As expected, the Federal Open Market Committee left short-term interest rates unchanged last week. However, the wording of the policy statement was decidedly hawkish, suggesting (contrary to market expectations) that officials are leaning toward a move on December 16. GDP growth wasn’t especially brisk in the third quarter, but that was due largely to slower inventory growth. Domestic demand remained strong, but monthly figures suggest a loss of momentum heading toward 4Q15. Ultimately, the Fed’s decision will remain data-dependent and there are many reports between now and then.

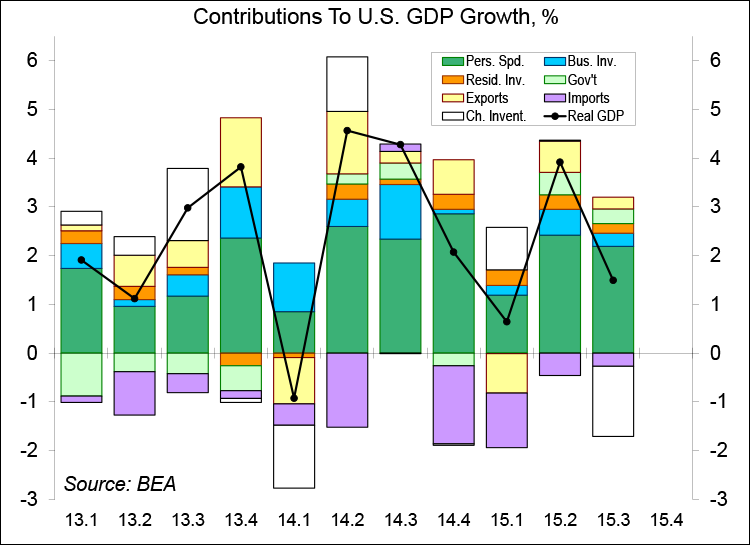

The advance estimate of GDP growth is always an adventure, as not all the pieces are known. However, the advance estimate for 3Q15 was largely in line with expectations, both in the headline number and in the details. In the monetary policy statement, the FOMC noted that “household spending and business fixed investment have been increasing at solid rates in recent months.” Well, that’s half right. Consumer spending led the way, rising at a 3.2% annual rate (down from 3.6% in 2Q15, which partly reflected a rebound from bad 1Q15 weather). Business fixed investment rose at a 2.1% pace (vs. +4.1% in 2Q15) – positive, but not quite “solid.” Homebuilding continued to advance. Exports rose at a 1.9% annual rate (+1.5% y/y), while imports, which have a negative sign in the GDP calculation, rose 1.8% (+5.5% y/y) – leaving little change in net exports. Inventories slowed sharply. These figures will be revised.

The September figures on personal income and spending were a bit weaker than expected (and expectations were soft), suggesting that consumer spending lost momentum at the end of the quarter. However, this isn’t horrible. We’ve had strong job gains over the last year and the drop in gasoline prices has added to consumer purchasing power (but a rise in rents has restrained those at the low end of the income scale).

The Fed appeared close to raising rates at the mid-September meeting, but refrained, noting that “recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term.” That phrase received a lot of attention at the time, but it was removed in the October 28 statement. The FOMC did note, however, that it would be “monitoring global economic and financial developments.”

Given the apparent “slow patch” in economic growth, and continued downside risks from abroad, why would the Fed even consider raising rates? It’s still largely about the job market. Fed officials believe that a lot of slack has been taken up in the job market in the last few years. While some slack clearly remains, officials expect to see considerably less slack in 12 to 18 months, which is when monetary policy changes should have an impact on the economy. The Fed doesn’t have to move to a neutral policy position right away, but it does have to start moving in that direction at some point.

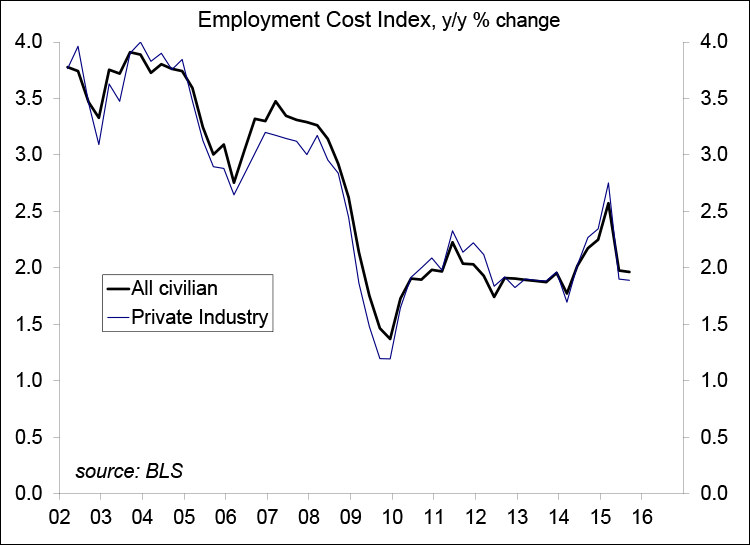

Still, there are some good arguments for waiting. Labor compensation growth has remained lackluster (cited previously by Fed Chair Yellen as a sign of economic slack) and we should see some further downward pressure on inflation.

Global economic weakness is clearly having an impact on U.S. firms that do business abroad, but it doesn’t appear to be large enough to threaten the current economic expansion (that is, expect somewhat slower growth, not a recession). Granted, global financial developments could still spin out of control, but that’s not the base-case scenario.

Given everything we know now, the bottom line is that the Fed policy statement implies that policymakers are on track to begin tightening in December. It’s up to the upcoming economic data reports to push the Fed off that path.