The Bureau of Economic Analysis will report its initial estimate of third quarter growth on Thursday. There’s always plenty of uncertainty in the advance estimate. The BEA does not have a complete picture and will have to make some assumptions about foreign trade and inventories in September. These figures will be revised, perhaps a lot, which is why it is more important to focus on the story behind the numbers.

Real GDP, according to the BEA, is “the value of the goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes.” Consumer spending accounts for 68% of GDP. Business fixed investment makes up about 13%; government consumption and investment about 18%. Exports account for 13%, but you have to subtract imports, which are about 15%. Inventories are perhaps the most confusing component. GDP is a flow ($/time), while inventories are a stock ($). The change in inventories ($/time) contributes to the level of GDP. The change in the change in inventories contributes to GDP growth. In other words, faster inventory growth adds to GDP growth, while slower inventory growth subtracts. This can get quite noisy from quarter to quarter, so one should focus on Final Sales (GDP less the change in inventories) or better yet, Final Sales to Private Domestic Purchasers (GDP less the change in inventories, net exports, and government).

Consumer spending growth appears to have been strong in 3Q15. The contraction in energy exploration should be less of a drag on business fixed investment. Inventory growth was very strong in the first two quarters of the year, but is widely expected to slow in 3Q15 (and perhaps a bit more in 4Q15). It’s hard to say by how much. We don’t have a complete picture for the quarter and figures have to be adjusted for price changes. Hence, there is a lot of uncertainty in the headline GDP figure.

While GDP is a quarterly figure, there is a GDP estimate near the end of every month. First comes the advance estimate (based on incomplete information), then the 2nd estimate (formerly called the “preliminary” estimate), then the 3rd(formerly called the “final” estimate) – each revision representing a more complete picture. Once a year, in late July, the figures undergo annual benchmark revisions, based on revised source data (and sometimes include methodology changes, such as when intellectual property products were added to business fixed investment in 2013). One should not get too wedded to any particular GDP estimate. The numbers will change. The story behind the numbers, the strengths and weaknesses of individual sectors typically doesn’t change a lot (but we’ve seen some large revisions in recent quarters).

We like to say that this was not your father’s recession we went through in 2008-2009. Rather, it was your grandfather’s depression. In the Great Depression, policymakers – especially the Federal Reserve – made all the wrong moves. This time, they got things mostly right. The one clear mistake was a premature move to austerity, which slowed the recovery. That’s not to say that austerity is never justified. Rather, to raise taxes or cut spending in a struggling economic recovery, when interest rates are low and the central bank has little leeway to offset contractionary fiscal policy, is the definition of “foolish.”

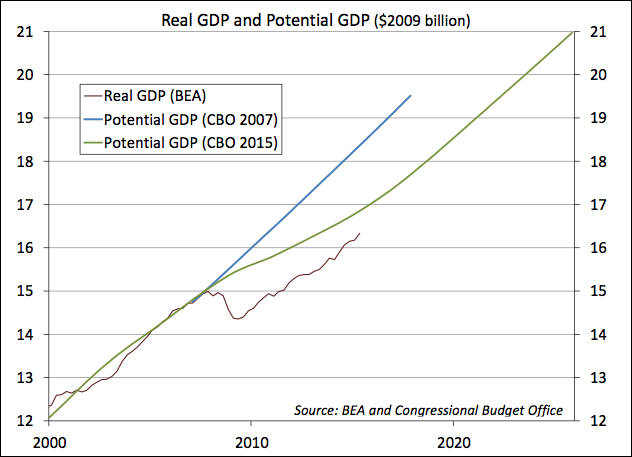

GDP is now a lot closer to its potential, but that’s largely because the path of potential GDP has fallen (reflecting a lower pace of capital investment). We’re still 11% below the pre-recession trajectory, with no expectation that we will get back to that previous path. Moreover, slower population growth and a slowdown in productivity growth may keep us on a much slower growth path in the years ahead – adding to fears of secular stagnation. The Fed can attempt to prevent this by keeping the pedal to the metal for a longer period.