83 Attractive Dividend Growth Stocks for Your Retirement Portfolios: Part 2A

Introduction

I recently completed a 3 part series of articles offered to assist retired investors in designing the equity portion of their retirement portfolios. In part 1 of this series I presented Peter Lynch’s 6 broad categories of stocks (businesses) that he wrote about in his best-selling book “One Up On Wall Street.” The primary objective of this first article was simply to provide the reader a general idea of the various categories of common stocks that were generally available to choose among. I presented one or two examples of each category in order to illustrate the advantages and/or disadvantages of each category. I also pointed out that not every category was appropriate for most conservative retired investors.

In part 2 I pointed out the importance of clearly defining whether your primary investment objective was for current income, future growth or a combination of both. I also touched on choosing the appropriate investment objective relative to whether you are already retired or whether you were in the accumulation phase and planning for future retirement. And I put forward that in order to successfully accomplish your goals, the most critical step was to clearly define them, because once that was done it is much easier to focus only on common stocks that possess the appropriate characteristics consistent with those goals.

In part 3 I discussed the advantages and disadvantages of a concentrated stock portfolio versus a more broadly diversified stock portfolio. In this article I presented the views of many renowned expert investors on the subject, as well as my own. I also discussed the advantages and disadvantages of building an equally-weighted stock portfolio versus overweighting certain sectors. And most importantly, I introduced what I considered the universal principle of starting with a plan that applies to all investors. And I added that it is not only imperative to have a plan, it’s even more vital to be disciplined about following it.

For the most part the above series of articles were primarily strategic in nature. I started out by presenting the various categories or types of stocks that investors could choose from. Then I discussed the importance of only choosing the most appropriate stocks to meet your own unique goals, objectives and risk tolerances. And finally, I presented various portfolio construction strategies that individuals could implement according to their own needs and risk tolerances.

Moving from the Strategic to the Specific

After completing the three-part series discussed above referencing available common stock options and strategies for designing the common stock portion of a retirement portfolio, it only seemed logical for me to move from the general to the specific. For the last few years, the overall stock market (S&P 500), and quality dividend growth stocks specifically had become extended based on valuation. However, during August and September of 2015 investors were given what I consider a pause that refreshes.

Although the stock market as represented by the S&P 500 has fallen approximately 6% since July 31, 2015, this would only be slightly more than half way to the definition of a market correction of 10% or more. However, since the beginning of the year (2015) many high-quality dividend growth stocks have, in fact, by definition experienced a bona fide correction. This includes many Dividend Champions and Contenders, which is important because they represent the best-of-breed dividend growth stocks for retirees to include in their portfolios for income.

Therefore, I felt it was appropriate to present an additional series of articles that readers could utilize in order to implement the strategies presented in the first series of articles with specific dividend growth stock examples and choices. In part 1 of this new series, I introduced two important principles that I believe are key to the successful implementation of a dividend growth portfolio in order to meet your specific and individual retirement yield objective or need.

Principle number 1 was to be realistic with your yield objective. The central idea behind this principle was to determine a range of yields available from quality, and most importantly, fairly valued dividend growth stocks of various categories. In other words, being clear about the yields available from quality empowers the investor to recognize that reaching for yields above those parameters is risky.

Principle number 2 was to determine how much income your portfolio needs to produce in order to meet your needs. Once this was determined, you could then mix-and-match your dividend growth stock choices appropriately. In other words, if your portfolio was large enough, you could focus on quality stocks with the highest yields and consistent records of dividend increases to meet your current needs. On the other hand, if you needed additional growth, you could focus on quality stocks that offered moderate yields but more growth.

83 Quality Dividend Growth Research Candidates Broken Down Into 4 Categories

I have screened the universe of quality dividend growth stocks that are currently fairly valued and came up with 83 research candidates I was comfortable presenting. In order to meet various individual investor goals or needs, I have broken this list down into 4 categories. The universal focus that I applied when making selections in all 4 categories was reasonable quality and attractive valuation.

The first category is comprised of 24 quality dividend growth stocks with above-average current yields. At the time of this writing the current yields on this first group range from a low of 2.9% to a high of 3.7%. I consider this first group of selections as foundational research candidates that can be utilized as core holdings for the equity portion of most every retiree’s portfolio.

The second category is comprised of 16 quality higher-yielding dividend growth stocks. At the time of this writing the current yields on this second group range from a low of 3.7% to a high of 5.6%. This second category is offered for those retirees that require more yield than was generally available from group 1, but are still looking for quality and safety. Selections from this group can be strategically utilized to increase the overall yield of the retirement portfolio.

The third category is comprised of 30 dividend growth stocks with lower yields but higher expected levels of capital appreciation and dividend growth (growth yield). At the time of this writing the current yields on this third group range from a low of 1.1% to a high of 2.9%. This third category is offered for those retirees or pre-retirees that require additional growth of both capital and dividend income. Selections from this group can be strategically utilized to generate a higher future total return and generate higher future dividend income when it is needed.

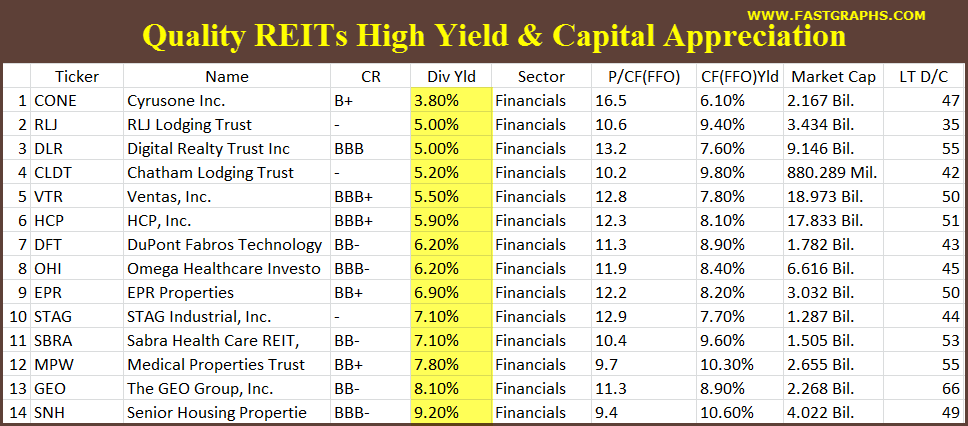

The fourth category is comprised of 14 high-quality fairly-valued and higher-yielding REITs. At the time of this writing the current yields on this fourth group range from a low of 3.8% to a high of 9.2%. This fourth category is offered for those retirees looking to increase both the current yield on their retirement portfolios and for the potential for capital appreciation. Selections from this group can be strategically utilized to generate a higher current yield and the opportunity for capital appreciation and income growth.

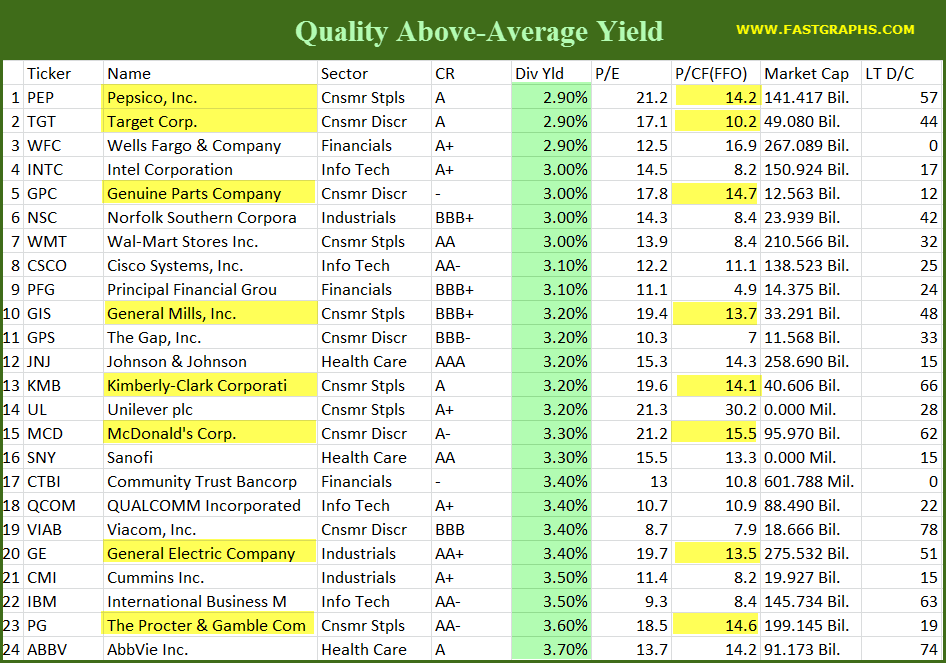

24 Fairly-Valued High-Quality Dividend Growth Stocks with Above-Average Yield

The following 24 research candidates with above-average current yields are listed in order of lowest to highest current dividend yield. The table presents the company’s ticker, name, sector, S&P credit rating dividend yield, current blended P/E ratio, current blended price to cash flow ratio (P/CF), market cap and long-term debt-to-capital ratio.

Note: some of these research candidates were selected based on attractive P/E ratios while others were chosen based on attractive price-to-cash flow ratios. I have highlighted those candidates that I believe are best evaluated based on cash flow valuations supporting current dividends and future dividend growth. Following the table I will present one example historical earnings and price correlated F.A.S.T. Graphs™ and one example where I believe the historical earnings and cash flow correlation is more appropriate for valuing the business.

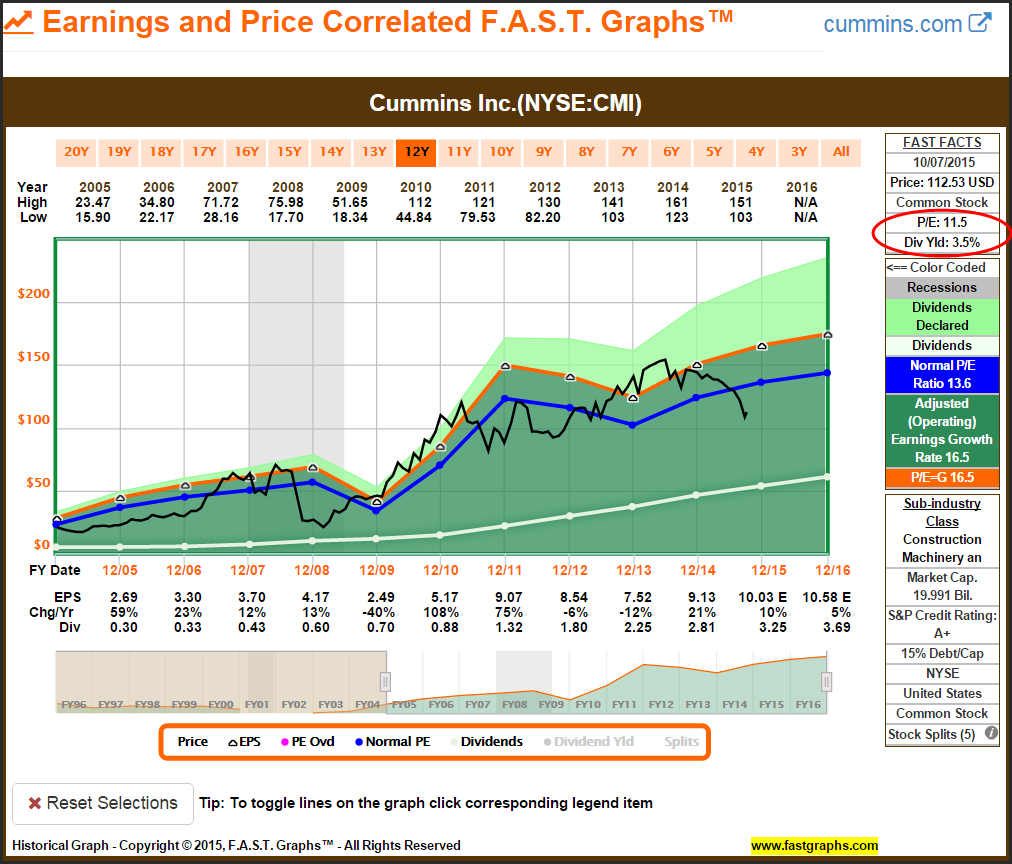

Cummins Inc. (CMI): Low P/E High-Yield

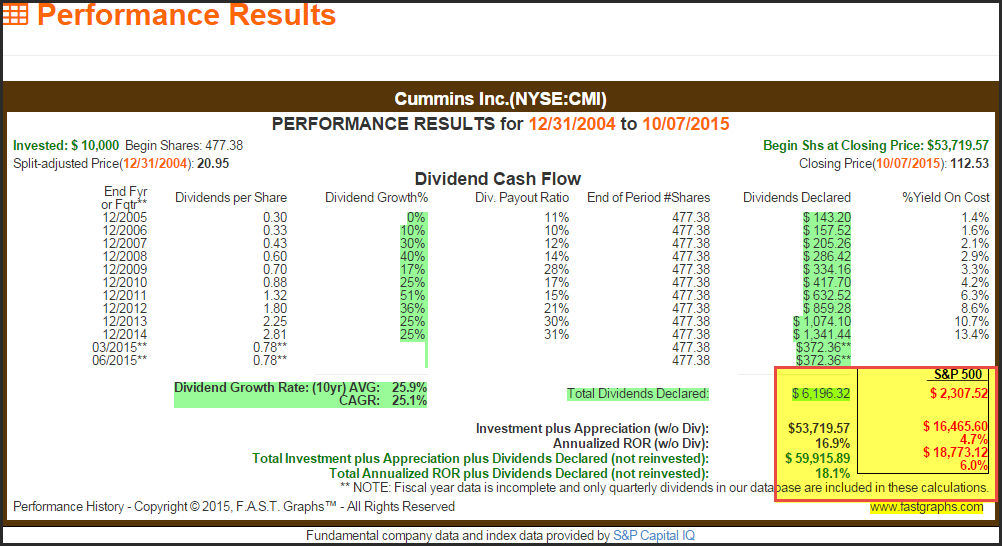

Cummins Inc. is a high-quality undervalued dividend growth stock with an A+ rating and a low debt-to-capital ratio of 15%. Since the beginning of 2015, the company’s stock price has fallen to a significantly low valuation level based on both earnings and its historical normal P/E ratio. This has resulted in the company currently providing an above-average dividend yield of 3.5%, coupled with the opportunity for significant capital appreciation when the company moves back to normal valuation levels. Although the company’s earnings history is moderately cyclical, its dividend growth record has been exemplary.

High current yield, and high dividend growth rate comes with historically low valuation makes Cummins a solid dividend growth opportunity for long-term oriented investors. Even at its current low valuation, Cummins has significantly outperformed the S&P 500 since 2005 on both cumulative dividend income and capital appreciation.

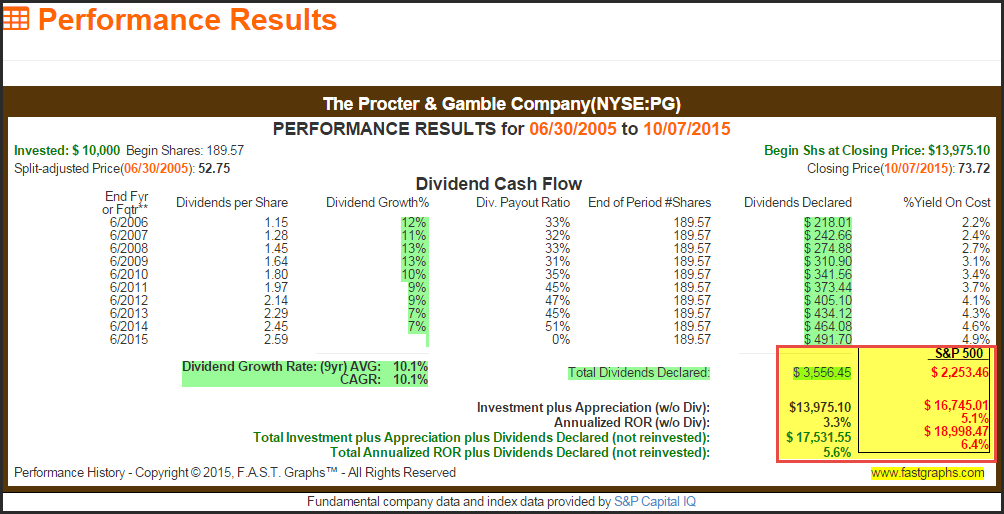

Procter & Gamble (PG): Low Price To Cash Flow Supports The Dividend

Procter & Gamble has a long history of trading at a premium P/E ratio. However, since I consider this primarily a high-quality high-yield investment, I believe it makes more sense to value it based on cash flow. On that basis, Procter & Gamble is soundly valued and offers a substantial 3.6% current yield potential for future dividend growth.

To me, investing in Procter & Gamble is all about high current yield and a high level of safety. Although the company has not outperformed the S&P 500 on a capital appreciation or a total return basis, it has outperformed the market based on total cumulative dividend income. These are the reasons why I consider Procter & Gamble a core holding.

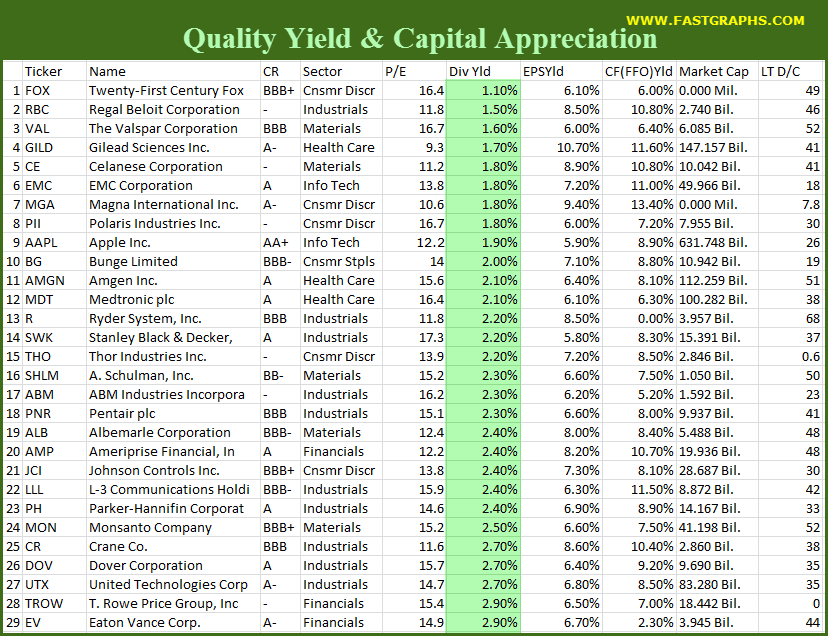

29 Fairly-Valued High-Quality Dividend Growth Stocks with Yield and Capital Appreciation Potential

29 Fairly-Valued High-Quality Dividend Growth Stocks with Yield and Capital Appreciation Potential

The research candidates presented in this group are offered for those retirees that need additional growth in their retirement portfolios to meet their future goals. The primary distinction between this group and the first group is greater capital appreciation and dividend growth potential. However, some of the higher-yielding candidates at the bottom of the list could overlap from group 2 to group 1 - and vice versa.

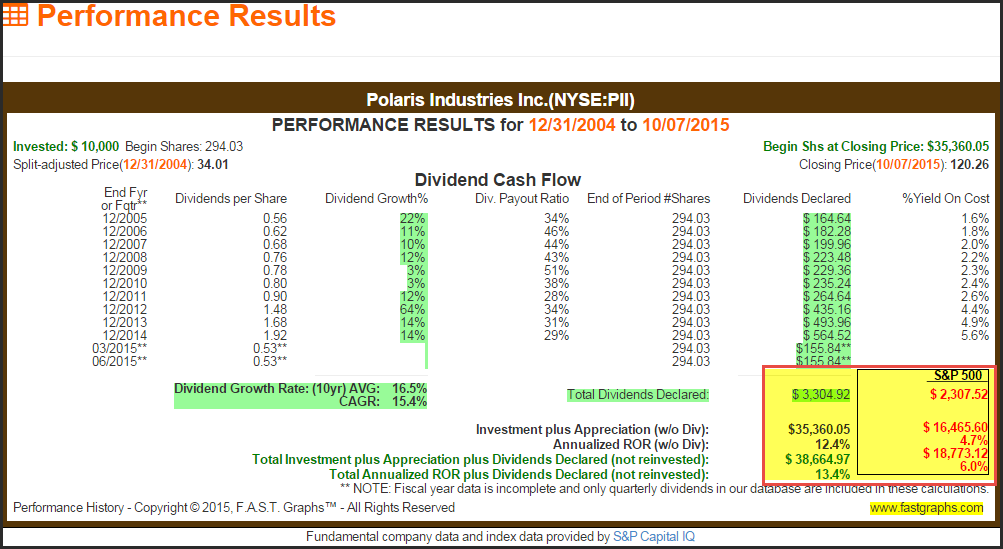

Polaris Industries Inc. (PII): A Growth Story Coming In To Fair Value

I believe that Polaris Industries’ recent weak performance was primarily due to significant overvaluation. Fundamentals have remained strong as both earnings and dividends have steadily increased at above-average rates. Although I would like to see this research candidate a little cheaper, I believe its growth potential represents an attractive long-term opportunity at current levels.

In spite of Polaris Industries’ recent price weakness, it has still outperformed the S&P 500 on both capital appreciation and cumulative dividend income since 2005. The potential for continued dividend growth and capital appreciation is above-average going forward as it has been in the past.

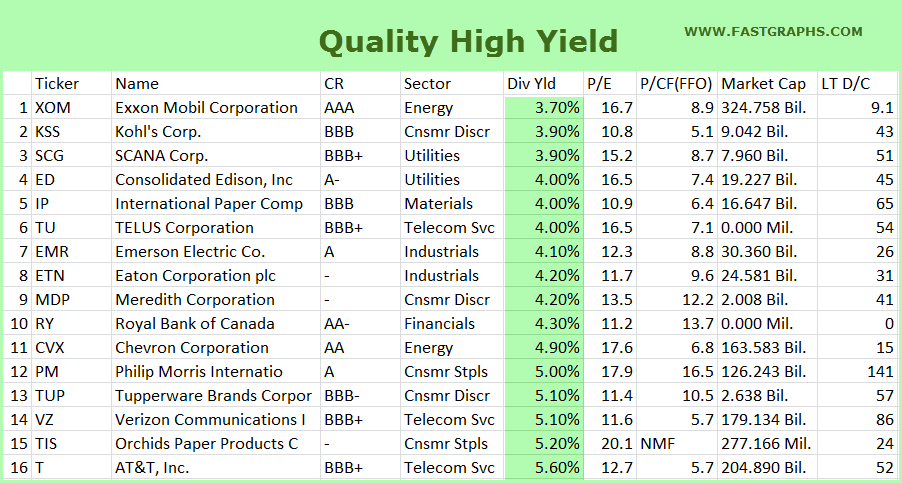

16 Fairly-Valued High-Quality High-Yield Dividend Growth Stocks

This third category of fairly-valued high-yield dividend growth stocks are offered for the consideration of those investors that need to get more current yield in their portfolios. However, as a general statement, the majority of these research candidates will not produce above-average growth of capital or dividend income. On the other hand, there are a few on the list that do, primarily because they are either currently very undervalued, or have hopefully short-term operating issues.

The major integrated oil and gas producers Exxon and Chevron represent examples of companies with hopefully short-term issues. Nevertheless, even though these are both extremely high-quality companies, there are risks that should be considered.

Eaton Corporation plc (ETN): High Yield Low Valuation

Eaton Corporation represents an example of a high-yield dividend growth stock that has recently become significantly undervalued. Consequently, the high-yield in this example is above historical norms as a result. Therefore, I think this example offers the opportunity for significant short and long-term capital appreciation - assuming the company moves back to a more normal valuation.

Although the company’s current low valuation has caused it to modestly underperform the market on a capital appreciation basis, the total return versus the S&P 500 has been very similar. The primary advantage however has been a significantly greater level of total cumulative dividend income than the market. Given today’s low valuation relative to the overall market and above-market current yield, that situation is very likely to reverse itself in the future.

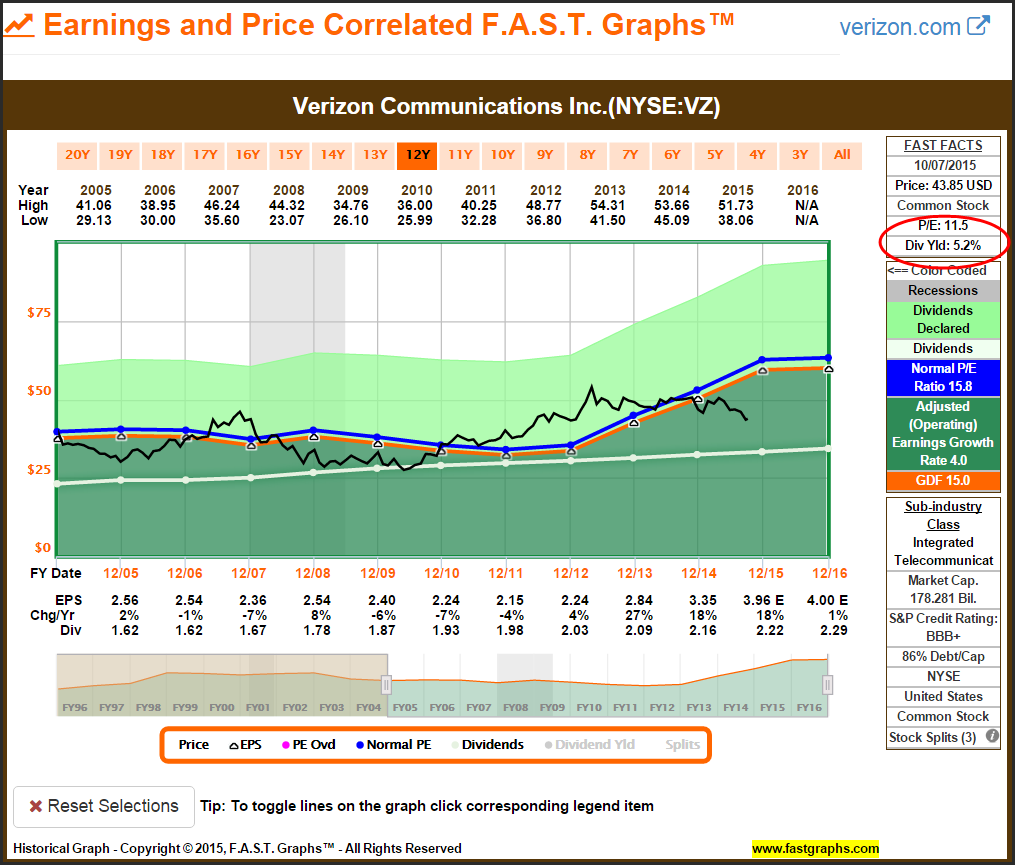

Verizon Communications Inc. (VZ): High Current Yield Low Valuation

I believe the major telecommunications companies AT&T and Verizon represent solid high-yield investments for retirees in need of maximum current income. Although neither of these companies provide opportunities for high capital appreciation, I believe both of their dividends are well protected by strong cash flow generation.

Both AT&T and Verizon get their appeal based on their high dividend yields. Although Verizon has protected principle since the beginning of 2005, capital appreciation has been minimal. On the other hand, total cumulative dividend income has been more than double what could have been earned in the S&P 500, or from the average bond over the same timeframe.

14 Fairly-Valued Reits For High Yield And Capital Appreciation

Although I am not a proponent of chasing yields, I believe that fairly-valued REITs are one place that retired investors can safely reach for higher yields and potential capital appreciation. Consequently, I believe that selectively integrating REITs into a retirement portfolio can provide significant benefits not available from typical corporations. REITs by law are required to pay out at least 90% of their taxable income to shareholders in the form of dividends. Additionally, many best-of-breed REITs provide opportunities for capital appreciation in addition to their high yield. Therefore, I think it makes a great deal of sense to sprinkle a few REITs into retirement portfolios for the higher-yielding growth potential they offer.

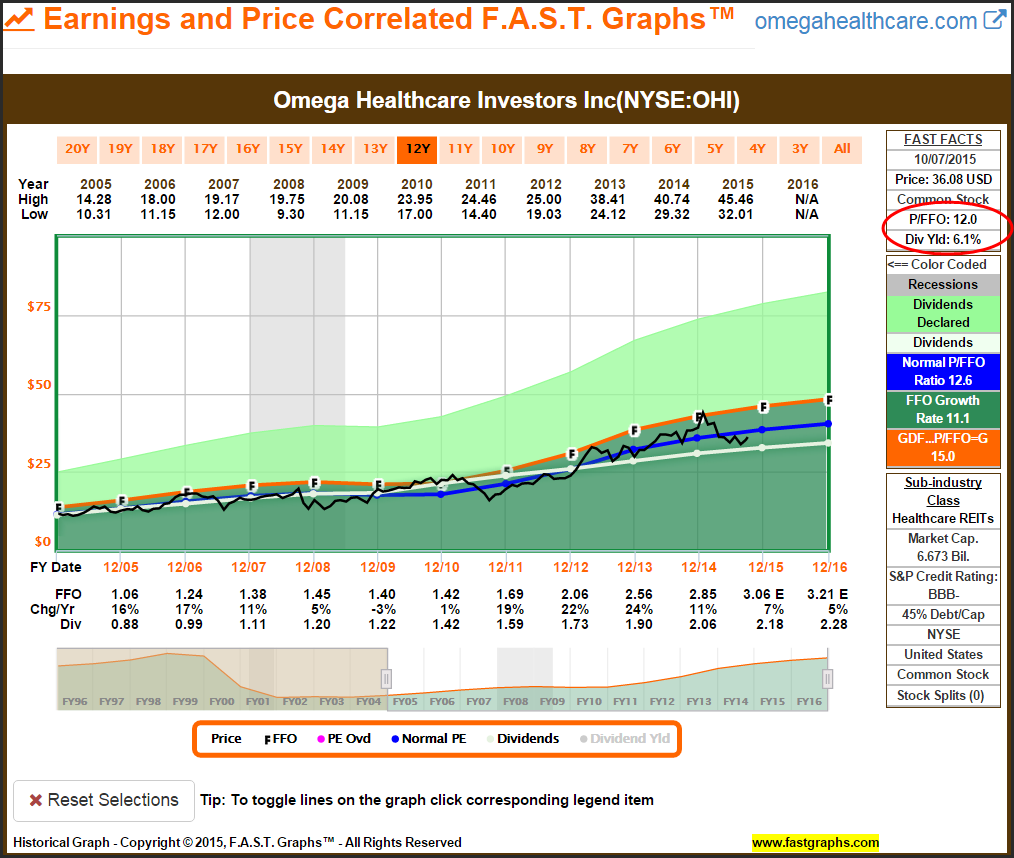

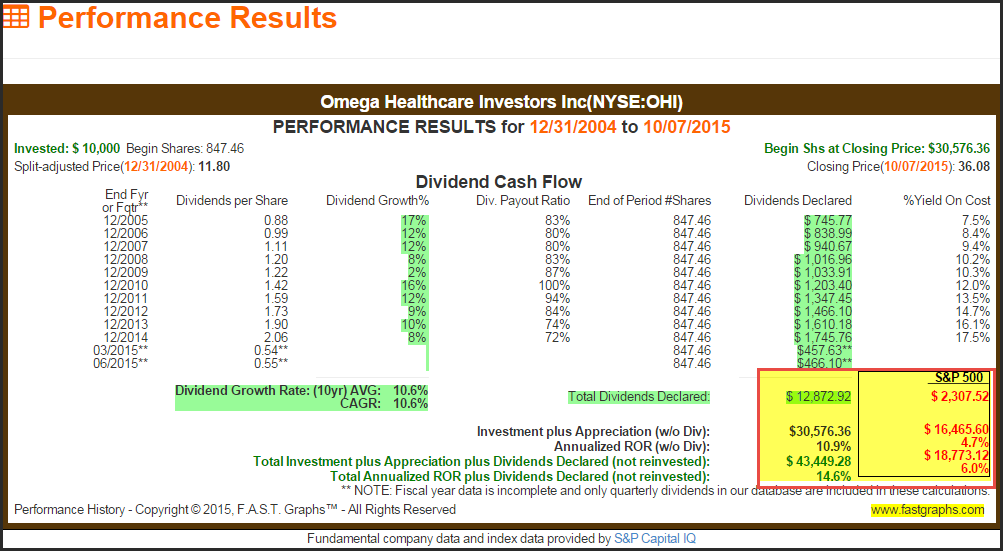

Omega Healthcare Investors Inc. (OHI): High Yield and Above-Average Capital Appreciation

Fairly valued Omega Healthcare offers a strong current yield of 6.1% and I consider it attractively valued. Moreover, as a major player in long-term health care facilities, I believe the company has a well-defined and bright long-term future. Given its current valuation, high current yield and potential for growth, I consider it an excellent option for retirees.

Since 2005 Omega has dramatically outperformed the S&P 500 on all accounts. Both capital appreciation and cumulative dividend income have dramatically outperformed the average company as represented by the S&P 500.

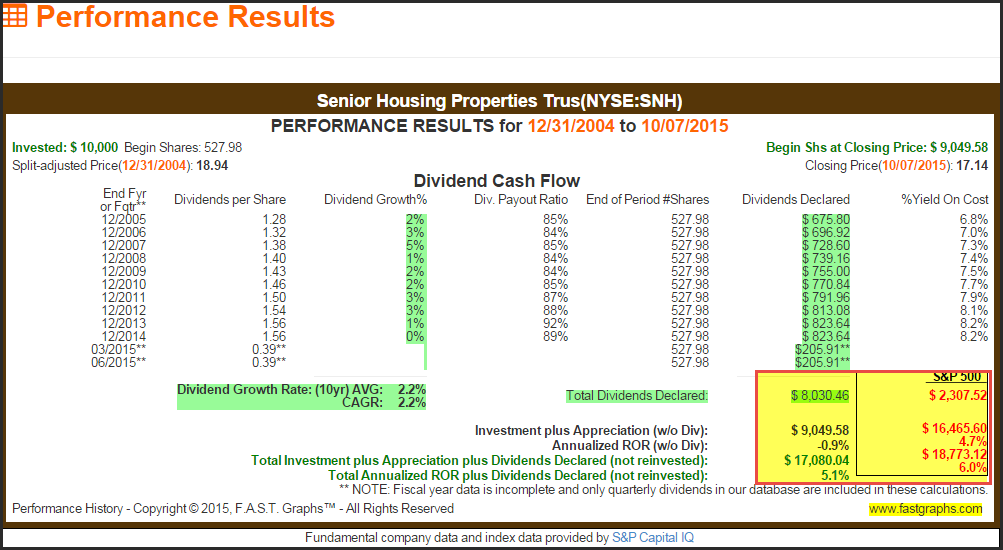

Senior Housing Properties Trust (SNH): Very High Yield Low Growth

Senior Housing Properties is the highest yielding but also one of the slowest growing REITs on my list. Nevertheless, I featured it for two reasons. First of all, I wanted to illustrate that not all REITs are the same, just as not all stocks are the same. My second reason was to provide a viable option for those retirees in need of high current yield. As previously mentioned, I am not a proponent of chasing yield. However, there are exceptions to every rule.

A quick examination of Senior Housing Properties clearly illustrates how it is different than many other REITs such as Omega Healthcare. Senior Housing Properties is clearly a yield investment. Consequently, I consider it only suitable for retired investors in need of maximum current income.

A Summary of Strategies and Approaches for Utilizing the Above Dividend Growth Stocks

In part 1 of this series I presented the ideas that retired investors should be realistic about the yields that are available in the marketplace. By realistic, I am referring to appropriate yields that are available from reasonable quality stocks trading at or near fair value. And then I suggested that retirees use that information to build portfolios that would meet their specific income needs and/or growth objectives.

In this part 2, I offered 4 primary categories of high-quality fairly-valued dividend growth stocks with varying attributes of yield or growth. With these various groupings of dividend growth stocks, retirees could pick and choose or mix-and-match from in order to meet their specific growth or income targets. There are virtually an infinite number of ways that this can be accomplished.

However, there are some general common sense approaches and methods that retirees can utilize and implement. The most appropriate approach is the one that is most likely capable of meeting each individual’s unique needs. Next I will list a few strategies that illustrate my point.

For the retired investor’s portfolio that is large enough to meet their living needs based on the realistic yields currently available, they might restrict their selections to the categories offering the highest current yields and maximum levels of safety. As stated in part 1, the key is to determine how much yield you need and then make your selections accordingly. For example, if a 3% current yield meet your objectives, you could limit your selections to only those companies that provided current yields of 3% or better.

In contrast, for the retiree in need of a yield higher than 3%, they could build a core portfolio including a large percentage of quality above-average yield companies with yields of 3% or better. Then they can blend in some of the higher-yielding companies in order to generate an overall portfolio yield greater than 3%. As a general rule, the more higher-yielding candidates you include, the lower your long-term capital appreciation potential might be. There is generally a trade-off between yield and growth. However, there are exceptions, as illustrated by some of the sample research candidates I featured in the article.

On the other hand, a retiree still in the accumulation phase might lean more heavily on companies from the quality yield and capital appreciation group. Since most of these companies have histories of growing their dividends and generating above-average capital appreciation, they might support that objective better than some of the higher-yielding groupings.

In summary, what I’m suggesting is mixing and matching research candidates from each of the groups that are appropriate for your current and/or future needs and objectives. But always keep in the back of your mind that higher yield typically comes at the cost of lower future growth, and vice versa.

Summary and Conclusions

The primary objective of this article was to provide specific examples of current attractively-valued dividend growth stock opportunities that could be utilized to construct appropriate equity portions of a retirement portfolio. My secondary objective was to illustrate the differences in current and future yields that are realistically available from high-quality dividend growth stocks in today’s market.

In my opinion, the best way to design a retirement portfolio that’s appropriate for you is by clearly understanding what is realistically available and then applying that knowledge towards constructing a successful long-term portfolio that’s just right for you. It comes down to knowing your options and then sensibly applying the correct mix to accomplish your goals.

In this part 2A I purposely refrained from discussing or presenting extremely high-yielding common stock categories. As I alluded to more than once, I am not personally a fan of reaching for yield, especially by investors in retirement. However, there are in fact many extremely high-yielding stocks that are available. In part 2B I will present several examples of extremely high-yielding companies such as BDCs, MLPs and mortgage REITs.

There are numerous companies in these categories that offer what at first glance appear to be irresistible and enticing double-digit current yields. Some of them have yields that are so high that they appear too good to be true. My objective in part 2B will be to illustrate the risks and dangers of investing in extremely high-yield securities. However, to be fair, I will also point out some of the advantages that these types of securities also offer.

Disclosure: Long CMI,PG,ETN,VZ,OHI.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.