- Can Household Finances Be Saved?

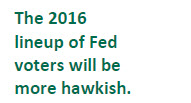

- Divisions Within The Fed Are Rising

- The Canadian Election

I’ve tried to instill that same sensibility in my children, with little success. Instead of making do, they struggle with the notion of doing without. They have to have the latest gadgets; they want new clothes each season; and don’t even talk to them about eating leftovers.

To be fair, they haven’t had to cope with a Great Depression. (Thank you, Mr. Bernanke.) But deferred gratification is essential to lifelong solvency. While the data suggest that Americans may be saving more than we thought, most aren’t saving nearly enough.

Many retirees and workers approaching retirement in the United States have limited financial resources. The 2013 Survey of Consumer Finances from the Federal Reserve points out that Social Security provides most of the retirement income for about half of U.S households age 65 and older. The same survey also notes that 29% of households age 55 and older do not have retirement savings or a defined benefit (DB) plan.

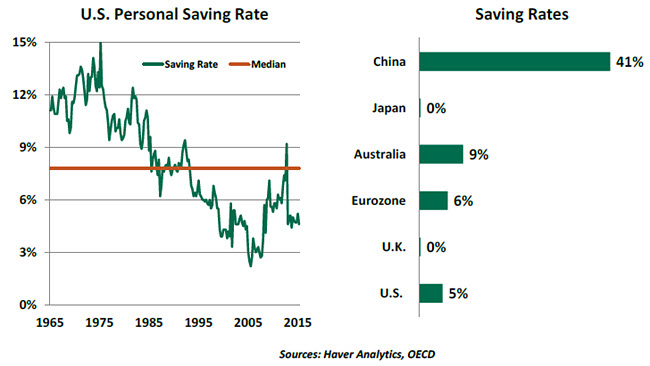

To many, a root cause of this is that Americans simply spend too much and save too little. The U.S. personal saving rate trended down to 2.2% of disposable income in mid-2005 from a high of 11.5% in 1982. The good news is that the saving rate has changed course in the last 10 years, but it is still far below the historical median.

U.S. household saving lags the pace seen in other countries. Differences between markets can be attributable to measurement challenges and to the presence of publicly provided retirement benefits. (The more generous these are, the less that households will save on their own.) Yet some countries clearly have the right idea on this front, Australia’s mandatory retirement contributions being a good example. And some have the wrong ideas: the United States has neither a generous public retirement program nor a deep reservoir of private saving.  To be fair, the most common measure of savings may understate the financial resources of households. In U.S. national income accounts, personal saving is the residual after subtracting taxes and spending from personal income. The personal saving rate is the ratio of personal saving to disposable income (personal income minus taxes).

To be fair, the most common measure of savings may understate the financial resources of households. In U.S. national income accounts, personal saving is the residual after subtracting taxes and spending from personal income. The personal saving rate is the ratio of personal saving to disposable income (personal income minus taxes).

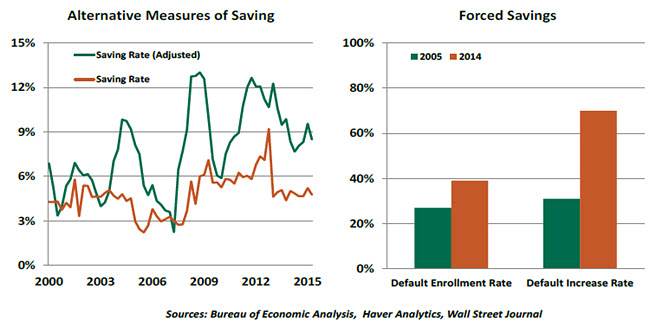

Personal saving excludes a number of elements that may ultimately provide support for retirement. Contributions to defined contribution (DC) plans are counted as saving, but gains in the value of those plans are not. Taxes paid on realized capital gains reduce the saving rate, but the realized capital gains do not count towards savings. The value of durable goods and home equity are also not considered. Including these items changes the picture of saving, as shown by the green line in the chart below.

Including asset price appreciation in a saving rate is somewhat controversial. Paper gains have not been realized and transferred to actual resources and can certainly shift over time. Some suggest that adding unstable components to the personal saving estimate is an overstatement, but ignoring them entirely seems to be an understatement.

Even after adjusting for potential understatement, the U.S. saving level remains low. The Center for Retirement Research offers estimates that a savings level of 14% would be ideal for the country as a whole. We have a long way to go before hitting that mark.

Fortunately, the retirement saving landscape is changing in a subtle way. Perhaps without realizing it, many households are on a track to a better financial future. Saving through programs at the workplace is considered by many as the most effective means to boost the nest eggs of employees. In the past 10 years, a large number of firms have implemented programs to nudge savings of employees.

Vanguard Group reports that a significant number of firms have increased the default contribution rate to retirement plans. Typically, 3.0% of employee compensation had been automatically diverted to retirement plans. A significant number of firms have raised this to 4.0% or more. Also, firms have also put in place auto-escalation policies for current and new workers so as to increase retirement contribution rates gradually, unless employees opt out. These developments suggest that a higher U.S. saving rate in the years ahead is likely.

Vanguard Group reports that a significant number of firms have increased the default contribution rate to retirement plans. Typically, 3.0% of employee compensation had been automatically diverted to retirement plans. A significant number of firms have raised this to 4.0% or more. Also, firms have also put in place auto-escalation policies for current and new workers so as to increase retirement contribution rates gradually, unless employees opt out. These developments suggest that a higher U.S. saving rate in the years ahead is likely.

It would certainly be ideal if households had a better understanding of what kind of resources they need for retirement and what levels of saving are needed to reach their goals. But these are complicated calculations and easy to defer. So the craft of engineering the correct outcomes through features in DC plans has a great deal of appeal.

In sum, savings in the United States are probably more ample than suggested by the personal saving rate. And measures are in place to improve saving over time. But there remains an important gap between what is available and what is needed. Additional thrift will certainly be required; so kids, eat your leftovers.

Hard to Interpret

It has been difficult to clearly understand the thinking of the Federal Reserve this year. To be fair, incoming information has created significant room for debate and doubt. But it appears that internal disagreements within the Federal Open Market Committee (FOMC) are further complicating an already complicated situation.

Over the past decade, the Fed has used forward guidance as regular part of its policy. By promising not to change rates until a particular date, or “for the foreseeable future,” the FOMC steers expectations and keeps longer-term interest rates low.

Earlier this year, the Fed moved away from such characterizations, choosing to depict its stance as “data-dependent.” In dropping calendar-based guidance, the Fed led onlookers to think that a rate hike was imminent, with the exact timing to be determined by incoming information. But now that several FOMC meetings have passed without any alteration in policy, markets began to wonder exactly what data would be sufficient to prompt change.

Policy is always data-dependent, so this is an honest way of depicting the Fed’s posture. But in the absence of additional clarification, the current form of communication is leading to an overemphasis on individual data points, which results in greater market volatility. The most- honest phrasing is proving to be the least helpful.

The uncertainty has been heightened by a sense that different FOMC members are interpreting the data in different ways. Prior to the September FOMC meeting, eight reserve banks submitted requests to raise the discount rate. This suggests that a plurality of Fed presidents were ready, at that time, to tighten monetary policy.

While some of these leaders must have been placated by discussions at the FOMC meeting itself (the decision to stay at zero passed by a vote of 9-1), others have become increasingly vocal about the case for raising rates. In response, two of the Fed’s governors recently offered public comments defending the decision to stay at zero.

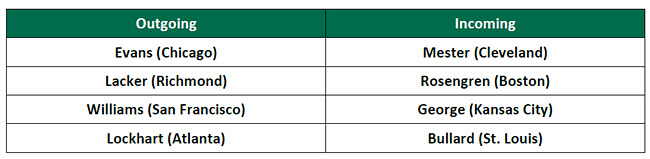

The dynamic within the FOMC could get more contentious with the annual rotation of voting members that will occur on January 1. Presidents of the regional reserve banks take turns at this on a set schedule.

During her last year as a voter in 2013, President Esther George was a consistent dissenter. Unemployment is considerably lower now, so chances are strong that she will vote against keeping interest rates near zero next year. President James Bullard’s recent speeches have pressed the case for higher rates. And President Loretta Mester arrived at the Cleveland Fed after serving as the research director at the Philadelphia Fed. Her boss there, Charles Plosser, was a vocal hawk.  There are two open seats on the Fed’s Board of Governors, and two individuals have been nominated for them. Community banker Allan Landon was proposed in January, and Kathryn Dominguez of the University of Michigan was proposed in July. The Senate Banking Committee has thus far declined to schedule a hearing on either one of them, which is highly disappointing. It seems unlikely that either of these individuals will have the opportunity to affect the Fed’s leanings anytime soon.

There are two open seats on the Fed’s Board of Governors, and two individuals have been nominated for them. Community banker Allan Landon was proposed in January, and Kathryn Dominguez of the University of Michigan was proposed in July. The Senate Banking Committee has thus far declined to schedule a hearing on either one of them, which is highly disappointing. It seems unlikely that either of these individuals will have the opportunity to affect the Fed’s leanings anytime soon.

So the new crowd might press harder for rate hikes sooner, and potentially more often, than others might prefer. A decision to remain close to zero could attract multiple dissents and pit the Reserve Bank presidents against the Board of Governors. Markets would probably not appreciate rising levels of institutional stress at the Fed, which has been a steadying hand for most of the past 30 years.

Janet Yellen may certainly use her powers of persuasion and leadership to forge consensus. But next year’s FOMC minutes may make for especially interesting reading.

Canada’s New Government Shifts Economic Priorities

As the autumn leaves change color across North America, Monday’s parliamentary election ushered in a new season in Canadian politics. Led by the youthful Justin Trudeau, the Liberal Party rode a late voter surge for change, ending 10 years of rule under Stephen Harper’s Conservative Party.

New Prime Minister Trudeau is no stranger to politics – his father Pierre led Liberal governments for the better part of 1968-1984. However, his status as a relative newcomer to public office has many asking: what policies will change, and how will they affect the Canadian economy?

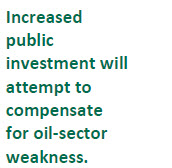

Already hit by low oil prices, Canada’s energy industry will face increased scrutiny under the new government. Trudeau’s aggressive stance on the environment and support for First Nations involvement will increase headwinds for the nation’s energy and mining industries. The new PM supports pipeline projects to the east (Energy East) and south (Keystone XL) but opposes west-bound projects, as these would increase oil tanker traffic off the Pacific coast.

While the Conservatives are ardent supporters of the Trans-Pacific Partnership, Trudeau has vowed to consult parliament before deciding whether to approve the pact. The Liberals have traditionally supported free-trade agreements and given a weaker left-wing New Democratic Party, Trudeau will likely give his approval. The deal would help reduce Canada’s trade dependence on the United States, which accounts for about 75% of Canadian exports.

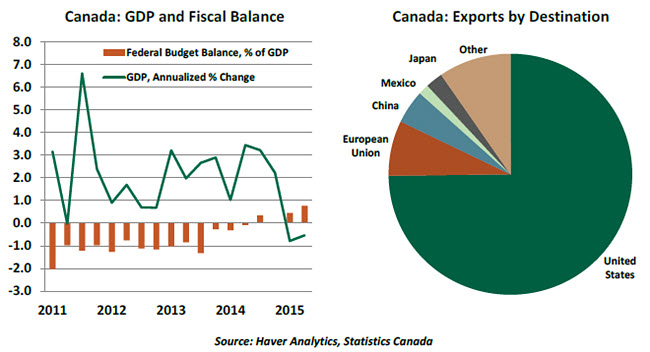

Fiscal policy will be more expansionary under the new government in an effort to boost sluggish growth. Notably, the Liberal plan calls for C$17 billion in public infrastructure spending over the next four years and increased taxes on wealthy Canadians. The plan aims to return the budget to a small deficit over the next three years, while federal debt-to-gross domestic product (GDP) declines to 27% by 2019-20.  The election’s impact on the Bank of Canada (BoC) is likely to be small. Holding the policy overnight rate steady at 0.50% on Wednesday, the BoC reduced its GDP growth forecasts for 2016 and 2017 (now 2.0% and 2.5%, respectively). It also noted that the economy has rebounded from the oil-driven technical recession seen in the first half of this year. Increased infrastructure spending will help pick up economic slack, but the boost will not be immediate. As such, the BoC isn’t likely to raise rates until 2017 as the economy gradually shifts toward non-energy exports in the coming years.

The election’s impact on the Bank of Canada (BoC) is likely to be small. Holding the policy overnight rate steady at 0.50% on Wednesday, the BoC reduced its GDP growth forecasts for 2016 and 2017 (now 2.0% and 2.5%, respectively). It also noted that the economy has rebounded from the oil-driven technical recession seen in the first half of this year. Increased infrastructure spending will help pick up economic slack, but the boost will not be immediate. As such, the BoC isn’t likely to raise rates until 2017 as the economy gradually shifts toward non-energy exports in the coming years.

The expected November 4 announcement of PM Trudeau’s cabinet will give further indications of the new government’s policy priorities.

(c) Northern Trust