Introduction

Reinvesting your dividends received from high-quality dividend growth stocks is a great, relatively conservative and proven way to build wealth over the long term. This is especially true and appropriate for investors in the accumulation phase that are planning for future retirement. Accumulating additional shares of dividend growth stocks can, and will, provide an increasing and eventually larger stream of income available at retirement when income is needed most.

There are two primary strategies that can be implemented to reinvest the dividends provided from a portfolio of dividend growth stocks. First of all, most high-quality dividend growth stocks investors have the option of enrolling in formal company dividend reinvestment programs, also known as DRIP plans.

When the investor formally enrolls in a dividend reinvestment plan, they will no longer directly receive their dividends in cash. Instead, the dividends will be automatically used to purchase additional shares of stock in the company. Also, if the company you own does not have a formal DRIP plan, many brokerage houses offer their own plans that will allow you to reinvest your dividends directly back into the company.

The second strategy for investors interested in investing their dividends is informally known as “collect and invest.” With this strategy, the investor allows their dividends to accumulate and then personally picks and chooses which companies they will add this fresh and received dividend capital to. The central idea behind this strategy is to avoid reinvesting dividends into high-priced or overvalued stocks and opting instead to reinvest accumulated dividends only into low-priced or undervalued stocks.

Which strategy is the best way to reinvest dividends?

One of the most commonly asked questions I receive from dividend growth investors is which or what is the best way to reinvest their dividends. The following is a classic example of this question that I was recently asked:

“Reinvesting Dividends? Currently for both my taxable and IRA accounts I reinvest all my dividends automatically back into those companies every quarter. Is this the best approach or should I reinvest these funds in stocks that are currently “fair valued” every quarter?”

In my personal opinion, both strategies are viable and attractive. Moreover, there are advantages and disadvantages to both. Automatically reinvesting dividends each quarter takes advantage of the underlying and proven principal of dollar cost averaging - but with a slight twist. I will elaborate more on the twist I’m referring to later in the article. The primary benefit of this principle is that it takes all decision-making, thought and emotion out of the equation.

If the price of the stock you are automatically reinvesting in is high (overvalued or expensive), your dividends automatically buy fewer shares. If the price of the stock you are automatically reinvesting in is low (undervalued or cheap), your dividends automatically buy more shares. Consequently, your money is in essence being more aggressive when prices are low and more conservative when they are high. In the long run, your average price will balance or average itself out. I am a big believer in dollar cost averaging; in over my almost 50 years in finance, I have seen it work quite well many times.

On the other hand, collecting dividends each quarter and then reinvesting them only in stocks that you feel are currently fairly valued is also a great strategy. In theory, you would be more likely to be making sound and more profitable investments with each dollar available. However, both judgment and time are required.

In other words, collecting dividends and then allocating them only to the stocks you feel are appropriate is both more research-intensive and time-consuming. Furthermore, both judgment and emotion are involved. Personally, this is the approach that I prefer and utilize. However, I am a professional that analyzes investments all day - every day. Therefore, I have the time, experience, and with all due humility, the knowledge to most effectively reinvest the dividends I gather into what I consider the best valued choices available at the time.

Consequently, I do not think either option is right or wrong. Moreover, I do not consider either option necessarily better or worse than the other. The best choice ultimately comes down to the one that each individual investor is most comfortable with and capable of executing. In the long run, I have seen both approaches succeed.

The Difference Between Dollar Cost Averaging And DRIP Investing (Dividend Reinvestment Plans)

DRIP investing plans, in essence, take advantage of the concept or principal of dollar cost averaging. However, there is a subtle difference based on the purest definition of dollar cost averaging. In its purest form, dollar cost averaging is mostly about applying a disciplined investment strategy. The discipline comes from investing a specific or equal amount of money over specific and consistent timeframes. For example, an investor might commit to investing $100, or $500, or $1000 each and every month for years. Here is the precise definition of 'Dollar-Cost Averaging ((DCA)) courtesy of Investopedia:

“The technique of buying a fixed dollar amount of a particular investment on a regular schedule, regardless of the share price. More shares are purchased when prices are low, and fewer shares are bought when prices are high.”

A DRIP plan (dividend reinvestment plan) works in the same disciplined fashion as dollar cost averaging, and therefore, offers similar benefits. However, there is a primary difference, but it is subtle in nature. When you are automatically reinvesting your dividends, the amount of money you are investing each quarter is not necessarily fixed.

If you are investing in Dividend Champions or Aristocrats, for example, your dividends are, in theory, increasing each year. Therefore, the total amount of money you are automatically reinvesting each year changes. You are still applying the discipline of investing on a regular schedule (quarterly), but the total amount of money you are investing varies each year. Nevertheless, you are still applying and receiving the benefit of buying more shares of stock when prices are low, and fewer shares when prices are high. Consequently, the averaging out aspect still applies. Here is the precise definition of a Dividend Reinvestment Plan courtesy of Investopedia:

“ DRIP' A plan offered by a corporation that allows investors to reinvest their cash dividends by purchasing additional shares or fractional shares on the dividend payment date.”

Reviewing the Theoretical Advantages and Disadvantages of DRIP versus Collect and Invest

I have already thoroughly covered the advantages of applying an automatic dividend reinvestment plan (DRIP). Nevertheless, the primary advantage is worth repeating and elaborating on. Every time an investor is required to make an investment decision, they are simultaneously placed in the position of making a potential mistake.

For example, a stock that they believe is undervalued based on current earnings, could be an illusion if future earnings collapse. In other words, their judgment and analysis could be in error. Furthermore, investors always face the innate emotional fight or flight response. In other words, it’s often hard to invest in a stock after its price has fallen precipitously. Even though it might be the right long-term decision, it’s often quite difficult to pull the trigger.

Consequently, the primary advantage of a DRIP program is that it takes advantage of the principle of dollar cost averaging, while simultaneously taking out the risk of judgment and emotion. However, the disadvantage is that it’s often hard for many investors to stick to the discipline. For example, it is often tempting to shut the DRIP program off during a major bear market. Ironically, bear markets have historically been the best time to become aggressive - not defensive.

In contrast, there can be significant advantages gained by applying the collect and invest strategy. In theory, if effectively applied, the collect and invest investor is never investing any of their money when stocks are overvalued. Therefore, in theory at least, their long-term returns, including higher future potential income, will consequently be greater. The opportunity provided by investing every dollar, regardless of its source, at sound and attractive valuations can be profound. In other words, every dollar you invest is being aggressive and buying the maximum number of shares of stock during times when prices are low (undervalued). In the long run, only investing at sound valuation will pay off handsomely.

However, this strategy as previously indicated is much more research and time-intensive. It takes time, effort and skill to be sure that all of your investments are being made at sound and attractive valuations. Additionally, as also previously stated, the individual investor also has to be effectively dealing with their emotions. Even though it has historically been profitable to invest during the throes of a bear market, it is also emotionally difficult to do. Most people don’t like to invest when they are scared or unsure.

Examples of Collect and Invest

In order to illustrate the advantages of the concept “collect and invest” I will utilize two blue-chip Dividend Champions. Both are extremely high-quality companies with similar historical growth characteristics of earnings and dividends. Both of these examples also have calendar year ending fiscal years.

However, I consider one of them extremely overvalued and the other attractively valued. Additionally, both of these blue-chip dividend stalwarts are currently offering yields just a little over 3%. Importantly, this exercise is hypothetical, and therefore, for illustrative purposes only.

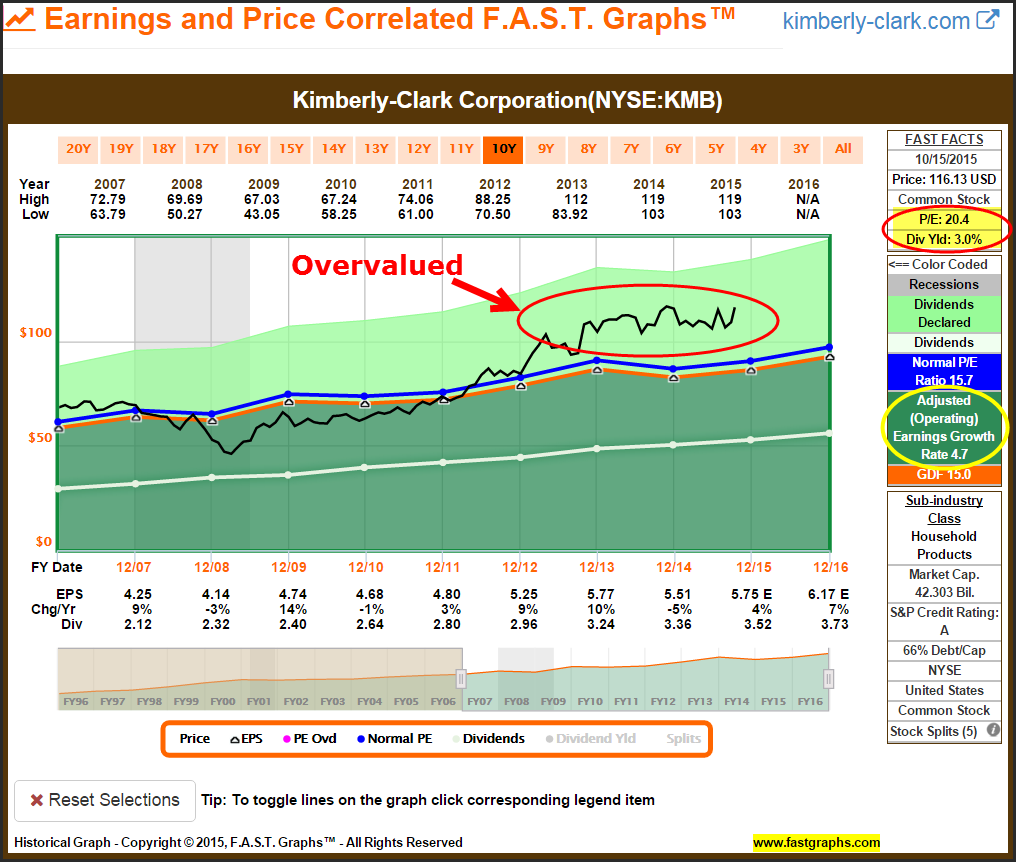

My first example is the Dividend Champion Kimberly-Clark Corporation (KMB), which is the company I consider currently overvalued. Kimberly-Clark currently trades at a blended P/E ratio of 20. With this in perspective, this means that I would have to pay $20 to buy one dollar’s worth of Kimberly-Clark’s earnings in order to purchase the source of my dividends. Since I consider that a high price to pay for their earnings, I would not be inclined to organically add to this position with fresh capital at current valuation.

To me, the dividend I would receive from Kimberly-Clark on the next payment would be fresh capital. Therefore, based on my judgment of current valuation, I would not be excited about having my Kimberly-Clark’s next dividend automatically reinvested. Regardless of the advantages of the principle of dollar cost averaging, I see this as a clear and vivid choice to not invest at this time. On the other hand, I would also interject that in order to successfully collect and invest, it’s important to have a fairly valued alternative available when I receive and collect my dividend.

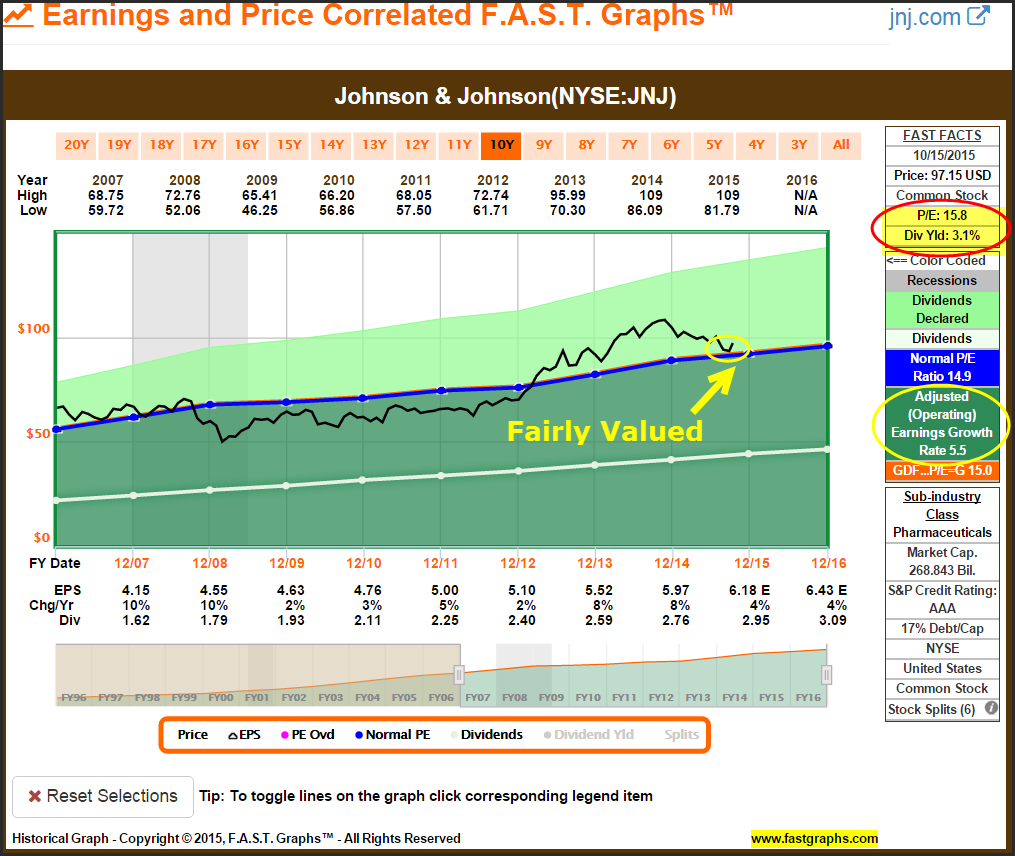

Fortunately, I do believe I have a viable alternative in Johnson & Johnson (JNJ) with similar quality characteristics and historical fundamental metrics. Johnson & Johnson is also a Dividend Champion that possesses very similar historical earnings and dividend growth rates as Kimberly-Clark. However, the primary difference is that Johnson & Johnson appears fairly valued currently. Consequently, I would rather add fresh capital to Johnson & Johnson at this time, than I would to Kimberly-Clark.

In order to achieve a similar current yield on new shares purchased, I would only be required to pay $15 for one dollar’s worth of Johnson & Johnson’s earnings. That is a 25% discount to what I would have to pay to purchase more Kimberly-Clark shares. But best of all, I am not giving up any growth potential in either earnings or dividends. Therefore, I am much more comfortable and motivated to purchase Johnson & Johnson today than I am Kimberly-Clark.

The collect and invest strategy provides me the opportunity to make these kinds of strategic investment decisions. I don’t need to be defensive with my dividend distribution from Kimberly-Clark; instead, I can aggressively invest it into Johnson & Johnson at a much more attractive valuation. I consider this an advantage over a DRIP strategy. However, it does require me to spend the time and effort to conduct analysis, which is a disadvantage to a DRIP plan. Nevertheless, I believe that with this example, I would do better in the long run by collecting and investing into a better valued alternative.

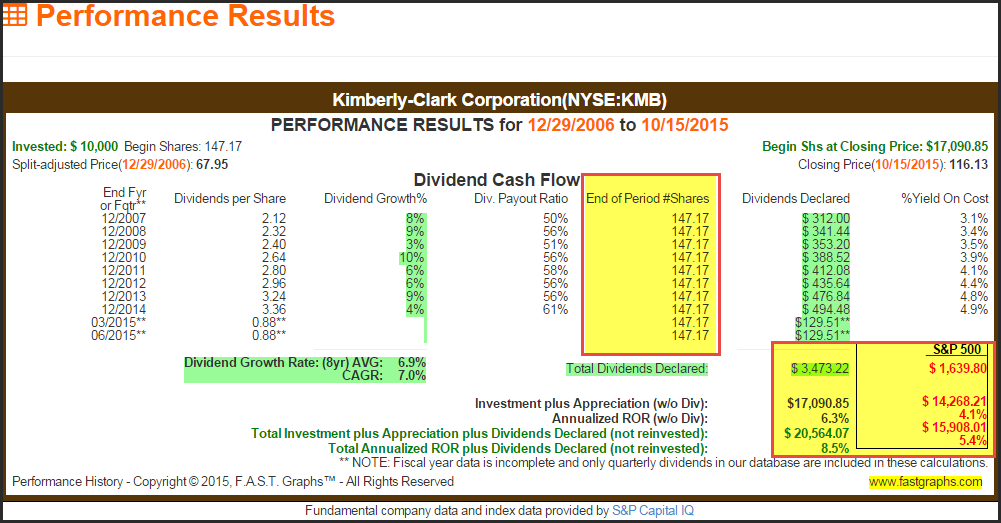

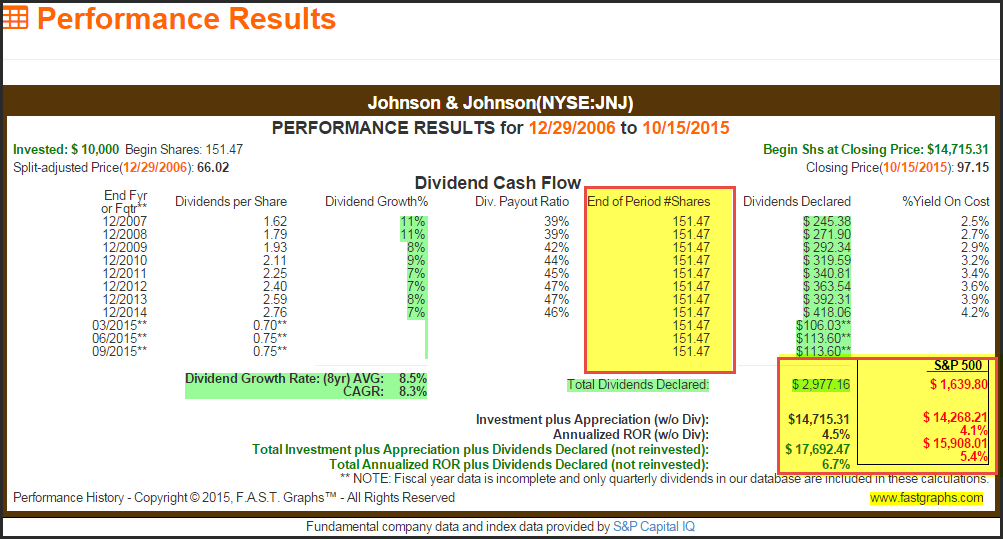

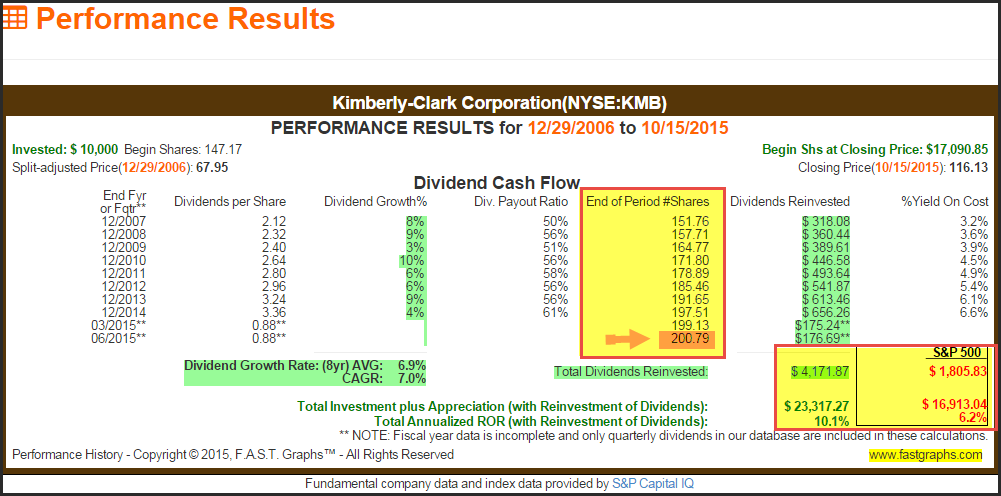

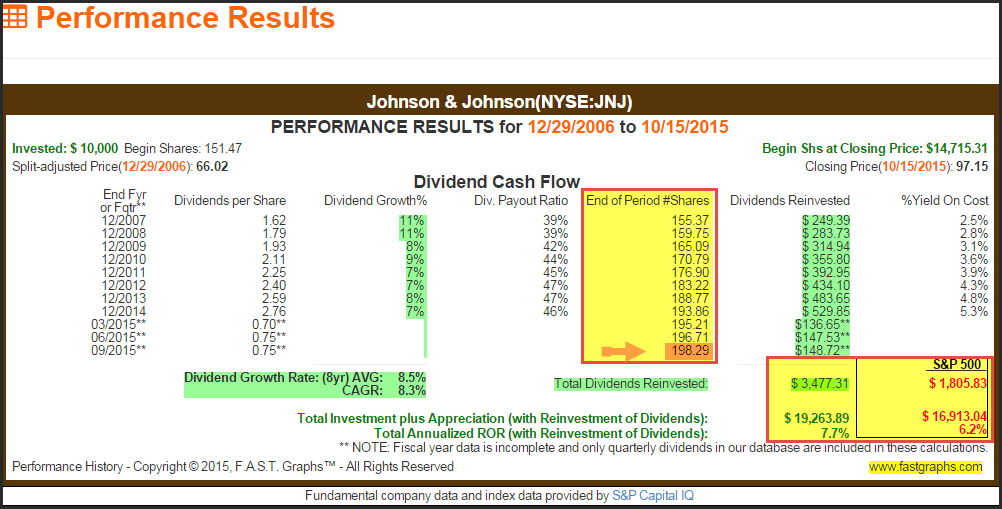

The following historical performance reports on both Kimberly-Clark and Johnson & Johnson clearly illustrate the similarities from a rate of return perspective of both companies. Although there is a slight total return advantage with Kimberly-Clark, it’s important to recognize that some of that has been achieved as a result of its current overvaluation. On the other hand, Kimberly-Clark has produced more cumulative total dividend income than Johnson & Johnson in spite of its overvaluation.

I have prepared the following short video (no link required) comparison between KMB and JNJ on live FAST Graphs to illustrate the benefit of collecting dividends and reinvesting the proceeds into fairly valued selections. The primary benefit of collect and invest, although it does take work and effort, is the idea that dividends will be reinvested into stocks only when they are attractively valued.

A Dividend Reinvestment Comparison

For the reader’s additional perspective, I offer a second set of performance results on both companies where dividends have been automatically reinvested at the end of each quarter. This would be analogous to a DRIP plan, and does illustrate the benefit of dividend reinvestment. In addition to the enhancements to both total cumulative income and total return, I suggest the reader focus on the column “End of Period # Shares.” For retired investors in the accumulation phase, the additional shares purchased will represent additional sources of dividend income in retirement years.

The Difference Between Dollar Cost Averaging And Averaging Down

There is one additional financial term that I would like to discuss that relates to the concepts of dividend reinvesting presented in this article. When discussing these concepts with individual investors, I have often found them confusing the terms dollar cost averaging with averaging down. These are not the same thing. Therefore, I thought it might be helpful to clarify the differences.

The concept of averaging down implies adding more shares to a holding at prices that are currently lower than your original cost basis. To me this concept makes the most sense when you originally invested in a quality stock at fair value that subsequently fell to a level where it was significantly undervalued.

The reason I add this concept to this discussion on reinvesting dividends, is because it is a strategy that I often found useful when managing my dividend growth portfolios, especially when my dividend growth portfolio is already fully invested. Furthermore, it also represents an additional advantage of the collect and invest strategy - flexibility.

Conceptually, the collecting of dividends provides the source of capital that I can utilize to take advantage of an extreme opportunity if and when it occurs. If I was automatically investing my dividends in a DRIP plan, I might not have that opportunity. However, the key to the attractiveness of this strategy is the notion that the stock I am averaging down was initially purchased at an attractive valuation.

DEFINITION of 'Average Down' courtesy of Investopedia:

The process of buying additional shares in a company at lower prices than you originally purchased. This brings the average price you've paid for all your shares down.

Summary and Conclusions

First and foremost, I consider myself a fan and advocate of both DRIP plans and the collect and invest strategy. Over the past 4 ½ decades, I have seen both dividend growth strategies produce excellent and successful results. Consequently, I don’t believe there is clear-cut evidence that suggests that one is better than the other. Both strategies possess advantages and disadvantages against the other. At the end of the day, it comes down to investor preferences and abilities.

DRIP plans provide discipline and take emotion and decision-making out of the equation. With this strategy, your dividend investment process is on autopilot so to speak. The collect and invest strategy in contrast requires the inclination and desire to analyze the stocks in your portfolio. In the long run, you may be able to generate better returns. However, it comes at the price of effort and attention.

Disclosure: Long KMB, JNJ at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.