“Whatever the form of risk and risk measurement one uses, the important thing to know is that diversification reduces risk and can be used to reduce risks without reducing returns.”

– Ray Dalio

Ray Dalio’s “risk parity” or “all weather” investment process has been the target of recent criticism. His firm, Bridgewater, manages $155 billion. I share with you today a piece Bridgewater penned a few weeks ago. It begins, “Since there has recently been a controversy about risk parity, since we were responsible for coming up with the idea, and since we now manage more of it than any other firm, we feel a responsibility for answering people’s questions about it.”

What is happening here is that QE’s have inflated risk assets and in particular U.S. equities, fixed income and high yield. If you are 100% U.S. equities, you are happy. I just don’t know anyone who has taken that much concentrated directional risk. This reminds me of the problem (or mental depression) value managers experienced in the late 1990s.

I remember my client Roberta telling me in December of 1999 that she was transferring her account to Merrill Lynch to invest in “safe stocks”. One of those “safe” stocks was Microsoft (MSFT). Back on December 27, 1999, Microsoft (MSFT) closed at $53.60/share. At the time, MSFT was the largest company in the world. Less than a year after hitting its all-time high at the end of 1999, Microsoft’s stock price fell more than 60% from $53.60 down to $20. The dot com bubble had burst. From its lows of the dot com crash to its highs prior to the peak of the mid-2000’s bull market, MSFT failed to make much headway. It was knocked back down into the mid-teens by early 2009 at the Great Financial Crisis low.

As the world recovered in the early part of the current bull market, MSFT failed to do much, but since the start of 2013, the company has been a big winner. Now 16 years after that 1999 high, MSFT finally recovered and set new all-time high. As my friends at Bespoke recently commented, “If you’ve stuck with it over the last 16 years, congratulations on finally getting back into the black!”

I received a call in mid-2002. Roberta’s husband was on the phone asking for advice on what he should tell Roberta. Her more than $1 million had dropped to $500,000. She was then in her late 60s. She didn’t recover. Roberta got pulled into the hype and bought and sold at the wrong times. A plan designed to drive a return and risk objective may have had a better shot at keeping her on path.

As a point of full disclosure, we own Microsoft in one of our equity mutual funds. It has been a core holding for us for several years.

PIMCO’s Andrew Hoffman presented at the Asset Summit yesterday. So far it is a flat return year for stock and bonds. October’s near record advance has helped yet flat it remains. He began his presentation with three key points: 1) returns have been low, 2) they are going to be lower (PIMCO’s 10-year forecast is 4% for stocks and 2% for bonds) and 3) get diversification – you must control your downside.

The unintended consequence of QE is the suppression of interest rates and the Fed’s failure to normalize rates has set in motion a growing crisis in pensions, especially among state and local governments in the U.S. and around the world. Not to mention the damage to the savers who have been forced into risks they may not fully understand. Hey, it’s been a great five years for equities, don’t let your Roberta jump “all in”. I picked up that “all in” lingo here in Vegas.

I’m shutting the laptop down and racing to the airport. I’m really looking forward to getting home. Hope you find the comments around diversification in the Dalio piece helpful. It is balanced and easy to follow. Share it with your clients if you feel it makes sense.

Included in this week’s On My Radar:

- Dalio on Risk Parity and All Weather – Defending (Explaining) Diversification

- Recession Watch

- China – What’s Going On In China

- Trade Signals – A State of Extreme Optimism

Dalio on Risk Parity and All Weather – Defending (Explaining) Diversification

I encourage a read of the entire piece. Here are a few excerpts:

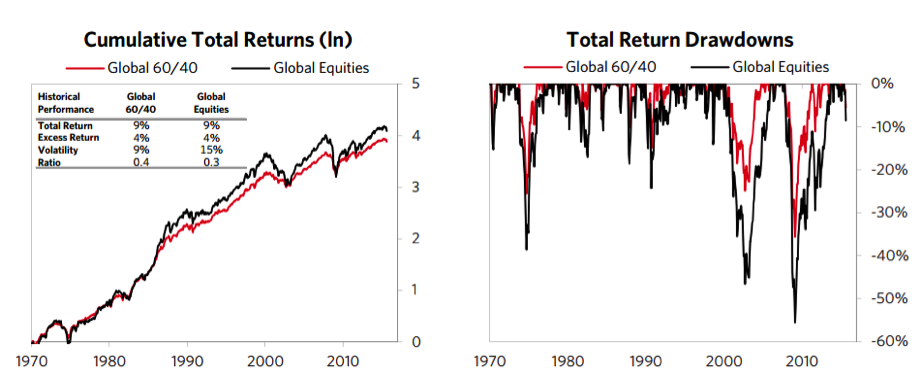

If you put 50% of your money in global stocks and 50% of your money in global bonds, over the last 20 years, the return of your portfolio would have been 98% correlated with stocks and had a return of 6.5%.

To have diversification, you would need the stocks and bonds to have comparable impacts on your portfolio. You could do that by taking more money out of stocks and putting it in bonds.

To do that over that period, you would have had to change the asset mix from 50/50 to about 25% stocks and 75% bonds. If you did that, you would have achieved your diversification and thus reduced the risk by about 3%.

You also would have reduced the return by about 50bps. On the other hand, if you levered up bonds to have a risk that was comparable to the risk of equities, the overall risk of the portfolio would have been virtually the same as the 50/50 portfolio (i.e., 7%) and the return would have been about 1.5% greater (8.0% versus 6.5%). That happened because the risk-return ratio was improved by the greater parity that was achieved. Diversification does that—i.e., it improves the ratio of return to risk.

If you understand that you can take that portfolio mix with an improved ratio and gear it up or down, then you can understand how you could deleverage the portfolio should you prefer it to have less risk rather than more return. We are just using this period and these numbers to convey the concept; any period will have somewhat different numbers, but the concept will be the same.

“Let’s look into that more carefully.

A traditional institutional portfolio has about 60% of its money in stocks and 40% in bonds. This 60/40 stocks/bonds portfolio may look diversified in capital terms, but because stocks are so much more volatile than bonds, bonds are providing virtually no diversification in such a portfolio. The returns of a global 60/40 portfolio are 98% correlated to the returns of its equity component. Also, the equity part of the portfolio had a bit higher return. As a result, the 60/40 portfolio had less risk and a bit less return than the 100% equity portfolio as shown in the chart on the left. The chart on the right shows how the risks of the “diversified” 60/40 portfolio would have done in relation to the undiversified 100% equity portfolio. As you can see, there wasn’t a heck of a lot of risk reduction – the drawdowns aren’t all that different. Such is the nature of the risk/return trade-offs as they are typically faced without the risk parity approach.

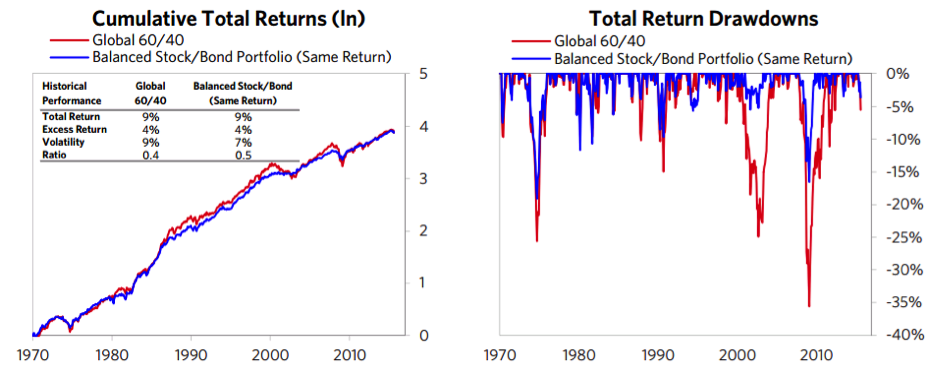

Now consider an alternative: a portfolio that levers bonds to a comparable risk to stocks, and holds equal risk in stocks and bonds with a degree of leverage in the bonds so that the expected return of the portfolio is the same as the expected return of the 60/40. Its annual and cumulative total returns would have looked like the below.

This portfolio could achieve the same return as the 60/40 with over 200bps less risk and much shallower drawdowns as seen below.

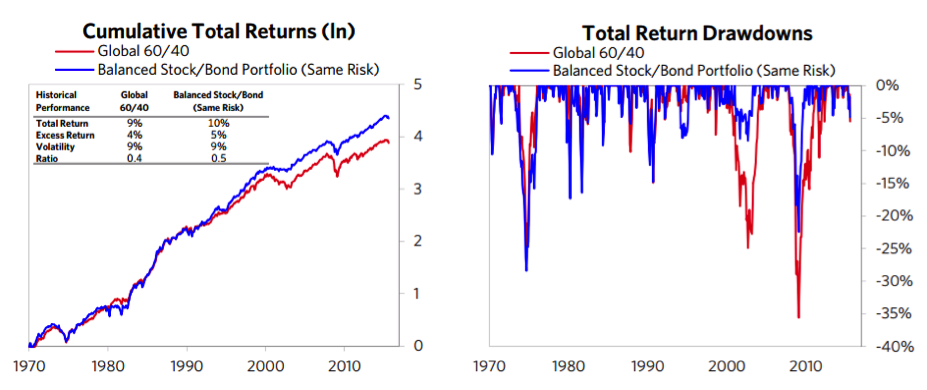

Most importantly, note that the ratio of return to risk is improved by a third (from 0.37 to 0.5). This gives the opportunity to take a little more risk, so that the risk of the portfolio is the same as the 60/40, and earn a higher return. As shown, the return of this portfolio was 100bps higher than the 60/40 with the same risk. The average size of losing periods is comparable between these two portfolios, but the balanced portfolio has less tail risk because its exposure is to two assets rather than one.

To be clear, we are just showing you these numbers in these periods to convey the concepts, not because these numbers are representative of all periods. Our main points are that a) no period is representative or knowable ahead of time, b) over any relevant time frame (e.g., 20 years, 5 years etc.—you pick it) we don’t know what will be good or bad, and c) that by altering their risk and returns of assets so that they are comparable, we can have comparable exposures to each without reducing our expected returns.

We just gave you a very simple example of just using stocks and bonds to convey the point. The same principle applies to all asset classes, though the risks steadily decrease without reducing the returns as more assets are added in this way. In other words, by apportioning the risks better by levering low risk assets and/or deleveraging high risk assets so that they have more parity and using these adjusted assets rather than just the unadjusted ones, we can create a better balanced portfolio. That’s risk parity.

There is much more in the paper. You can find it here.

Talk to your advisor representative about how much concentrated risk you might be taking and how you can smartly improve your return and risk profile.

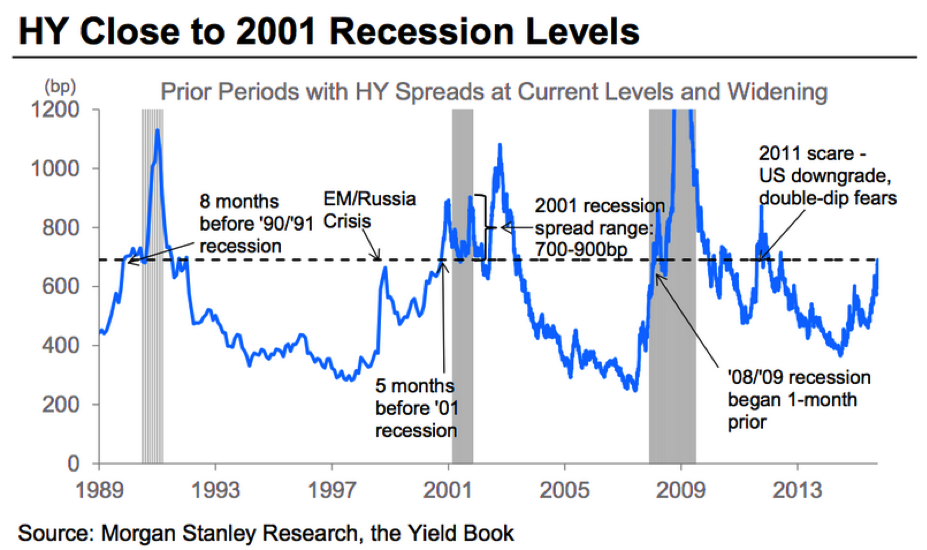

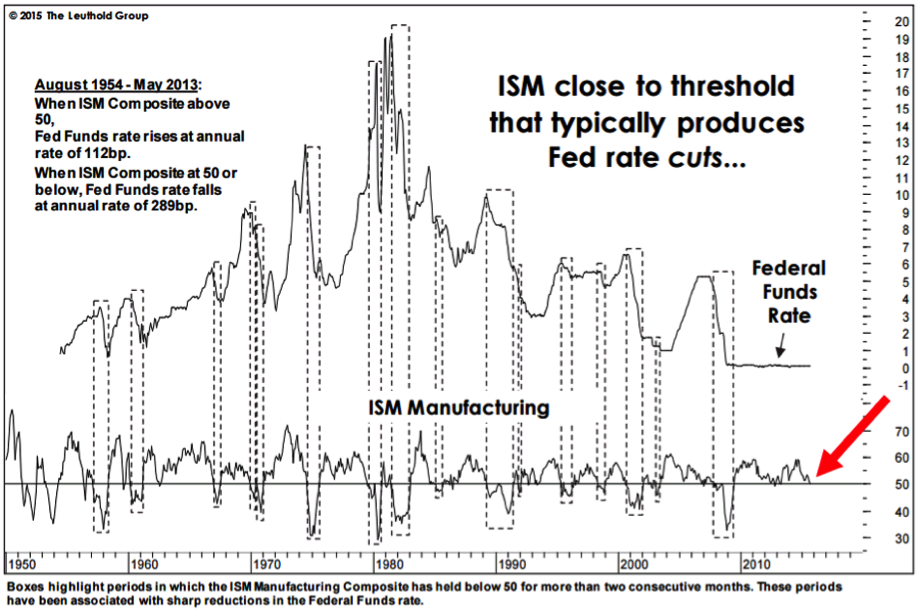

Recession Watch

I came across a few interesting charts regarding recession. To be clear, my view is that we are not in recession and 2016 presents a 50% probability of recession. My favorite recession indicator (see Trade Signals below) is currently signaling “no U.S. recession”.

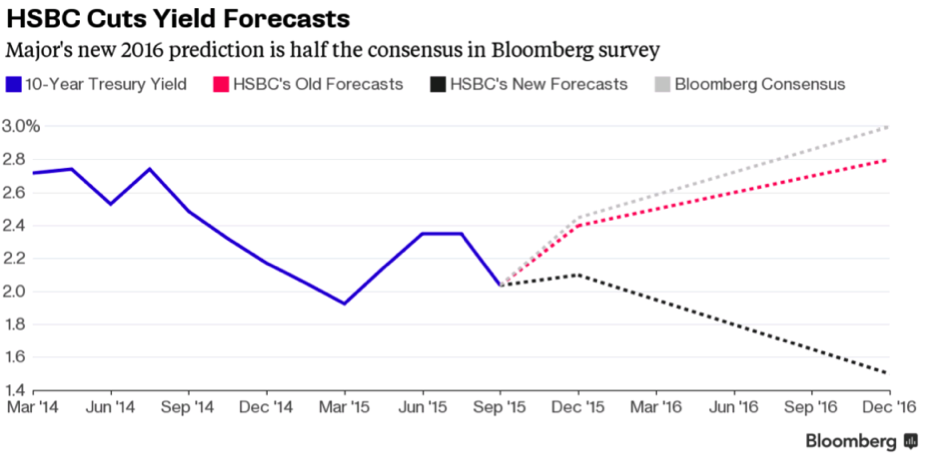

And this from Bloomberg: HSBC’s Major, Who Called 2014 Bond Rally, Cuts Yield Forecasts. Wall Street consensus estimate is for the 10-year to finish 2016 at a 3% yield. HSBC is calling for 1.5%.

Put HSBC in the Lacy Hunt camp. Global growth is slowing but growth exists none the less. Debt is the issue everywhere. Let’s keep a close eye on the recession probability charts and also watch the high yield bond market for clues. I’m in the lower for longer interest rate camp.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

China – What’s Going On In China

A short and well done article. Worth the read. China Just Upended the Rules That Governed the Global Economy for the Last 30-years

Trade Signals – A State of Extreme Optimism – 10-28-2015

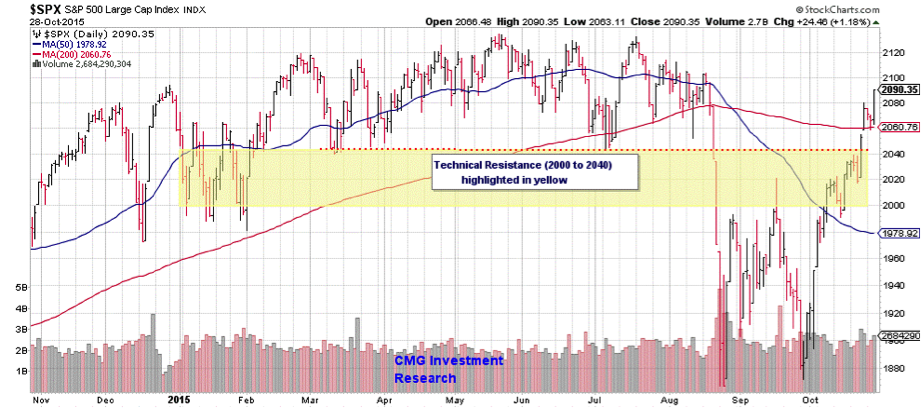

Short-term investor sentiment is now excessively optimistic which is short-term bearish for stocks. The S&P 500 Index sits today at 2090. The next important resistance sits at 2100. There is significant resistance at the prior high near 2133.

Having broken above important technical resistance (dotted red line in chart that follows) a pullback test of that breakout makes sense. Look for a correction to the 2040 area. It remains a good time to hedge.

I continue to favor a 30% weighting in equities (hedged). The market remains overvalued. My favorite “weight of evidence” indicator, the CMG NDR Large Cap Mo Index, is improving but remains in a sell. It moved to a sell signal on June 30, 2015. The S&P 500 Index closed that day at 2063.

A move above 2133, a break-out to new all-time highs, will signal a stronger environment for stocks. The hope of QE (Europe, Japan, U.S.) is once again driving the risk-on play. Indeed, a period of unusual and unprecedented central bank activity. My two cents: Continue to own equities but hedged and stay broadly diversified.

Included in this week’s Trade Signals:

Equity Trade Signals:

- CMG NDR Large Cap Momentum Index: Sell signal on June 30, 2015 at S&P 500 Index 2063

- 13/34-Week EMA on the S&P 500 Index: Sell Signal – Bearish Trend Environment for Stocks

- Volume Demand is greater than Volume Supply: Sell signal for Stocks

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Neutral (short-term Bullish for Equities)

- Daily Trading Sentiment Composite: Excessive Optimism (short-term Bearish for Equities)

Fixed Income Trade Signals:

- The Zweig Bond Model: Buy Signal

- High Yield Model: Buy Signal

Economic Indicators:

- Don’t Fight the Tape or the Fed: Indicator Reading = 0 (Neutral for Equities)

- S. Recession Watch – My Favorite U.S. Recession Forecasting Chart: Signaling No Recession

Click here for the link to the charts.

A note on NDR: You’ll find I point to NDR research from time to time. For years I have subscribed to Ned Davis Research. They are an independent research firm. Their clients are institutional (professional) investor clients like CMG. They are one of the most respected research firms in the business. NDR offer several levels of subscription. You can contact them directly at Ned Davis Research at 617-279-4878 to learn more (ask for Dan). Please know that neither I nor CMG are compensated in any form. I’m just a big fan of their research and their way of thinking. Ned Davis authored one of my favorite books titled, Being Right or Making Money. I highly recommend it.

Personal note

I’m writing to you from the Alternative Asset Summit in Las Vegas. I present this morning on moves that family offices are making in today’s market. Much of my comments today will be around diversification and overall tactical weightings.

I’m often asked about my view on the markets. I believe that investing is not a game of perfect, it is a game of risk management. That is where diversification and hedging come in. This to allow compounding to work its magic over time. Jeff Saut from Raymond James recently called the August market bottom and is now on record calling an intermediate-term top. He’s good, real good, but timing the market is, in my view, an impossible task to execute consistently. One hundred percent on target – no way.

Frankly, as with most investment risks, there is a lot of wrong on the way to being right. As Dalio points out, one period in time does not determine if you are right or wrong. Success is embedded in the long-term advantages the math of compound interest brings.

New York follows on November 5, 6 and 9 for meetings and several media interviews. I’m really looking forward to meeting Barron’s Ben Levisohn on Monday the 9th. I’m a long-time big fan of his work.

More soccer in the weekend plans. Our boys are in the league semi-final game tomorrow (high school). There will be a lot of energy at the dinner table. Fun! Next week, Susan’s mom is having an important birthday. We’ll be meeting her in the city. She was crazy about Frankie Valli and we have tickets to the Broadway show Jersey Boys.

A business trip through Seattle to Bend, Oregon to visit my business coach Jim Ruff is in the works and I’ll be presenting at the 20th Annual Global Indexing and ETFs Conference on December 6 – 8 in Scottsdale, Arizona. You can find that agenda here. Let me know if our paths will be crossing; I’d love to get a coffee with you.

The Alternative Asset Summit this past week in Las Vegas was productive. I walked away with a few investment ideas that I hope to share with you in a future letter. A deeper due diligence dive is needed first.

I had a nice breakfast this morning with the creator of ETmFs or exchange traded mutual funds. We all benefit from great creators. This is good news for you and me as we look to build stronger portfolios. The conference routine can be a grind but I’m always surprised at the new relationships that show promise. It is typically the (seemingly) unexpected ones that are most important. Kind of fun how that works.

Wishing you a great weekend! Happy Halloween!

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG White Paper Understanding Tactical Investment Strategies you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at@askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History: Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Provided are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out of the money covered calls and buying out of the money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out of the money put options for risk protection.

Please note the comments at the bottom of this Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group

© CMG Capital Management Group