a good job at predicting recessions (often before they occur).

Included in this week’s On My Radar:

- Valuations and Forward 10-Year Returns

- Global Recession (Yes), U.S. Recession (No)

- Trade Signals – Excessive Optimism (ST Bearish)

Valuations and Forward 10-Year Returns

When I began my career in February 1984, the median PE of the S&P 500 Index was a low 9.7 (price to earnings). Over the next ten years, the S&P 500 grew from 157.06 to 467.14. A 10-year annualized gain of 11.52%.

The bull market picked up speed. From 1990 to 2000, the S&P 500 Index went from 353.40 to 1464.47. A 10-year annualized gain of 15.28%. Find me some more of that! The attractive entry point was a median PE of 13.9 at the beginning of 1990. Recall the 1990/91 recession? The median PE low occurred in September of that year at 11.5.

Near the end of the great bull market, median PE reached the low 20s and subsequent 10-year returns were predictably low. From 2000-2010, the S&P 500 Index averaged -0.48% per year. I’ve selected a few dates that reflect starting median PE, where the S&P 500 Index was at the start date and where it finished 10-years later. Red arrows highlight levels of high PE and low returns. Green arrows indicate low PE and high returns.

Source: Bloomberg data, CMG Investment Research, NDR median PE calculation using Worldscope data.

While the data is not perfect it, at least to me, it is telling. Valuation metrics can tell us a lot about probable forward returns but it tells us little on timing. Here is a look at the current median PE through October 2015 (all data based on reported earnings – and not Wall Street’s forward guestimates).

The number is 21.9.

Also above (boxed in blue) is a useful measure of median fair value, overvalued targets and undervalued targets for the S&P 500. In short, the market is currently overvalued (though QE, foreign capital flows, etc. could make overvalued grow to be even more overvalued. Short-term, don’t know. Long-term (say ten years), expect low returns.

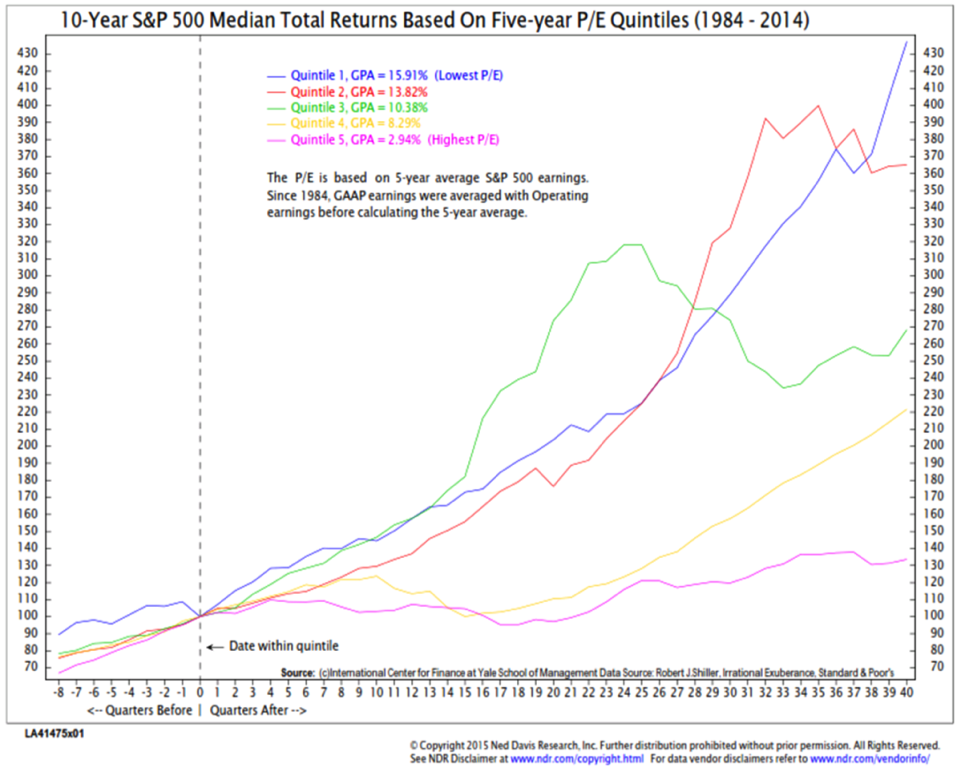

Next is a look at data compiled by NDR at my request from 1985 to present. It breaks median PE into five categories ranked from least expensive (Quintile 1) to most expensive (Quintile 5) then shows what the median 10-year return was for each category.

With a current median PE of 21.9, we sit in Quintile 5 (most expensive) – projecting 2.94% 10-year annualized returns. Just not good enough! Especially with a Fed trying to drive inflation north of 2%.

I’ve seen similar research dating back to 1925. It’s a comparable story. I think it is better to reduce and hedge equity exposure when the markets are expensively priced and increase equity exposure when the markets are inexpensively priced.

In the “what can you do about this” category: One idea is to follow the PE quintiles on a monthly basis (I tend to update the numbers in OMR monthly) and increase your exposure as the market becomes more favorably priced.

Global Recession (Yes), U.S. Recession (No)

In recessions, all sectors of the economy are affected. Some worse than others. Manufacturing and tradable goods tend to get hit the worst while the service sector tends to hold up a little better.

We are seeing a slowdown in worldwide trade. Commodities are in a severe bear market. The developed world has accumulated too much debt. Deflation is in control.

I follow several recession watch indicators. Following is a Global Recession Probability Model. This is how NDR explained this, “It looks at “Leading Indicators (CLIs) created by OECD for 35 countries. Each CLI contains a wide range of economic indicators such as money supply, yield curve, building permits, consumer and business sentiment, share prices, and manufacturing production. There are usually five to ten indicators, which vary by type and weight, depending on the country, and are selected based on economic significance, cyclical behavior, and quality. A score above 70 indicates high recession risks while a score below 30 means low risks.” Source: NDR

Note the blue line – specifically when it rises above the red dotted line at 70. Note how it tends to identify periods of global recession. Not perfect but the 86% success rate is pretty good. It is currently signaling a high probability of global recession (upper right red arrow).

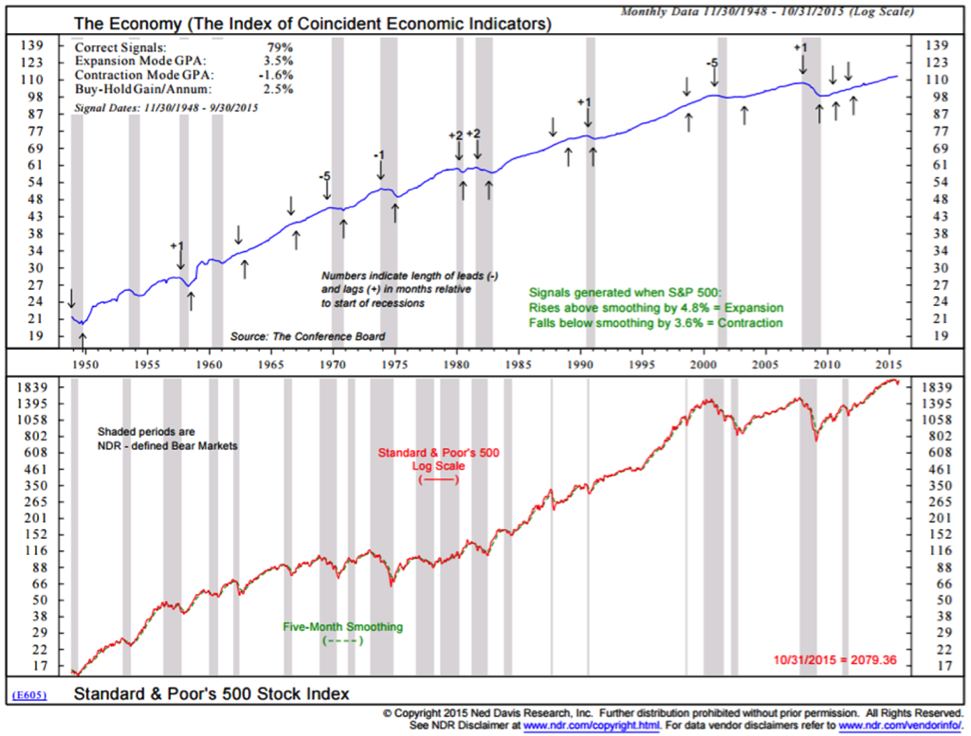

The next chart is my favorite U.S. recession prediction chart. While we are ultimately not immune to the global slowdown, right now this chart is showing no signs of a U.S. recession. Arrows mark signals. Gray shaded areas mark recessions. Let’s keep an eye out for the next down arrow.

A quick note on NDR: For years I have subscribed to Ned Davis Research. They are an independent research firm. Their clients are institutional (professional) investor clients like CMG. They are one of the most respected research firms in the business.

They offer several levels of subscription. You can contact them directly at Ned Davis Research at 617-279-4878 to learn more. Please know that neither I nor CMG are compensated in any form. I’m just a big fan of their research and their way of thinking. As a side, Ned Davis authored one of my favorite books titled, Being Right or Making Money. A great book full of sound practical advice.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here.

Trade Signals – Excessive Optimism (ST Bearish), High Global Recession Risk, No Sign of U.S. Recession

Included in this week’s Trade Signals:

Equity Trade Signals:

- CMG NDR Large Cap Momentum Index: Sell Signal on June 30, 2015 at S&P 500 Index 2063

- Long-term Trend (13/34-Week EMA) on the S&P 500 Index: Sell Signal – Bearish for Stocks

- Volume Demand is greater than Volume Supply: Sell signal for Stocks

- NDR Big Mo: Buy Signal for Stocks

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Excessive Optimism (short-term Bearish for Equities)

- Daily Trading Sentiment Composite: Excessive Optimism (short-term Bearish for Equities)

Fixed Income Trade Signals:

- The Zweig Bond Model: Buy Signal

- High Yield Model: Buy Signal

Economic Indicators:

- Don’t Fight the Tape or the Fed: Indicator Reading = 0 (Neutral for Equities)

- Global Recession Watch – High Global Recession Risk

- U.S. Recession Watch – Low U.S. Recession Risk

Click here for the link to the charts.

Concluding Thought

I have written frequently about “median PE” as a valuation measure and its strength as a tool to help us predict returns over the coming ten years. I believe a recession is probable in 2016 but a number of things could push that event further down the road (more creativity from global central bankers, tax cuts, and a grand infrastructure government rebuild plan – to name a few). We will have another recession (we tend to get one or two each decade). Not a bad thing, just an “it is” thing. Frankly, it is healthy for the long-term success of an economy. The important point is that it is in recession that we find the best buying opportunities.

The next recession may prove to be a bit more challenging. As Rickards (appropriately) points out, “U.S. interest rates are already zero. Japanese interest rates are zero also. European interest rates are negative. All of these central banks have printed trillions of dollars in their respective currencies under various QE programs. They are at the point where they simply cannot print trillions more without risking political backlash or the collapse of confidence in their currencies.”

The Fed is not favorably positioned. Keep a close eye on the recession charts.

Personal note

“Your success and happiness lie in you. Resolve to keep happy, and your joy and you shall form an invincible host against difficulties.” – Helen Keller

What a warm few days in New York City. As I raced across town from a Bloomberg interview to meeting a new reporter at the WSJ, I hoped I wouldn’t break out into a full sweat. I have a few meetings this afternoon, then home and hopefully some weekend golf with the kids.

The last two nights have been great fun though. I have eaten way too much (and the wine – too much of that as well). We took Susan’s mom to see Jersey Boys. She is a big Frankie Valli fan. It was my second time seeing the show and I’d go again. We all loved it.

“Resolve to keep happy!” That reminds me of Susan’s mom. She lives it!

Celebrating Patty’s 75th birthday are Susan, Patty and sons Jim and Rob. We are all a little slower going this morning. Let’s just say that Uncle Jim is a master at picking fine wine.

Here is a toast to the beautiful people in your life!

Wishing you a great weekend!

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG White Paper Understanding Tactical Investment Strategies you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at@askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History: Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Provided are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out of the money covered calls and buying out of the money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out of the money put options for risk protection.

Please note the comments at the bottom of this Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Captial Management Group

© CMG Capital Management Group