There is a great deal of research around investor behavior. For example, our brains notice when a group provides an answer that is different from ours, the disparity is unpleasant. For many, aligning with the group is more rewarding for the brain than being independent and correct.

This, of course, leads to herding and drives markets to become overvalued and undervalued over time. Listen to Grantham, Hussman, Arnott, Easterling or me and you walk away with probable low forward annualized return expectations of just 0% to 4% percent, before advisor fees (robo of full service) and inflation, over the next ten years. Not going to cut it for the baby boomers like me or the pensions needing to hit their 7-8% actuarial targets.

Investing is not a game of perfect. It is a game of probabilities. As Ben Graham pointed out – confidence and conviction in your facts. Behaviorally, conviction is tested every day.

This past week, I came across “What’s Going On in Your Brain?” It is a high level summary of various behavioral studies. I share some of the highlights with you today and suggest it may be a good piece to share with your clients.

“Buy when everyone is selling and sell when everyone else is buying” as Sir John Templeton said to me long ago, makes logical sense. But he added, “It will be one of the most difficult things for you to do.” I was in a room full of brokers at the Union League in Philadelphia (then age 24 and full of confidence) and Sir John took the stage. Those few words were perhaps the best advice I ever received.

Something happens to us individuals. The tendency is to emotionally misfire at the wrong time. Still 30 years later, I often hear his whisper when I find myself getting swept up in emotion created by a market move. His advice remains sound today and can be acted upon by establishing a sound process.

Towards that direction, I wrote a piece this week for Forbes titled, Using ETFs And Options To Hedge Equity Exposure In An Overvalued Market. It is a deeper dive into ways to hedge your equity exposure (establishing a sound process). I believe the market is richly priced so some form of hedging makes sense today. Should another global central banker whisper QE, like Draghi did yesterday, the markets will rally until at some point confidence in policy is lost. When? Who knows? Wish I knew. We can smartly hedge when markets are overvalued and provide a less emotional ride.

Finally, do you remember the movie “Back to the Future”? In “Back to the Future Part II,” Marty McFly travels to October 21, 2015, to save his children, yet to be born. I watched it several times and tried to get my kids to watch but hey they are experiencing many of the predictions real time. In this weeks piece, I share some of the predictions that came true, some that did not and share a few predictions from futurist Ray Kurzweil, the director of engineering at Google. He also has authored five bestselling books, holds 20 doctorates and is known as one of America’s leading inventors.

Forbes magazine called Kurzweil the “ultimate thinking machine.” What he shares with us below is way cool! I’m rooting for Ray!

Included in this week’s On My Radar:

- What’s Going On in Your Brain? Common Investor Biases and Where They Come From

- Bull Market or Bear Market

- Back to the Future – October 21, 2015 Arrived

- Trade Signals – At Technical Resistance, ST Sentiment is Neutral

What’s Going On in Your Brain? Common Investor Biases and Where They Come From

I came across a great piece from Credit Suisse authored by Michael J. Mauboussin and Dan Callahan, CFA. It is about human behavior and investing. I write often about the counterintuitive nature of investing and how investors tend to buy and sell at the wrong times. Yet, in these missteps opportunity is created.

Here are a few highlights:

In recent decades, psychologists, economists, and neuroscientists have worked together to understand how our behaviors depart from the standards of normative economic theory and why exactly we have a proclivity to do so.

Scientists now have technology to observe brains of individuals as they decide and have crafted experiments to compare behaviors of people with normally functioning brains with those who had their brains altered through stroke, surgery or disease. This research has lifted the veil on the mental processes behind our choices. Some of the findings include the following:

- Humans are social and generally want to be part of the crowd. Studies of social conformity suggest that the group’s view may shape how we perceive a situation. Those individuals who remain independent show activity in a part of the brain associated with fear.

- We are natural pattern seekers and see them even where none exist. Our brains are keen to make causal inferences, which can lead to faulty conclusions.

- Standard economic theory assumes that one discount rate allows us to translate value in the future to value in the present and vice versa. Yet, humans often use a high discount rate in the short term and a low one in the long term. This may be because different parts of the brain mediate short- and long-term decisions.

- We suffer losses more than we enjoy gains of comparable size although the magnitude of loss aversion varies across the population and even for each individual based on recent experience. As a result, we sometimes forgo attractive opportunities because the fear of loss looms too large.

Concluding: The challenge now is to create processes and procedures that manage or mitigate the biases that arise from these tendencies. (Emphasis mine)

Here is the link to the full piece. If you’re like me you’ll find yourself nodding your head at many of the findings. Ugh – we humans.

Bull Market or Bear Market

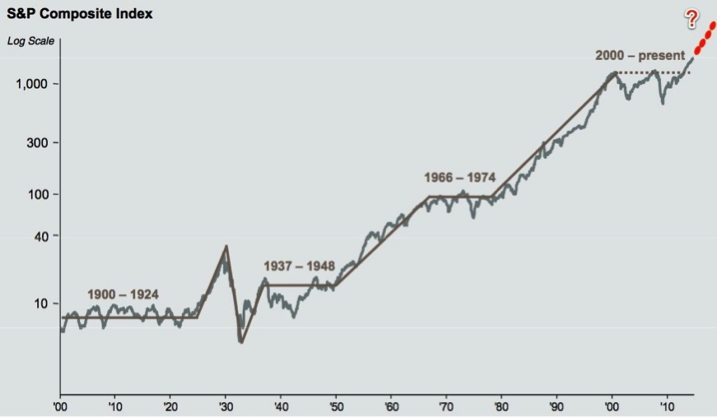

Next I share with you a shortened version, and several well done charts, from a piece Henry Blodget, founder of Business Insider, did titled, “Market History is Calling, and It’s Saying Stock Performance Will be Crappy for Another 10 Years”. Hat tip to John Mauldin (Outside the Box).

Long-term valuation analysis suggests that we are still working through the aftermath of the highest level of stock market valuation in history — the peak of the tech bubble in 2000 — and that this workout process will take at least another five to ten years.

Over the past century, the market has gone through distinct “bull” and “bear” phases. These, on average, are 10 to 25 years each. Specifically:

- A 29-year bull market from 1900-1929

- An ~20-year bear market from 1930-1950

- An ~15-year bull market from 1951-1966

- An ~15 year bear market from 1967-1982

- An ~18 year bull market from 1982-2000

- An ~? year bear market from 2000-?

Some people think the latest “bear” phase ended in 2009. They also think we’re in the middle of a glorious “bull” phase again.

The bulls look at this chart and point out that we moved sideways for ten years after 2000, say that was plenty and predict that stocks will now forge even higher for years as the new bull market continues.

Bears, meanwhile, look at the chart and see a temporary, Fed-fueled spike in the middle of a long bear market that they believe will see at least one more big downtrend and correction (likely lasting years) before it is done.

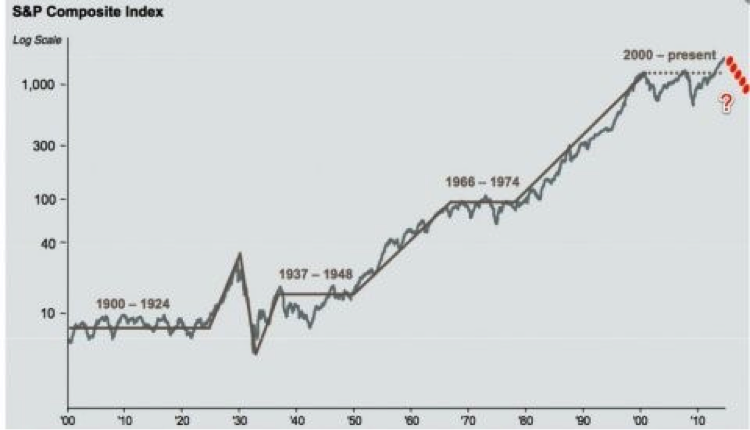

So who’s more likely to be right? Well, let’s add more information to that chart.

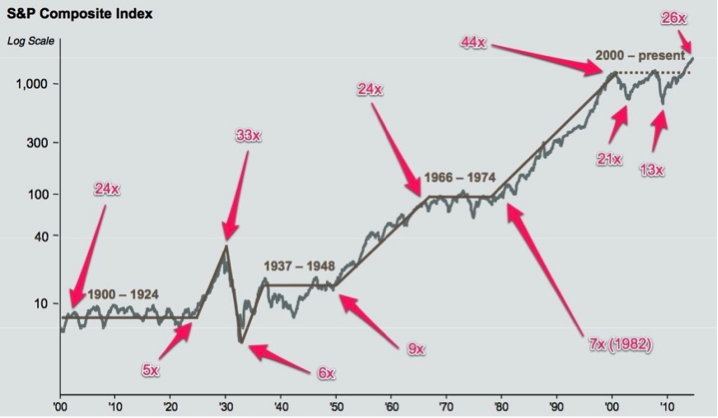

Throughout history, stock prices have loosely gravitated around the “fundamentals” of the underlying companies — namely, earnings. Specifically, stocks have traded in a range of 5X cyclically adjusted earnings (at bear market lows) to 44X earnings (at the peak of the biggest bull market in history — the one that ended in 2000). The “average” P/E ratio over this period, meanwhile, has been about 15X.

When you add P/E ratios to the charts above, you quickly notice a pattern:

- Sustained bear market periods have begun when the P/E is very high (~25X+).

- Sustained bull market periods, meanwhile, have begun when the P/E is very low (5X to 9X).

In other words, sustained bull markets begin when investors are so disgusted by stocks — and so pessimistic about the future of stocks — that they’ll pay only 5X to 9X earnings for them. Sustained bear markets begin when investors are so giddy with excitement about stocks and the prospects for stocks that they’ll happily pay 25X earnings or more for them.

So, what does all this tell us?

Nothing conclusive, unfortunately. No one knows the future.

Let’s make a couple of observations about our current situation:

- First, even after the recent market wobble, stocks are still more expensive than they have been at any time in the past century with the exception of 2000 and 1929 and we know what happened after those years. For the “new bull market” to continue indefinitely, the market’s P/E would have to continue to keep rising toward the P/E at the historic 2000 market peak — which, it is worth noting, was followed by a devastating crash.

- Second, if we are indeed in the middle of a new bull market, the bear market “workout period” following the 2000 peak would have been one of the shortest in history and we were starting from the highest valuation in history, by a mile.

Blodget concludes, “Unless something has changed that makes the past 115 years of market history irrelevant (always possible, but probably not likely), it would not be surprising if the biggest bull market peak in market history was followed by one of the biggest bear market workouts in history — one that, perhaps, might last as long or longer than any major workout period to date.”

My two cents is to use valuation metrics as a risk trigger tool. When the market is expensive, like today, hedge your equity exposure and/or raise some cash. The cost is small relative to the risk that comes in expensively priced markets. Also, when interest rates are low today, increase your weightings towards alternatives (defined as anything other than traditional stock and bond buy and hold). You want to be in a position to take advantage of the opportunities inexpensively priced markets bring you. Mainly, much higher forward annualized returns.

Back to the Future – October 21, 2015

This is quick and fun. If, like me, you watched Marty McFly and Doc Brown 26 years ago in the movie Back to the Future, I think you’ll enjoy this:

Here are some of the predictions the movie got right:

- Brain controlled wireless video games

- 3d movies

- Handheld tablet computers

- Video conferencing

- Virtual reality wearable technology

- Wall mounted widescreen TVs with multiple TV channels

- Biometric scanners – fingerprint scanners as door locks

- Power clothing (self-drying and self-tying shoelaces-launching in 2016)

Here are some that they got wrong:

- Flying cars

- Ubiquitous fax machines (now a relic of the past)

- Hoverboards – they would have been way cool

- Fusion – net positive energy fusion

- A time machine

This from Peter Diamandis – A few amazing things we have today that they missed:

- Rapid, cheap whole genome sequencing and editing – We now have the ability to sequence a full human genome for under $1,000. The technology is developing at 3x the rate of Moore’s Law. We now have the ability to cheaply and precisely edit the genome with CRISPR/CAS 9. This will open up a new frontier of health and longevity that will have enormous implications on the future.

- 3D Printing – You can 3D print just about anything these days from 300 different materials… Plastics, metals, concrete, chocolates, human cells… Complexity is free and scalability is inherent.

- Emergence of AI – We are in the early days of artificial intelligence. Tens of billions of capital are being poured into an AI “arms race” over the last decade. One fun recent example is Tesla’s “autopilot” software upgrade that just came out – their AI can drive you autonomously on the highway.

- On-Demand Economy – Amazon is working on same-day delivery mechanisms (possibly using drones). Uber has become ubiquitous as the simplest, most reliable way to get around.

- GPS – We really take for granted how good the GPS units in our phones really are. They receive up-to-the-second traffic data, route us to the shortest path, and even give us “street view” or satellite imagery to investigate what a place looks like before we get there.

- Private Spaceflight and Hyperloop: While Back to the Future flaunted flying DeLoreans, I’m proud of where we are with private spaceflight and the start of Hyperloop.

Here is a few future predictions from Ray Kurzweil:

- Governments, businesses, and economists have all been caught off guard by the geopolitical shifts that happened with the crash of oil prices and the slowdown of China’s economy. Most believe that the price of oil will recover and that China will continue its rise. They are mistaken. Instead of worrying about the rise of China, we need to fear its fall; and while oil prices may oscillate over the next four or five years, the fossil-fuel industry is headed the way of the dinosaur. The global balance of power will shift as a result.

- LED light bulbs, improved heating and cooling systems, and software systems in automobiles have gradually been increasing fuel efficiency over the past decades. But the big shock to the energy industry came with fracking, a new set of techniques and technologies for extracting more hydrocarbons from the ground. Though there are concerns about environmental damage, these increased the outputs of oil and gas, caused the usurpation of old-line coal-fired power plants, and dramatically reduced America’s dependence on foreign oil.

- The next shock will come from clean energy. Solar and wind are now advancing on exponential curves. Every two years, for example, solar installation rates are doubling, and photovoltaic-module costs are falling by about 20 percent. Even without the subsidies that governments are phasing out, present costs of solar installations will, by 2022, halve, reducing returns on investments in homes, nationwide, to less than four years. By 2030, solar power will be able to provide 100 percent of today’s energy needs; by 2035, it will seem almost free — just as cell-phone calls are today.

- For decades, manufacturing was flooding into China from the U.S. and Europe and fueling its growth. And then a combination of rising labor and shipping costs and automation began to change the economics of China manufacturing. Now, robots are about to tip the balance further.

- Foxconn had announced in August 2011 that it would replace one million workers with robots. This didn’t occur, because the robots then couldn’t work alongside human workers to do sophisticated circuit board assembly. But a newer generation of robots such as ABB’s Yumi and Rethink Robotics’ Sawyer can do that. They are dexterous enough to thread a needle and cost as much as a car does.

- China is aware of the advances in robotics and plans to take the lead in replacing humans with robots. Guangdong province is constructing the world’s first “zero-labor factor,” with 1,000 robots which do the jobs of 2,000 humans. It sees this as a solution to increasing labor costs.

- The problem for China is that its robots are no more productive than their counterparts in the West are. They all work 24×7 without complaining or joining labor unions. They cost the same and consume the same amount of energy. Given the long shipping times and high transportation costs it no longer makes sense to send raw materials across the oceans to China to have them assembled into finished goods and shipped to the West. Manufacturing can once again become a local industry.

- It will take many years for Western companies to learn the intricacies of robotic manufacturing, build automated factories, train workers, and deal with the logistical challenges of supply chains being in China. But these are surmountable problems.

- What is now a trickle of manufacturing returning to the West will, within five to seven years, become a flood.(Source)

- He said that in the 2030s, health care and technology will merge so millions of microscopic robots will swim in our bloodstream. He said in the 2020s, 3D printing will reach a level of sophistication at which we will all print out our clothes.

- The cost of technology is falling by about half each year. These trends will greatly change human life in the next few decades, especially in the intersection of information technology and biotechnology. In particular, he said technology is getting smaller, and we are about two decades away from microscopic robots, or nanobots, being introduced into the human bloodstream. They will be able to identify and attack diseases and repair damaged parts of the human body.

- Kurzweil said human genes are simply strings of data, and the goal is to rebuild an outdated piece of bio-software.

- Because of such advances, Kurzweil said he believes immortality is within the grasp of humanity. In the middle of the next decade, he said, human life expectancy will start to grow by at least a year every year, so it will fade into the distance as we age.

- Quoting Ray, “Fundamentally, I think information technology will overcome poverty, disease, aging — many of the things that have challenged humanity throughout history.”(Source)

I’m rooting for Ray!

Trade Signals – At Technical Resistance, ST Sentiment is Neutral

Investor sentiment has moved from “extremely pessimistic” (which is short-term bullish for the market) to neutral; however, the daily sentiment indicator is nearing “extreme optimism” (which would be short-term bearish for the market). Evidence suggests it is best to buy when everyone is selling and sell when everyone is buying (at points of sentiment extremes). No extreme today – let’s call it neutral.

The weight of evidence continues to suggest to that the market has entered into a cyclical bear market. Extreme pessimism suggested a bounce and that bounce has occurred (the S&P 500 rallied back up to where it broke down in late August). Watch for moves to extreme optimism especially when price action has reached important technical resistance. Investor optimism is growing again.

A quick summary on the signals:

- The CMG NDR Large Cap Momentum Index remains in a sell (June 30, 2015 at S&P 500 Index level 2063).

- You’ll also see that the 13/34-week moving average indicator remains in a downtrend. Overall, trend evidence remains negative for equities.

- The Zweig Bond model remains bullish on high quality bonds.

I remain in the hedge/sell the rallies camp. The market remains overvalued, the Fed wants to raise rates, global growth is slowing and a probable recession is near. This would all be less of an issue if the market was attractively priced. It is not. See “Valuations, Forward Returns and Recession”.

Included in this week’s Trade Signals:

Equity Trade Signals:

- CMG NDR Large Cap Momentum Index: Sell signal on June 30, 2015 at S&P 500 Index 2063

- 13/34-Week EMA on the S&P 500 Index: Sell signal

- Volume Demand is greater than Volume Supply: Sell signal for Stocks

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Neutral (short-term Bullish for Equities)

- Daily Trading Sentiment Composite: Neutral (short-term Bullish for Equities)

Fixed Income Trade Signals:

- The Zweig Bond Model: Buy Signal

- High Yield Model: Buy Signal

Economic Indicators:

- Don’t Fight the Tape or the Fed: Indicator Reading = 0 (Neutral for Equities)

- U.S. Recession Watch – My Favorite U.S. Recession Forecasting Chart: Signaling No Recession

Click here for the link to the charts.

For years I have subscribed to Ned Davis Research. They are an independent research firm. Their clients are institutional (professional) investor clients like CMG. They are one of the most respected research firms in the business. NDR offer several levels of subscription. You can contact them directly at Ned Davis Research at 617-279-4878 to learn more (ask for Dan). Please know that neither I nor CMG are compensated in any form. I’m just a big fan of their research and their way of thinking. Ned Davis authored one of my favorite books titled, Being Right or Making Money. I highly recommend it.

Personal note

I went to a physical therapist last week. Last February, acting more like 23 instead of 53, I ruptured my left ACL while skiing. The upside is that the ACL injury opened up a window of opportunity to take care of my right hip.

Anyway, I stopped going to therapy in June and continued to work out on my own. With ski season nearing, I thought it a good time to check in with a pro. Physical Therapist “PT” Mike asked me how I thought I was doing and I said I think I’m about 80% there. I’m not even close and PT Mike is now kicking by butt. Thought I was close. I had no idea. I’ve got two months to get in form. A nice goal.

When you think about robo technology, I just don’t think there is anything that will replace the value of a trusted advisor. Sometimes we all need a coach, advisor, counselor and friend. Sometimes we all need a guy like PT Mike to kick us in the butt. Some individuals can do it on their own. Many can’t. Some will use one type of platform and others may use both. If you are an advisor, think about embracing the robo technology for some clients (a low fee offering) and maintaining your full service business. Know that your trusted advice will never be replaced. We people need people.

I have to say I feel like a kid in the candy store with my new hip. Technology has advanced and so has the procedure. It was an easy fix for me. If you are bone-on-bone like I was, know that there is hope. If you are considering a hip fix, I’d be happy to share what I know with you.

I’m flying to Las Vegas next Tuesday to present at the Alternative Investor Summit on ETFs and Strategy. There is a lot going on in the liquid alt space and this is one of the bigger conferences of the year. New York follows on November 9 and 10. A business trip through Seattle to Bend, Oregon to visit my business coach Jim Ruff is in the works and I’ll be presenting at the 20th Annual Global Indexing and ETFs Conference on December 6 – 8 in Scottsdale, Arizona. You can find that agenda here. Let me know if our paths will be crossing; I’d love to get a coffee with you.

Many weekend soccer games await, the uniforms are washed (teenage boys can smell) and the car is gassed up and ready to go. Here is a toast to you and your family and all the miles you put in to make it great.

Here is my Matthew – Thus the ACL. I’m done trying to chase this. Click here for a video.

Have a great weekend!

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG White Paper Understanding Tactical Investment Strategies you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at@askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History: Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Provided are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out of the money covered calls and buying out of the money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out of the money put options for risk protection.

Please note the comments at the bottom of this Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc (or any of its related entities-together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual Funds involve risk including possible loss of principal. An investor should consider the Fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM and the CMG Tactical Futures Strategy FundTM is contained in each Fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM and CMG Tactical Futures Strategy FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually mange client assets; and, (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (i.e. S&P 500 Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500 Composite Total Return Index (the “S&P”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard & Poor’s chooses the member companies for the S&P based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10 year period would decrease a 10% gross return to an 8.9% net return. The S&P is not an index into which an investor can directly invest. The historical S&P performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professionals.

Written Disclosure Statement. CMG is an SEC registered investment adviser principally located in King of Prussia, PA. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at (http://www.cmgwealth.com/disclosures/advs).

© CMG Capital Management Group